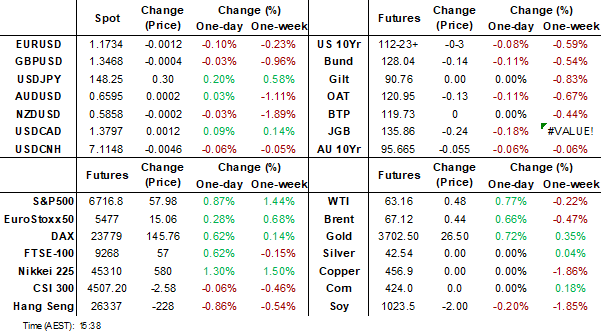

MNI EUROPEAN MARKETS ANALYSIS:Leverage Funds Add To JPY Shorts

- The USD BBDXY index has probed above 1200 today, continuing to recover from recent lows. US Tsy yields have drifted a little higher.

- USD/JPY is above 148.00. Last week's CFTC update showed leveraged funds adding to JPY shorts. JGB futures have been weighed though, as the various LDP leadership candidates outline potential policies.

- RBA Governor Bullock appeared before parliament and stated since the Aug policy meeting data outcomes have been close to expectations or slightly better. The central bank meets next week. As expected, China loan prime rates were held steady today. South Korean first 20-days trade data was mixed, a better headline, but seasonal impacts weighed on export growth.

- Central bank speak features post the Asia close today.

MARKETS

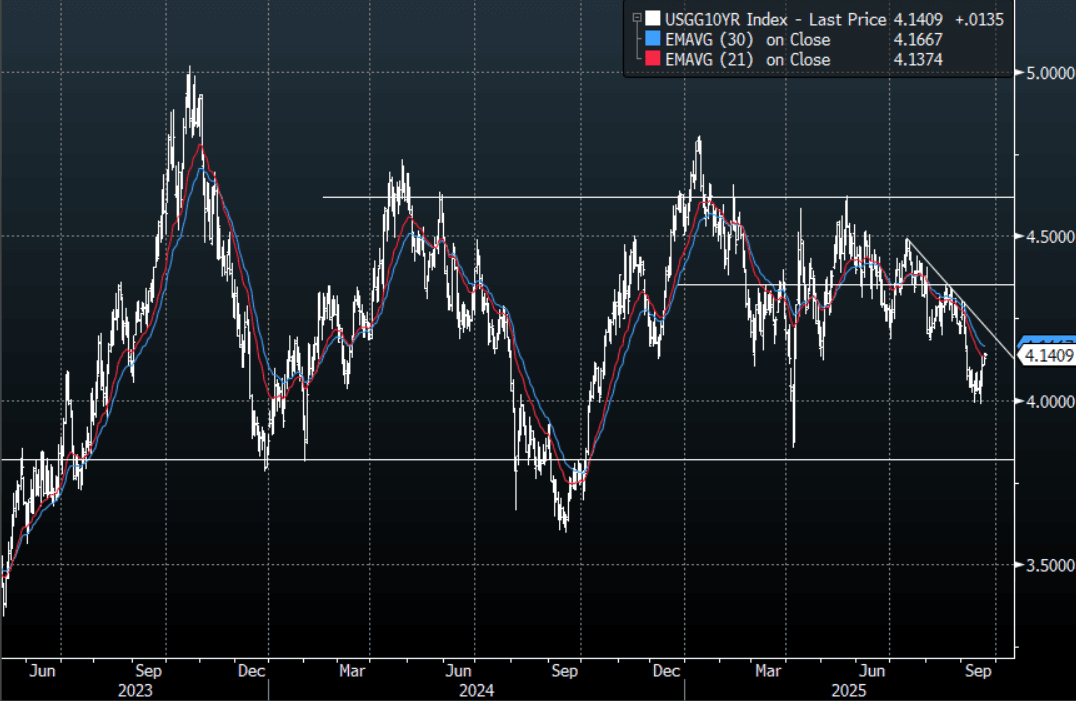

US TSYS: Asia Wrap - Yields Continue To Retrace Higher

The TYZ5 range has been 112-22 to 112-27+ during the Asia-Pacific session. It last changed hands at 112-23, down 0-01 from the previous close.

- The US 2-year yield has edged higher trading 3.578%, up 0.01 from its close.

- The US 10-year yield is trading around 4.141%, up 0.01 from its close.

- 10-Year Yields could not extend below 4.00% and have bounced as the Fed could not meet the markets very dovish expectations. The first buy-zone is now back towards the 4.20% area where I suspect demand should return initially. A sustained break through 4.00% is needed for the focus to then turn towards the 3.80% area.

- Robin Brooks on X: “Germany's real 10-year yield crossed above 1% this month, the first time it's been here since 2011. This is a destabilizing force for the Euro zone, because it pushes up yields everywhere else, including for highly indebted countries. It's already impacting Spain and France...”

- ISABELNET on X: “LEI - A 0.5% decline in the US Leading Economic Index (LEI) in August 2025 indicates an ongoing slowdown in US economic activity.”

- (Bloomberg) -- Asset-manager net long position in long-bond futures was unwound at a rapid pace in the week to Sept. 16., CFTC data shows. Other bigger positioning shifts saw hedge funds cover shorts in 5-year note futures while asset managers extended net long in ultra-long bond futures.

- Data/Events: Chicago Fed Nat Activity Index

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Market Sells Off As LDP Deliver Speeches

JGB futures are weaker and at session lows, -30 compared to the settlement levels.

- Japan’s LDP leadership candidates delivered policy speeches in Tokyo, with lawmaker Toshimitsu Motegi pledging to uphold a policy of no tax increases. Kobayashi announced plans to enhance screening for foreign inward investment. A recent poll shows Takaichi as the top pick to lead the LDP with 28.3% support. Chief Cabinet Secretary Hayashi noted that Japan’s past aversion to a strong yen has diminished but warned that potential Fed rate cuts could strengthen the yen and hurt the export-reliant economy.

- The BOJ kept rates at 0.5%, but two members dissented in favour of a 25bp hike, arguing the price target is "more or less achieved" and rates should move "closer to neutral," highlighting stronger hawkish voices within the board. See the full MNI BoJ Review here:

- Cash US tsys are 1-2bps cheaper in today's Asia-Pac session after Friday's modest sell-off.

- Cash JGBs are 1-5bps cheaper across benchmarks, led by the futures-linked 7-year. The benchmark 10-year yield is 2.3bp higher at 1.667%, a new cycle high.

- Swap rates are 2-4bps higher. Swap spreads are mostly wider.

- Tomorrow, the local calendar will be closed for a holiday.

BOJ: MNI BoJ Review – September 2025: Cautious But Signals Progress

Executive Summary

- Policy Decision & Dissents: The BOJ kept rates at 0.5%, but two members dissented in favour of a 25bp hike, arguing the price target is “more or less achieved” and rates should move “closer to neutral,” highlighting stronger hawkish voices within the board.

- Governor Ueda’s Tone: Ueda remained balanced, noting “underlying inflation is approaching 2%, but the 2% level has not yet been reached” and that there is “little sign of tariff having impact on Japan’s economy,” while emphasising ongoing global uncertainty and data dependency.

- Inflation & Growth Outlook: Core inflation remains above 3% with wage growth expected to keep inflation “floating above 2%.” Risks from tariffs are seen as contained, and potential supports include “Fed rate cuts,” “AI-related investment,” and “deregulation.”

- Rate Hike Timing & Risks: Views diverge—some expect a hike in October following the Tankan Survey and LDP leadership election, while others see January 2026 as the base case. Political risks (e.g., dovish LDP candidates) and Fed-driven yen appreciation could delay tightening.

- Asset Sales: The BOJ will gradually sell ¥330bn of ETFs and ¥5bn of J-REITs annually, a pace that would take “more than 100 years” to unwind holdings. The Bank aims to “avoid losses as much as possible” and limit market disruption, though acceleration remains possible.

- See full MNI BoJ Review here

AUSSIE BONDS: Grinding Weaker Through The Session

ACGBs (YM -4.0 & XM -5.0) are weaker and at cheaps.

- In today's testimony to the House of Representatives Standing Committee on Economics, RBA Governor Bullock stated that the RBA expects recent interest rate cuts to support household and business spending. Labour market conditions are near full employment, though unemployment has risen slightly since the last meeting, with some tightness remaining. Household consumption growth is expected to continue as real incomes rise. Since the August meeting, domestic data have been broadly in line with or slightly stronger than expectations. The overall economic outlook remains clouded by uncertainty.

- Cash US tsys are 1-2bps cheaper in today's Asia-Pac session after Friday's modest sell-off.

- Cash ACGBs are 3-4bps cheaper with the AU-US 10-year yield differential at +14bps.

- The bills strip is -3 to -4 across contracts.

- RBA-dated OIS pricing is giving a 25bp rate cut in September a 5% probability, with a cumulative 27bps of easing priced by year-end.

- August CPI data is due on Wednesday.

- This week, the AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond on Tuesday, A$1000mn of the 3.00% 21 November 2033 bond on Wednesday and A$900mn of the 2.75% 21 November 2029 bond on Friday.

- Tomorrow, the local calendar will see S&P Global PMIs.

RBA: Data Since Aug Meeting In Line Or Stronger Than Expected

RBA Governor's Bullock testimony before parliament earlier today covered a lot of ground, but didn't much light on the broader monetary policy outlook. Most notably since the August meeting, domestic data have been broadly in line with or slightly stronger than expectations. Still, the overall economic outlook remains clouded by uncertainty. This suggests little risks of a policy shift at next week's RBA meeting, although market pricing remains close to flat.

- In today's testimony to the House of Representatives Standing Committee on Economics, RBA Governor Bullock stated that the RBA expects recent interest rate cuts to support household and business spending. Household consumption growth is expected to continue as real incomes rise.

- The RBA noted not to read too much into the recent jobs data (which was weaker than market forecasts). Labour market conditions are near full employment, though unemployment has risen slightly since the last meeting, with some tightness remaining.

- The RBA also welcomed the new monthly CPI, which will print in Nov (for the Oct reference period), but it will still rely on the quarterly inflation update, particularly as the monthly CPI takes time to bed down from analytical stand point.

BONDS: NZGBS: Bear-Steepener To Start The Week

NZGBs closed showing a bear-steepener, with benchmark yields flat to 3bps higher.

- Cash US tsys are 1-2bps cheaper in today's Asia-Pac session after Friday's modest sell-off.

- Swap rates closed 1-2bps higher.

- Bloomberg - "Kiwibank Now Sees RBNZ Cash Rate Ending Year at 2.25%. Now expect a 50 basis-point cut in October followed by a 25bp cut in November so that the cash rate ends the year at 2.25%. "It has become crystal clear that the Kiwi economy is not recovering" and "the Reserve Bank needs to do more."

- RBNZ dated OIS pricing closed little changed across meetings. 33bps of easing is priced for October, with a cumulative 59bps by November 2025.

- The local calendar will be empty until Friday's Consumer Confidence data.

- On Thursday, the NZ Treasury plans to sell NZ$250mn of the 4.50% May-30 bond and NZ$200mn of the 3.50% Apr-33 bond.

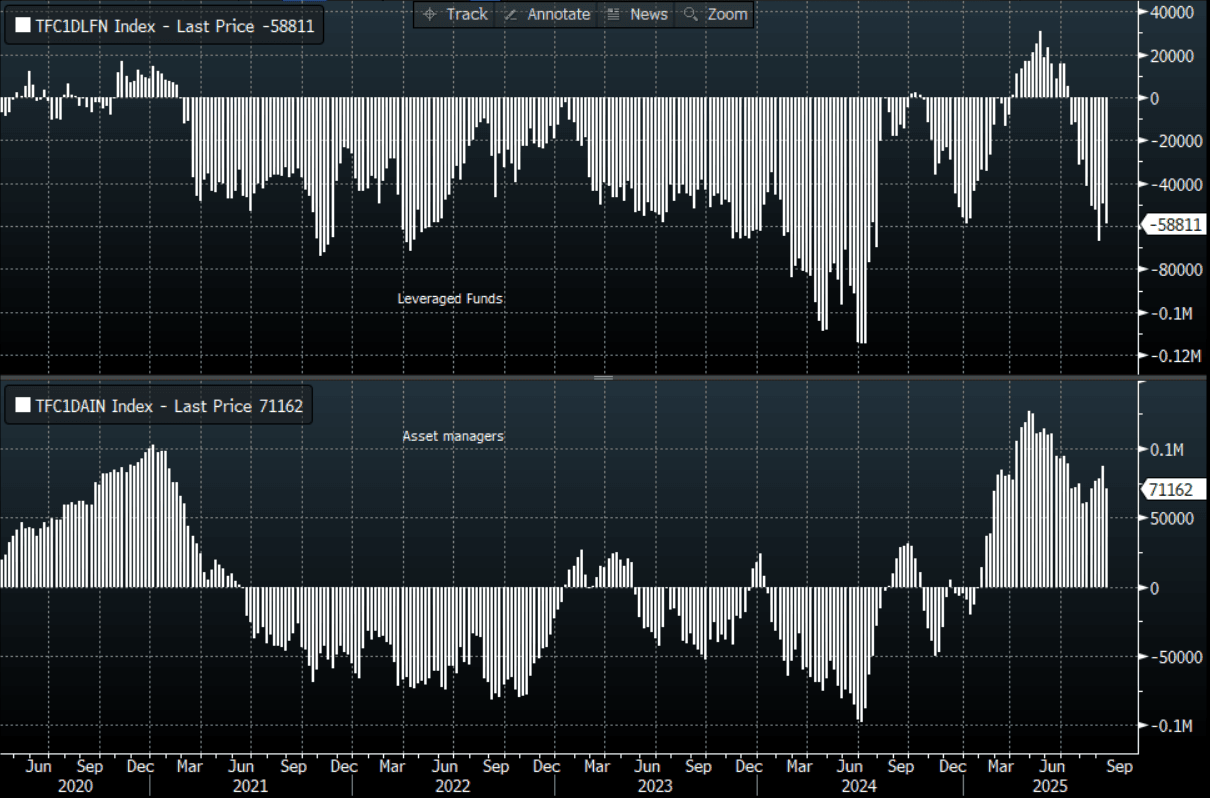

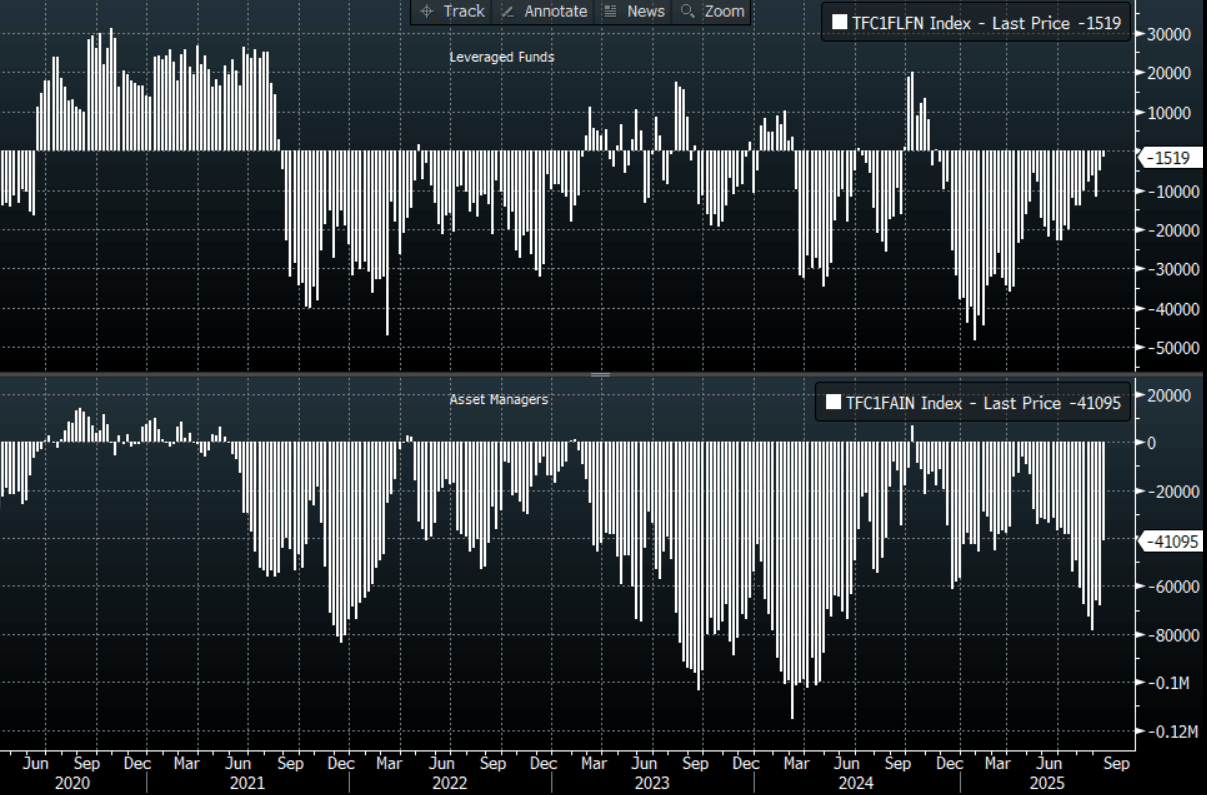

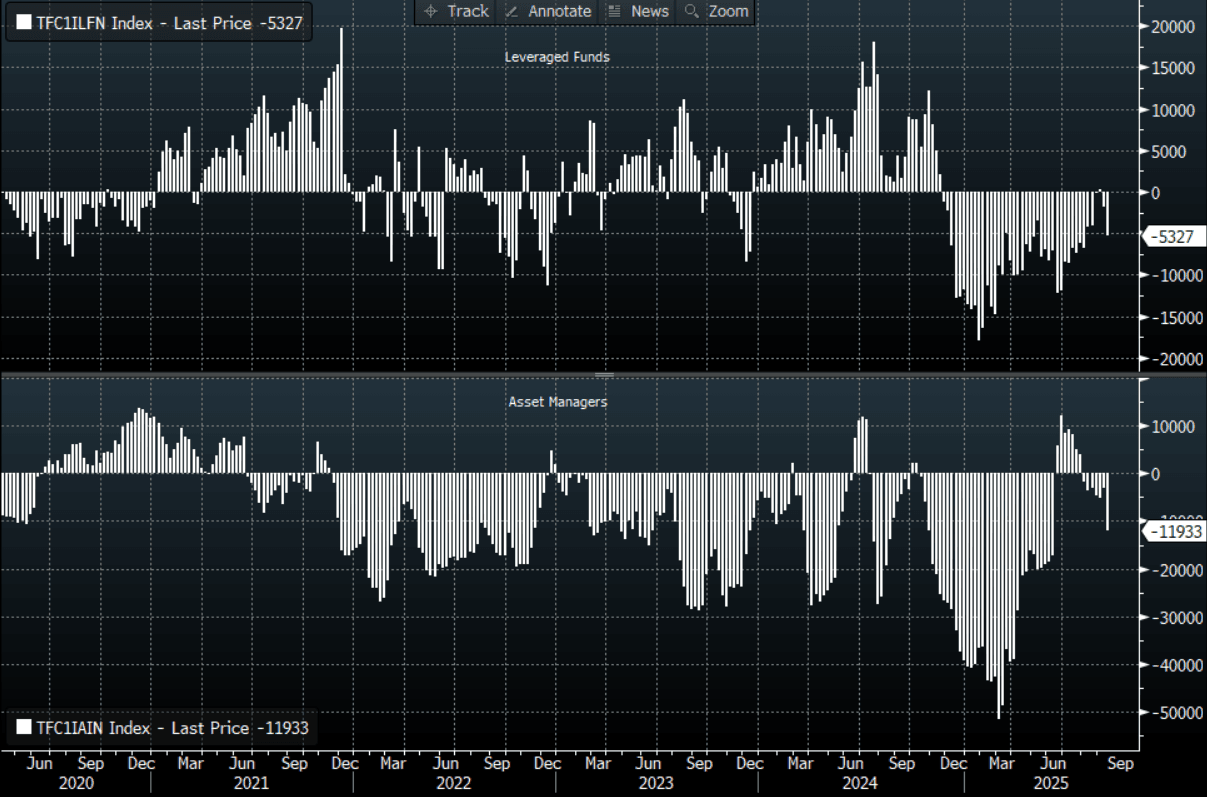

FOREX: JPY Sold, AUD & GBP Bought Per CFTC

Yen selling was a notable standout in last week's CFTC positioning update. Leveraged players added to existing shorts, while asset managers cut back on yen longs (see the table below). This is up to Tuesday last week (Sep 16th). USD/JPY price action saw a sharp move lower last Wednesday sub 146.00, but we quickly recovered and track near 148.00 in latest dealings. Friday's BoJ outcome was as expected in terms of rates on hold, albeit with some hawkish dissent. The tightening bias remains, although uncertainty prevails on timing.

- AUD/USD shorts being cut back by asset managers was the other notable feature from last week's CFTC update. The +27k in net buying saw shorts cut back to -41k. A renewed focus point is around hedging by local pension funds of offshore assets. There has been some sell-side focus on this being a AUD support point, while the RBA's Hauser also noted that rising FX hedging is also a longer term risk for such flows.

- Elsewhere, we saw GBP in demand, with leveraged players added to longs, while asset managers cut back on GBP shorts by 25k.

- For NZD, leveraged and asset manager players were net sellers of NZD. Interestingly this came ahead of Thursday's Q2 GDP disappointment last week.

- CFTC positioning shifts are showing a clear bias in favor of AUD over NZD at this stage. The AUD/NZD cross has broken higher, last near 1.1255.

Table 1: CFTC Positioning Change & Outright Position By Major Currency

| Leveraged Contracts | Asset manager Contracts | |||

| Weekly Change | Outright Position | Weekly Change | Outright Position | |

| JPY | -9220 | -58811 | -16077 | 71162 |

| EUR | -642 | 8195 | 4428 | 413192 |

| GBP | 8781 | 29793 | 25717 | -44709 |

| AUD | 3562 | -1519 | 27238 | -41095 |

| NZD | -3453 | -5327 | -8812 | -11933 |

| CAD | -194 | -47864 | 6311 | -58722 |

| CHF | -1837 | -1789 | 6984 | -35323 |

| MXN | 7114 | 36111 | 2567 | 40238 |

Source: CFTC/Bloomberg Finance L.P./MNI

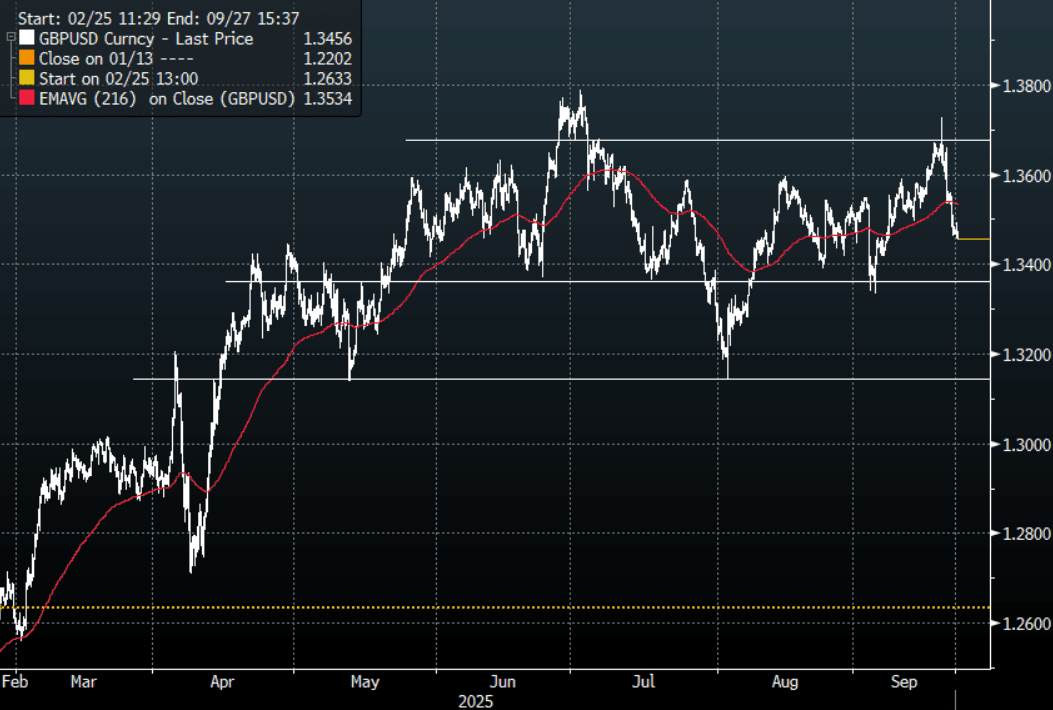

FOREX: Asia FX Wrap - USD Continues To Retrace, BBDXY Probes Above 1200

The BBDXY has had a range of 1198.77 - 1200.20 in the Asia-Pac session; it is currently trading around 1200, +0.15%. The USD continues to grind out gains as the market is being forced to recalibrate, having gone into last week's FOMC a little over its skis in terms of positioning. How far can this market retrace, I suspect sellers would be all over a bounce back toward the 1200/1210 area initially. A break below 1180 has been put off for now, but it feels like it's just a question of time before we have another look down there.

- EUR/USD - Asian range 1.1726 - 1.1748, Asia is currently trading 1.1730. The pair rejected the move above 1.1900 and quickly retraced. The market will be looking for dips back towards 1.1700 to find support to build a base from which to move higher again.

- GBP/USD - Asian range 1.3458 - 1.3474, Asia is currently dealing around 1.3455. The pair rejected the break higher and has moved back into the middle of its recent range. No clear direction for the moment.

- USD/CNH - Asian range 7.1134 - 7.1194, the USD/CNY fix printed 7.1106, Asia is currently dealing around 7.1150. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX -0.10%, Gold $3691, US 10-Year 4.142%, BBDXY 1200, Crude Oil $63.08

- Data/Events : EZ Consumer Confidence

Fig 1: GBP/USD Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: Asia Wrap - USD/JPY Probes Above 148.00, Leveraged Funds Add To JPY Shorts

The USD/JPY range has been 147.88 - 148.38 in the Asia-Pac session, it is currently trading around 148.35, +0.25%. USD/JPY is doing some work just above the 148.00 area. The price is still within its recent 146-149 range, and we need a convincing break on either side to see some clearer direction again. Neither the FOMC nor the BOJ were able to provide any clarity, the market will start turning its focus towards payrolls which seems a lifetime away.

- MNI BoJ Review – September 2025: Cautious But Signals Progress: Policy Decision & Dissents: The BOJ kept rates at 0.5%, but two members dissented in favour of a 25bp hike, arguing the price target is "more or less achieved" and rates should move "closer to neutral," highlighting stronger hawkish voices within the board.

- Governor Ueda's Tone: Ueda remained balanced, noting "underlying inflation is approaching 2%, but the 2% level has not yet been reached" and that there is "little sign of tariff having impact on Japan's economy," while emphasising ongoing global uncertainty and data dependency.

- "JAPAN'S TAKAICHI TOP PICK TO LEAD LDP RACE WITH 28.3%: FNN POLL" - BBG

- "JAPANESE PM CONTENDER AND CHIEF CABINET SECRETARY HAYASHI: JAPAN'S PAST AVERSION TO STRONG YEN HAS DIMINISHED, WHEN ASKED ABOUT RISK FED RATE CUT PROSPECTS COULD PUSH UP YEN VS DOLLAR, HURT JAPAN'S EXPORT-RELIANT ECONOMY.” - RTRS

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.85($430m), 147.25($897m), 146.80($502m). Upcoming Close Strikes : 145.00($1.52b Sept 24), 150.00($922m Sept 25) - BBG.

- CFTC data shows last week asset managers reduced their JPY longs slightly +71162( Last +87239), leveraged funds again used the dip to add their short position believing the support will continue to hold -58811(Last -49951).

Fig 1 : JPY CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia Wrap - AUD/USD Consolidates Around 0.6600, AM's Reduce Shorts

The AUD/USD has had a range of 0.6581 - 0.6604 in the Asia- Pac session, it is currently trading around 0.6595, +0.02%. US stocks initially tried lower on the H-1B visa story but have failed to follow through in our session. The USD retracement continues to grind higher, time will tell how long the reprieve lasts. The AUD/USD should still see dips supported for now with the first buy-zone back towards the 0.6550 area.

- MNI - In today's testimony to the House of Representatives Standing Committee on Economics, RBA Governor Bullock stated that the RBA expects recent interest rate cuts to support household and business spending. Labour market conditions are near full employment, though unemployment has risen slightly since the last meeting, with some tightness remaining. Household consumption growth is expected to continue as real incomes rise. Since the August meeting, domestic data have been broadly in line with or slightly stronger than expectations. The overall economic outlook remains clouded by uncertainty.

- "BULLOCK: RBA GETTING CLOSER TO MISSION ACCOMPLISHED ON CPI, RECENT CHINESE ECONOMIC DATA HAVE NOT BEEN SO GREAT - [RTRS]"

- "RBA'S HUNTER: LOOKS LIKE ECONOMY IS IN A `CYCLICAL UPTURN” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6510(AUD356m), 0.6525(AUD705m), 0.6600(AUD546m). Upcoming Close Strikes : 0.6600(AUD703m Sept 24), 0.6650(AUD908m Sept 23), 0.6720(AUD791m Sept 24) - BBG

- CFTC Data last week shows Asset managers started to significantly reduce their shorts, -41095(Last -68333). The Leveraged community has pulled back their shorts to be almost flat, -1519(Last -5081).

- AUD/JPY - Asia-Pac range 97.48 - 97.85, Asia is trading around 97.85.The pair has stalled towards 98.50, dips back towards 96.50/97.00 should be expected to be supported now first up.

Fig 1: AUD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

NZD: Asia Wrap-NZD/USD Trades Heavy Around 0.5850, CFTC Shows Shorts Being Built

The NZD/USD had a range of 0.5847 - 0.5868 in the Asia-Pac session, going into the London open trading around 0.5860, -0.05%. US stocks initially tried lower on the H-1B visa story but have failed to follow through in our session. The USD retracement continues to extend though time will tell how long the reprieve lasts. The NZD underperformance got a real nudge from the poor GDP data last week. While the USD continues to pullback the NZD/USD is a great vehicle to express that but when the USD sellers return the NZD underperformance will once again be best expressed in the crosses. The 0.5800 is important support, I suspect we will see buyers around this area initially. A sustained break through there would turn the focus back towards the 0.5500 lows.

- Bloomberg - “Kiwibank Now Sees RBNZ Cash Rate Ending Year at 2.25%. Now expect a 50 basis-point cut in October followed by a 25bp cut in November so that the cash rate ends the year at 2.25%. “It has become crystal clear that the Kiwi economy is not recovering” and “the Reserve Bank needs to do more.”

- MNI Brief: China Sept LPR Remains Unchanged. China’s LPR held steady on Monday, in line with expectations, with more easing expected later in the year as the economy suffers stronger headwinds, according to a statement on the website of the PBOC.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6020(NZD374m). Upcoming Close Strikes : 0.5900(NZD372m Sept24) - BBG

- CFTC Data of last week shows Asset Managers beginning to rebuild their short positions in the NZD, -11933(Last -3121). The Leveraged community is doing the same as it looks to rebuild its own shorts, -5327(Last -1874). Positioning shows the market is again turning bearish on the NZD.

- AUD/NZD range for the session has been 1.1240 - 1.1267, currently trading 1.1255. The Cross has broken above the multiple highs towards the 1.1200 area and is looking to accelerate higher on the back of some very poor NZ Q2 GDP data last week. Dips should now continue to be supported as the market turns its focus towards the 1.1400/1.1500 area.

Fig 1: NZD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

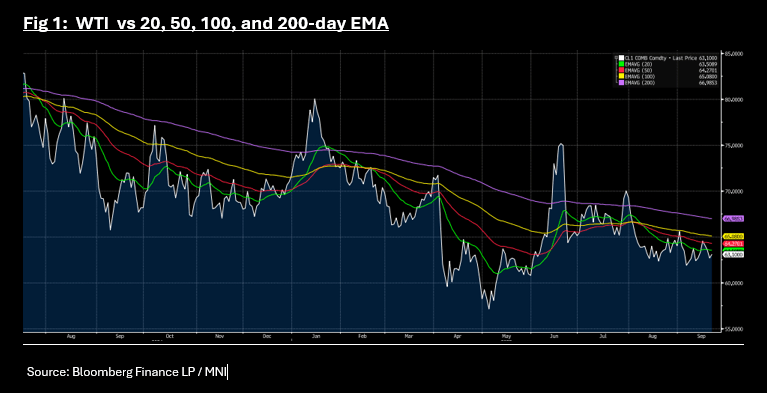

COMMODITIES: Oil and Gold Both Up in Monday Trade

- Oil rose Monday, after a very poor finish last week. WTI is up +0.64% to USD$63.08 bbl and Brent is up +0.66% to USD$67.12 bbl in the Asia trading day.

- Late Friday the EU President indicated the latest move is to target refineries, traders and petrochemical companies that are still buying Russian oil in a bid to starve Moscow and end the war in Ukraine. China and India remain the highest profile of buyers but the EU seems intent on casting the net much wider.

- This comes as French President Macro describes the EU's reliance on Russia now as 'marginal' as Trump continues to pressure Europe to eradicate Russian purchases.

- The EU has already passed a ban that will prohibit importing petroleum products refined from Russia crude starting next year, and the bloc is discussing banning imports of Russian liquefied natural gas from 2027.

- WTI remains firmly below all major moving averages today, despite the gains.

- Gold is reaching yet another new high as it rises +0.21% today to USD$3,693.00. The recent cut in interest rates gave a further boost to gold, already with strong upward momentum with traders now pouring over Chairman Powell's comments for clues as to the next move.

- At $3,693 gold is above all major moving averages with the 20-day of $3,588.90 below.

ASIA STOCKS: HSI Down on EV Decline

The Hang Seng was dragged lower today despite positivity elsewhere in the region by EV car makers. News over the weekend that Warren Buffet had sold down his shares in BYD sent the stock into reverse this morning and is down -3.5%. Japanese shares breathed a sigh of relief as news that the BOJ plans to sell down its equity ETF holdings were revealed, with an ultra long time horizon for the sale. In Korea, Samsung received a boost with its shares up strongly on news it received approval from Nvidia to used its advanced memory chips.

- The Hang Seng is down 1% in Monday trade as onshore bourses are up modestly. The CSI 300 is up +0.07%, Shanghai Comp +0.07% and Shenzhen Comp +0.14%.

- The NIKKEI is up +1.37% reaching a new high of 45,666.18.

- The KOSPI is up +0.55% to reach 3,464.27.

- The FTSE Malay KLCI is up just +0.12% in Monday's trade.

- The Jakarta Composite is one of the few fallers, down modestly by -0.12%.

- The NIFTY 50 is trading near to where it opened on Monday after finishing up last week.

ASIA STOCKS: Taiwan & South Korea Inflows Stall, Mixed Trends In SEA

At the end of last week, positive inflow momentum slowed into both South Korea and Taiwan. Taiwan's $500mn in net outflows was the largest daily outflow since Aug 22. As we noted through the second half of last week, inflow momentum for Taiwan had risen to the highest monthly levels and we have only just ticked past the half way point of September. Hence some consolidation was arguably not surprising. the 5-day sum of net inflows remains positive but is back under $1bn. At the end of last week, the SOX index fell in the US, but this had followed very strong gains on Thursday

- It is a similar backdrop for South Korea, although it only saw modest outflow pressures on Friday. The Kospi has started this week firmly, up 1% earlier, as Samsung rose following positive news on a chip qualification test with Nvidia.

- Elsewhere, we saw another large outflow day from Thailand on Friday (which followed Thursday outflows of a similar magnitude). The SET index is back down from cycle highs, closing last Friday under 1300.

- In contrast, Indonesia saw a decent inflow day on Friday. Sentiment has steadily improved following the replacement of the FinMin. The JCI closed above 8050 on Friday, close to fresh intra-day cycle highs.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | -70 | 1321 | -977 |

| Taiwan (USDmn) | -500 | 937 | 8342 |

| India (USDmn)* | 89 | 322 | -15203 |

| Indonesia (USDmn) | 172 | 183 | -3546 |

| Thailand (USDmn) | -100 | -159 | -2711 |

| Malaysia (USDmn) | 49 | 172 | -3635 |

| Philippines (USDmn) | 4 | 6 | -721 |

| Total (USDmn) | -356 | 2782 | -18451 |

| * Data Up To Sep 18 |

Source: Bloomberg Finance L.P/MNI

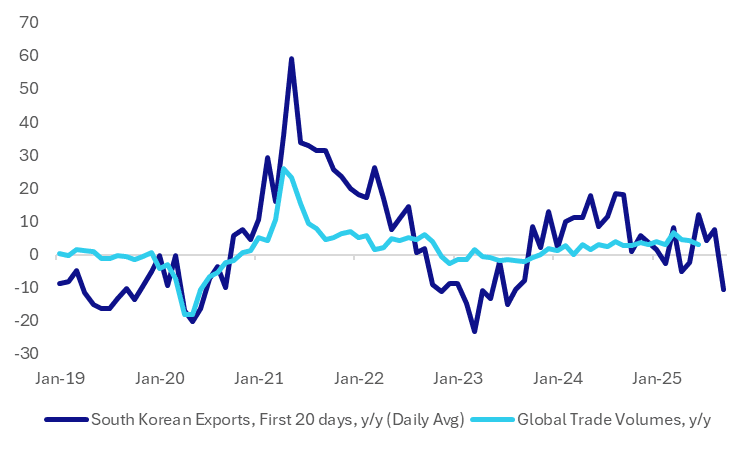

MACRO UPDATE: South Korea Exports Give Warning Sign For Global Trade

The earlier first 20-days of September trade data for South Korea flashed a warning sign for global trade growth (albeit with caveats on the data). The chart below plots the daily average of the first 20-days export growth in y/y terms against global trade volumes, also in y/y terms.

- The daily average which takes into account differences in working days between years, fell to -10.6%y/y in Sep, the weakest print since late 2023. The last time we were this soft global trade volumes was also in negative territory.

- Arguably the result may not surprise the market too much, given higher tariff levels are expected to weigh on trade growth as we progress towards the end of 2025.

- Also via BBG: "Monday’s trade data show a larger-than-usual gap between seasonally adjusted and unadjusted figures because of the shifting Chuseok holidays... The real question is how much momentum can be sustained after the Chuseok holidays.”

- The headline figure was much stronger at +13.5%y/y for the first 20-days of Sep.

- This will be a watch point for the local authorities, given President Lee is keenly focused on boosting growth. More broadly, given South Korea's key role in global supply chains, the data will be watched for signs of broader trends in the global trade outlook.

Fig 1: South Korea First 20-days Exports Y/Y (Daily Average) and Global Trade Volumes Y/Y

Source: Bloomberg Finance L.P./MNI

ASIA FX: USD/CNH Down Slightly, Briefing Later, USD/KRW Away From 1400

In North East Asia FX, the trend has mostly been for USD softness, although TWD has lost a little ground versus the USD. Aggregate FX moves have been fairly modest though in Monday trade to date.

- USD/CNH tracks near 7.1150, down slightly from end Friday levels. The USD/CNY fixing moved lower, but so too was the market estimate, with the fixing error little changed. The onshore equity backdrop is little changed. The Trump-Xi phone call appeared to keep relations on an improving trend (with the two leaders set to meet at the APEC forum later this year). Note a little later on (3pm local time), we will have a press conference featuring the key financial regulators, including the PBoC. Per BBG: "Monday’s briefing is framed as a review of the sector’s 2021–2025 “achievements,” whereas last year’s was focused on “financial support” for high-quality development, indicating today’s briefing could be more retrospective." So not much fresh policy impetus may come out of today's briefing.

- Spot USD/KRW is lower, last near 1393/94, up around 0.25% in won terms. Session lows rest at 1390.8. Onshore equities are higher, albeit away from best levels, last +0.50% for the Kospi. Positive news for Samsung (post Nvidia chip testing) has likely aided offshore equity inflows. Earlier data showed holiday distortions impacting the first 20-days of Sep export growth (headline was positive but daily average y/y was down -10.6%).

- USD/TWD got above 30.30 in the first part of trade, but we sit slightly weaker now, last around 30.26, still off around 0.16% in TWD terms.

- Spot USD/HKD is under 7.7700, fresh multi month lows, with higher Hibor rates offsetting the slightly firmer US yield backdrop in recent sessions. Month/quarter end may be aiding tighter liquidity trends.

CHINA: Country Wrap: LPRs Unchanged Today

Market Summary: The Hang Seng is down 1% in Monday trade as onshore bourses are up modestly. The CSI 300 is up +0.20%, Shanghai Comp +0.07% and Shenzhen Comp +0.12%. The Yuan Reference Rate at 7.1106 Per USD; Estimate 7.1157 as the 10-Yr CGB yield drops to 1.79%

- The total bond holdings by foreign institutional investors in China’s interbank market were 3.83t yuan by the end of August, according to data released by the People’s Bank of China’s Shanghai office. Their holdings account for about 2.3% of bonds under custody in the market. The investors held 2.01t yuan of China government bonds and 740b yuan of bonds issued by policy banks. (source PBOC)

- The People's Bank of China left the one-year loan prime rate unchanged at 3.0% and the five-year loan prime rate at 3.5%, according to a notice by the central bank released Monday. Analysts polled by Reuters expected no changes to the one-year and five-year LPRs. China's benchmark rates did not change despite the US Federal Reserve slashing its benchmark interest rate by 25 basis points. (source MNI)

SOUTH KOREA: Country Wrap: Industry Minister Focuses on Export Momentum

Market Summary: The KOSPI is up +0.55% to reach 3,464.27 as the Won is the best regional performer with gains of +0.25% to touch 1,393.40. Bonds are steady with the 10-Yr relatively unchanged from Friday at 2.83%

- The industry ministry said Monday it will do its "utmost" to maintain Korea's export momentum amid global trade uncertainties, noting the government will faithfully implement support measures for local companies affected by U.S. tariffs. (source Korea Times)

- Korea saw the steepest hike in tariffs imposed on its exports to the United States among major trading partners of the U.S. in the second quarter of 2025, data showed Sunday, following Washington's new trade policy. (source Korea Times)

INDONESIA: Country Wrap: New Scheme to Encourage FX Repatriation

Market Summary: The Jakarta Composite is one of the few fallers, down -0.35% today and IDR is weakening further to 16,603. Bonds are weak also with yields off 1-4bps. The 10-Yr is up +3bps at 6.33%

- Indonesia’s Communications and Digital Ministry (Komdigi) will maintain its 2026 budget ceiling at Rp8 trillion ($488 million), which will primarily fund ongoing digital infrastructure projects and basic operational costs, a senior official said on Friday. (source Antara)

- Indonesia is preparing a new market-based incentive scheme to encourage citizens to repatriate U.S. dollar savings held abroad, Finance Minister Purbaya said Friday, outlining one of his first major policy priorities since taking office. Speaking after meeting President Prabowo Subianto at the presidential palace in Jakarta, Purbaya said the program is expected to be rolled out within a month. He added that the measures will not be compulsory but will instead provide attractive incentives for Indonesians to keep their dollar funds domestically. (source Jakarta Globe)

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 22/09/2025 | 1230/0830 | * | Industrial Product and Raw Material Price Index | |

| 22/09/2025 | 1230/1330 | BOE Pill At BIS-ECB-SUERF Workshop | ||

| 22/09/2025 | 1345/1545 | ECB Lane At BIS-ECB-SUERF Workshop | ||

| 22/09/2025 | 1345/0945 | New York Fed's John Williams | ||

| 22/09/2025 | 1400/1600 | ** | Consumer Confidence Indicator (p) | |

| 22/09/2025 | 1400/1000 | St. Louis Fed's Alberto Musalem | ||

| 22/09/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 22/09/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 22/09/2025 | 1600/1200 | Cleveland Fed's Beth Hammack | ||

| 22/09/2025 | 1600/1200 | Richmond Fed's Tom Barkin | ||

| 22/09/2025 | 1715/1315 | BOC Sr Deputy speaks at LSE panel on supervision | ||

| 22/09/2025 | 1800/1900 | BOE Bailey Fireside Chat On Supervision | ||

| 22/09/2025 | 1945/1545 | BOC Deputy Kozicki speaks at BIS panel on central bank frameworks | ||

| 23/09/2025 | 2300/0900 | *** | Judo Bank Flash Australia PMI | |

| 23/09/2025 | - | Riksbank Meeting | ||

| 23/09/2025 | 0715/0915 | ** | S&P Global Services PMI (p) | |

| 23/09/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 23/09/2025 | 0730/0930 | *** | Riksbank Interest Rate Decison | |

| 23/09/2025 | 0730/0930 | ** | S&P Global Services PMI (p) | |

| 23/09/2025 | 0730/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 23/09/2025 | 0800/1000 | ** | S&P Global Services PMI (p) | |

| 23/09/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 23/09/2025 | 0800/1000 | ** | S&P Global Composite PMI (p) | |

| 23/09/2025 | 0830/0930 | *** | S&P Global Manufacturing PMI flash | |

| 23/09/2025 | 0830/0930 | *** | S&P Global Services PMI flash | |

| 23/09/2025 | 0830/0930 | *** | S&P Global Composite PMI flash | |

| 23/09/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 23/09/2025 | 0900/1000 | BOE Pill Fireside Chat At Pictet Research Institute Symposium | ||

| 23/09/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 23/09/2025 | 1230/0830 | * | Current Account Balance | |

| 23/09/2025 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 23/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 23/09/2025 | 1300/0900 | Fed Governor Michelle Bowman | ||

| 23/09/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 23/09/2025 | 1345/0945 | *** | S&P Global Services Index (flash) |