MNI EUROPEAN MARKETS ANALYSIS: USD Weakness Not Uniform

- Official Japan and US comments helped USD/JPY correct lower, but we remain above key support. US Tsy yields have been very quiet, while NZ yields have crept higher supported by firmer local data.

- The USD is mostly softer elsewhere, although USD/PHP hit a fresh record high. South Korea GDP was better than forecast but this did little for local assets.

- Later August US S&P Cotality & FHFA house prices, October Richmond & Dallas Fed indices and October Conference Board consumer confidence as well as German November GfK consumer confidence and ECB bank lending survey are released.

MARKETS

US TSYS: Quiet Day as Curves Modestly Flatter

Despite weakness across major equity bourses, US bond futures didn't see a lead in with TYZ5 posting only modest gains. Up +02 at 113-15+ the the 10-Yr price action was muted as volumes remained modest throughout the trading day.

Cash volumes were light also, capping yield moves.

- The US 2-Yr is 3.499% (+0.4bp)

- The US 5-Yr is 3.607% (+0.3bp)

- The US 10-Yr is 3.979% (-0.4bps) as it consolidates below the 4.00% recent range bottom.

- The US 30-Yr is 4.551% (-0.3bp)

Focus for markets tonight will be US$69bn 2-Yr auction, US$70bn 5-Yr auction and various bill auctions.

Economic Data focus is on :

10/28/2025 9:00 FHFA House Price Index MoM (-0.1%, -0.1%)

10/28/2025 9:00 S&P Cotality CS 20-City MoM (-0.07%, -0.10%), YoY (1.82%, 1.40%)

10/28/2025 10:00 Richmond Fed Mfg Index (-17, -10)

10/28/2025 10:00 Conf. Board Consumer Confidence (94.2, 93.4)

10/28/2025 10:30 Dallas Fed Services Activity (-5.6, --)

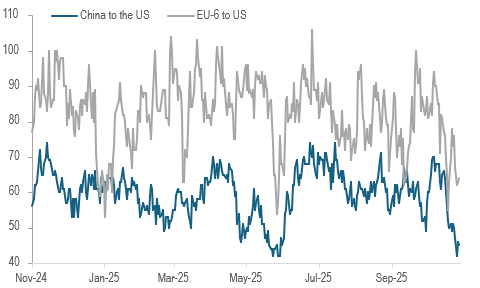

GLOBAL MACRO: China To US Container Ship Count Down Over Oct As Tensions Rise

US President Trump’s tour of Asia is bringing trade back into focus. Treasury Secretary Bessent said that a draft US-China deal had been reached and Trump and President Xi are expected to formalise it when they meet on Thursday. Shipments from China to the US have fallen sharply over October as tensions intensified again but may now recover when it is confirmed that an additional 100% US tariff will be avoided from 1 November. There was significant frontloading of exports to the US by its major partners in H1 to beat tariff deadlines and some payback in H2 had been expected.

- The US was also to add a duty for every Chinese ship docking in the US but that has now been delayed for a year, which may have also pressured departures.

- Bloomberg’s container ship count from Korea to the US declined significantly this month too from around 40 at the start of October to around 25 over the weekend. The two continue to work towards a trade agreement but Bessent said the details are too complex to be finalised while Trump meets President Lee in Korea on Wednesday.

- The number of vessels leaving Japan for the US has trended lower since mid-year but may have stabilised towards the end of October. Trump visited Japan Tuesday and signed vague trade and critical mineral agreements as details still need to be decided. He and new PM Takaichi have a good relationship. He was positive on US-Japan trade.

- Many of the details on the EU-US trade deal are also yet to be decided. Vessels leaving the EU-6 for the US have been running at a lower trend in H2 to date than in Q2.

Bloomberg container ship count (rolling 15 day period)

Source: MNI - Market News/Bloomberg Finance L.P.

JGBS: Futures Firmer But Under Resistance Level, Back End Yields Off 1-2bps

JGB futures have drifted a little higher, last 136.17, +.21, versus settlement levels, but recent ranges continue to prevail. Dips under 136.00 continue to be supported, but we remain comfortably sub key short term resistance (137.30). A positive bias from US Tsy futures has helped, although likewise in this space, we continue to track within recent ranges (as markets await the FOMC). Cash JGBs are biased lower, led by the 10 and 20yr tenors.

- There has been a lot of focus today on US-Japan meetings, with US President Trump & Japan PM Takaichi headlines crossing today, although remarks were mostly high level. Takaichi reiterated intentions around increased defense expenditure (2% of GDP by March next year), which is a potential fiscal pressure point but hasn't impacted sentiment today.

- The US Tsy also gave a read out of the Tsy Secretary and Japan FinMin meeting, with Bessent emphasizing the need for sound monetary policy to keep inflation expectations anchored and avoid FX volatility. These remarks have helped the yen today.

- Our policy team noted that even with a sluggish underlying inflation backdrop, hike risks are still on the cards from Dec of this year.

- Cash JGB yields see the 10yr back to 1.65% (off 2bps), while the 30yr is again flirting with the 100-day EMA support point, last around 3.07%.

AUSSIE BONDS: Front End Yields Up, Nov RBA Easing Risks Pared, Q3 CPI Tomorrow

Aussie 3yr (YM) bond futures underperformed, last 96.545, off 3.5bps. 10yr futures were up a touch to 95.815. The bias in US Tsy futures has been to nudge higher, support the Aussie 10yr but the 3yr is likely reflecting near term uncertainties around the RBA outlook, with tomorrow's Q3 CPI print in focus. ACGB yields are mixed, as the curve flattens, the front end 3yr establishing itself back above 3.40% (last 3.44%), while the 10yr has drifted lower to 4.165%. This leaves the 3/10s curve at +72bps, flatter by 5bps.

- The AU-US 10yr spread is near +19bps, so back towards the upper ends of its recent range. We see spread compression trades re-emerge above +30bps, but a lot depends on tomorrow's Australian Q3 CPI print.

- Key watch points for CPI tomorrow are as follows: Bloomberg consensus expects trimmed mean to print at 0.8% q/q & 2.7% y/y, which would see a pickup in the 2q/2q annualised rate to 2.8% from 2.6%. This outcome could argue for a hold or a cut dependent on the revised outlook and services inflation result. This week Bullock reiterated that labour data are volatile and while the 0.2pp rise in the September unemployment rate to 4.5% was surprising, it could fall again in October. Thus she would like more information.

- Market pricing has around 10bps of easing priced in for Nov, we were around 16bps at the end of last week. A full cut is priced by the Feb meeting next year.

AUSTRALIA: Q3 Trimmed Mean Forecast To Stabilise At 2.7% Y/Y But Q/Q To Rise

Q3 CPI data are released 29 October and are likely to be a key input into the next RBA decision on 4 November. The focus will remain on the trimmed mean which Bloomberg consensus is forecasting to rise 0.8% q/q and remain at 2.7% y/y. In August the RBA expected it to moderate to 2.6% y/y by Q4 2025 and signs that there are upside risks to underlying inflation returning to the 2.5% band mid-point as expected may drive a prolonged pause in easing to allow more information to be gathered.

- Forecasts for Q3 underlying trimmed mean are between 0.7% and 1.0% q/q & 2.5% and 2.8% y/y. CBA and Westpac are in line with consensus while ANZ and NAB are slightly higher at 0.9% & 2.8% expecting a pickup in core inflation.

- In the Bloomberg October survey, Westpac has a Q4 2025 rate cut, while ANZ, NAB and CBA don’t expect the next move to be until H1 2026.

- Bloomberg consensus expects Q3 headline CPI to rise 1.1% q/q to be up 3.0% y/y after Q2’s 0.7% q/q & 2.1% y/y. This series continues to be distorted by government electricity rebates.

- Consensus estimates range from 0.7% to 1.0% q/q and 2.6% to 3.1% y/y with local banks CBA, NAB and Westpac all at consensus but ANZ expecting slightly higher at 1.2% q/q & 3.1%.

- September headline inflation is projected to pick up to 3.1% y/y from August’s 3.0% with forecasts between 2.9% and 3.3%. NAB and Westpac are in line with consensus, while ANZ is higher at 3.2%. Goldman Sachs expects 3.3%.

RBA: Higher Core CPI Could Drive RBA Pause In November & Await More Data

The RBA August projections had another 25bp of easing in Q4 based on market pricing. This still allowed underlying inflation to settle close to the 2.5% band mid-point over 2026. Wednesday’s Q3 CPI data will be important for how it impacts the RBA’s inflation outlook which will be key for the 4 November decision. A pause at the November meeting is likely to leave the December meeting live though. Market pricing reflects a good degree of uncertainty around November.

- The AUD OIS is currently not sure with 10bp priced in for November and 17bp by year end but this could move sharply with Q3 CPI.

- Key watch points for CPI tomorrow are as follows: Bloomberg consensus expects trimmed mean to print at 0.8% q/q & 2.7% y/y, which would see a pickup in the 2q/2q annualised rate to 2.8% from 2.6%. This outcome could argue for a hold or a cut dependent on the revised outlook and services inflation result.

- Contained services, core around 2.6-2.7% y/y or below would likely drive further easing, but even 2.8% could see another hold in November as the Board waits for more data, especially given it sees “signs that private demand is recovering”.

- Bullock said the Board was concerned about the rise in some of monthly CPI components, especially services. She noted that it has been sticky overseas and so the change in Q3 market services prices will be monitored. It moderated to 2.9% y/y in Q2 from 3.3%.

- This week Bullock reiterated that labour data are volatile and while the 0.2pp rise in the September unemployment rate to 4.5% was surprising, it could fall again in October. Thus she would like more information. The Board also looks at the 3-month averages and the Q3 unemployment rate only rose 0.1pp to 4.3% while underemployment fell 0.2pp to 5.8%.

- There are a lot of key data before the December meeting which could drive a November pause to wait and see, including surveys but also October jobs on 13 November, Q3 wages 19 November, October CPI 26 November (first full sample monthly CPI) and Q3 GDP 3 December.

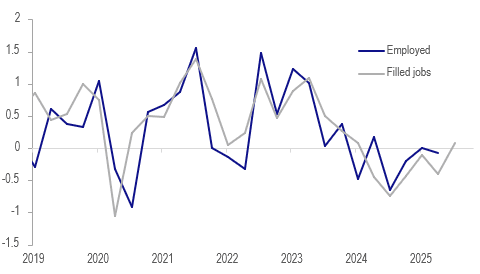

NEW ZEALAND: Filled Jobs Signal Q3 Labour Market Stabilisation

Q3 NZ filled jobs rose 0.1% q/q signalling that employment likely stabilised in the quarter after falling 0.1% q/q in Q2. Q3 labour market data print on 5 November and will be an important input into the 26 November RBNZ decision. September jobs rose 0.3% m/m to be down 0.4% y/y up from August’s +0.1% m/m & -0.9% y/y. Vacancies are also consistent with the start of a labour market recovery as SEEK job ads rose each month in Q3 to be up 4.3% q/q.

- Q3’s rise in filled jobs was the first since Q1 2024 and the labour market was slowing at that time.

NZ employment q/q%

- The largest monthly rise in filled jobs in almost two years was driven by the services sector. Services rose 0.4% m/m, goods-producers +0.1% m/m but primary industries fell 0.5% m/m.

- Compared to a year ago education and healthcare outperformed with jobs up 2.0% y/y and 1.8% y/y respectively. The market economy’s demand for labour is weak with construction down 4.5% y/y, professional & technical services -2.6% and manufacturing -1.7% but lower rates may help this turn around in coming quarters.

- Youth employment remains a problem with filled jobs for 15-19 years down 6.6% y/y, but there has been an increase in those in education since the labour market weakened. 20-24 years is 2.6% y/y lower and 25-29 -2.9% y/y.

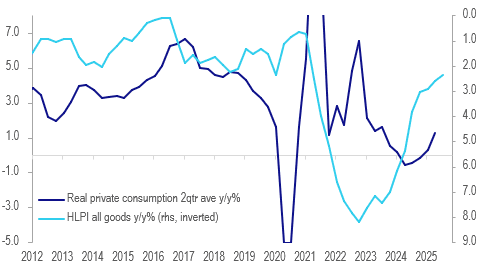

NEW ZEALAND: Moderating Living Costs Suggest Ongoing Consumption Recovery

NZ’S household living-costs price index (HLPI) for Q3 rose 2.4% y/y, below the CPI at 3.0%, down from 2.6% in Q2 and 3.8% in Q3 2024. It tends to lead real private consumption growth by two to six quarters, as lower living cost inflation boosts real incomes and thus purchasing power. The recent trend signals that the tentative recovery in spending growth should continue after Q2’s 1.5% y/y rate.

NZ household cost of living vs consumption %

- The RBNZ’s 250bp of easing to end-September has made a major contribution to moderating living costs with the interest HLPI -14.3% y/y in Q3 after -7.7% y/y. It peaked at +44.9% y/y in Q4 2022.

- Interest payments on all types of loans are likely to continue to aid households as the OCR was cut 50bp in October and another 25bp is expected on 26 November as well as the continued rolling over of mortgages onto lower rates.

- Rental cost inflation also moderated in Q3 to 2.6% y/y from 3.4%.

- Electricity costs and council rates remain a burden for households rising 11.3% y/y and 8.8% y/y in Q3 respectively.

- HLPI inflation ran above the CPI for around three years before falling below it in Q2 2025.

NZ HLPI y/y%

Source: MNI - Market News/Statistics NZ

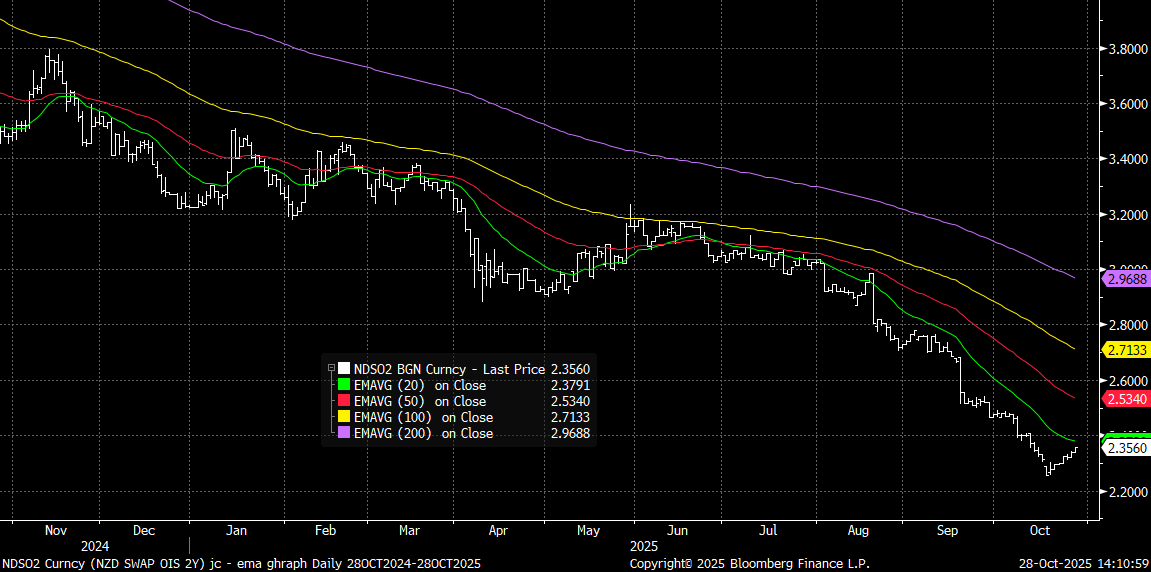

BONDS: NZGBS: 2yr Swap Close To 20-day EMA Resistance, Better Data Helps

NZGB yields have been biased higher as Tuesday trade unfolded, supported by earlier data outcomes. The 2yr is up nearly +2bps to 2.54%, while the 5yr is up near 3bps. The 10yr has seen a more modest rise and is still sub 4.00% at this stage. We are still sub key EMAs, but focus will rest on whether we can test higher. The 2yr swap rate is close to 2.36%, closing in on a test of its 20-day EMA resistance point, see the chart below.

- Earlier data showed Q3 NZ filled jobs rose 0.1% q/q signalling that employment likely stabilised in the quarter after falling 0.1% q/q in Q2. Q3 labour market data print on 5 November and will be an important input into the 26 November RBNZ decision.

- Other data showed NZ’S household living-costs price index (HLPI) for Q3 rose 2.4% y/y, below the CPI at 3.0%, down from 2.6% in Q2 and 3.8% in Q3 2024. It tends to lead real private consumption growth by two to six quarters. The recent trend signals that the tentative recovery in spending growth should continue after Q2’s 1.5% y/y rate.

- RBNZ pricing still has a 25bps cut priced in for the Nov meeting, but OIS dated contracts for 2026 are slightly firmer. For July 2026 we are around 2.18%, against mid Oct lows near 2.00%.

- The NZ 2/10s curve has flattened today, off around 2bps to +146bps. The NZ-US10yr spread is holding above flat, last +3bps.

- Tomorrow, the local data calendar is empty.

Fig 1: NZ 2yr Swap Rate & Key EMAs

Source: Bloomberg Finance L.P/MNI

FOREX: US & Japan Comments Aid USD/JPY Dip, Still Above Key EMAs

Yen has outperformed so far in Tuesday trade, with USD/JPY back testing under 152.00 and up around 0.60% in yen terms so far today. US-Japan meetings have dominated the headlines (with Bessent remarks aiding yen gains), while we also saw some verbal FX jawboning from Japan's economic minister, which has also likely helped at the margins. The BBDXY index is down 0.205 to 1209.15.

- The readout from the meeting between the US Tsy Secretary and the Japan FinMin highlighted: ""Bessent highlighted the “important role of sound monetary policy formulation and communication in anchoring inflation expectations and preventing excess exchange rate volatility, as conditions are substantially different twelve years after the introduction of Abenomics,” (via BBG). So, whilst the upcoming Thursday monetary policy meeting wasn't discussed, Bessent is stating the different macro landscape between now and when Abenomics and that FX volatility will pick up if monetary policy is not conducted properly, which will likely concern the US authorities.

- Still, USD/JPY is some distance from the 50-day EMA, which is still back under 150.00.

- CHF has also risen, last 0.7930/35, up 0.25%. Lower US yields from Monday have also likely aided safe haven gains today. US equity futures are little changed.

- AUD and NZD are higher, although more so the Kiwi. NZD/USD was last 0.5780, looking to establish a base above the 20-day EMA. NZ front yield ends are drifting a little higher, with some data outcomes helping these trends. AUD/USD is a little higher last 0.6560, still above all key EMAs, as focus shifts to tomorrow's key Q3 CPI outcome.

- Later August US S&P Cotality & FHFA house prices, October Richmond & Dallas Fed indices and October Conference Board consumer confidence as well as German November GfK consumer confidence and ECB bank lending survey are released.

ASIA STOCKS: Markets Mixed as Investors Wait for News from APEC Summit

The record period for Asia's major bourses took a breather today ahead of the APEC summit as the world awaits to see what 'deals' are announced. With the focus on a US China pact and further news on the USD$350bn investment fund for Korea investment in the US, China and Korea were among the fallers today. The hopes of a US China trade pact has seen flows into EM funds strengthen with the Vanguard FTSE Emerging Markets ETF has had over $400m of net inflows in recent days with investors seeking to benefit from a cooling of the trade war. This comes despite key markets hitting new all time highs in advance of the APEC summit.

- The KOSPI was one of the biggest fallers of the major markets down -1.25% and back below 4,000.

- The NIKKEI has done very little whereas the major bourses in China have all delivered modest gains with onshore indexes +0.20 - 0.40% higher whilst the HSI did very little.

- The Jakarta Composite fell heavily yesterday and the weakness carried on into today with falls of -0.18%. The losses sees the JCI at 8,106 and dip below the 20-day EMA of 8,126. It has traded below the 20-day EMA only once in the last month, failing to hold losses as buyers returned.

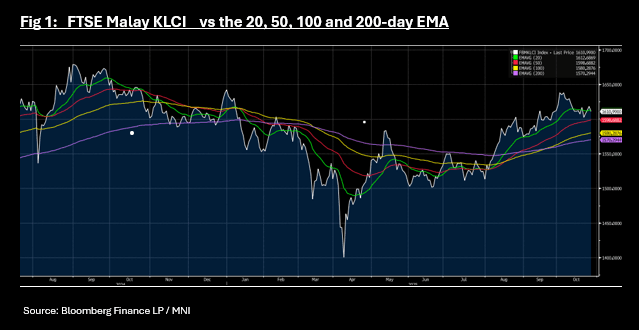

- The FTSE Malay KLCI is one of the biggest fallers, despite the potential for a trade deal that could be imminently announced with the US, as President Trump visits. Malaysia and the US upgraded ties to the highest rung possible, and the two sides pledged to deepen maritime security cooperation at a time when the US and China are competing for influence across the region (per BBG). Down -0.45% today sees the index break below the 20-day EMA which it has tried unsuccessfully to hold below on several occasions this month.

ASIA STOCKS: Risk On Drives Monday Inflows, But South Korea Seeing Fresh Outflow

Major markets saw strong inflow momentum to start the week on Monday, aided by the risk on bounce induced by positive US-China trade headlines/developments. Taiwan saw just over $1bn in net inflows, although this wasn't enough to bring the 5-day sum back into positive territory. The Taiex is trying to move higher today, but is just short of record highs, holding near 28000.

- For South Korean markets, net inflows were not quite as strong yesterday, while early trends today are notably poorer. Close to $1bn in net outflows has been seen in Tuesday trade to date (see KSFINET Index on BBG), as the Kospi softens, down more than 1%. The local index has surged so far in Oct and is still close record highs above 4000. US-South Korea trade concerns persist particularly over the $350bn investment pledge and its impact on local FX. BBG notes onshore retail investors moving into USD denominated assets to protect against further FX losses. This may be impacting offshore investor sentiment as well.

- Indian inflow momentum remained positive into the end of last week, but had slowed. Chatter around the US-India trade deal has died down somewhat, while local equity index gains have slowed relative in Oct.

- In SEA, inflow momentum remains strong into Indonesia, not impacted by FX weakness. Trends are more mixed elsewhere.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 617 | 101 | 3596 |

| Taiwan (USDmn) | 1019 | -1375 | 6054 |

| India (USDmn)* | 65 | 61 | -16105 |

| Indonesia (USDmn) | 72 | 295 | -2787 |

| Thailand (USDmn) | -70 | 290 | -2932 |

| Malaysia (USDmn) | -58 | -61 | -4179 |

| Philippines (USDmn) | -5 | -14 | -730 |

| Total (USDmn) | 1639 | -704 | -17083 |

| * Data Up To Oct 24 |

Source: Bloomberg Finance L.P./MNI

OIL: Crude Steady On Excess Supply Concerns But Monitoring Sanctions Impact

Oil prices are steady in today’s APAC session after being little changed on Monday as the market looks to Wednesday’s Fed decision and Sunday’s OPEC meeting. There are conflicting forces with the market continuing to worry about excess supply with seaborne crude elevated but also aware that the latest US/EU sanctions on Russia could cause disruption as well as increase demand for non-Russian crude. Thus oil could range trade while waiting for new supply/demand developments. Both Brent and WTI are down only slightly in October.

- WTI is down 0.1% to $61.24/bbl after reaching an intraday low of $61.10. Initial support is at $59.64, 23 October low, and resistance at $62.59, 24 October high. Moves higher appear to be corrective.

- Brent has been trading between initial support at $63.86, 24 October low, and resistance at $66.78, 24 October high. The benchmark is little changed at $65.64/bbl after falling 0.5% on Monday but remains above the 50-day EMA at $65.15.

- Russia’s Lukoil is looking to sell its overseas interests following the latest sanctions and Germany has asked for a delay to allow Rosneft to deal with its German assets.

- OPEC meets on Sunday to decide the December output target which could rise again, although there is little spare capacity outside Saudi Arabia. With supply an ongoing concern inventory data will continue to be monitored. US industry-based figures are released on Tuesday.

- Later August US S&P Cotality & FHFA house prices, October Richmond & Dallas Fed indices and October Conference Board consumer confidence as well as German November GfK consumer confidence and ECB bank lending survey are released.

Gold Range Trading Ahead Of October Fed Decision

Gold range traded during today’s APAC session with breaks above $4000 continuing to be temporary. Prices have just dipped and are down 0.3% to $3970.0 after a high of $4019.68 and intraday low at $3964.01. It found some support from the weaker US dollar (BBDXY -0.2%) while US yields are steady. There was little news to drive safe-haven flows in either direction ahead of Wednesday’s Fed decision.

- Gold has held above support at $3944.9, 9 October low, but remains well below initial resistance at $4186.4, 17 October low. Bullion continues to be in overbought territory despite the recent correction.

- Central bank buying, especially from the PBoC, has provided medium-term support to gold prices and this is generally expected to continue. In line with this, the Bank of Korea said today that it is considering extra purchases for its reserves over the medium- to long-term which would be the first time in 10 years.

- Silver is down 0.3% to $46.68 and has also been in a narrow range between $46.620 and $47.227, below initial support at $47.55, 22 October low. The trend also remains overbought and the current decline is seen as corrective.

- Equities are mixed with the S&P e-mini flat, KOSPI down 1.2% but CSI 300 up 0.2%. Oil prices are lower with WTI -0.2% to $61.16/bbl. Copper is down 0.6%.

- Later August US S&P Cotality & FHFA house prices, October Richmond & Dallas Fed indices and October Conference Board consumer confidence as well as German November GfK consumer confidence and ECB bank lending survey are released.

ASIA FX: USD/PHP To Fresh Record Highs, KRW Underperforms Broader USD Weakness

Asia FX trends are mixed in NEA, with CNH and TWD rallying, but KRW faltering. USD/CNH has tested under 7.1000. In SEA, focus has been on USD/PHP, which rallied to fresh record highs above 59.0. MYR and THB are firmer though. The CNY fixing/onshore CNY spot helped sentiment, along with lower USD/JPY levels, although regional equity sentiment has mostly been softer.

- USD/CNH got to lows of 7.0956 earlier, but we sit back closer to 7.1000 now. The USD/CNY fix was again set lower, but reaction in USD/CNH more came after the spot open (which also broke under 7.1000). Focus remains on Thursday's meeting between Trump and XI, with some good news already priced into FX markets. For USD/CNH downside focus will be at mid Sep lows of 7.0851.

- Spot USD/KRW has bucked the softer USD/CNH trend, and yen gains. We have rebounded to 1435/36, up around 0.20%. Offshore equities have fallen over 1%, but still remain up strongly for Oct to date. Offshore investors have been strong net sellers so far today. Concern around the US-South Korea trade deal, particularly what the investment pledge will mean for FX markets has also been cited as weighing on local investor sentiment. In contrast, USD/TWD has tracked lower, down to 30.60/65, up around 0.25% in TWD terms.

- USD/PHP surged above 59.00 not long after the open, getting to fresh cycle highs of 59.19, before some selling interest emerged. Familiar themes are in play around domestic growth concerns, equity outflows and more BSP easing expected. The central bank stated the FX rate is market determined and via BBG: "“When we do participate in the market, it is largely to dampen inflationary swings in the exchange rate over time rather than to prevent day-to-day volatility,” the Bangko Sentral ng Pilipinas said in a statement on Tuesday."

- USD/MYR has fallen back towards 4.2000, aided by the firmer yuan back drop and broader USD softness.

- USD/THB is back to 32.55/60 so back eyeing a 100-day EMA downside test.

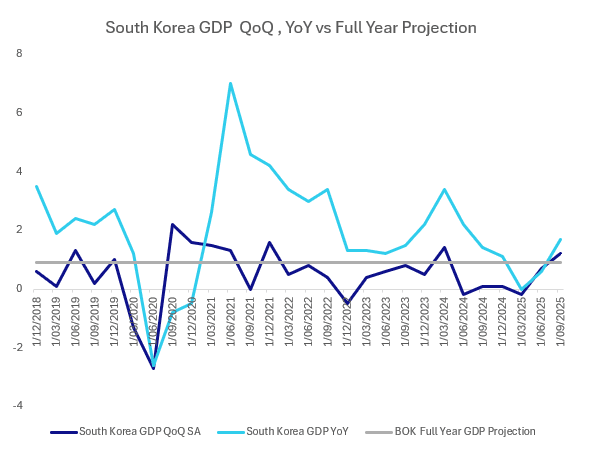

SOUTH KOREA: GDP Tops Forecasts, Time Now on Side for Next Rate Move

- The momentum in the Korean economy seems to be building as the 3Q result topped estimates.

- Coming on the back of comments from the President on BBG TV about the housing market, particularly Seoul. “The truth is, the Republic of Korea is sitting on a very dangerous potential crisis, a ticking bomb — that is excessive real estate investment,” Lee told Bloomberg TV in an interview. “If we were to lower interest rates, this could stimulate real estate prices, which is already an issue for us. The BOK made the right decision (last week) by keeping rates unchanged instead of cutting them.”

- Korea's 3Q advance GDP printed at +1.7% YoY, ahead of expectations of +1.2% and significantly up from 2Q result of 0.6%

- The 3Q advance GDP QoQ was +1.2% topping expectations of 1%.

- Manufacturing was strong at +1.2% QoQ; +3.3% YoY, whilst construction declined -8% YoY

- Services were up +1.3% QoQ and 2.2% YoY.

- Despite the headwinds from tariff forecast to knock -0.4% off GDP, exports have held up well in Korea up +12% in September.

- As the BOK held last week on account of the real estate sector, the market has now no expectations for rate cuts over the coming 12 months and the potential for the central bank to be on hold for some time as the property market corrects.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 28/10/2025 | 0700/0800 | * | GFK Consumer Climate | |

| 28/10/2025 | 0900/1000 | ** | ISTAT Consumer Confidence | |

| 28/10/2025 | 0900/1000 | ** | ISTAT Business Confidence | |

| 28/10/2025 | 0900/1000 | ** | ECB Bank Lending Survey | |

| 28/10/2025 | 0900/1000 | ** | ECB Consumer Expectations Survey | |

| 28/10/2025 | 1000/1000 | * | Index Linked Gilt Outright Auction Result | |

| 28/10/2025 | - | FOMC Meeting | ||

| 28/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 28/10/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 28/10/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 28/10/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 28/10/2025 | 1400/1000 | *** | Conference Board Consumer Confidence | |

| 28/10/2025 | 1400/1000 | ** | Richmond Fed Survey | |

| 28/10/2025 | 1400/1000 | ** | housing vacancies | |

| 28/10/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 28/10/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 28/10/2025 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note | |

| 29/10/2025 | - | Bank of Japan Meeting | ||

| 29/10/2025 | 0001/0001 | * | Brightmine pay deals for whole economy | |

| 29/10/2025 | 0030/1130 | *** | CPI Inflation Monthly | |

| 29/10/2025 | 0030/1130 | *** | CPI inflation | |

| 29/10/2025 | 0700/0800 | Flash Quarterly GDP Indicator | ||

| 29/10/2025 | 0700/1500 | ** | MNI China Money Market Index (MMI) | |

| 29/10/2025 | 0800/0900 | *** | GDP (p) | |

| 29/10/2025 | 0930/0930 | ** | BOE Lending to Individuals | |

| 29/10/2025 | 0930/0930 | ** | BOE M4 | |

| 29/10/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 29/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 29/10/2025 | 1100/1200 | ** | PPI | |

| 29/10/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 29/10/2025 | 1345/0945 | *** | Bank of Canada Policy Decision |