MNI EUROPEAN MARKETS ANALYSIS: USD Supported On Dips

- JGB back end yields are down sharply, as Rtrs reported that the Japan MOF may shift the composition of its bond issuance plan for the current fiscal year. This followed earlier remarks from the FinMin that bond markets would be monitored closely.

- The USD has been supported as the session unfolded, with USD/JPY rebounding over 100pips from its lows. US Tsy yields are down in sympathy with JGB moves. Regional equities are mostly weaker.

- Later the Fed’s Kashkari and Barkin appear. US April durable orders, May consumer confidence & Dallas Fed manufacturing index, March US house prices, French preliminary May CPI and euro area EC May survey are released.

MARKETS

US TSYS: Asia Wrap - Long-End Leads Yields Lower

The TYM5 range has been 110-01 to 110-07+ during the Asia-Pacific session. It last changed hands at 110-07, up 0-04 from the previous close.

- The US 2-year yield has drifted lower, dealing around 3.976%, down 0.01 from its close.

- The US 10-year yield has moved lower, dealing around 4.483%, down 0.03 from its close.

- The move was led by the long-end, the yield curve has flattened as a result - 2s10s -1.50 at 50.054.

- FT - "Quasi-governmental entities like Japan Post, Norinchukin, and GPIF together own over a trillion dollars of foreign bonds. The government could urge them to support the Japanese bond market. But that would likely involve selling their foreign bond holdings — most likely Treasuries — to buy JGBs. With Japan-US tariff negotiations under way, does Japan really want to be seen as the reason Treasury yields keep rising?" https://x.com/elerianm/status/1926273166520746139

- Bloomberg - “Donald Trump’s erratic policies offer a “prime opportunity” to strengthen the euro’s international role as a reserve currency, letting the EU enjoy lower borrowing costs and protections from sanctions, Christine Lagarde said.”

- The 10-year look likely to see supply on any dips in yield in the short-term, should yields hold above 4.40% the target looks to be the 4.75% area. Watch for any announcements though relating to the SLR, this could have an impact on a market that is already quite short.

- Data/Events : Durable Goods, FHFA House Price Index, Conference Board, Dallas Fed Man Activity.

JGBS: Massive Bull-Flattener, MoF May Tweak Long-End Issuance

JGB futures are stronger and approaching session highs, +30 compared to settlement levels, after reversing almost all of early weakness.

- A headline late in our session: "Japan's Ministry of Finance will consider tweaking the composition of its bond issuance plan for the current fiscal year ending in March 2026, which could involve trimming the issuance of super-long bonds, two sources with direct knowledge of the plan told Reuters".

- MNI: BOJ's Ueda Sees Inflation Near 2%, Easing Still Needed (See here)

- Robin Brooks on X: Japan is at the heart of the global rise in long-term yields. To be honest, I'm surprised the rise has been allowed to be as rapid as it has. At 240% debt to GDP, Japan really can't allow long-term yields to keep rising the way they have. This is where fiscal dominance is acute. (See here)

- Cash US tsys are 2-5bps richer, with a flattening bias, in today's Asia-Pac session after yesterday's holiday.

- Cash JGBs are 1-16bps richer across benchmarks, with the curve flatter. The benchmark 40-year yield is 16.3bps lower at 3.393% ahead of tomorrow's supply. ICYMI, last week's 20-year auction saw poor demand metrics.

- Swaps have twist-flattened, with rates 1bp higher to 12bps lower. Swap spreads are wider.

JAPAN DATA: Services PPI Slightly Above Estimates But Off Recent Y/Y Highs

The Japan April services PPI printed at 3.1% y/y, versus a market forecast of 3.0%. The March read was revised higher to 3.3% (from 3.1% originally reported). The chart below plots the PPI services y/y outcome (the white line) against headline CPI y/y. The PPI has come off its highs from early 2025, but still remains quite elevated by historical standards.

- The monthly rise was 0.5%, versus a 0.8% gain in March. BBG notes the 3 month annualized pace firmed to 2.3%, from 00.6% in March. We are still sub the 4.8% pace seen on this metric in Dec last year.

- Overall, this print suggests elevated inflation pressures persist, albeit without fresh upside from late 2024/early 2025.

- Note we get Tokyo CPI this Friday for May.

Fig 1: Japan Services PPI Y/Y Versus Japan CPI Y/Y

Source: MNI - Market News/Bloomberg

AUSSIE BONDS: Stronger Ahead Of Tomorrow's CPI Data

ACGBs (YM +4.0 & XM +6.0) are stronger with US tsys 2-4bps richer in today's Asia-Pac session after yesterday's holiday.

- Cash ACGBs are 4-6bps richer with the AU-US 10-year yield differential at -16bps.

- The bills strip richer, with pricing +1 to +4.

- RBA-dated OIS pricing is showing a 25bp rate cut in July as a 72% probability, with a cumulative 75bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- Today, the local calendar has been light.

- The focus remains on tomorrow's April CPI, which is forecast to moderate to 2.3% y/y from 2.4%. The trimmed mean has been around 2.7% y/y for four consecutive months. There will be limited updates to the services components being the first month of the quarter.

- Some of the components of Q1 GDP are also released this week, namely construction (Wed) and private capex (Thu).

- April retail sales print on Friday and are projected to rise 0.3% m/m after increasing the same amount in March.

- The AOFM plans to sell A$1200mn of the 4.25% 21 March 2036 bond on Friday.

BONDS: NZGBS: Closed On A Strong Note Ahead Of Tomorrow’s RBNZ Policy Decision

NZGBs closed richer and at session bests, with benchmark yields 3-4bps lower.

- Swap rates closed 2-4bps lower, with the 2s10s curve flatter.

- The RBNZ decision is announced tomorrow with the OCR widely expected to be cut 25bp to 3.25%, bringing total easing this cycle to 225bp.

- 23 out of 24 analysts surveyed by Bloomberg are forecasting this outcome.

- Given heightened uncertainty, the MPC is likely to retain its easing bias again, stating it has “scope” to cut rates further if required and its updated OCR path will be scrutinised to this end. A downward revision bringing the terminal to below 3%, estimated 'neutral', would signal a need for accommodation.

- The attention will be on the medium-term which is likely to show a softer outlook driven by weaker trading-partner growth due to recent global uncertainty. The RBNZ said in April that “on balance, these developments create downward risks to the outlook for economic activity and inflation in New Zealand”. See MNI RBNZ Preview here)

- Markets continue to price in 25bps of easing for tomorrow's meeting, with 64bps expected by November 2025.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond and NZ$225mn of the 4.25% May-36 bond.

RBNZ: MNI RBNZ Preview-May 2025: May 25bp Cut, Then?

- Download full report here.

- The RBNZ decision is announced on May 28 and rates are widely expected to be cut 25bp to 3.25% bringing total easing this cycle to 225bp. 23 out of 24 analysts surveyed by Bloomberg are forecasting this outcome.

- Given heightened uncertainty, the MPC is likely to retain its easing bias again stating it has “scope” to cut rates further if required and its updated OCR path will be scrutinised to this end. A downward revision bringing the terminal to below 3%, estimated 'neutral', would signal a need for accommodation.

- The attention will be on the medium-term which is likely to show a softer outlook driven by weaker trading-partner growth due to recent global uncertainty. The RBNZ said in April that “on balance, these developments create downward risks to the outlook for economic activity and inflation in New Zealand”.

- Markets continue to price in 25bps of easing for the May meeting, with a total of 64bps expected by November 2025.

FOREX: Asia FX Wrap - Quiet Asian Session

The BBDXY has had a range of 1208.48 - 1210.80 in the Asia-Pac session, it is currently trading around 1210. “The ECB’s Gediminas Simkus says there’s a growing danger that inflation will fall short of the central bank’s 2% target due to trade friction and a stronger euro, adding there’s scope for a rate cut next month”(BBG). “Donald Trump’s erratic policies offer a “prime opportunity” to strengthen the euro’s international role as a reserve currency, letting the EU enjoy lower borrowing costs and protections from sanctions, Christine Lagarde said.”(BBG)

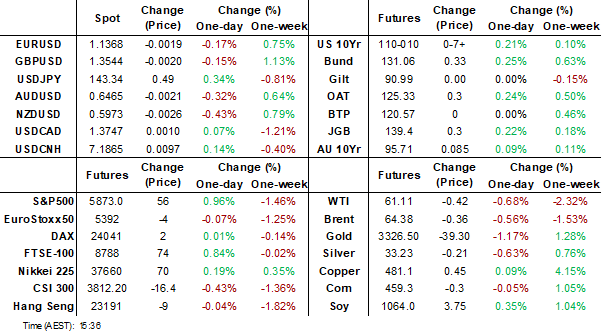

- EUR/USD - Asian range 1.1383 - 1.1407, Asia is currently trading 1.1390. EUR has had a quiet day in the Asian session. What stood out from the price action on Friday was how well the EUR held up in the face of a potential 50% increase in tariffs, and it was again the USD that took the brunt of the impact. This clearly shows the market's current outlook and leans into the growing “sell America “ theme. Dips back to 1.1200/1300 should be supported.

- GBP/USD - Asian range 1.3557 - 1.3587, Asia is currently dealing around 1.3565. The GBP is breaking the Pivotal Weekly Resistance in the 1.3500 area, all eyes will be on how the market reacts up here as most participants return. A sustained break though would signal a potential acceleration of the trend higher.

- USD/CNH - Asian range 7.1712 - 7.1851, the USD/CNY fix printed 7.1876. Asia is currently dealing around 7.1840. Sellers should be found on a bounce back towards the 7.2200 area again. Andreas Steno Larsen on X : The elephant in the room. USDCNH needs to go to 6.80 at least. https://x.com/AndreasSteno/status/1926115935200440525

- Cross asset : SPX +0.89%, Gold $3340, US 10-Year 4.48%, BBDXY 1210, Crude oil $61.31

- Data/Events : Ger Gfk Consumer Confidence, France CPI, EZ Consumer Confidence

JPY: Asia Wrap - USD/JPY Back Under Pressure

The Asia-Pac USD/JPY range has been 142.12 - 142.96, Asia is currently trading around 142.55. USD/JPY was under pressure early in our session as BOJ Governor Ueda sounded confident the central bank would meet its inflation target. A headline late in our session: "Japan's Ministry of Finance will consider tweaking the composition of its bond issuance plan for the current fiscal year ending in March 2026, which could involve trimming the issuance of super-long bonds, two sources with direct knowledge of the plan told Reuters". The long end in the JGB's extended their move lower late in our session and USD/JPY is attempting to bounce off its lows.

- MNI: BOJ's Ueda Sees Inflation Near 2%, Easing Still Needed https://www.mnimarkets.com/articles/mni-bojs-ueda-sees-inflation-near-2percent-easing-still-needed-1748306760883

- “The upcoming 40-year JGB auction tomorrow will be closely watched following a lackluster 20-year sale last week — a sign of the caution that still runs deep among long-end investors.”(BBG)

- Robin Brooks on X : Japan is at the heart of the global rise in long-term yields. To be honest, I'm surprised the rise has been allowed to be as rapid as it has. At 240% debt to GDP, Japan really can't allow long-term yields to keep rising the way they have. This is where fiscal dominance is acute. https://x.com/robin_j_brooks/status/1926991620370522435

- USD/JPY again struggled to hold onto any gains above 143.00, can Ueda’s comments get it to break below 142.00 or does this level hold again.

- The price action last week shows the market is still much more comfortable selling rallies, resistance is now back towards 144.00/145.00. The focus will turn once more to the pivotal 140.00 area, a break of which will open a much deeper move lower.

Options : Close significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 143.00($1.81b May 28), 143.00($3.06b May 30), 140.00($2.68b May 30).

Fig 1 : JGB 30 Year Daily Chart

NZD: Asia Wrap - Struggling To Hold Above 0.6000

The NZD/USD had a range of 0.5986 - 0.6007 in the Asia-Pac session, going into the London open trading around 0.5995. The NZD has drifted a little lower in a quiet Asian session, with US Stocks giving back their small overnight gains.

- (Bloomberg) - “Data since the April meeting have shown a softer labor market. Inflation has perked up but not enough to stop the RBNZ from proceeding with a 25-bp rate cut.”

- “There is significant downside risk to the growth outlook stemming from the global trade war. Even so, the 1Q CPI outcome is likely to see the RBNZ maintain its current OCR projections for only modest rate cuts.”

- Markets continue to price in 25bps of easing for tomorrow's meeting, with 64bps expected by November 2025.

- The NZD continues to trade in a 0.5850/0.6050 range, can it find the momentum to break this week, as the “sell America” trade gathers pace.

- The support back towards 0.5800 has held very well, and while this continues to hold expect buyers to be around on dips. The first target is the highs just above 0.6000, a break here could provide the spark for the next leg higher.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5725(NZD1.09b May 28)

- CFTC Data showed Asset managers maintaining their shorts, while the leveraged community added a decent clip back to their own short.

AUD/NZD range for the session has been 1.0803 - 1.0824, currently trading 1.0820. A sustained break above 1.0930 is needed to turn the focus higher, until then expect supply on bounces.

Fig 1: AUD/NZD Spot Daily Chart

Source: MNI - Market News/Bloomberg

AUD: Asia Wrap - Drifts Lower in The Crosses

The AUD/USD has had a tight range of 0.6475 - 0.6495 in the Asia- Pac session, it is currently trading around 0.6485. A very quiet session in Asia with AUD weakness coming through in the crosses, and the USD continuing to be sold against an Asian basket.

- The AOFM sells A$400mn of the 4.25% 21 June 2034 Green Bond: Average Yield (%): 4.2162 (prev. 4.1725), Bid/Cover: 5.1625x (prev. 4.8875x).

- The AUD range has been pretty muted during the Asian session. The AUD continues to hold up pretty well against the USD so If you want to express a short it looks best to do that in the crosses for now.

- Expect buyers to continue to be around on dips while the support in the AUD holds, a close back below 0.6300/50 would start to challenge the newly formed uptrend. A break above 0.6550 and the move higher could begin to accelerate.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6510(AUD1.55b), 0.6550(AUD 610m), 0.6500(AUD 443m). Upcoming Close Strikes : none

- CFTC Data shows Asset managers have continued to add to their shorts, the Leveraged community also added to shorts though still a very small position.

AUD/JPY - Today's range 92.14 - 92.76, it is trading currently around 92.30. The pair could not hold back above 93.00 overnight. A sustained close back below 91.50/92.00 is needed to turn the focus back towards the lows again.

Fig 1: AUD/JPY spot Daily Chart

Source: MNI - Market News/Bloomberg

ASIA: Major Bourses Down in Weak Day Across Region

Following yesterday's decline of -8.60%, China's BYD fell again today dragging the Hang Seng lower and impacting sentiment in the region. BYD is down -3.6% today as concerns grow that its sales success hides the scale of discounting in China. BYD announced price cuts of over 30% to stabilise the performance. BYD stock had risen over 70% this year, putting the recent falls in context.

In Korea holding companies are rallying with some up over 10% as expectations that a new president may be more shareholder friendly. One of Malaysia's biggest banks Maybank quarterly earnings showed solid loan growth and a 4% rise in income for the first quarter. With net foreign inflows of over $250m in May, Indonesia's Jakarta Composite is set to continue its recent run of good performance.

- China's major bourses were all lower today with the Hang Seng down -0.18%, CSI 300 -0.55%, Shanghai -0.33% and Shenzhen down -0.65%

- The KOSPI fell -0.66% today as markets hold their breath ahead of the BOK this week.

- The FTSE Malay KLCI fell again today, down -0.52% eighth day of losses out of the the last eleven trading days.

- The Jakarta Composite did very little today but remains over 6% better for the week.

- The Straits Times in Singapore eked out modest gains of +0.13% and the PSEi in the Philippines was flat.

- The NIFTY 50 is down -0.88% yet is holding on to a +1.8% gain for the month to date.

ASIA STOCKS: Big Inflows for Taiwan

After last week’s slow week, this week has started off on a positive note with strong inflows into Taiwan and South Korea.

- South Korea: Recorded inflows of +$135m yesterday, bringing the 5-day total to -$3m. 2025 to date flows are -$11,470. The 5-day average is -$1m, the 20-day average is +$79m and the 100-day average of -$115m.

- Taiwan: Had inflows of +$426m as of yesterday, with total inflows of +$1,571m over the past 5 days. YTD flows are negative at -$10,020. The 5-day average is +$314m, the 20-day average of +$441m and the 100-day average of -$104m.

- India: Had inflows of +$69m as of the 23rd, with total outflows of -$1,365m over the past 5 days. YTD flows are negative -$10,578m. The 5-day average is -$273m, the 20-day average of +$175m and the 100-day average of -$119m.

- Indonesia: Had inflows of +$20m as of yesterday, with total inflows of +$128m over the prior five days. YTD flows are negative -$2,797m. The 5-day average is +$26m, the 20-day average +$12m and the 100-day average -$32m.

- Thailand: Recorded outflows of +$35m as of yesterday, inflows totaling +$100m over the past 5 days. YTD flows are negative at -$1,652m. The 5-day average is +$20m, the 20-day average of -$4m and the 100-day average of -$17m.

- Malaysia: Recorded outflows of -$15m as of yesterday, totaling -$106m over the past 5 days. YTD flows are negative at -$3,198m. The 5-day average is -$22m, the 20-day average of +$31m and the 100-day average of -$22m.

- Philippines: Saw no flows yesterday, with net outflows of -$28m over the past 5 days. YTD flows are negative at -$256m. The 5-day average is -$6m, the 20-day average of +$2m the 100-day average of -$3m.

OIL: Crude Expects Another Large OPEC Output Increase, Meeting May 31

- Oil prices are down slightly today after finishing little changed yesterday. WTI is 0.5% lower at $61.24/bbl after reaching a high of $61.74 earlier. Brent is down 0.3% to $64.56 off the peak of $64.98. The market continues to monitor US trade talks especially with the EU but the focus now is on the May 31 OPEC meeting where another large output increase is expected to be agreed. The USD index is up 0.1%, which is probably moderately weighing.

- While energy markets remain concerned that the imposition of outsized tariffs would weigh on global energy demand, it is currently focussed on the impact of OPEC’s production plans on an already expected market surplus. The group increased output by over 400kbd in both April and June, more than expected. Apparently, a rise of a similar size is being discussed for July.

- There is key US data this week to gauge the strength of demand including orders (Tues), Q1 GDP revision (Thus), PCE (Fri), Trade (Fri) and Uni Michigan consumer confidence (Fri). There are also US crude & product data.

- Later the Fed’s Kashkari and Barkin appear. US April durable orders, May consumer confidence & Dallas Fed manufacturing index, March US house prices, French preliminary May CPI and euro area EC May survey are released.

GOLD: Bullion Under Pressure As Trade Talks Continue

Gold prices are slightly lower today down 0.3% to $3334.00 off the intraday low of $3331.99. Flight-to-quality flows continue to recede as trade negotiations continue with the current focus on US-EU.

- With the US appearing more open to reaching trade deals ahead of its July deadline, Bloomberg estimates that gold-backed ETFs have seen five consecutive weeks of outflows. However, the market remains nervous about the US’ fiscal position and any perception of a further deterioration would be supportive for bullion.

- Equities are mixed with the Hang Seng down 0.2% but S&P e-mini up 0.9% and ASX +0.3%. US 10yr yields are lower. Oil prices are down with WTI -0.3% to $61.34/bbl. Copper is 0.9% lower and iron ore has tested $95.80/t. Silver is down 0.7% to $33.25, close to the intraday low.

- Later the Fed’s Kashkari and Barkin appear. US April durable orders, May consumer confidence & Dallas Fed manufacturing index, March US house prices, French preliminary May CPI and euro area EC May survey are released.

CHINA: Country Wrap: Moody's Affirms China's Rating

- Moody's decision to affirm China's A1 ratings on Monday is a positive reflection of the improving prospects for the country's economy, the Chinese Ministry of Finance said. Since the fourth quarter of last year, the Chinese government has implemented a series of macroeconomic policies, economic indicators have improved, market expectations and confidence have stabilized, and the medium and long-term sustainability of debt has improved, the ministry said. (source China Daily)

- China's industrial firms saw a 3% increase in profits in April, driven by a government trade-in program and demand for manufactured products despite higher US tariffs.

- Improving earnings are crucial to bolstering business confidence, and stronger corporate balance sheets could reduce the urgency of additional stimulus by Beijing to meet its annual growth target. The government's program to subsidize equipment upgrades and consumer goods has boosted demand for industrial products, with manufacturing leading profit gains among industrial firms, particularly in high-tech sectors like artificial intelligence-enhanced manufacturing. (source BBG)

- China's major bourses were all lower today with the Hang Seng down -0.18%, CSI 300 -0.55%, Shanghai -0.33% and Shenzhen down -0.65%

- Yuan Reference Rate at 7.1876 Per USD; Estimate 7.1869

- Bonds continue their period in a tight range with the CGB 10YR at 1.69%

INDIA: Country Wrap: Monsoon This Year Likely to Ease Core Inflation

- A favorable monsoon in 2025 is expected to ease food inflation and support rural demand. However, the impact will hinge on how evenly and timely the rainfall is distributed across regions. With the India Meteorological Department (IMD) predicting an 'above normal' monsoon in 2025, economists said that the outlook raises hopes for a robust harvest, easing inflationary pressures and providing a much-needed boost to rural consumption. With more than 75 per cent of the country's annual rainfall occurring during the June-September period, a strong monsoon has direct implications for agricultural output, food prices, rural incomes, and overall economic momentum. A well-distributed and timely monsoon can ease food inflation, support agriculture output while also giving the Reserve Bank of India more headroom for accommodative monetary policy. However, this will depend not just on the 'above normal' monsoon but also its spatial and temporal distribution. (source BBG)

- Benchmark yields barely budged on Monday as the record ₹2.69 lakh crore dividend payout declared by the Reserve Bank of India (RBI) on Friday fell short of market expectations of ₹3 lakh crore. The RBI had paid ₹2.1 lakh crore dividend to the Centre last fiscal. The benchmark 10-year bonds closed at 6.25%, down by one basis point from the previous session. Shorter-term yields are, however, expected to trend lower going ahead given the comfortable liquidity, steepening the yield curve. (source EC Times)

- The NIFTY 50 is down -0.88% yet is holding on to a +1.8% gain for the month to date.

- The rupee fell today alongside most regional peers. Down -0.30 the rupee is at 85.34

- Bonds were marginally better with the IGB 10YR -1bps at 6.24%

SOUTH KOREA: Country Wrap: Consumer Sentiment Up in May

- Foreign currency deposits in South Korea fell by $680 million to $96.26 billion in April from March, driven by a $2.08 billion decline in dollar deposits due to raw material payments and loan repayments by companies, Bank of Korea data indicated. Euro deposits rose by $970 million due to temporary deposits of current transaction costs due to the strengthening of the euro, while yuan deposits increased by $310 million due to dividend receipts from some companies, the release said. (source BBG)

- South Korea's composite consumer sentiment index increased by 8 points to 101.8 in May from 93.8 in April, indicating a rebound, according to data released by the Bank of Korea on Tuesday. A reading above 100 indicates an improvement in outlook, while a reading under 100 suggests pessimism. Sentiment toward current living standards rose by three points to 90, while sentiment on the future outlook grew five points to 97. The outlook for future household income was three points higher at 99, and sentiment for future household spending climbed three points to 108. Optimism regarding current local economic conditions increased by 11 points to 63, and the reading for future domestic economic conditions was 18 points higher at 91. (source BBG)

- The KOSPI fell -0.66% today as markets hold their breath ahead of the BOK this week.

- The won was marginally weaker today as all eyes on the BOK on Thursday. The won fell -0.07% to be at 1,371.41

- Bonds have rallied across the curve with the KTB 10TR -2.5bps at 2.74%

MALAYSIA: Country Wrap: 10% Tariff Acceptable - Minister

- The US reducing its proposed tariffs on Malaysia to a 10% baseline would be seen as a positive move, Investment, Trade and Industry Minister said, conceding that a previously hoped for levy of zero may not be possible. “To be fair, and the US has also been public about this, that the 10% is not negotiable — it seems to be the floor,” he said in an interview with Bloomberg TV on Tuesday on the sidelines of a regional summit in Kuala Lumpur. (source BBG)

- Malaysian Prime Minister Anwar Ibrahim has expressed confidence that the 46th ASEAN Summit, held in Kuala Lumpur this week, will lead to a common stance on several critical matters, Tempo.co reported. “I am very optimistic because we have already achieved consensus on a number of key issues,” Anwar said in a special interview with the media on May 25, as reported by Antara. He attributed the progress to constructive discussions held both at the heads-of-state level and across ministerial forums. Among the agreed joint positions are ASEAN’s response to US import tariffs, strategies for digitalization and regional connectivity, Timor-Leste’s accession progress, and efforts to address the crisis in Myanmar. (source BBG)

- The FTSE Malay KLCI fell again today, down -0.52% eighth day of losses out of the the last eleven trading days.

- The ringgit was weaker by -0.06% today at 4.21

- Bonds saw higher yields across most maturities with he 10YR at 6.82% (+0.5bps today)

ASIA FX: USD/CNH Edges Higher, KRW Flat, TWD Outperforms

In NEA FX markets, the USD has found some support as the session has progressed, particularly against CNH and KRW. TWD has modestly outperformed. Broader USD sentiment has improved against the majors, with yen gains pared as back end JGB yields come lower (post reports that the MOF may tweak its issuance plan, via Rtrs).

- USD/CNH is back close to 7.1860, up nearly 0.15% versus end Monday levels. Earlier fresh YTD lows yesterday were at 7.1616. Onshore spot is also higher, last above 7.1900. Outside of broader USD gyrations we have seen some softness in local equities as well. The CSI 300 is off more than 3% from recent May highs. Strong competition in the EV sector is one factor which has weighed on investor sentiment. Industrial profits for April edged up to 3% y/y.

- Spot USD/KRW has been supported at 1365 level today. We were last near 1370, close to session highs, but little changed versus end Monday levels. USD/KRW appears to have followed USD/CNH shifts for the most part today. Earlier we had the consumer sentiment number bounce, whilst inflation expectations edged down.

- Spot USD/TWD is lower, back under 29.90, but away from best levels for the session in the pair. Tailwinds from strong equity flows this month may be aiding sentiment, while we have the monitor indicator due a little later.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 27/05/2025 | 0600/0800 | * | GFK Consumer Climate | |

| 27/05/2025 | 0645/0845 | *** | HICP (p) | |

| 27/05/2025 | 0800/0400 | Minneapolis Fed's Neel Kashkari | ||

| 27/05/2025 | 0900/1100 | * | Consumer Confidence, Industrial Sentiment | |

| 27/05/2025 | 1000/1100 | ** | CBI Distributive Trades | |

| 27/05/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 27/05/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 27/05/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 27/05/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 27/05/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 27/05/2025 | 1300/0900 | ** | FHFA Quarterly Price Index | |

| 27/05/2025 | 1300/0900 | ** | FHFA Quarterly Price Index | |

| 27/05/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 27/05/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 27/05/2025 | 1700/1300 | * | US Treasury Auction Result for 2 Year Note | |

| 28/05/2025 | - | Reserve Bank of New Zealand Meeting | ||

| 28/05/2025 | 0130/1130 | *** | CPI Inflation Monthly | |

| 28/05/2025 | 0130/1130 | *** | Quarterly construction work done | |

| 28/05/2025 | 0200/1400 | *** | RBNZ official cash rate decision | |

| 28/05/2025 | 0600/0800 | ** | Retail Sales | |

| 28/05/2025 | 0600/1400 | ** | MNI China Money Market Index (MMI) | |

| 28/05/2025 | 0645/0845 | ** | PPI | |

| 28/05/2025 | 0645/0845 | *** | GDP (f) | |

| 28/05/2025 | 0645/0845 | ** | Consumer Spending | |

| 28/05/2025 | 0700/0900 | ** | Economic Tendency Indicator | |

| 28/05/2025 | 0755/0955 | ** | Unemployment | |

| 28/05/2025 | 0800/0400 | Minneapolis Fed's Neel Kahkari | ||

| 28/05/2025 | 0800/1000 | ** | ECB Consumer Expectations Survey | |

| 28/05/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 28/05/2025 | 1255/0855 | ** | Redbook Retail Sales Index |