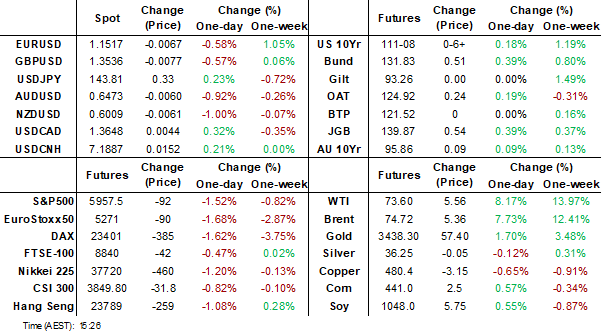

MNI EUROPEAN MARKETS ANALYSIS: USD Rebounds Amid Risk Off

- Oil prices surged as headlines crossed that Israel had launched strikes on Iran, including its nuclear facilities. We are off best levels, but still up 8% for the session. Israel has stated that the strikes will continue until its objectives are met. The US has stated it wasn't involved in the strikes while Iran has vowed to respond against both the US and Israel.

- US equity futures slumped, and US yields were lower as well. The USD has risen, with safe havens JPY and CHF initially outperforming, but those gains have been pared. Higher beta FX is weaker across the board.

- Looking ahead, focus will be on whether Middle East tensions escalate further. On the data front, we get final CPI reads for May in Germany and France. In the US, the June preliminary U. Of Mich. Sentiment reading prints.

MARKETS

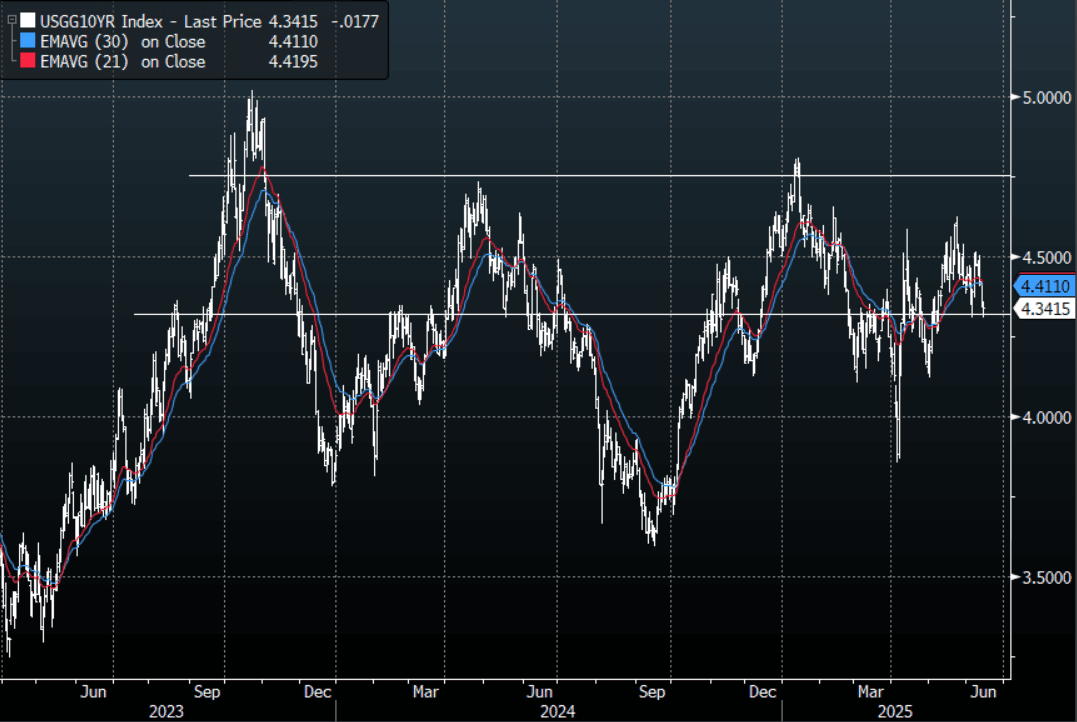

US TSYS: Asia Wrap - Yields Off Their Lows But Shorts Look Vulnerable

The TYU5 range has been 110-31 to 111-13 during the Asia-Pacific session. It last changed hands at 111-05, up 0-03 from the previous close.

- The US 2-year yield gapped lower, it is currently dealing back around 3.889%, down 0.02 from its close.

- The US 10-year yield moved sharply lower, it is trading back around 4.342%, down 0.02 from its close.

- (Bloomberg) - “"We struck at the heart of Iran's nuclear enrichment program. We struck at the heart of Iran's nuclear weaponization program. We targeted Iran's main enrichment facility in Natanz. We targeted Iran's leading nuclear scientists working on the nuclear bomb. We also struck at Iran's ballistic missile program," Netanyahu says in televised statement."

- Earlier remarks from US Secretary of State Rubio stated that Israel took unilateral action against Iran and that the US was not involved in the strikes. Rubio stated that Iran should not target US interests or personnel in the region (per BBG).

- The 10-year yield gapped lower on the cash open and tested its 4.30% support once more, this area needs to hold if yields are to move higher. A sustained break back below 4.30% and you would think more shorts will be pared back potentially putting a short-term top in place. Demand likely to be seen back to 4.40/45%

Data/Events: U. of Mich Survey

Fig 1: US-10 Year Yield Daily Chart

- Source: MNI - Market News/Bloomberg Finance L.P

ISRAEL: Netanyahu - Military Operation Will Continue Until Threat Removed

Headlines have crossed from Israel Prime Minister Netanyahu, who spoke about the military strikes being carried out on Iran.

- Netanyahu said that this was a decisive moment in Israel's history, and added the military operation will continue for as many days as it takes to remove the threat. It is targeting Iran's nuclear infrastructure, ballistic missile factories and military capabilities (per RTRS/BBG).

- It is also targeted Iran's main enrichment facility in Natanz, along with nuclear scientists working on the nuclear bomb program, Netanyahu added.

- Below is a quite via BBG:

- "“We struck at the heart of Iran’s nuclear enrichment program. We struck at the heart of Iran’s nuclear weaponization program. We targeted Iran’s main enrichment facility in Natanz. We targeted Iran’s leading nuclear scientists working on the nuclear bomb. We also struck at Iran’s ballistic missile program,” Netanyahu says in televised statement."

- Earlier remarks from US Secretary of State Rubio stated that Israel took unilateral action against Iran and that the US was not involved in the strikes. Rubio stated that Iran should not target US interests or personnel in the region (per BBG).

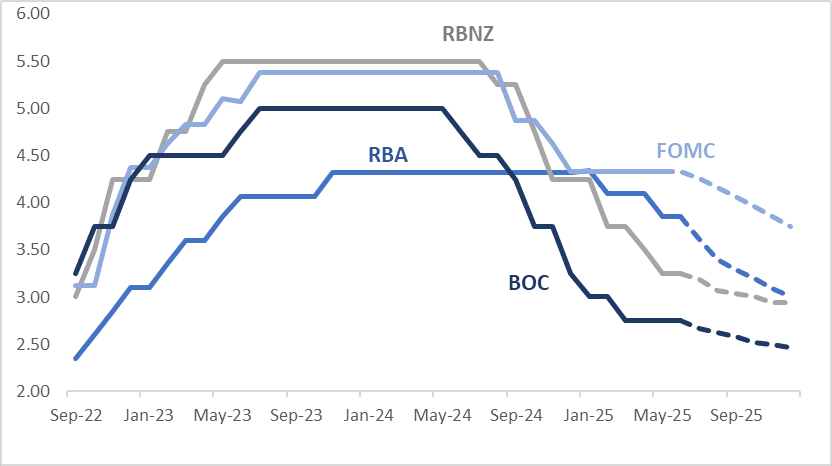

STIR: $-Bloc Markets Little Changed Over Past Week, Focus On FOMC

Interest rate expectations across dollar-bloc economies were broadly stable over the past week, with all markets showing net changes of less than 5bps through December 2025.

- The next key event for the region is the FOMC’s June 18 policy meeting, where a 25bp rate cut is currently given a ~2% probability.

- While Chair Powell refrained from commenting on monetary policy during the inter-meeting period, his FOMC colleagues spoke extensively—and consistently. Nearly all echoed the message that the Committee can and should remain patient in making upcoming rate decisions.

- They identified inflation as the more pressing dual-mandate risk, citing resilient economic activity and a solid labour market in recent "hard" data. However, they cautioned that the full impact of tariffs is likely to show up in inflation data over the summer, tempering the significance of recent disinflation trends—including, likely, the May CPI report. Although longer-term inflation expectations are still considered anchored, many participants voiced concern that this may not last.

- Looking ahead to December 2025, current market-implied policy rates and cumulative expected easing are as follows: US (FOMC): 3.75%, -58bps; Canada (BOC): 2.46%, -29bps; Australia (RBA): 3.01%, -84bps; and New Zealand (RBNZ): 2.94%, -31bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

JGBS: Richer With Global Bonds As Israel Strikes Iran

JGB futures (JBU5) are sharply stronger at 139.30, +48 compared to settlement levels, but well off session bests (138.80).

- News that Israel had conducted an airstrike in Iran earlier today sent global yields tumbling.

- Netanyahu said that this was a decisive moment in Israel's history, and added that the military operation will continue for as many days as it takes to remove the threat. (per RTRS/BBG).

- Iran stated that it will respond harshly against the US and Israel in response to the attacks.

- Cash US tsys are 1-3bps richer, with a steepening bias, in today's Asia-Pac session.

- The Bank of Japan (BoJ) is expected to keep its policy rate unchanged at 0.50% at its June 16–17 meeting, with focus turning to whether it will slow the pace of its JGB purchase reductions. The BoJ is likely to outline its bond-buying schedule through Q1 2027 to provide more transparency while maintaining flexibility. Markets see little risk of a rate hike at this meeting, with a projected policy rate of 0.60% by December.

- Cash JGBs are 2-5bps richer across benchmarks, with a flatter curve.

- Swap rates are flat to 6bps lower.

- The local calendar will be empty on Monday, ahead of the BoJ Policy Decision on Tuesday.

AUSSIE BONDS: Richer With Risk-Off After Israeli Strike On Iran

ACGBs (YM +5.0 & XM +6.5) are richer, but well off bests, after a major escalation in Middle East tensions after Israel launched strikes on Iranian nuclear facilities/military targets.

- Israel's comments suggest that military operations will continue until its objectives are met. Iran stated that it will respond harshly against the US and Israel in response to the attacks.

- "Iran Says to Respond 'Harshly' Against US, Israel Over Attacks. Iran's Armed Forces spokesperson Abolfazl Shekarchi says "the Zionist regime and the US will receive a harsh blow," in response to Israel's attacks earlier Friday. " - BBG.

- Cash US tsys are 1-2bps richer, but off session bests, in today’s Asia-Pac session.

- Cash ACGBs are 5-6bps richer with the AU-US 10-year yield differential at -17bps.

- The bills strip has bull-flattened, with pricing +3 to +5.

- RBA-dated OIS pricing is softer across meetings today. A 25bp rate cut in July is given a 87% probability, with a cumulative 80bps of easing priced by year-end.

- The local calendar will be empty on Monday.

- Next week, the AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond on Tuesday, A$900mn of the 2.75% 21 June 2035 bond on Wednesday and A$800mn of the 1.00% 21 December 2030 bond on Friday.

BONDS: NZGBS: Closed With A Bull-Flattener But Well Off Bests, Mid-East In Focus

NZGBs closed well off session bests but still showing a bull-flattener, with benchmark yields flat to 2bps lower. News that Israel had conducted an airstrike in Iran earlier today sent global yields tumbling. NZGBs were as much as 5-8bps richer early in the session.

- Netanyahu said that this was a decisive moment in Israel's history. It is targeting Iran's nuclear infrastructure, ballistic missile factories and military capabilities. (per RTRS/BBG).

- "Iran Says to Respond 'Harshly' Against US, Israel Over Attacks. Iran's Armed Forces spokesperson Abolfazl Shekarchi says "the Zionist regime and the US will receive a harsh blow," in response to Israel's attacks earlier Friday. " - BBG.

- Cash US tsys are 1-2bps richer, but off session bests, in today’s Asia-Pac session.

- NZGBs have underperformed its $-bloc counterparts with the NZ-US and NZ-AU 10-year yield differentials closing today’s session 4bps wider at +21bps and +38bps respectively.

- RBNZ nowcast estimate of New Zealand Q1 GDP growth is 0.63% - BBG

- Swap rates closed 3-4bps lower.

- RBNZ dated OIS pricing closed 2-3bps softer across meetings. 6bps of easing is priced for July, with a cumulative 30bps by November 2025.

- On Monday, the local calendar will see Performance Services Index data ahead of Food Prices on Tuesday.

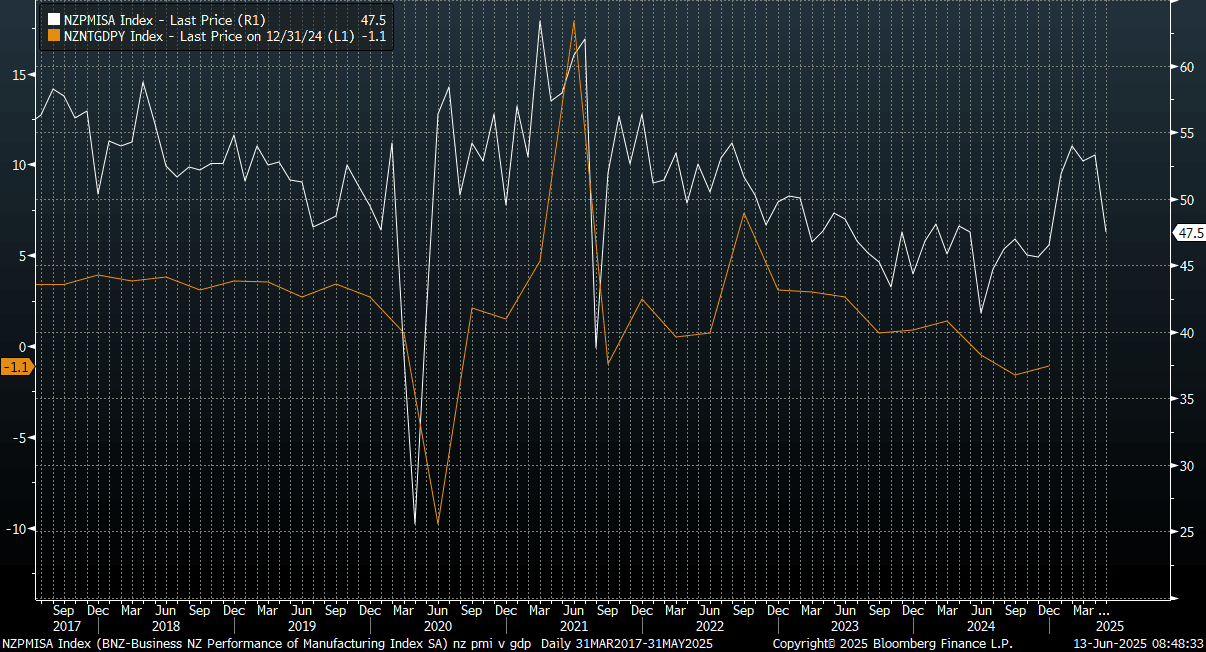

NEW ZEALAND: Manufacturing PMI Slumps In may, Giving Back 2025 Gains

New Zealand's BusinessNZ manufacturing PMI fell sharply in May to 47.5 from a revised 53.3 print for April. This largely unwinds all of the improvement seen in the first part of 2025. The index was at 46.5 in Dec 2024.

- Apart from finished stocks we saw all of the 5 sub indices fall below the 50.0 level, with new orders the weakest to 45.3 from 50.8. Employment fell to 45.7 from 54.6 in April.

- The chart below plots the PMI headline index against NZ GDP growth y/y. If this correction lower in the PMI persists then it suggests the NZ GDP rebound will be short lived. "PMI is yet another indicator that suggests an increased risk that the bounce in GDP in the six months through March “could come to a grinding halt”: BNZ senior economist Doug Steel" via BBG.

Fig 1: NZ BusinessNZ PMI Versus GDP Y/Y

Source: Bloomberg Finance L.P. /Business NZ/BNZ

FOREX: Asia FX Wrap - The USD Tries To Bounce, Can It Follow Through ?

The BBDXY has had a range of 1197.45 - 1204.41 in the Asia-Pac session, it is currently trading around 1203. "Iran Says to Respond ‘Harshly’ Against US, Israel Over Attacks. Iran’s Armed Forces spokesperson Abolfazl Shekarchi says “the Zionist regime and the US will receive a harsh blow,” in response to Israel’s attacks earlier Friday. " - BBG. How the USD trades on this news will be key to how we move forward from here, can it bounce with oil and as a safe haven ? If not what is that telling us ?

- EUR/USD - Asian range 1.1528 - 1.1614, Asia is currently trading 1.1520. EUR has rejected the move above 1.1600 in the Asian session as the USD bounces across the board. Dips should continue to find demand, first support around 1.1400 then the 1.1100/1200 area. EUR/USD looked to have broken the pivotal 1.1500 area overnight, this needs to be sustained to signal a larger move higher.

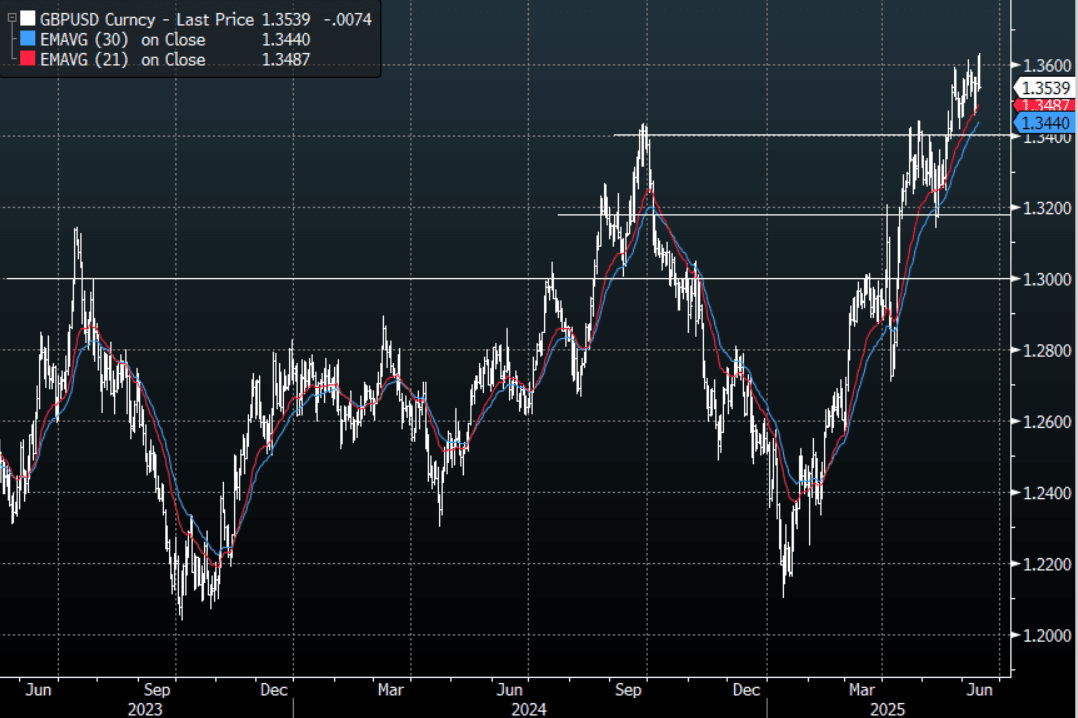

- GBP/USD - Asian range 1.3541 - 1.3632, Asia is currently dealing around 1.3530. The GBP like everything else has fallen pretty hard off its highs and once again looks to have failed to hold onto its momentum as it tries to sustain a break above its pivotal Weekly resistance. First support seen back towards 1.3400/50.

- USD/CNH - Asian range 7.1713 - 7.1859, the USD/CNY fix printed 7.1772. Asia is currently dealing around 7.1890. Sellers should be around on bounces while price holds below the 7.2500 area.

- Cross asset : SPX -1.67%, Gold $3428, US 10-Year 4.34%, BBDXY 1205, Crude oil $74.60

Data/Events :Ger CPI, Fra CPI, Spain CPI, Italy Trade Balance, EZ Trade Balance & Industrial Prod

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

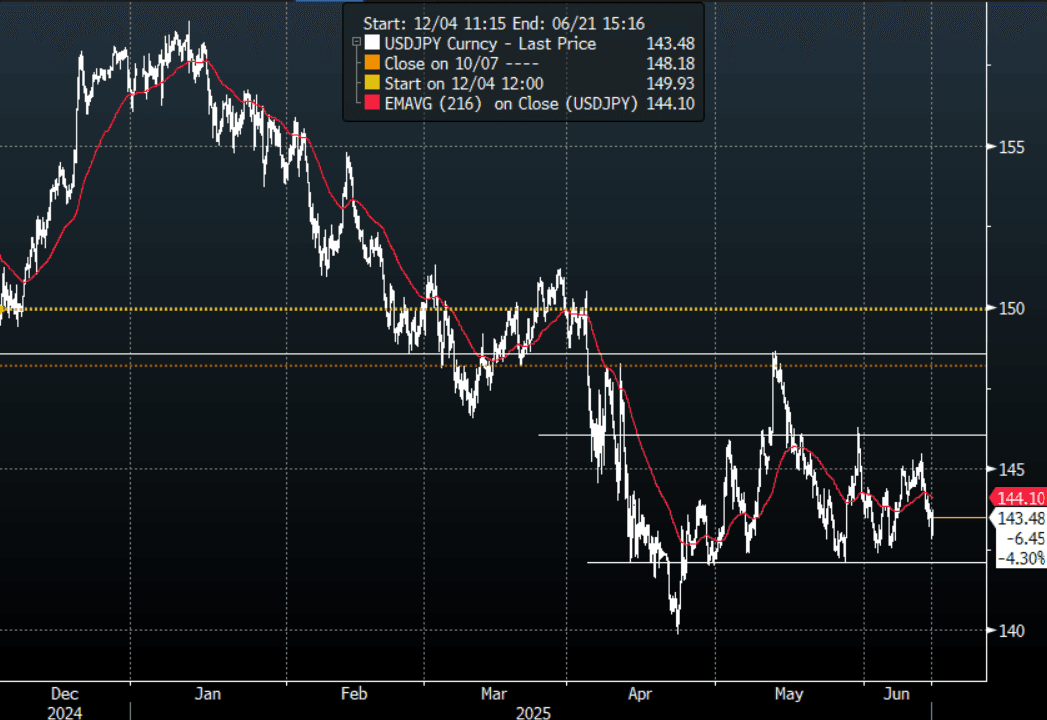

JPY: Asia Wrap - JPY Bought As A Safe Haven

The Asia-Pac USD/JPY range has been 142.80 - 144.14, Asia is currently trading around 143.50. USD/JPY was under pressure for most of the Asian session as US yields and Stocks both moved lower in response to Israel's attack on Iran. The JPY is normally sought out as a safe haven when risk begins to turn lower, the move in oil though could provide some headwinds for the move lower in USD/JPY but it does feel any bounces are going to be met with supply in the short-term. USD/JPY has bounced as we head into the London session clawing back all the day's losses.

- “Tokyo and Washington are still far apart, a Japanese opposition leader said.”(BBG)

- (Bloomberg) - “AKAZAWA: EXPECT BILATERAL DEAL TO SEPARATE JAPAN FROM OTHERS, NO CHANGE IN STANCE OF SEEKING REVIEW OF US TARIFFS”

- "KATO: IMPORTANT NOT TO LOSE MARKET TRUST IN JAPAN'S FINANCES, WANT TO PURSUE BOTH ECON REVITALIZATION AND FISCAL HEALTH, DIDN'T DISCUSS JAPAN'S TREASURIES HOLDINGS WITH BESSENT" - BBG

- With US yields under pressure and the risk backdrop badly souring the path of least resistance seems to be lower, I would expect decent supply again back towards 144.00/145.00 on the day.

- Price is back in its recent 142.00 - 147.00 range and will need a break either side of that to get a clearer direction. Price action does suggest 142.00 is likely to be tested first.

- The market still seems very confident of a move lower in USD/JPY but with positioning quite large now we have seen the risk of pullbacks increase.

Options : Close significant option expiries for NY cut, based on DTCC data: 144.00($1.46bm), 145.00($598m). Upcoming Close Strikes : 145.00($4.87b June 16).

Fig 1 : USD/JPY Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia Wrap - Risk Currencies Knee-Jerk Lower

The AUD/USD has had a range of 0.6457 - 0.6533 in the Asia- Pac session, it is currently trading around 0.6480. The AUD has been under large pressure for most of our session as the risk-on move unravels on the back of a wave of airstrikes currently being carried out on Iran. The knee-jerk move lower in risk currencies like the AUD and NZD was swift and has continued to trade heavy while risk looks like its correction could have more to play out.

- "Iran Says to Respond ‘Harshly’ Against US, Israel Over Attacks. Iran’s Armed Forces spokesperson Abolfazl Shekarchi says “the Zionist regime and the US will receive a harsh blow,” in response to Israel’s attacks earlier Friday. " - BBG

- The AUD/USD has capitulated back below the 0.6500 area just as it looked likely to break higher. The inability to break above 0.6550 on multiple occasions now will have some bulls a little concerned.

- Price back in the middle of the 0.6350 - 0.6550 range, a sustained break above 0.6550 is needed for the move higher to accelerate. How the USD trades on this news will be key to how we move forward from here, can it bounce with oil and as a safe haven ?

- Expect buyers to continue to be around on dips while the support in the AUD holds, a close back below 0.6350 is needed to challenge the newly formed uptrend. How far this correction in US stocks goes will determine the likelihood of this support holding.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6500(AUD450m). Upcoming Close Strikes : 0.6560(AUD 549m June 16), 0.6455(AUD426m June 16)

AUD/JPY - Today's range 92.32 - 93.83, it is trading currently around 92.95. Price has turned quickly lower again this morning as risk unravels. A clear lower high in place now and AUD/JPY looks set to test its support. A break back below 91.50/92.00 will see the move lower regain momentum and the focus will turn to the year's lows once more.

Fig 1: AUD/JPY spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

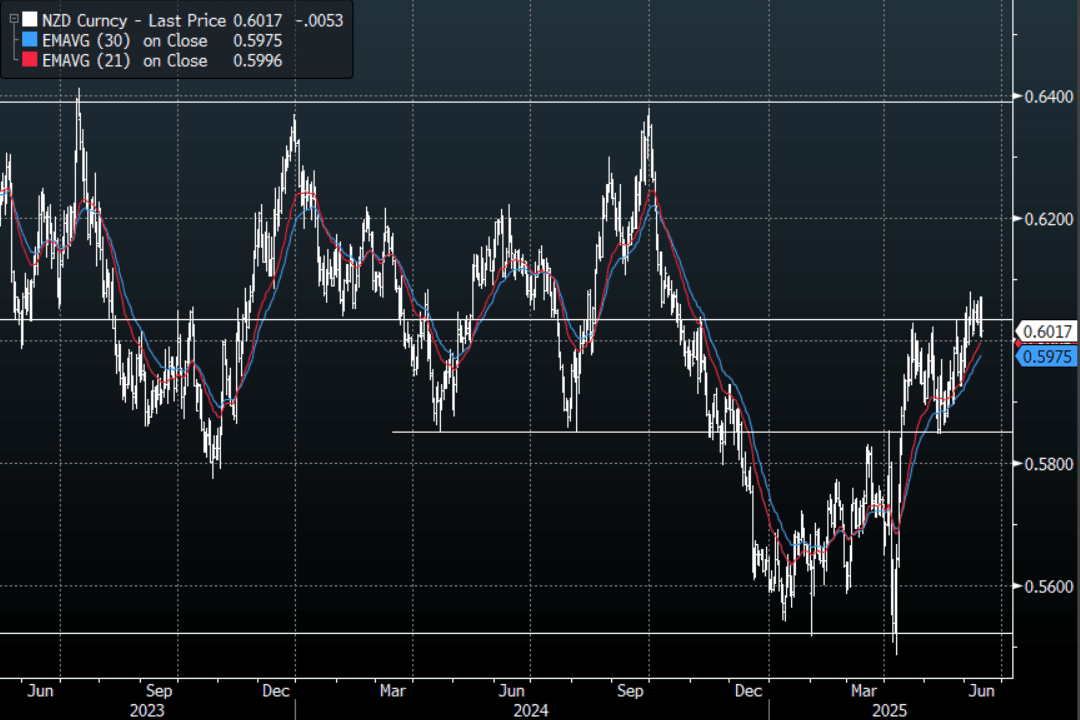

NZD: Asia Wrap - Can NZD/USD Hold Above 0.6000 With Risk Breaking Down

The NZD/USD had a range of 0.6004 - 0.6070 in the Asia-Pac session, going into the London open trading around 0.6020. The NZD has been under large pressure for most of our session as the risk-on move unravels on the back of a wave of airstrikes currently being carried out on Iran. The knee-jerk move lower in risk currencies like the AUD and NZD was swift and has continued to trade heavy while risk looks like its correction could have more to play out. The NZD is still trying hard to hold above its 0.6000 support, if risk falls further can it continue to do so ?

- '*RBNZ NOWCAST ESTIMATE OF NEW ZEALAND 1Q GDP GROWTH IS 0.63%" - BBG

- Manufacturing PMI Slumps In May, Giving Back 2025 Gains : New Zealand's BusinessNZ manufacturing PMI fell sharply in May to 47.5 from a revised 53.3 print for April. This largely unwinds all of the improvement seen in the first part of 2025. The index was at 46.5 in Dec 2024.

- The NZD’s inability to accelerate above 0.6050 could see the move higher stall in the short term, first support is seen back towards the 0.5950 area. How the USD trades on this news will be key to how we move forward from here, can it bounce with oil and as a safe haven ? If not what is that telling us.

- While the support around 0.5850 holds there should be buyers around on dips. A clear break above 0.6050/0.6100 is needed to provide the spark for the next leg higher.

AUD/NZD range for the session has been 1.0746 - 1.0774, currently trading 1.0770. A top looks in place now just above 1.0900, the cross topped out on Monday towards the 1.0800/25 sell area, the first target looks to be around 1.0650.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Risk Off Post Israel Strikes On Iran Weighs On Sentiment

Asia equities are down across the board (except for the Philippines), as risk aversion has spiked following Israel attacks on Iran (including nuclear facilities), in a major escalation of Middle East tensions. US equity futures are down sharply, albeit up slightly from session lows in latest dealings.

- US Nasdaq futures were off 2% at one stage, but sit down around 1.8% in latest dealings. Eminis were last off 1.6%, with the index back under 6000. The simple 200-day MA is back at 5900.

- The US stated it wasn't involved in the attacks, but Iran stated it will respond harshly against both the US, Israel over the attacks. Oil prices for WTI were up close to $10/bbl at one stage but has settled someone since.

- In Asia Pac equities, Japan markets are off around 1%, while at the break Hong Kong and China markets are down 0.70-0.75%. India markets are down a little over 1% in the first part of trade, with oil sensitivity in play.

- South Korea is marginally the worst performer, off over 1.2%, giving back some of the recent outperformance. The Kosdaq has slumped over 3% though.

- Losses are mostly more modest elsewhere, while Philippines markets are bucking the softer trend, up close to 0.45%.

OIL: Benchmarks Surge As Israel Attacks Iran

Oil benchmarks sit sharply higher as markets digest the major escalation in Middle East tensions/conflicts after Israel launched strikes on Iran nuclear facilities/military targets (including Iranian Military personnel). Israel comments suggest that military operations will continue until its objectives are met, while focus is also on Iran's response. The country stated it will respond harshly against the US and Israel in response to the attacks.

- Iran reported that there was no damage to its oil refineries or storage tanks (per BBG). Trump stated that he still hopes that Iran comes to the negotiation table.

- After opening around $69/bbl, WTI got as highs at $77.62/bbl. We sit slightly lower now, last near $74.5/bbl, still up for 9.4% for the session. Brent was last near $75.6/bbl after earlier highs of $78.50/bbl were reached. Brent is up close to 10% so far today. For the week, Brent is tracking 14.50% firmer. WTI is up over 15% for the week. If sustained,

- Earlier Zerohedge noted the short CTA positioning in oil (via BoFA), which may have exacerbated today's surge.

- For WTI, mid Jan highs were around $80.75-80/bbl, which could be an upside target on further gains for the benchmark.

GOLD: Pushing Towards New High After Israeli Airstrike On Iran

Gold is 1.3% higher at 3428 in today’s Asia-Pac session, with risk off following Israel's strike on Iran fuelling bullion demand.

- Netanyahu said that this was a decisive moment in Israel's history and added that the military operation will continue for as many days as it takes to remove the threat. It is targeting Iran's nuclear infrastructure, ballistic missile factories and military capabilities (per RTRS/BBG).

- It is also targeting Iran's main enrichment facility in Natanz, along with nuclear scientists working on the nuclear bomb program, Netanyahu added.

- Earlier remarks from US Secretary of State Rubio stated that Israel took unilateral action against Iran and that the US was not involved in the strikes. Rubio stated that Iran should not target US interests or personnel in the region (per BBG).

- According to MNI’s technicals team, suggests the following as upside levels to be mindful of: RES 2: $3435.6/3500.1 - High May 7 / High Apr 22 and bull trigger / RES 3: $3547.9 - 1.764 proj of the Feb 28 - Apr 3 - Apr 7 price swing / RES 4: $3578.0 - 2.000 proj of the Dec 19 - Feb 24 - Feb 28 swing.

ASIA FX: KRW Bears To Brunt Off Risk Off, TWD Outperforms

In North East Asia FX, the USD is firmer, particularly against KRW, as markets are gripped by risk off following Israel strikes on Iran (including its nuclear facilities). TWD is outperforming, making fresh multi year highs in the first part of trade.

- USD/KRW spot has surged nearly 1% higher, virtually unwinding all of Thursday's won gains. The pair was last near 1370. Earlier highs this week were close to 1375, while recent lows rest around the 1351 level. We have seen South Korean equities retrace lower, with the Kospi off a little over 1%, while the Kosdaq has fallen over 3%. The won is sensitive to broader risk shifts, while the spike in oil is a terms of trade headwind if it is sustained.

- USD/TWD traded to lows of 29.50 in the first part of Friday dealing, continuing Thursday's better TWD trend. These were levels last seen in 2022. USD/TWD has recovered some ground since, last back to 29.60/65, only 0.10% stronger in TWD terms. It was reported earlier that Taiwan will measures to encourage insurers to invest more domestically (see this BBG link).

- USD/CNH has pushed higher, albeit only up 0.15% versus end Thursday levels in the US. We were last close to 7.1850, with CNH seeing some negative spillover from USD gains elsewhere. Earlier USD/CNH opened closer to 7.1700.

- Spot USD/HKD is little changed, last close to 7.8490.

ASIA FX: THB Outperforms With Gold Surge, Oil Sensitive Plays Weaker

In South East FX markets, the USD is higher across the board, albeit to varying degrees. THB is outperforming, little changed at this stage versus end Thursday levels. PHP is down around 0.40%, while in India, spot INR is off 0.60%, with higher oil prices a factor. MYR is also down though, which tends to have a positive terms of trade relationship with higher oil prices. Equity markets in the region are all weaker, except for the Philippines.

- USD/THB got to lows of 32.33 earlier, but we sit back in the 32.45/50 region now. The spike in gold prices (+1.3%) on market risk aversion in response to the Israel attacks on Iran, has likely help baht outperform.

- USD/INR is up 0.60%, last close to 86.10. This is fresh highs in the pair back to mid April. Sensitivity to the oil price spike (Brent last up around 9.3%) a little factor.

- USD/SGD is modestly higher, close to 1.2820, so outperforming some other trends in the region and higher beta FX like AUD and NZD.

- USD/IDR is back close to 16300, off around 0.4% in IDR terms. USD/PHP has pushed back above 56.00, last close to 56.15, off around 0.50% for the session. The oil price spill could be in play as well for PHP.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 13/06/2025 | 0600/0800 | *** | Final Inflation Report | |

| 13/06/2025 | 0600/0800 | *** | HICP (f) | |

| 13/06/2025 | 0645/0845 | *** | HICP (f) | |

| 13/06/2025 | 0700/0900 | *** | HICP (f) | |

| 13/06/2025 | 0830/0930 | ** | Bank of England/Ipsos Inflation Attitudes Survey | |

| 13/06/2025 | 0900/1100 | ** | Industrial Production | |

| 13/06/2025 | 0900/1100 | * | Trade Balance | |

| 13/06/2025 | - | *** | Money Supply | |

| 13/06/2025 | - | *** | New Loans | |

| 13/06/2025 | - | *** | Social Financing | |

| 13/06/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 13/06/2025 | 1230/0830 | ** | Wholesale Trade | |

| 13/06/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 13/06/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 13/06/2025 | 1500/1700 | ECB Elderson At Senior Supervisor's Conference | ||

| 13/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 13/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |