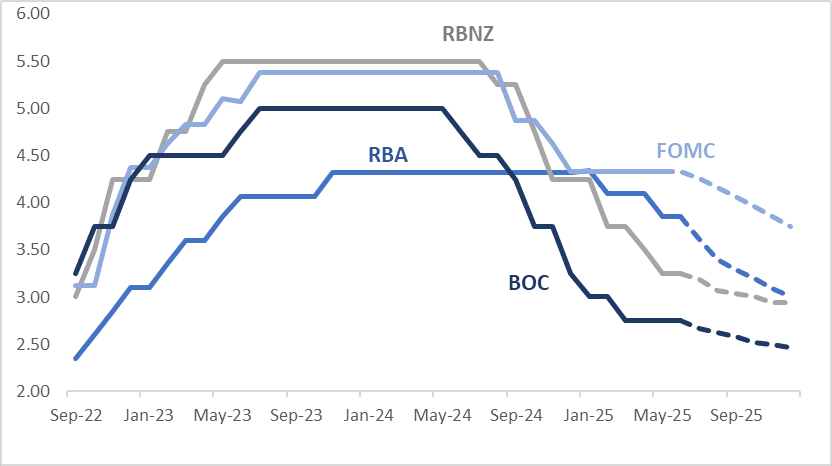

STIR: $-Bloc Markets Little Changed Over Past Week, Focus On FOMC

Jun-13 03:43

Interest rate expectations across dollar-bloc economies were broadly stable over the past week, with all markets showing net changes of less than 5bps through December 2025.

- The next key event for the region is the FOMC’s June 18 policy meeting, where a 25bp rate cut is currently given a ~2% probability.

- While Chair Powell refrained from commenting on monetary policy during the inter-meeting period, his FOMC colleagues spoke extensively—and consistently. Nearly all echoed the message that the Committee can and should remain patient in making upcoming rate decisions.

- They identified inflation as the more pressing dual-mandate risk, citing resilient economic activity and a solid labour market in recent "hard" data. However, they cautioned that the full impact of tariffs is likely to show up in inflation data over the summer, tempering the significance of recent disinflation trends—including, likely, the May CPI report. Although longer-term inflation expectations are still considered anchored, many participants voiced concern that this may not last.

- Looking ahead to December 2025, current market-implied policy rates and cumulative expected easing are as follows: US (FOMC): 3.75%, -58bps; Canada (BOC): 2.46%, -29bps; Australia (RBA): 3.01%, -84bps; and New Zealand (RBNZ): 2.94%, -31bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: RBNZ Dated OIS Pricing Firms Since CPI But Much Less Than AUS

May-14 03:42

RBNZ-dated OIS pricing is flat to 3bps firmer across meetings today, leaving rates 2–14bps above levels seen prior to the Q1 CPI release on April 17.

- Q1 New Zealand CPI came in hotter than expected at 0.9% q/q, lifting the annual rate to 2.5% from 2.2% in Q4. Both tradeables and non-tradeables components contributed to the upside surprise.

- However, the RBNZ’s preferred measure of underlying inflation—the sectoral factor model—edged lower to 2.9% in Q1, down from a downwardly revised 3.0% in Q4. This marks the lowest print since Q2 2021 and places core inflation just under the top of the RBNZ’s 1–3% target band.

- In Australia, Q1 headline and underlying CPI exceeded expectations by 0.1pp, although the trimmed mean slowed to 2.9% y/y, falling within the RBA’s target band for the first time since Q4 2021.

- For comparison, RBA-dated OIS pricing is now 4–40bps firmer than pre-Q1 CPI levels recorded on April 30.

Figure 1: RBNZ Dated OIS Current vs. Pre-CPI Levels (%)

Source: MNI - Market News / Bloomberg

CHINA: Bond Futures Lower in Morning Trade

May-14 03:04

- China's bond futures are all lower in morning trading.

- The 10YR future is lower by -0.10 at 108.56 and has breached the 50-day EMA of 108.59. The next key level below is the 100-day EMA of 108.32.

- The 2YR future is lower by -0.05 at 102.46 and remains firmly below all major moving averages. The nearest being the 20-day EMA at 102.46.

- CGB bond yields are stable with the CGB 10YR at 1.66%

MNI EXCLUSIVE: Insight On German FDI Into CHina

May-14 02:52

A leading German industry leader in China provides insight into German FDI. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.