STIR: Limited Reaction In EUR STIRs To Slightly Firm German State Prints

Limited reaction in EUR STIRs to the German state-level CPI data, even as our initial read points to slight upside risks to the national CPI consensus of 0.2% M/M (due 1300BST today). If realised, this would come alongside higher-than-expected readings in both Spain and France, suggesting upside risks to the 1.9% Y/Y Eurozone-wide consensus (vs 2.0% prior).

- The bias for Euribor futures has been tilted to the downside throughout this morning, following the hawkish leaning Fed decision yesterday evening.

- ECB-dated OIS now price ~12bps of easing through year-end, with 17bps of cuts priced through March 2026.

- The median analyst still leans in favour of one more 25bp cut this cycle, but a substantial minority look for the deposit rate to be held at 2.00% going forward.

| Meeting Date | ESTR ECB-Dated OIS (%) | Difference Vs. Current Effective ESTR Rate (bp) |

| Sep-25 | 1.901 | -2.3 |

| Oct-25 | 1.869 | -5.5 |

| Dec-25 | 1.802 | -12.2 |

| Feb-26 | 1.786 | -13.8 |

| Mar-26 | 1.756 | -16.8 |

| Apr-26 | 1.759 | -16.5 |

| Jun-26 | 1.764 | -16.0 |

| Jul-26 | 1.769 | -15.5 |

| Source: MNI/Bloomberg Finance L.P. | ||

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ITALY DATA: Weaker Than Expected June Manuf PMI; New Orders Down As In Spain

In contrast to Spain, the Italian manufacturing PMI was weaker-than-expected at 48.4 (vs 49.5 cons, 49.2 prior). The index has now been in contractionary territory for 15 consecutive months. However, as in Spain, it was another report that flagged weakness in export orders alongside reductions in output charges.

Key notes from the release:

- "Italian goods producers stated that a sustained decline in new orders led them to reduce their production levels"..."Global economic uncertainty and muted customer demand hampered new sales intakes, according to manufacturers. The solid fall in total new work was weighed down by a renewed decrease in new export orders in June. New sales from abroad fell as firms noted difficulties reaching out to new clients and weakness in demand conditions in existing markets".

- "June data indicated a second successive monthly decrease in input costs faced by Italian manufacturers"..."In line with lower costs and in a bid to boost new sales, Italian goods producers lowered their output charges at the end of the second quarter".

- "Manufacturers remained in retrenchment mode during June, as they reduced headcounts and lowered input buying".

- "Input buying, meanwhile, decreased at a solid pace. Despite weaker demand for inputs, supplier performance deteriorated for the first time in three months, amid logistics delays and vendor shortages".

CROSS ASSET: Best traded Volumes went through in Bonds, USDJPY tests 143.00

- Best traded volumes for Bund on that earlier extension from 130.50 all the way up to 130.73, 31.5k lots went through during that 5 minutes window.

- The initial gradual demand was seen in the longer end US Treasuries some 45 minutes ago, helping the 10yr Yield towards that 4.1942% support, for now printed a 4.1871% low.

- The next resistance in Bund noted at 130.80 has held, printed a 130.73 high.

- US Tnotes is seeing some selling interest at the top of its range in Futures, at that low Yield level.

- Regardless for FX, USDJPY is eyeing a break through 143.00 now, so far printed

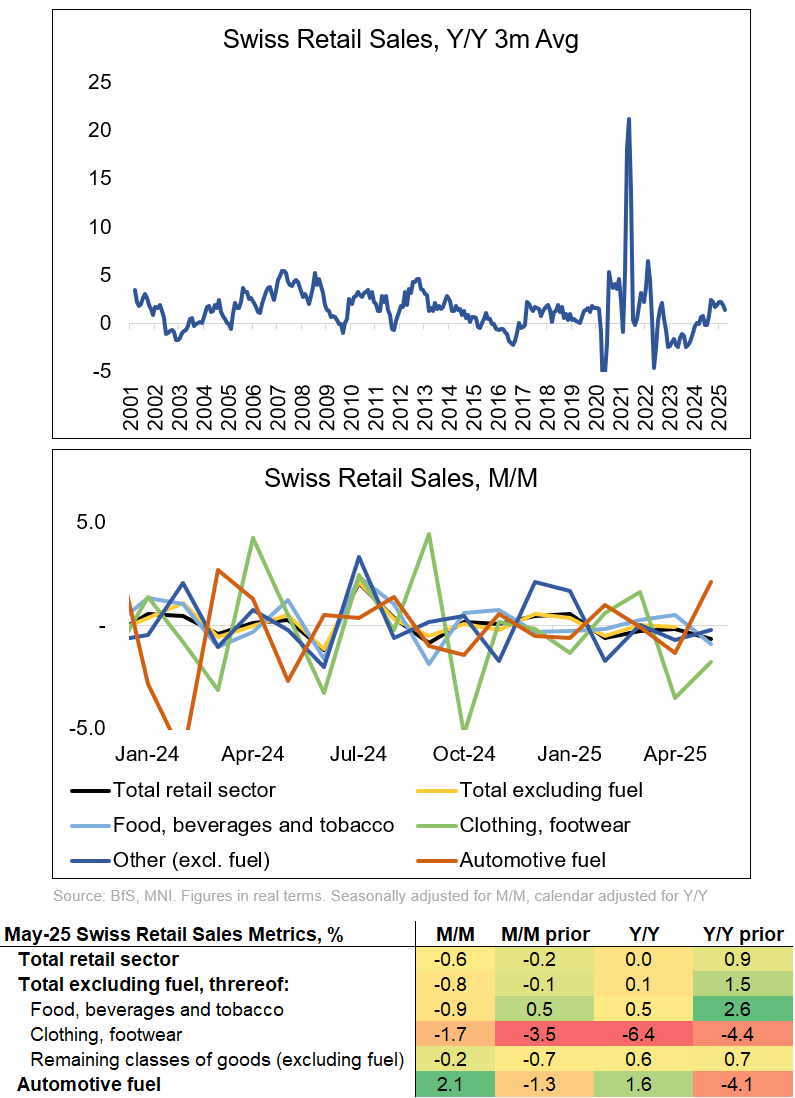

SWITZERLAND DATA: Weak May Retail Sales Likely Of Limited SNB Concern

Swiss (real) retail sales were weak in May, at -0.6% M/M, the joint lowest sequential reading in the series since September 2024.

- The data is another indication that the SNB's call for softer Swiss economic momentum towards Q2 materializes (following yesterday's June KOF underperformance at 96.1 vs 99.3 consensus). Remember that the SNB sees 1.0-1.5% growth in 2025 - even though Q1 already printed a strong 0.8% Q/Q.

- Nevertheless, we'd argue the SNB's main concern when considering a move into negative rates territory would be inflation dynamics, not economic activity.

Petrol station / fuel sales were strong in May - the print excl. that printed -0.8% M/M, and all remaining main subcategories printed negatively on a sequential comparison. See table for details.