US TSYS: Asia Wrap - Yields Off Their Lows But Shorts Look Vulnerable

Jun-13 04:02

The TYU5 range has been 110-31 to 111-13 during the Asia-Pacific session. It last changed hands at 111-05, up 0-03 from the previous close.

- The US 2-year yield gapped lower, it is currently dealing back around 3.889%, down 0.02 from its close.

- The US 10-year yield moved sharply lower, it is trading back around 4.342%, down 0.02 from its close.

- (Bloomberg) - “"We struck at the heart of Iran's nuclear enrichment program. We struck at the heart of Iran's nuclear weaponization program. We targeted Iran's main enrichment facility in Natanz. We targeted Iran's leading nuclear scientists working on the nuclear bomb. We also struck at Iran's ballistic missile program," Netanyahu says in televised statement."

- Earlier remarks from US Secretary of State Rubio stated that Israel took unilateral action against Iran and that the US was not involved in the strikes. Rubio stated that Iran should not target US interests or personnel in the region (per BBG).

- The 10-year yield gapped lower on the cash open and tested its 4.30% support once more, this area needs to hold if yields are to move higher. A sustained break back below 4.30% and you would think more shorts will be pared back potentially putting a short-term top in place. Demand likely to be seen back to 4.40/45%

Data/Events: U. of Mich Survey

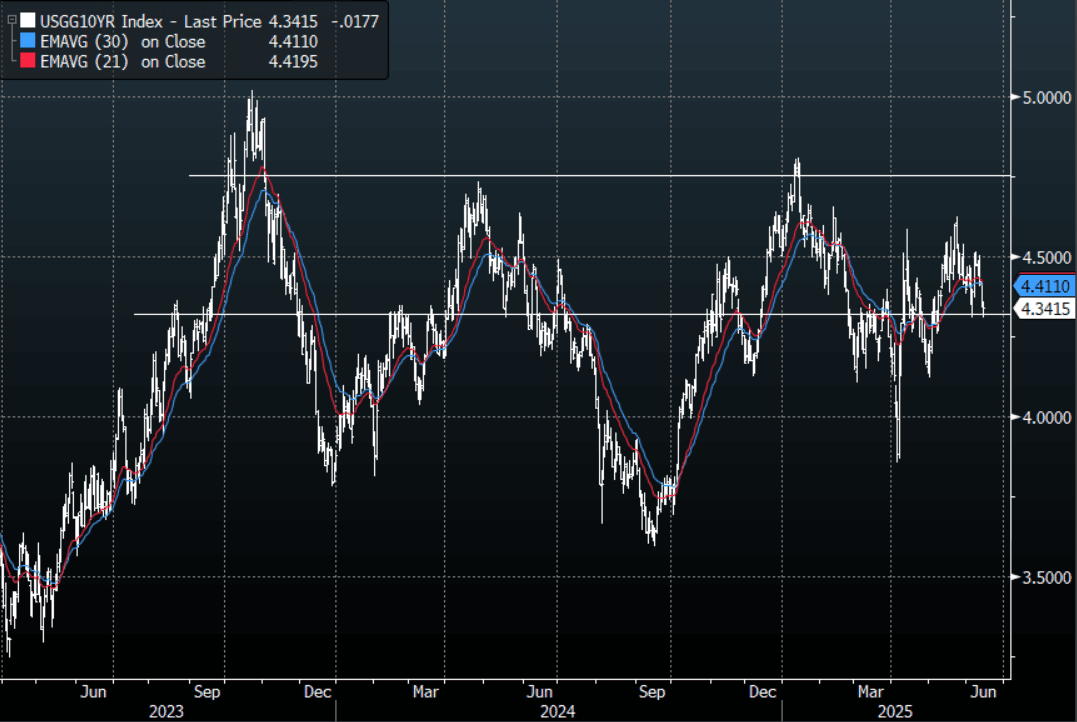

Fig 1: US-10 Year Yield Daily Chart

- Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: RBNZ Dated OIS Pricing Firms Since CPI But Much Less Than AUS

May-14 03:42

RBNZ-dated OIS pricing is flat to 3bps firmer across meetings today, leaving rates 2–14bps above levels seen prior to the Q1 CPI release on April 17.

- Q1 New Zealand CPI came in hotter than expected at 0.9% q/q, lifting the annual rate to 2.5% from 2.2% in Q4. Both tradeables and non-tradeables components contributed to the upside surprise.

- However, the RBNZ’s preferred measure of underlying inflation—the sectoral factor model—edged lower to 2.9% in Q1, down from a downwardly revised 3.0% in Q4. This marks the lowest print since Q2 2021 and places core inflation just under the top of the RBNZ’s 1–3% target band.

- In Australia, Q1 headline and underlying CPI exceeded expectations by 0.1pp, although the trimmed mean slowed to 2.9% y/y, falling within the RBA’s target band for the first time since Q4 2021.

- For comparison, RBA-dated OIS pricing is now 4–40bps firmer than pre-Q1 CPI levels recorded on April 30.

Figure 1: RBNZ Dated OIS Current vs. Pre-CPI Levels (%)

Source: MNI - Market News / Bloomberg

CHINA: Bond Futures Lower in Morning Trade

May-14 03:04

- China's bond futures are all lower in morning trading.

- The 10YR future is lower by -0.10 at 108.56 and has breached the 50-day EMA of 108.59. The next key level below is the 100-day EMA of 108.32.

- The 2YR future is lower by -0.05 at 102.46 and remains firmly below all major moving averages. The nearest being the 20-day EMA at 102.46.

- CGB bond yields are stable with the CGB 10YR at 1.66%

MNI EXCLUSIVE: Insight On German FDI Into CHina

May-14 02:52

A leading German industry leader in China provides insight into German FDI. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.