JPY: Asia Wrap - JPY Bought As A Safe Haven

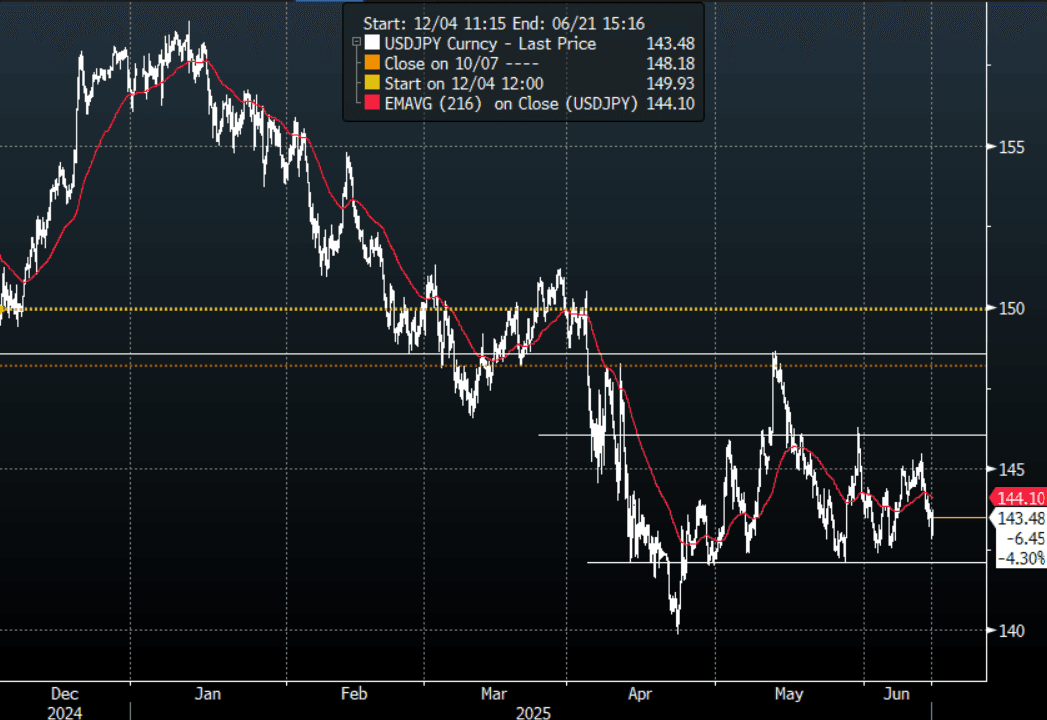

The Asia-Pac USD/JPY range has been 142.80 - 144.14, Asia is currently trading around 143.50. USD/JPY was under pressure for most of the Asian session as US yields and Stocks both moved lower in response to Israel's attack on Iran. The JPY is normally sought out as a safe haven when risk begins to turn lower, the move in oil though could provide some headwinds for the move lower in USD/JPY but it does feel any bounces are going to be met with supply in the short-term. USD/JPY has bounced as we head into the London session clawing back all the day's losses.

- “Tokyo and Washington are still far apart, a Japanese opposition leader said.”(BBG)

- (Bloomberg) - “AKAZAWA: EXPECT BILATERAL DEAL TO SEPARATE JAPAN FROM OTHERS, NO CHANGE IN STANCE OF SEEKING REVIEW OF US TARIFFS”

- "KATO: IMPORTANT NOT TO LOSE MARKET TRUST IN JAPAN'S FINANCES, WANT TO PURSUE BOTH ECON REVITALIZATION AND FISCAL HEALTH, DIDN'T DISCUSS JAPAN'S TREASURIES HOLDINGS WITH BESSENT" - BBG

- With US yields under pressure and the risk backdrop badly souring the path of least resistance seems to be lower, I would expect decent supply again back towards 144.00/145.00 on the day.

- Price is back in its recent 142.00 - 147.00 range and will need a break either side of that to get a clearer direction. Price action does suggest 142.00 is likely to be tested first.

- The market still seems very confident of a move lower in USD/JPY but with positioning quite large now we have seen the risk of pullbacks increase.

Options : Close significant option expiries for NY cut, based on DTCC data: 144.00($1.46bm), 145.00($598m). Upcoming Close Strikes : 145.00($4.87b June 16).

Fig 1 : USD/JPY Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: RBNZ Dated OIS Pricing Firms Since CPI But Much Less Than AUS

RBNZ-dated OIS pricing is flat to 3bps firmer across meetings today, leaving rates 2–14bps above levels seen prior to the Q1 CPI release on April 17.

- Q1 New Zealand CPI came in hotter than expected at 0.9% q/q, lifting the annual rate to 2.5% from 2.2% in Q4. Both tradeables and non-tradeables components contributed to the upside surprise.

- However, the RBNZ’s preferred measure of underlying inflation—the sectoral factor model—edged lower to 2.9% in Q1, down from a downwardly revised 3.0% in Q4. This marks the lowest print since Q2 2021 and places core inflation just under the top of the RBNZ’s 1–3% target band.

- In Australia, Q1 headline and underlying CPI exceeded expectations by 0.1pp, although the trimmed mean slowed to 2.9% y/y, falling within the RBA’s target band for the first time since Q4 2021.

- For comparison, RBA-dated OIS pricing is now 4–40bps firmer than pre-Q1 CPI levels recorded on April 30.

Figure 1: RBNZ Dated OIS Current vs. Pre-CPI Levels (%)

Source: MNI - Market News / Bloomberg

CHINA: Bond Futures Lower in Morning Trade

- China's bond futures are all lower in morning trading.

- The 10YR future is lower by -0.10 at 108.56 and has breached the 50-day EMA of 108.59. The next key level below is the 100-day EMA of 108.32.

- The 2YR future is lower by -0.05 at 102.46 and remains firmly below all major moving averages. The nearest being the 20-day EMA at 102.46.

- CGB bond yields are stable with the CGB 10YR at 1.66%

MNI EXCLUSIVE: Insight On German FDI Into CHina