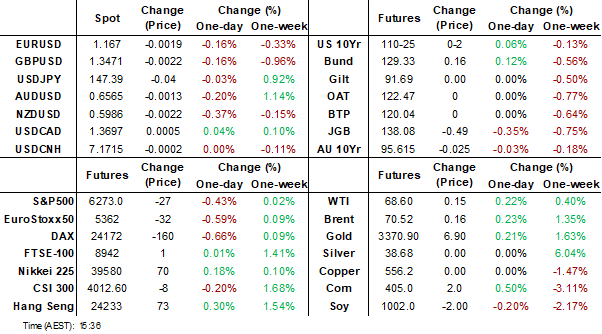

MNI EUROPEAN MARKETS ANALYSIS: USD Firmer Amid Equity Softness

- US and EU equity futures are weaker, following the weekend news of Trump's 30% tariff threat versus the EU. There have also been reports that Trump will increase support to Ukraine, including providing offensive weapons. Oil prices haven't reacted much though.

- China trade figures were slightly firmer than forecast in June, but market reaction has been limited. Japan core machine orders eased in y/y terms, but still painted a resilient Capex backdrop.

- The USD is trading higher, particularly against higher beta plays.

Source: Bloomberg Finance L.P./MNI

MARKETS

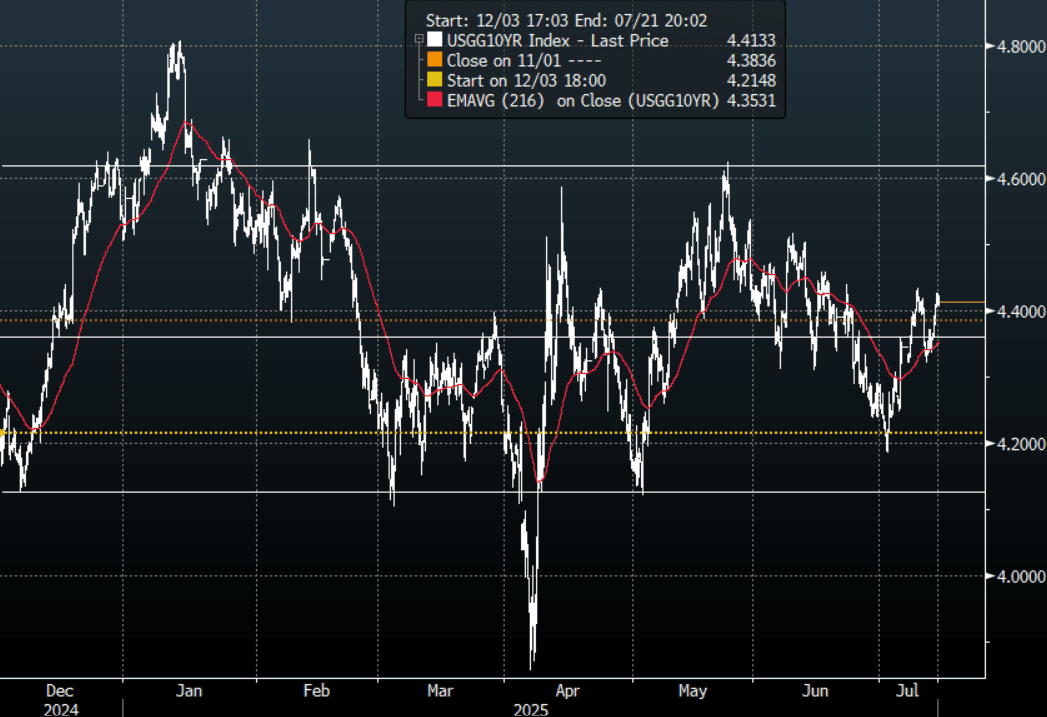

US TSYS: Asia Wrap - Quiet Session For US Bonds

The TYU5 range has been 110-24+ to 110-28 during the Asia-Pacific session. It last changed hands at 110-27, up 0-04 from the previous close.

- The US 2-year yield has edged lower trading around 3.88%

- The US 10-year yield has edged higher trading around 4.413%.

- The 10-year yield is again testing the 4.40/45% pivot within its wider 4.10% - 4.65% range. The market is clearly worried about inflation and the CPI this week will be a critical input into the market's thinking. A sustained close back above the 4.45% area could see more longs pared back, above here and the focus will turn back to the 4.60% area.

- Nick Timiraos on X: “Penn’s Peter Conti-Brown: “We are in a high-stakes moment in the history of the Federal Reserve. It seems clear to me that the Trump administration, using various mechanisms, [has] now cooked up a post-hoc explanation for Powell’s removal.”

- "TRUMP: IF POWELL TO STEP DOWN WOULD BE A GOOD THING" - BBG

- MNI BRIEF: US Budget Surplus $27B In June; YTD Deficit $1.3T. The U.S. government posted a USD27 billion budget surplus for June, up USD98 billion from a year earlier, reflecting strong tax receipts and collections of import duties, the Treasury Department said Monday.

Fig 1: 10-Year US Yield Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Bear-Steepening As Upper House Elections Approach

JGB futures are sharply weaker and hovering near session lows, -46 compared to settlement levels.

- (Bloomberg) " The Bank of Japan finished selling millions of dollars of stocks it bought from besieged banks, ending a nearly two decade process. The BOJ's holdings of the shares purchased from banks hit zero as of July 10, falling from 2.5 billion 10 days ago, according to its balance sheet report."

- "JAPAN RULING BLOC MAY LOSE MAJORITY IN ELECTION: JNN ANALYSIS" – BBG

- Cash US tsys are slightly cheaper, with a steepening bias, in today's Asia-Pac session after Friday's bear-steepener.

- Cash JGBs are flat to 4bps cheaper across benchmarks, with the 20-year leading. The benchmark 10-year yield is 6.4bps higher at 2.578% versus the cycle high of 2.605%.

- Swap rates are flat to 6bps higher, with a steeper curve. Swap spreads are tighter out to the 20-year and wider beyond.

- Tomorrow, the local calendar will be empty apart from 5-year Climate Transition supply.

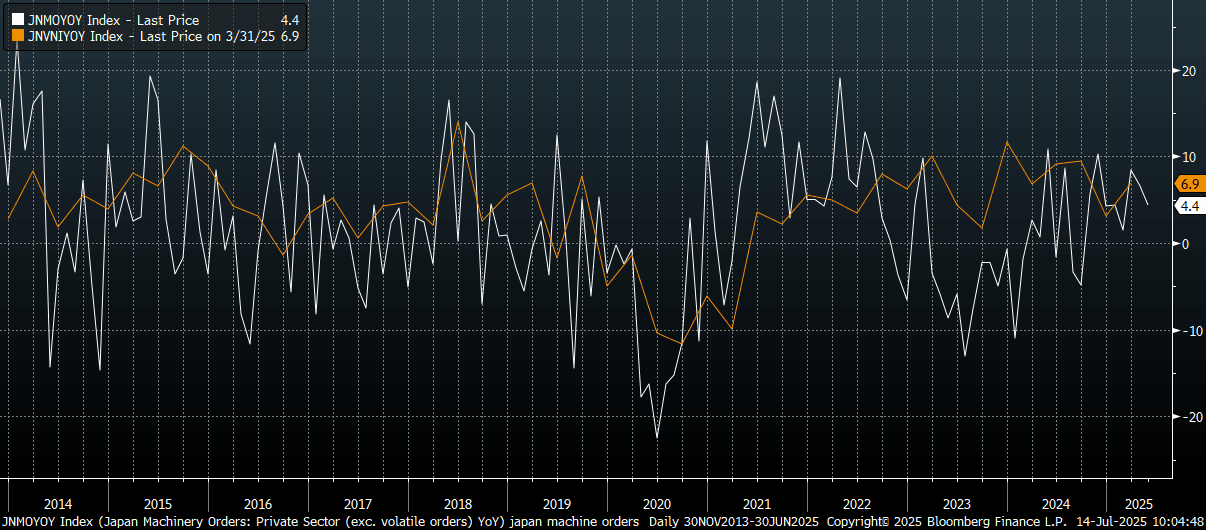

JAPAN DATA: Core Machine Orders Y/Y Slows, But Still Pointing To Resilient Capex

Japan May machine orders were slightly above market forecasts in m/m terms. We printed at -0.6%m/m, versus the -1.5% forecast. The April fall of -9.1% was unrevised. In y/y terms we were slightly below forecasts, printing 4.4%, versus 5.2% expected, while 6.6% was the May outcome.

- The chart below plots core machine orders, in y/y terms, against Japan quarterly capex (also in y/y terms). It implies some softer Capex momentum risks all else equal, but still positive growth.

- Looking at the detail, manufacturing orders fell by 1.8%m/m (after a 0.6% dip in April). Non-manufacturing surged by 30.4%m/m though, to provide some offset.

Fig 1: Japan Core Machine Orders & Capex (Y/Y)

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Slightly Cheaper, Narrow Ranges, Jun-54 Supply Tomorrow

ACGBs (YM -2.0 & XM -2.0) sit weaker after dealing in narrow ranges in today’s Sydney session.

- Cash US tsys are slightly cheaper, with a steepening bias, in today's Asia-Pac session after Friday's bear-steepener.

- Cash ACGBs are 2-3bps cheaper with the AU-US 10-year yield differential at -6bps. At -6bps, the differential is positioned near the middle of the +/- 30bps range that has held since November 2022.

- The bills strip is slightly cheaper, with pricing -1 to -3.

- RBA-dated OIS pricing is slightly firmer across meetings today. A 25bp rate cut in August is given an 88% probability, with a cumulative 59bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- Tomorrow, the local calendar will see Westpac Consumer Confidence.

- This week, the AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond tomorrow, A$800mn of the 4.25% 21 March 2036 bond on Wednesday and A$1100mn of the 1.00% 21 November 2031 bond on Friday.

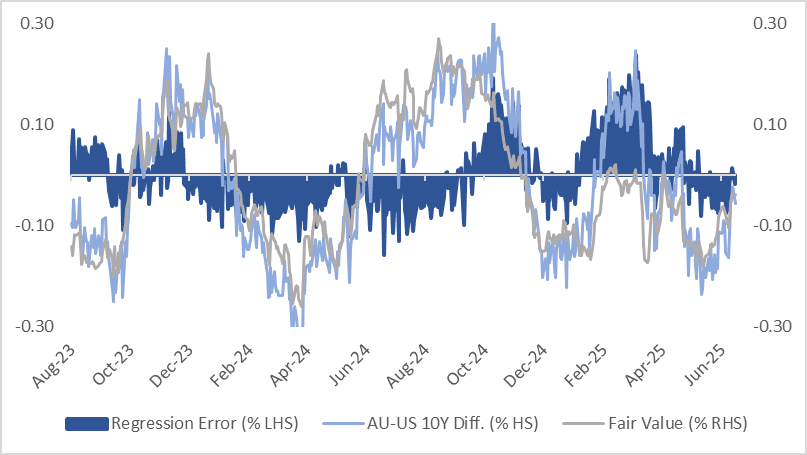

AUSSIE BONDS: AU-US 10Y Diff Is Near Middle Of Range

The AU-US 10-year cash yield differential currently stands at -6bps, positioned near the middle of the +/- 30bps range that has held since November 2022.

- A simple regression of the 10-year yield differential against the AU-US 1-year forward 3-month swap rate (1Y3M) differential over the past year suggests the current spread is slightly below fair value at -4bps.

- The 1Y3M differential, a key gauge of expected relative policy trajectories over the next 12 months, has traded within a 40bp range this year and is currently in the top half of the range at ~-5bps after last week’s surprise decision by the RBA to leave the cash rate unchanged at 3.85%.

- In early February, the 1Y3M differential had declined approximately 100bps since mid-September 2024, falling from +60bps to -40bps.

Figure 1: AU-US Cash 10-Year Yield Differential (%)

Source: Bloomberg Finance LP / MNI

BONDS: NZGBS: Closed Near Cheaps, Bear-Steepener

NZGBs closed near the session’s worst level, showing a modest bear-steepener. Benchmark yields were flat to 3bps higher. The NZ-US 10-year yield differential closed 2bps tighter at +14bps.

- The New Zealand performance of services index rebounded somewhat in June, rising to 47.3 from 44.1 (per BNZ and Business NZ). We are still sub the early 2025 highs for the index, which was just above the 50 expansion/contraction point.

- (Bloomberg) -- RBNZ balance sheet has shrunk further in June, according to data posted on the central bank website Monday in Wellington. Total assets declined to NZ$72.4b from NZ$77.3b at May 31, and from NZ$84.4b at June 20, 2024, the smallest since November 2020.

- Swap rates closed flat to 2bps higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed slightly softer across meetings. 19bps of easing is priced for August, with a cumulative 34bps by November 2025.

- Tomorrow, the local calendar will be empty.

- On Thursday, the NZ Treasury plans to sell NZ$200mn of the 4.50% May-30 bond, NZ$200mn of the 4.25% May-36 bond and NZ$50mn of the 1.75% May-41 bond.

NEW ZEALAND: Mixed June Card Spending Trends, Down For Q2

June card spending figures were mixed, with total spending down 0.2% m/m, after a 0.3% May gain. Card spending for retail rose 0.5%m/m, after a revised 0.1% fall in May.

- The rise in retail card spending was the first increase since Feb of this year. Services rose 0.7%m/m.

- while Core spending was up 0.7%m/m, with apparel, durables and consumables all posting rises versus May outcomes. Vehicles, ex fuel, fell by 2.7%m/m.

- In y/y terms, total card spending was -1.1%, versus -1.8% in May. For retail, we saw a 1.0%y/y gain, versus -0.7% in May.

- Non-retail industry spend was down 1.8%m/m and down 8.1% y/y.

- Stats NZ noted, "The total value of electronic card spending, including the two non-retail categories (services and other non-retail), decreased by $419 million (1.5 percent) compared with the March 2025 quarter."

NEW ZEALAND: Services PMI Firmer In June, But Still Comfortably Sub 50.0

The New Zealand performance of services index rebounded somewhat in June, rising to 47.3 from 44.1 (per BNZ and Business NZ). We are still sub the early 2025 highs for the index, which was just above the 50 expansion/contraction point.

- The improvement in the services index mirrors, to some degree, the rebound in the manufacturing index from last Friday (48.8 from 47.4).

- Looking at the sub indices of the services PMI we can observe rebound in new orders to 48.8 from 43.4 (the manufacturing PMI also saw a rebound in new orders).

- Still only stocks/inventories for the services PMI is above 50 (in terms of the sub-indices). Activity/sales rose to 44.5 from 40.3, while employment was barely changed at 47.4.

- BNZ remained pessimistic post the print: "Every month it remains below 50 suggests service sector conditions are getting worse not better” (via BBG).

- Focus will be on whether the firmer new orders backdrop continues and translates into better economy wide activity trends. The RBNZ did consider easing last week due to the softer economic backdrop.

FOREX: Asia FX Wrap - BBDXY Holding Around 1200

The BBDXY has had a range of 1198.51 - 1200.95 in the Asia-Pac session, it is currently trading around 1200, +0.05%. The BBDXY has once again found decent supply capping the 1200 area. Price action is interesting though in that the price is not violently moving lower from these bouts of strength as it did in the past. The price does look stretched and the market is short so a correction is not out of the question. Axios via (BBG) - Trump To Announce 'Aggressive' Ukraine Weapons Plan : Headlines have crossed from Axios that US President Trump will announce an 'aggressive' Ukraine weapons plan Monday. "President Trump will announce a new plan to arm Ukraine on Monday that is expected to include offensive weapons, two sources with knowledge of the plans tell Axios."

- EUR/USD - Asian range 1.1662 - 1.1698, Asia is currently trading 1.1680. The pair tried lower on the open but has again seen solid demand again just towards the 1.1650 area in our session. The price is still starting to look a little stretched in the short term and is vulnerable to any correction in the USD, first support is back towards 1.1600 then more importantly the 1.1450 area.

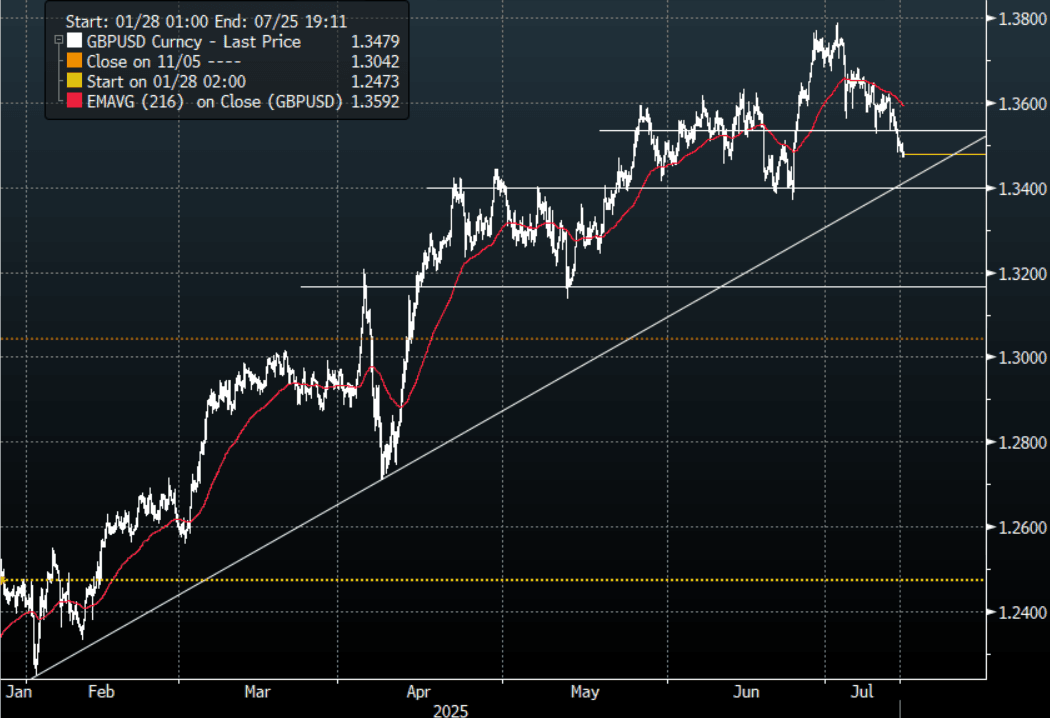

- GBP/USD - Asian range 1.3472 - 1.3504, Asia is currently dealing around 1.3480. Price has rejected the move higher but the USD would need to gain momentum higher for GBP/USD to extend lower in the short-term. First support right here around 1.3500 a break below here would signal a deeper pullback to the more important 1.3350/1.3400 area.

- USD/CNH - Asian range 7.1686 - 7.1758, the USD/CNY fix printed 7.1491, Asia is currently dealing around 7.1700. Sellers should be around on bounces while price holds below the 7.2500 area and the PBOC manages the fix lower.

- Cross asset : SPX -0.45%, Gold $3354, US 10-Year 4.415%, BBDXY 1200, Crude oil $68.41

- Data/Events : Germany BBG Economic Survey, France BBG Economic Survey, EZ BBG Economic Survey, Spain BBG Economic Survey

Fig 1: GBP/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

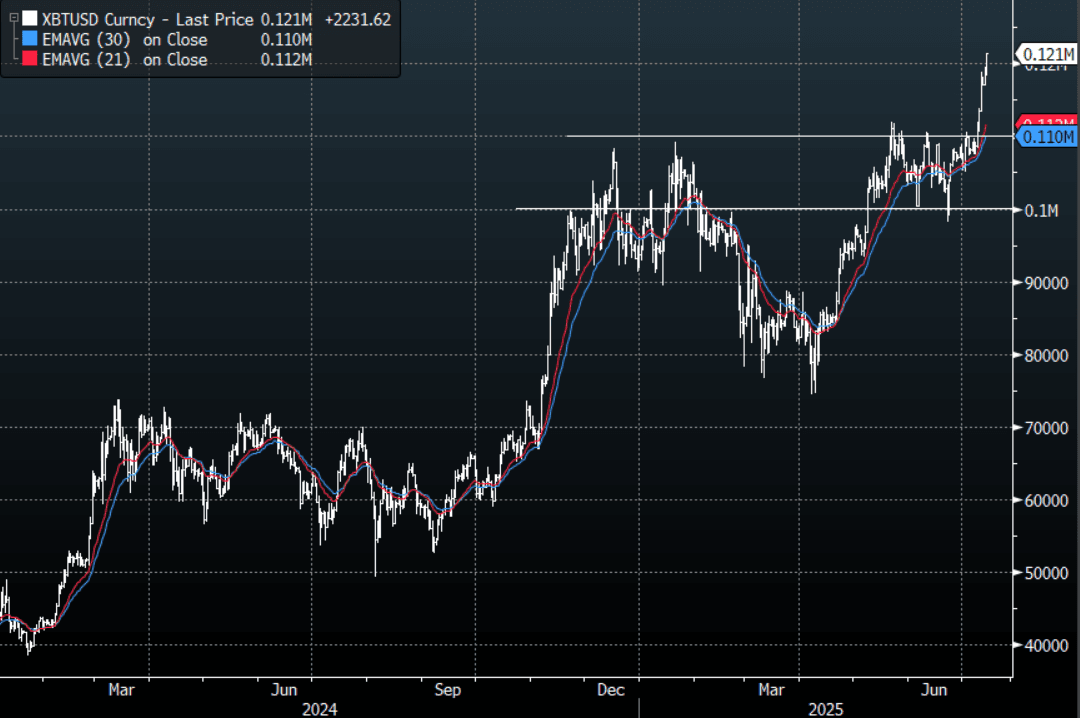

CRYPTO: Bitcoin Makes New Highs Through $120 000 As We Head Into Crypto Week

Bitcoin has had a range of $118 312.80 - $121 365.19 in the Asia- Pac session, it is currently trading around $121 280, +1.80%. Bitcoin is making new all time highs through $120 000 this morning as the market and institutional in particular seem to be getting ahead of what they perceive to be an important week for the industry.

- (Bloomberg) - ‘House Plans ‘Crypto Week’ to pass Stablecoin, Other Bills. House Republicans are turning their attention toward advancing President Trump’s cryptocurrency agenda as they seek to send landmark stablecoin legislation to the president’s desk and advance other digital currency legislation. The week of July 14 is set to be “Crypto Week.”

- Lance Roberts on X:“There has been a lot of talk about the demise of the dollar, even though it still comprises 58% of foreign reserves. However, one thing that could change that is the rise of stablecoins, where 99% of all stablecoins are pegged to the dollar. If the world goes digital, as expected, the dollar may be the dominant reserve."

- Andreas Steno Larsen - “Big week in relation to the legislative landscape for BTC/Crypto in the US next week and BTC is making a weekend breakout as we speak. ”

Fig 1 : Bitcoin Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

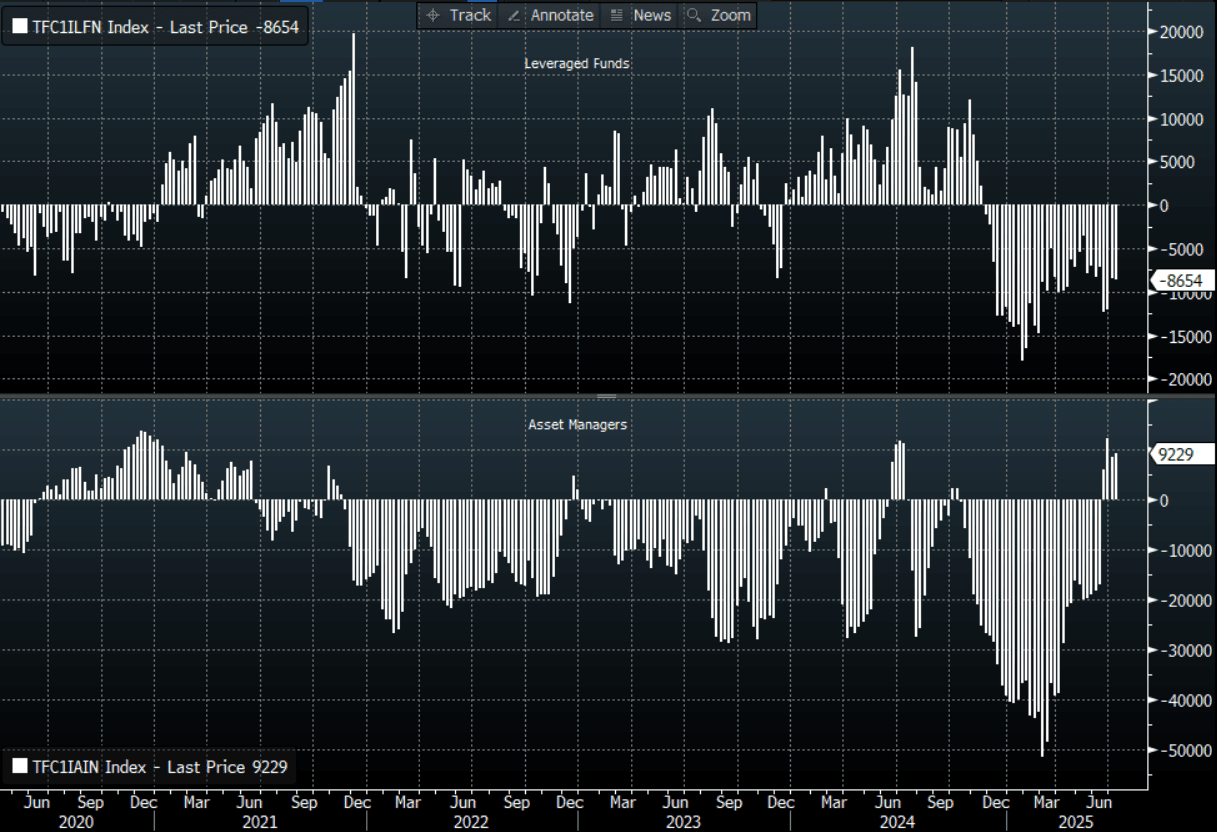

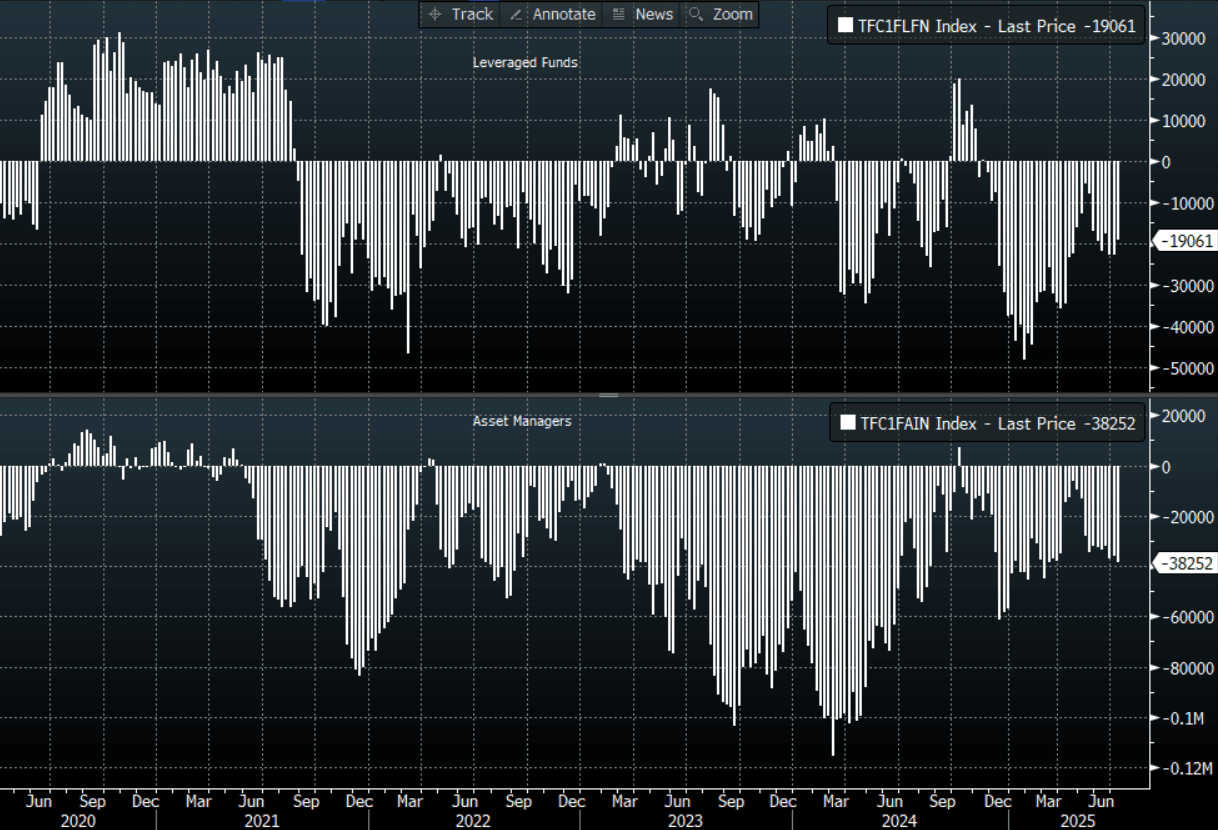

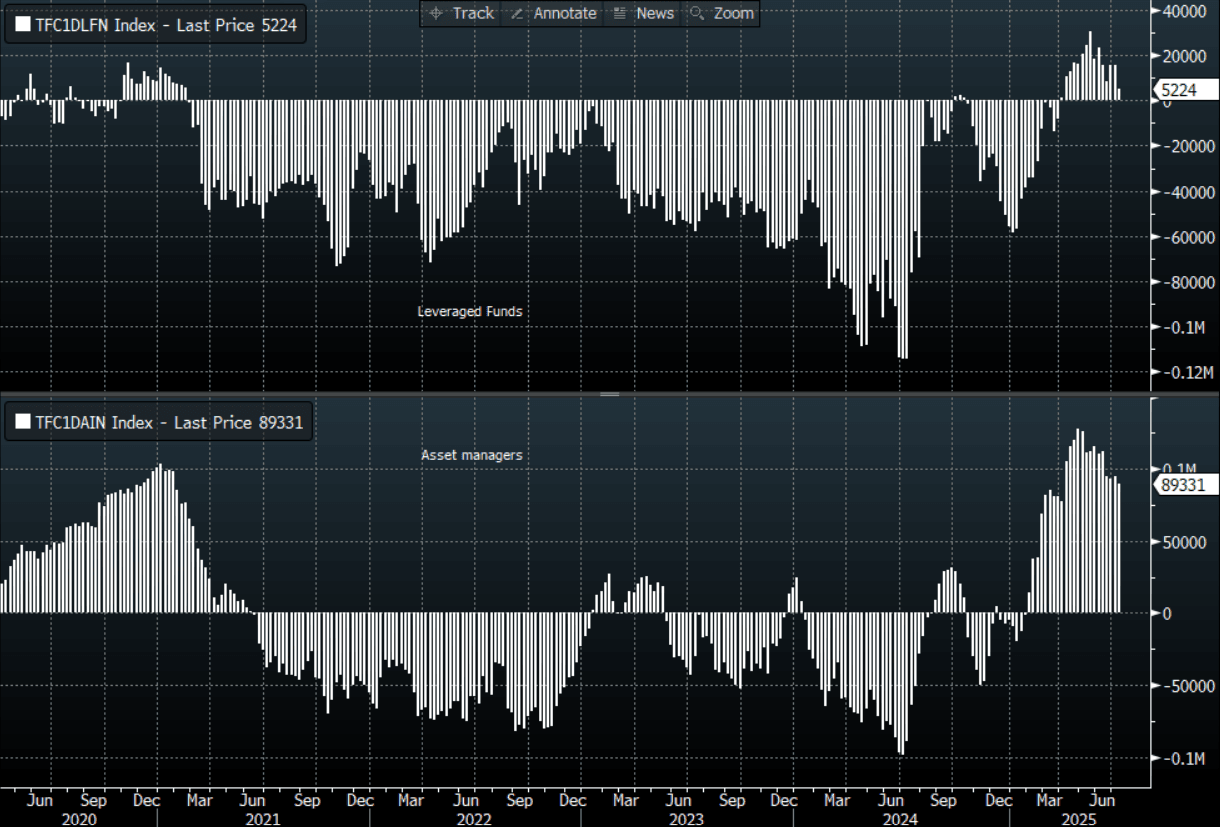

FOREX: Yen Longs Trimmed, CAD Shorts Added To

The most notable feature of last week's CFTC FX positioning update (for the week ending July 8th), was the cut back in yen long positioning, see the table below. Leveraged players cut JPY net longs by close to 10.6k, but maintained an outright long of just over 5k. Asset managers were more modest in their trimming (-5.4k). These moves follow USD/JPY's rebound back above 147.00 recently. USD/JPY was also supported on dips last week, which may hint at more trimming of JPY longs. Focus remains on trade negotiations as the Aug 1 deadline approaches (when tariff rates rise to 25%).

- Elsewhere for EUR and GBP, leveraged and asset manager position shifts were mixed. Leveraged players trimmed EUR longs almost back to flat, but asset managers raised their net long position by more.

- For GBP/USD it was the opposite, but aggregate positioning was little changed.

- For AUD, leveraged players trimmed net shorts, while asset managers sold more A$ modestly.

- CAD was sold by both leveraged names and asset managers, adding to outright shorts for both segments.

Table 1: CFTC Positioning Update - Weekly Changes, Outright Positions By Major Currencies

| Leveraged Contracts | Asset manager Contracts | |||

| Weekly Change | Outright Position | Weekly Change | Outright Position | |

| JPY | -10574 | 5224 | -5422 | 89331 |

| EUR | -3189 | 1843 | 8062 | 374805 |

| GBP | 4164 | 40643 | -4504 | -14294 |

| AUD | 3842 | -19061 | -2260 | -38252 |

| NZD | -230 | -8654 | 714 | 9229 |

| CAD | -1917 | -28985 | -5884 | -42270 |

| CHF | 129 | 1416 | -442 | -37274 |

| MXN | 787 | -5334 | 4820 | 44319 |

Source: Bloomberg Finance L.P./MNI

NZD: Asia Wrap NZD/USD - Challenging Support Just Below 0.6000

The NZD/USD had a range of 0.5981 - 0.6015 in the Asia-Pac session, going into the London open trading around 0.5985, -0.40%. Risk is opening on the backfoot this morning as the world has to again digest Trump's next round of tariffs this time on Europe and Mexico, E-Mini -0.40%, NQ -0.40%. NZD/USD needs to hold this support just below 0.6000 to build for another test higher, the risk is the USD taking a leg higher. A break below this support and the market would look back towards the 0.5850/0.5900 area.

- NZ Data - Services PMI Firmer In June, But Still Comfortably Sub 50.0 : The New Zealand performance of services index rebounded somewhat in June, rising to 47.3 from 44.1 (per BNZ and Business NZ). We are still sub the early 2025 highs for the index, which was just above the 50 expansion/contraction point.

- NZ Data - Mixed June Card Spending Trends, Down For Q2: June card spending figures were mixed, with total spending down 0.2% m/m, after a 0.3% May gain. Card spending for retail rose 0.5%m/m, after a revised 0.1% fall in May.

- (Bloomberg) -- RBNZ balance sheet has shrunk further in June, according to data posted on the central bank website Monday in Wellington. Total assets declined to NZ$72.4b from NZ$77.3b at May 31, and from NZ$84.4b at June 20, 2024, smallest since November 2020.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : none.

- CFTC Data shows Asset Managers added slightly to their newly built longs in NZD +9229, the Leveraged community added slightly to their shorts last week -8654.

- AUD/NZD range for the session has been 1.0927 - 1.0972, currently trading 1.0970. TThe cross has broken out of its recent range and is now trying to push through the more pivotal 1.0950 area. Dips back to 1.0850/1.0900 should now be supported as the pair tries to build momentum to move higher.

Fig 1: NZD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia Wrap - AUD/USD Moves Away From 0.6600 After A Soft Open For Risk

The AUD/USD has had a range of 0.6558 - 0.6588 in the Asia- Pac session, it is currently trading around 0.6565, -0.20%. CFTC Data does not show any real reduction in the AUD short positions, the price action at the end of last week suggested there might have been some paring back of these so it's interesting to see it has not had an impact yet. Risk is opened on the backfoot this morning as the world has to again digest Trump's next round of tariffs this time on Europe and Mexico. AUD/USD is being capped by decent supply towards 0.6000, price needs to clear this to gain momentum for a push higher until then it looks back to the range.

- (Bloomberg) -- “The IMF data show reserve managers shifting into USD in 4Q 2024, reducing most other currencies by modest amounts. The exceptions were large drops in the percentage of holdings for AUD and GBP. For the Aussie dollar that was the single largest change in allocations in either direction since 2012. In 1Q 2025 the shift out of AUD ramped up massively, to the lowest level on record.”

- “The US government is pressing Japan and Australia to clarify their roles in the event of a US-China war over Taiwan, a move that upsets America’s two key allies in the region, the FT reported.” -BBG

- The AUD/USD continues to hold above its support around 0.6500, looks like it's back to the 0.6500 - 0.6600 range and it should now take its cues from the USD. Watching to see if the market can build on this outperformance and break above 0.6600.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6560(AUD631m July 15), 0.6495(AUD611m July15), 0.6700(AUD611m July 16).

- CFTC Data shows Asset managers added to their shorts slightly -38252, the Leveraged community pared back their shorts to -19061.

AUD/JPY - Today's range 96.46 - 96.93, it is trading currently around 96.75, -0.20%. The pair has had a good move above 96.00 and this time looks to be building real momentum to extend higher. The market has been caught wrong-footed in both legs of this pair and price action suggests a potential move back to 99.00/100.00. Dips back to 95.50/96.00 should now be supported.

Fig 1: AUD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

JPY: Asia Wrap USD/JPY - Consolidating Above 147.00

The Asia-Pac USD/JPY range has been 146.86 - 147.57, Asia is currently trading around 147.30, -0.10%. The pair has traded sideways with little direction, the soft opening for risk saw some reprieve for JPY longs in the crosses. The USD/JPY relentless march higher has been pretty telling, challenging a market positioned the wrong way. Price is now consolidating some of those recent gains, dips back towards 145.00 should now find support first up. CFTC Data shows leveraged funds have pared back their JPY longs almost back to flat, Asset managers have pared back some of their position but still continue to run a decent sized long JPY position.

- (Bloomberg) - " The Bank of Japan finished selling millions of dollars of stocks it bought from besieged banks, ending a nearly two decade process. The BOJ's holdings of the shares purchased from banks hit zero as of July 10, falling from 2.5 billion 10 days ago, according to its balance sheet report."

- JAPAN DATA - Core Machine Orders Y/Y Slows, But Still Pointing To Resilient Capex.

- "JAPAN RULING BLOC MAY LOSE MAJORITY IN ELECTION: JNN ANALYSIS” - BBG

- (Bloomberg) - Options traders appear to be positioning for the yen to weaken further in the near-term due to looming US inflation data and Japan’s upper house elections.

- USD/JPY has lost all downside momentum for now and is back in its wider 142.00 - 148.00 range. The Market is long JPY and should the USD manage to continue to correct higher the risk is a move back to the top end of the range to further challenge the conviction of the shorts.

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.10($514m).Upcoming Close Strikes : 146.50($1.25b July 16).

- CFTC data shows Asset managers reduced their JPY longs slightly +89331, while leveraged funds have almost squared their newly built JPY longs +5224.

Fig 1 : JPY CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Modest Gains Evident For Most Markets, Despite Negative US Futures

Asian stock markets have had a fairly indifferent start to the trading week, albeit with a positive bias for most markets. At this stage, aggregate moves are not much beyond 0.50% for the major regional bourses. US equity futures are down close to 0.40% at this stage. Weekend threats from US President Trump on a 30% tariff for the EU (as well as Mexico) has weighed on sentiment. EU futures are down around 0.60% at this stage. There appears to be room for negotiations but concrete deals might be difficult to achieve ahead of the August 1 deadline.

- China and Hong Kong markets are marginally higher in the first part of Monday trade. The CSI 300 holding above 4000 at this stage, while the HSI is above 24000. Earlier we have China June trade data, where export and import growth marginally surprised on the upside. These trends don't look spectacular but are holding up well considering tariff levels.

- Japan markets are marginally higher in the first part of Monday trade. We continue to sell upward pressure on longer dated JGB yields. We have upper house elections later this week. Local news wires noted that the ruling bloc may struggle to keep its majority (FNN ANALYSIS via BBG).

- South Korea's Kospi is showing modest outperformance, up +0.40%, near 3190 in index terms. The sell-side consensus remains for higher Kospi levels, with Goldman's upgrading its target, while J.P. Morgan stated the index could get to 5000 within the next few years.

- Taiwan markets are struggling for further upside, with the Taiex down around 0.70% at this stage.

- The ASX 200 is around flat. In SEA, aggregate moves aren't large at this stage. Thailand, Indonesia and Philippines markets are all in the green.

ASIA STOCKS: Equity Flows Ended Last Week Positively, Taiwan The Standout

Asia Pac equity inflow momentum was mostly positive into the end of last week. South Korea and Taiwan remained the standouts, see the table below.

- Taiwan has seen just over $1bn in net inflows over the past 5 trading sessions. South Korea trailed slightly, at just above $700mn. The early impetus for South Korean markets today is modest outflow pressures, as US equity futures track weaker in response to Trump's 30% tariff threat against the EU and Mexico (made over the weekend).

- Markets remain hopeful that lower tariff rates can be negotiated ahead of the Aug 1 deadline. Earnings, particularly in the tech space will be the other focus point.

- Elsewhere inflow momentum was positive into Indian markets, as YTD outflows continue to be scaled back.

- A positive end to the week for Thailand was also evident.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 274 | 711 | -8578 |

| Taiwan (USDmn) | 615 | 1073 | -1915 |

| India (USDmn)* | 98 | 614 | -7805 |

| Indonesia (USDmn) | 28 | -115 | -3502 |

| Thailand (USDmn) | 68 | 90 | -2366 |

| Malaysia (USDmn) | -24 | -122 | -2793 |

| Philippines (USDmn) | 1 | -14 | -562 |

| Total (USDmn) | 1060 | 2237 | -27520 |

| * Data Up To July 10 |

Source: Bloomberg Finance L.P./MNI

OIL: Little Reaction To Rumours Around Ukraine Weapons Plan

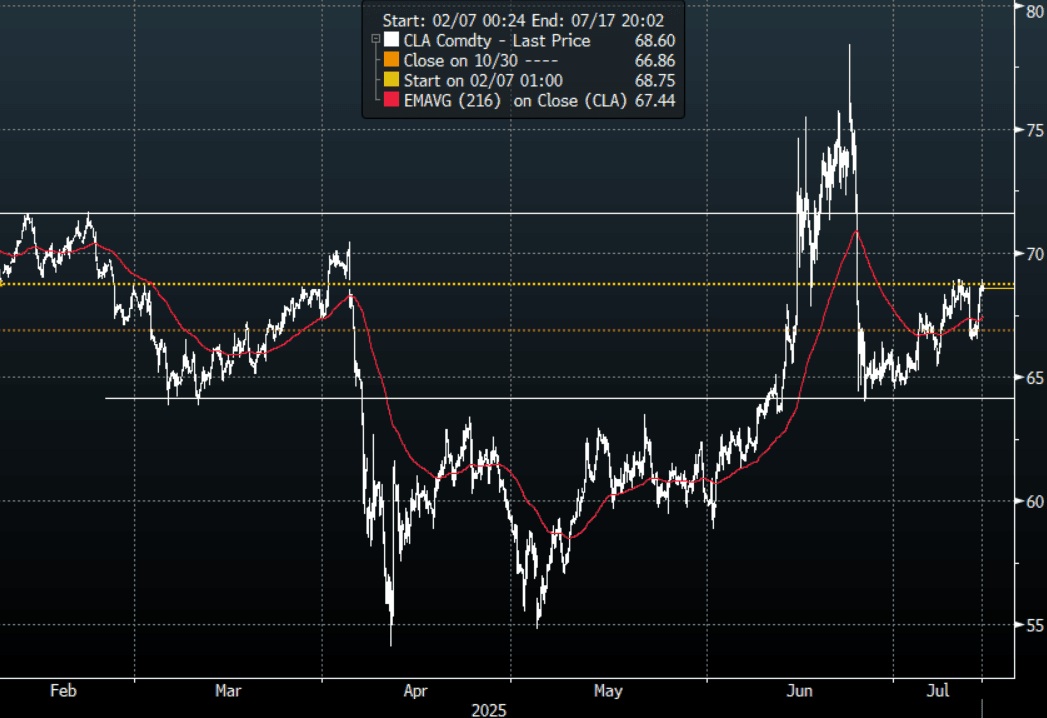

The Asia-Pac range for the CLQ5(WTI) contract was $68.41 - $68.95, it is currently trading around $68.50 in the Asia-Pac session. “In futures markets, oil rose a second day as President Donald Trump declared 30% tariffs on imports from the European Union and Mexico over the weekend, ahead of a “major statement” on Russia.” - BBG

- MNI RUSSIA: Kremlin Waits On Trump Statement As US Pres Could Use PDA For Weapons. Kremlin spox Dmitry Peskov, speaking to reporters, says that regarding US President Donald Trump's comments regarding a "major statement" on Russia to be delivered on 14 July, "We are waiting for it, [we] want to understand what he meant."

- Axios via (BBG) - Trump To Announce 'Aggressive' Ukraine Weapons Plan : Headlines have crossed from Axios that US President Trump will announce an 'aggressive' Ukraine weapons plan Monday. "President Trump will announce a new plan to arm Ukraine on Monday that is expected to include offensive weapons, two sources with knowledge of the plans tell Axios."

- The Real Fly on X: SEN GRAHAM: "A turning point regarding Russia's invasion of Ukraine is coming...I expect, in the coming days, you will see weapons flowing at a record level to help Ukraine defend themselves".

- Brent for September settlement is trading at $70.49 a barrel on the ICE Futures in Asia.

Fig 1: WTI Crude Future Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

GOLD: Steady Today After Friday Strong Gain

Gold is little changed in today’s Asia-Pac session, after closing ~1% higher at $3355.59 on Friday.

- This came despite US tsys finishing Friday’s session with a bear-steepener. Higher rates are typically negative for gold, which doesn’t pay interest. Cash US tsys are slightly mixed in today's Asia-Pac session, with yields 1bp lower to 1bp higher.

- (Bloomberg) – “Gold has a raft of supportive drivers, from central-bank buying and investor inflows into exchange-traded funds to concerns about the trade war and, separately, the US fiscal outlook.”

- “Central banks and other institutions accumulated about 77 tons of gold on average each month from January through to May, according to Goldman Sachs Group Inc., which maintained forecasts for bullion to rally to fresh records in the coming quarters.”

- Mounting pressure on Federal Reserve Chair Jerome Powell continues, with President Donald Trump criticising his monetary policy approach as overly restrictive.

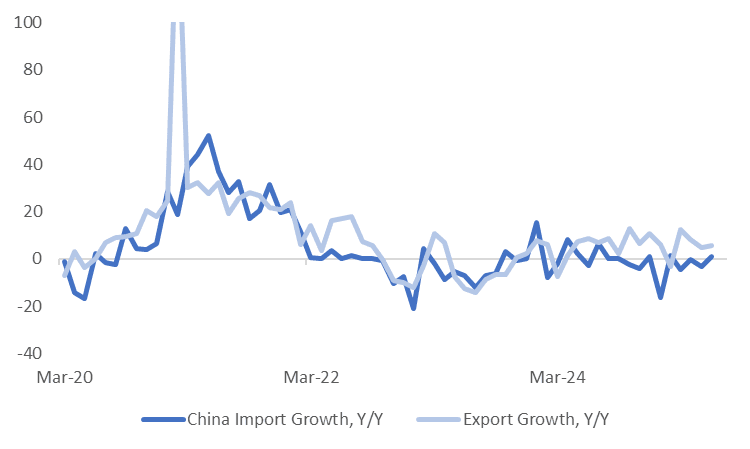

CHINA DATA: Export & Import Trends Improve, Rare Earth Exports Rebound

China June trade figures were slightly better than forecast. Exports rose 5.8%y/y, against a 5.0% forecast (4.8% was the May outcome). Imports rose 1.1%y/y, versus 0.3% forecast and -3.4% for May. The trade surplus pushed higher to $114.8bn, slightly above forecasts (near $112bn), while the May print was $103.22bn.

- In terms of commodity import volumes, we had coal down slightly to 33.04mln tonnes (36.04 was the May outcome). Crude oil rose though as did iron ore (to 105.95mln tonnes). Copper and natural gas rose, while soybeans fell slightly.

- Our China policy team noted that H1 imports were impacted by lower commodity prices: "Bulk commodities accounted for about 30% of China's total import value, Wang said, noting the average price of crude oil, iron ore and soybeans dropped more than 10% y/y in H1, dragging down the overall growth rate by 2.7 percentage points."

- Rare earth export volumes rose 32% in m/m terms and were +11.9%y/y. This was a sticking point from the US side around recent trade negotiations. China promised to accelerate export licenses in this space.

- Still, overall exports to the US were still down 16.1%y/y (per BBG). The trade surplus with the US rose to $26.57bn, the first rise since March of this year.

- The trade surplus with the EU eased to $25.94bn from $26.62bn. the surplus with Hong Kong rose to $26.15bn from $22.97bn.

- China also saw lower trade deficits with both Taiwan and Australia.

Fig 1: China Export & Import Trends Y/Y

Source: Bloomberg Finance L.P./MNI

ASIA FX: USD/KRW Drifts Higher Amid Tariff Concern, THB Outperforms

The bias in USD/Asia pairs has been to gravitate higher in the first part of Monday trade. This mirrors some of the moves seen in the majors space, where higher beta plays like NZD and AUD have underperformed. Equity futures for US and EU markets are weaker, following weekend tariff threats on the EU and Mexico from US President Trump. There are also reports that Trump may expand US support to Ukraine, including offensive weapons. Regional Asia Pac equities aren't see much fallout at this stage though, with some markets in SEA up close to 1%.

- USD/CNH is little changed, last holding close to 7.1700. The USD/CNY fixing edged higher but remained sub 7.1500. June trade data was slightly better than forecast, with export growth close to 6%y/y, while import growth rebounded more than forecast. The trade surplus was also wider than forecast. Market impact from the data was negligible.

- Spot USD/KRW has risen towards 1380 in line with the risk off tone seen in the majors. We aren't too far away from the 50-day EMA resistance point (.The Kospi is still rallying, amid continued positive sell-side view points. Earlier the South Korean trade minister stated it may be possible to reach an 'in principle' trade agreement by Aug 1, with progress made around discussions on key industrial sectors (per RTRS).

- USD/TWD spot is little changed, last still holding above 29.20. USD/HKD spot remains just under the top end of the peg band near 7.8500.

- In SEA, USD/PHP is up around 0.30%, last near 56.65/70, while USD/IDR is up by 0.20%, the pair close to 16245 in latest dealings. We remain within recent ranges for both pairs. USD/SGD is up at 1.2815, slightly weaker in SGD terms, despite a Q2 GDP beat.

- USD/THB is bucking these trends, the pair last in the 32.40/45 region (up around 0.20% in THB terms), close to recent lows near 32.30. Headlines cross earlier of "*THAILAND PREPARING 200B BAHT SOFT LOANS FOR TARIFF-HIT FIRMS" (via BBG), which may be aiding local equity market sentiment. The tourism arrivals estimate for 2025 was cut too 35mln from 40mln, although some slowing has already been evident in recent months.

SINGAPORE: Q2 Growth Stronger Than Forecast, Singapore Avoids Recession

Singapore's Q2 advance GDP print came in stronger than forecast, up 1.4%q/q, versus the 0.8% forecast. The Q1 fall was revised to -0.5% (from -0.6%q/q). In y/y terms we were 4.3%, against a 3.6% forecasts and 4.1% Q1 outcome.

- The detail showed manufacturing at +0.1%q/q, after a 5.5% fall in Q1. Construction rose 4.4%q/q, after falling 1.8% in Q1. Services growth also accelerated to 1.4%q/q (from 0.6% in Q1). All this sub categories saw y/y growth in the 4-5.5% range (with manufacturing the strongest).

- Today's outcome is a positive result, as there were concerns earlier in the year the Singapore economy could enter into a technical recession (2 consecutive quarters of negative growth). For now, this has been avoided and while this is the advance GDP print, it would seem unlikely revisions would erode all of the 1.4%q/q growth.

- The government's forecast for growth this year is 0-2%, with much uncertainty resting on the trade/tariff outlook as we progress through the second half.

- Note that the MAS July policy meeting outcome is due before the end of the month (July21-31 is the range listed by BBG), with today's growth outcome adding at the margin for the MAS to hold at this meeting (after easing in H1 this year).

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 14/07/2025 | 0600/0800 | *** | Final Inflation Report | |

| 14/07/2025 | - | *** | Money Supply | |

| 14/07/2025 | - | *** | New Loans | |

| 14/07/2025 | - | *** | Social Financing | |

| 14/07/2025 | 1230/0830 | ** | Wholesale Trade | |

| 14/07/2025 | 1500/1700 | ECB Cipollone At EU Parliament | ||

| 14/07/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 14/07/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 15/07/2025 | 2301/0001 | * | BRC-KPMG Shop Sales Monitor | |

| 15/07/2025 | 0200/1000 | *** | GDP | |

| 15/07/2025 | 0200/1000 | *** | Fixed-Asset Investment | |

| 15/07/2025 | 0200/1000 | *** | Retail Sales | |

| 15/07/2025 | 0200/1000 | *** | Industrial Output | |

| 15/07/2025 | 0200/1000 | ** | Surveyed Unemployment Rate M/M | |

| 15/07/2025 | 0700/0900 | *** | HICP (f) | |

| 15/07/2025 | 0900/1100 | ** | Industrial Production | |

| 15/07/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 15/07/2025 | 1230/0830 | *** | CPI | |

| 15/07/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/07/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/07/2025 | 1230/0830 | *** | CPI | |

| 15/07/2025 | 1230/0830 | *** | CPI | |

| 15/07/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 15/07/2025 | 1300/0900 | * | CREA Existing Home Sales | |

| 15/07/2025 | 1315/0915 | Fed Vice Chair Michelle Bowman |