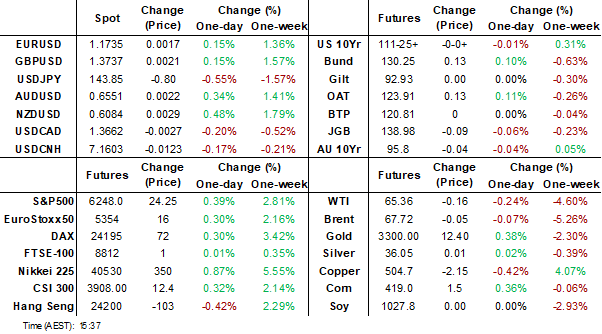

MNI EUROPEAN MARKETS ANALYSIS: USD Back Under Pressure

- USD downside pressure has resumed today as we approach month/quarter end. Focus remains on trade discussions, with Canada ending its digital tax to get negotiations with the US back on track. Trump rhetoric around US-Japan trade talks reportedly remained firm. US Tsy yields are little changed, while equity futures are positive.

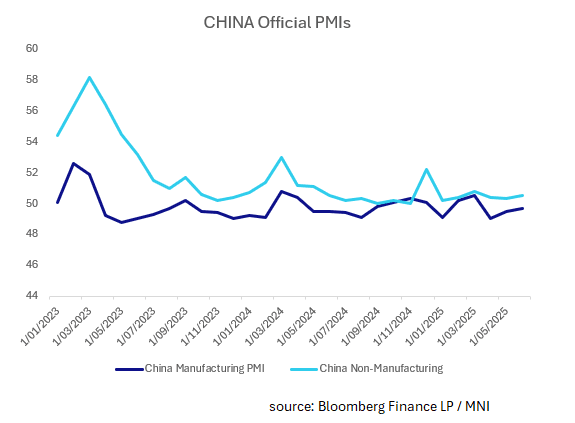

- On the data front, it has mostly been second tier today, except for China official PMIs. They were better than expected, but manufacturing remained in contraction.

- Coming up we have German retail sales and preliminary June CPI. In the UK GDP revisions are out. In the US, on the data front, the MNI Chicago PMI Prints, while the Atlanta Fed's MNI connect event is also held.

MARKETS

US TSYS: Asia Wrap - Long-End Yields Edge Higher

The TYU5 range has been 111-22 to 111-27 during the Asia-Pacific session. It last changed hands at 111-24, down 0-02 from the previous close.

- The US 2-year yield is almost unchanged trading around 3.748%.

- The US 10-year yield has edged higher trading around 4.287%, up 0.01 from its close.

- Block Sell FVU5: SELL 3463 of FVU5 traded at 108-27 1/4, post-time 12:44:04 AEST (DV01 $150,988). The contract is currently trading at 108-27+, -0-00 1/4 from closing levels.

- The 10-year yield has accelerated through its support, this should clear the way for a move lower with the 4.10% area the first target. 10-year yields should now find demand on any bounce back to the 4.35/40% area.

- (Bloomberg) - “In the week ended June 24, positioning data showed a heavy amount of short covering from hedge funds in US 10-year note futures, according to latest CFTC data. Elsewhere, asset managers liquidated net longs in 10-year note futures, while adding to duration long in ultra 10-year note futures.”

- (Bloomberg) - “Trump’s $4.5 trillion tax-cut bill now shifts to the Senate, where a final vote is expected to spill into Monday. The Senate version would add $3.3 trillion to US deficits over a decade, the Congressional Budget Office estimated.”

- Data/Events: MNI Chicago PMI, Dallas Fed Man. Activity

JGBS: Cheaper, Trump Criticises US-JN Auto Trading, 10Y Supply Tomorrow

JGB futures are weaker, -13compared to settlement levels, but off worst levels.

- “The 25% sectoral tariff on automobiles remains a sticking point in US-Japan trade talks, but its impact on growth may be less severe than feared due to a weak yen. Japanese car export prices to North America have fallen 17.7% in dollar terms, likely due to manufacturers absorbing the tariff cost to stay competitive, but export prices in yen terms remain comparable to early 2022.” (BBG)

- The Real Fly on X: "Trump criticised the U.S.-Japan auto-trade relationship as unfair, referring to Japan's negotiator as "MR. Japan," and warned of possible new tariffs ahead of the looming July 9 deadline."

- Cash US tsys are slightly mixed, with a steepening bias, in today's Asia-Pac session after Friday's modest losses. The market awaits speeches from Fed officials and developments in President Donald Trump's $4.5 trillion tax-cut bill.

- Cash JGBs are flat to 3bps cheaper across benchmarks, with the 20-year underperforming. The benchmark 10-year yield is 0.2bp higher at 1.440% ahead of tomorrow's supply.

- Swap rates are 1-2bps higher.

- Tomorrow, the local calendar will see Tankan Index, S&P Global PMI Mfg and Consumer Confidence Index data alongside 10-year supply.

AUSSIE BONDS: Cheaper As Markets Await US Tax Bill Developments

ACGBs (YM -4.0 & XM -4.5) are weaker after a subdued session of trading. Ranges have been relatively narrow.

- The China Official PMIs followed the familiar theme of recent releases, with the PMI manufacturing in mild contraction and the PMI non-manufacturing barely holding in expansion.

- Cash US tsys are slightly mixed, with a steepening bias, in today's Asia-Pac session after Friday's modest losses. The market awaits speeches from Fed officials and developments in President Donald Trump’s $4.5 trillion tax-cut bill.

- Cash ACGBs are 3-4bps cheaper with the AU-US 10-year yield differential at -12bps.

- The bills strip is -2 to -3 across contracts.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in July is given a 94% probability, with a cumulative 81bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- Tomorrow, the local calendar will see Cotality Home Value and S&P Global PMI Mfg data.

- This week, the AOFM plans to sell A$1200mn of the 2.75% 21 June 2035 bond on Wednesday and A$1000mn of the 2.25% 21 May 2028 bond on Friday.

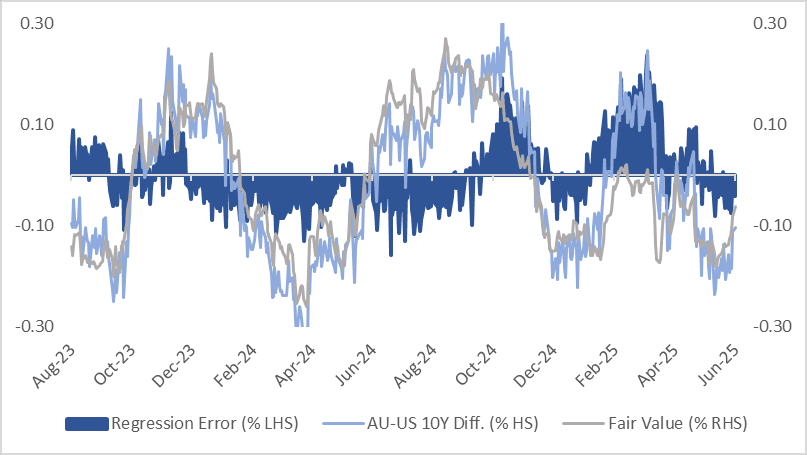

AUSSIE BONDS: AU-US 10Y Diff Remains In The Bottom Of Range

The AU-US 10-year cash yield differential currently stands at -11bps, positioned in the bottom of the +/- 30bps range that has held since November 2022.

- A simple regression of the 10-year yield differential against the AU-US 1-year forward 3-month swap rate (1Y3M) differential over the past year suggests the current spread is slightly below fair value at -6bps.

- The 1Y3M differential, a key gauge of expected relative policy trajectories over the next 12 months, has traded within a 40bp range this year and is currently in the top half of the range at ~-11bps.

- In early February, the 1Y3M differential had declined approximately 100bps since mid-September 2024, falling from +60bps to -40bps.

Figure 1: AU-US Cash 10-Year Yield Differential (%)

Source: MNI - Market News / Bloomberg

BONDS: NZGBS: Closed Moderately Cheaper, Subdued Session Of Trading

NZGBs closed 2bps cheaper across benchmarks after a subdued session of trading.

- The ANZ business activity and confidence measures rose in June. On activity, we moved back to 40.9, from 34.8 in May, while confidence rebounded to 46.3, from 36.6 prior. The improvement in June follows a move lower in these headline indices since the end of Q1. We remain off cyclical highs for both measures, activity reached 50.3 in Dec last year, while confidence was at 65.7 in October last year. The Q2 averages for both activity and confidence were below the Q1 outcomes.

- ANZ noted: “In terms of what firms are actually experiencing, there’s been a bit of a slump recently in both activity and employment." (via BBG).

- Swap rates closed 1-3bps higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed slightly firmer across meetings. 4bps of easing is priced for July, with a cumulative 32bps by November 2025.

- Tomorrow, the local calendar will see the NZIER Business Opinion Survey.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond, NZ$175mn of the 2.75% Apr-37 bond and NZ$50mn of the 2.75% May-51 bond.

NEW ZEALAND: Business Activity & Confidence Up, But Still Off Cycle Highs

The New Zealand ANZ business activity and confidence measures rose in June. On activity we moved back to 40.9, from 34.8 in May, while confidence rebounded to 46.3, from 36.6 prior. The improvement in June follows move lower in these headline indices since the end of Q1. We remain off cyclical highs for both measures, activity reached 50.3 in Dec last year, while confidence was at 65.7 in October last year. The Q2 averages for both activity and confidence were below the Q1 outcomes.

- In terms of the detail, the sub-indices ticked higher, with exports up to 13.9, while investment rose to 19.9 (from 11.6 in May). Costs and wages also rose. The cost sub index to 79, while wages were at 76.1, still sub recent highs for this index.

- The construction outlook improved, but again these indices are still sub recent highs. Employment printed at 10.8, which compares with an earlier high of 18.1 (April this year).

- Pricing intentions rose to 46.3 from 45.4. Inflation expectations were unchanged at 2.71%.

- ANZ noted: “In terms of what firms are actually experiencing, there’s been a bit of a slump recently in both activity and employment. While economic growth in 1q was decent at 0.8% q/q, the omens for 2q are not looking nearly so positive” (via BBG).

- This is consistent with the softer average readings in the headline indices for Q2.

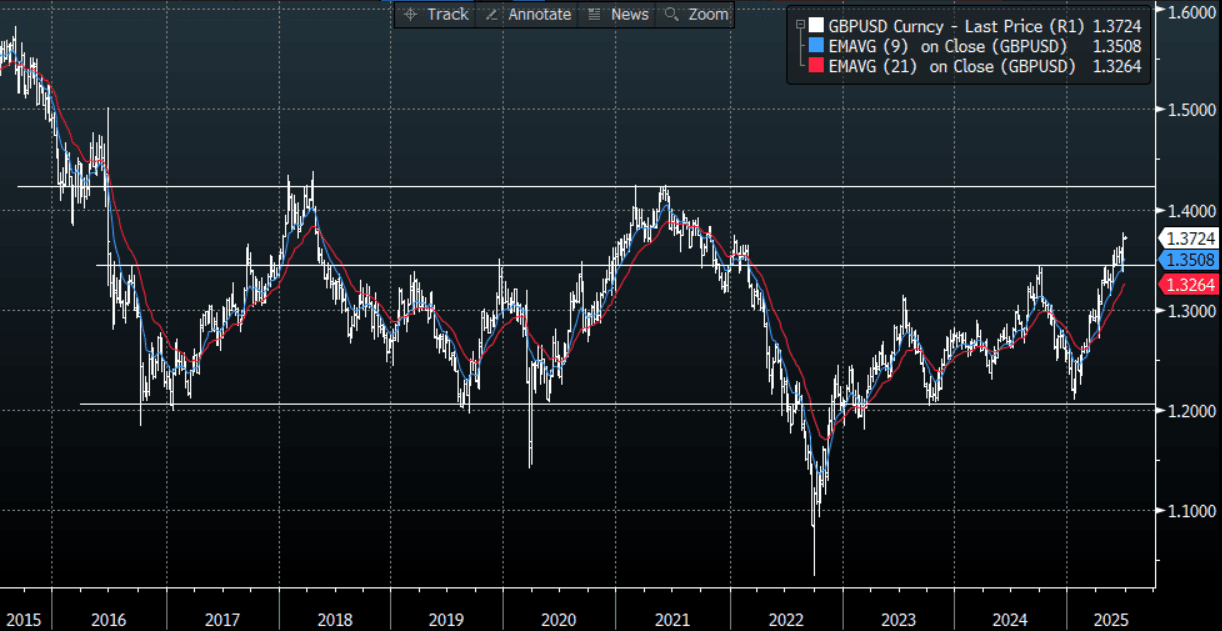

FOREX: Asia FX Wrap - The USD Back Under Pressure

The BBDXY has had a range of 1192.42 - 1197.35 in the Asia-Pac session, it is currently trading around 1194. The USD opened under pressure and gave back most of the gains it made on Friday after Canada rescinded its digital services tax. CHINA Official PMIs for June: The Official PMIs followed the familiar theme of recent releases with the PMI manufacturing in mild contraction and the PMI non-manufacturing barely holding in expansion.

- EUR/USD - Asian range 1.1712 - 1.1739, Asia is currently trading 1.1720. While the USD remains on the back foot the EUR will continue to be supported, first support is back towards 1.1500. This move seems to be accelerating and will now be looking towards 1.2000 and beyond.

- GBP/USD - Asian range 1.3705 - 1.3730, Asia is currently dealing around 1.3715.This move higher now looks to have broken convincingly higher and with the USD looking like it is set for another leg lower Cable could potentially now target levels back towards 1.4200.

- USD/CNH - Asian range 7.1599 - 7.1706, the USD/CNY fix printed 7.1586. Asia is currently dealing around 7.1635. Sellers should be around on bounces while price holds below the 7.2500 area and the PBOC manages the fix lower.

- Cross asset : SPX +0.42%, Gold $3280, US 10-Year 4.285%, BBDXY 1193, Crude oil $65.20

- Data/Events : Ger Retail Sales & CPI, Spain Current Account Balance, Italy Deficit to GDP YTD & CPI, EZ M3 Money Supply

Fig 1: GBP/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

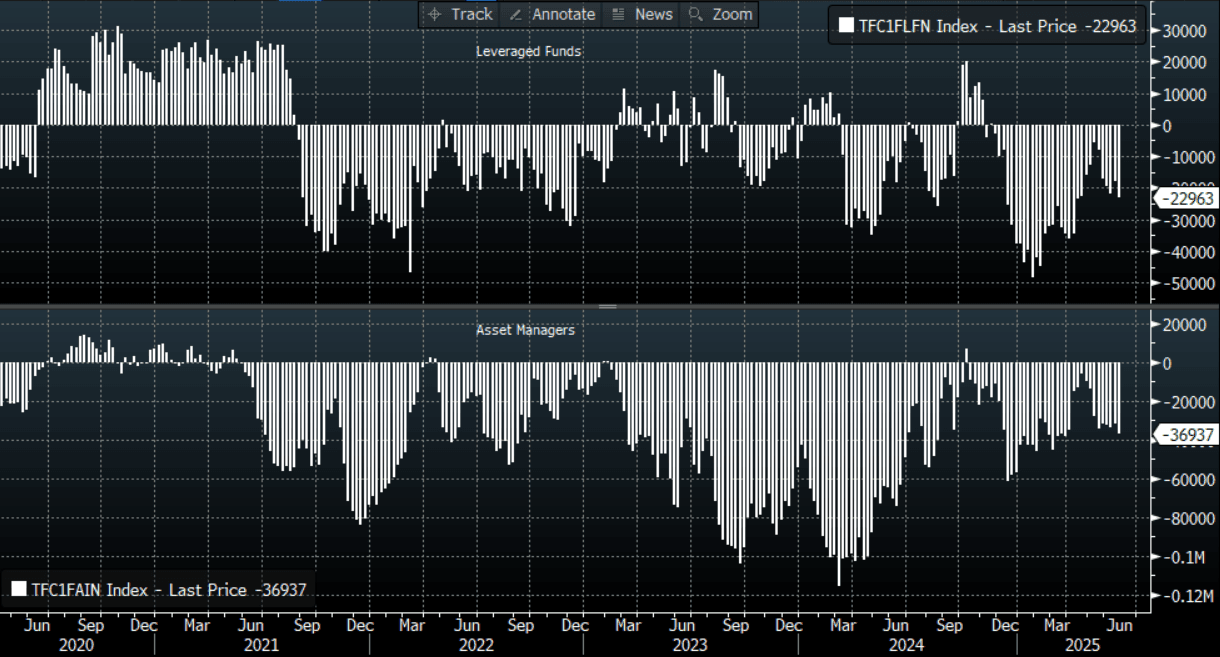

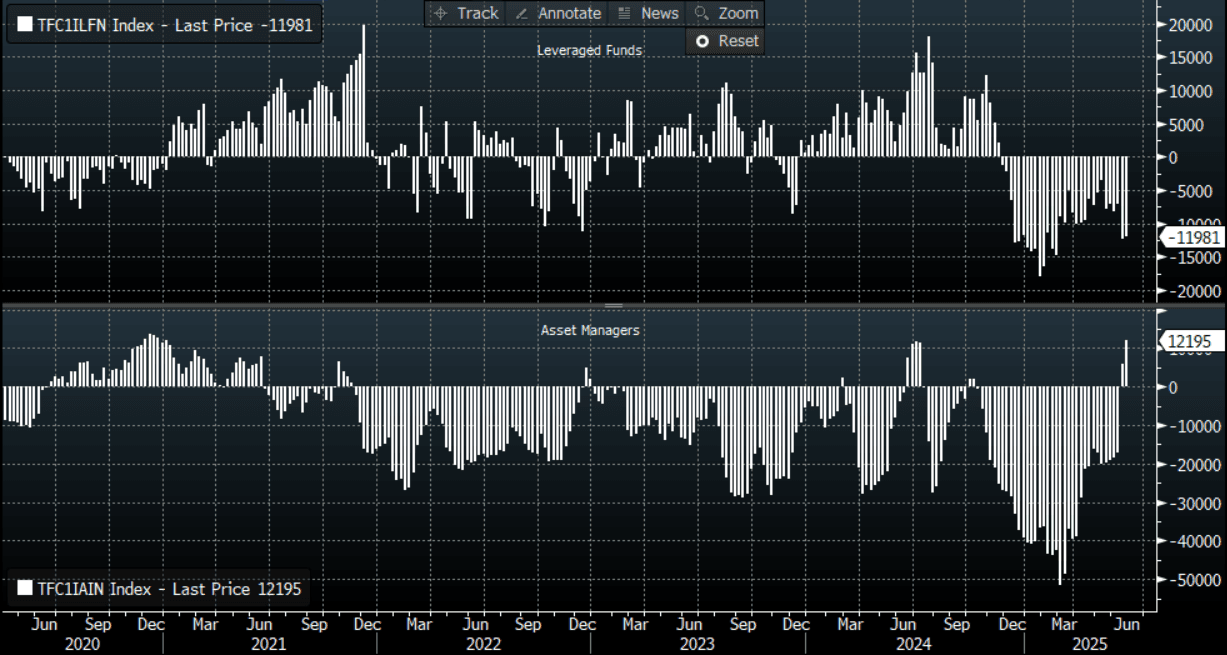

FOREX: AUD Sold Per CFTC, USD Selling By Leveraged Players Evident Elsewhere

The CFTC positioning update for the week ending June 24th showed a shift against the USD, particularly in terms of leveraged investors (albeit for the A$). Asset managers were more mixed in terms of the weekly shift.

- Net selling of the A$, by both leveraged players and asset managers was a standout last week. Both investor bases remain net short the A$. Given generally positive AUD/USD momentum, such flows may be to play for AUD underperformance on key crosses rather than against the USD.

- Leveraged investors added notably to net longs for JPY, EUR and GBP. CAD shorts were also reduced.

- In the asset manager space, aggregate shifts for JPY and EUR weren't large, but net shorts for GBP were added too.

- For NZD, we saw asset managers add longs. At +12k, net longs for this segment is a clear contrast to the still meaningful short asset managers are running with for the AUD.

Table 1: CFTC FX Positioning By Currency & Investor Type

| Leveraged Contracts | Asset manager Contracts | |||

| Weekly Change | Outright Position | Weekly Change | Outright Position | |

| JPY | 7301 | 15935 | -1627 | 93003 |

| EUR | 13536 | 11534 | 3479 | 360688 |

| GBP | 11240 | 45408 | -6974 | -15114 |

| AUD | -5251 | -22963 | -5129 | -36937 |

| NZD | 279 | -11981 | 6322 | 12195 |

| CAD | 4259 | -29077 | 6742 | -26085 |

| CHF | 1639 | 3545 | -930 | -36787 |

| MXN | -2794 | -10542 | 207 | 37986 |

Source: Bloomberg Finance L.P./CFTC/MNI

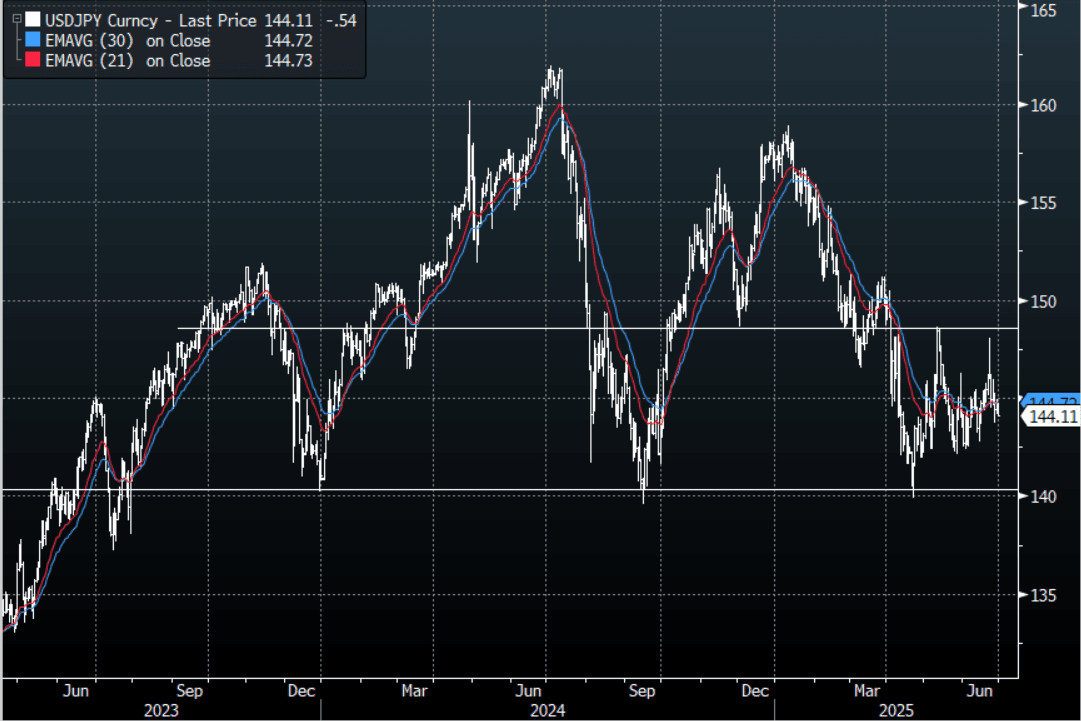

JPY: Asia Wrap - USD/JPY Comes Off, Testing 144.00

The Asia-Pac USD/JPY range has been 144.08 - 144.76, Asia is currently trading around 144.09, -0.40%. USD/JPY has drifted lower in our session, though still in the middle of its wider 142.00 - 148.00 range. "US President Donald Trump characterized trade in cars between the US and Japan as unfair and floated the idea of keeping 25% tariffs on autos in place." (BBG)

- The Real Fly on X: "Trump criticized the U.S.–Japan auto-trade relationship as unfair, referring to Japan’s negotiator as “MR. Japan,” and warned of possible new tariffs ahead of the looming JULY 9 deadline.” https://x.com/The_Real_Fly/status/1939488012741521660

- (Bloomberg) -- Japan's industrial production rose less than expected in May, missing analysts' estimates as the US tariffs hit the nation's exports. Factory output increased 0.5% from the previous month, the Industry Ministry reported Monday. Economists had expected a 3.5% gain. Output fell 1.8% from a year earlier, missing expectations of a 1.6% rise.

- CFTC data shows Asset managers paring back their JPY longs very slightly +93003, while leveraged funds added to their longs again trying to rebuild their position +15935.

- The rejection of 148.00 points to a potential top being in place now and shows just how quick the market is to return to selling USD’s. USD/JPY is looking for a fresh catalyst in the middle of its 142.00 - 148.00 range, while the USD continues to move lower this should see sellers on any bounce for now.

Options : Close significant option expiries for NY cut, based on DTCC data: 143.85($985m), 145.50(845m).Upcoming Close Strikes : 143.85($885m June 30), 145.00($1.02b July 1)

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia Wrap - AUD struggling To Bounce

The AUD/USD has had a range of 0.6527 - 0.6543 in the Asia- Pac session, it is currently trading around 0.6535, +0.08%. A tight range in a very quiet Asian session, US Equity futures have opened strongly in Asia printing new all-time highs, ESU5 +0.4%, NQU5 +0.5% after Canada rescinds its digital services tax. The AUD has surprisingly had very little reaction to this as it still looks for a catalyst to probe above the 0.6550/0.6600 resistance. CFTC Data shows Asset managers increasing their shorts -36967, the Leveraged community has also added to their shorts -22963. Given how poorly the USD is trading one would expect most of these shorts are being expressed in the crosses where the AUD trades poorly particularly against the EUR and GBP.

- Private credit rose 0.5% m/m (estimate +0.6%) in May versus +0.7% in April.

- Melbourne Institute inflation index rose 0.1% m/m in June versus -0.4% in May. Inflation index rose 2.4% y/y versus +2.6% in May.

- (Dow Jones) “Recent turmoil in global financial markets is fueling overseas demand for New South Wales state government bonds, despite concern about a rise in public-sector debt levels in Australia.”

- The AUD/USD is attempting to break through the top of its recent range as the pressure on the USD increases.

- The AUD needs a sustained break above 0.6550/0.6600 to potentially start building momentum for an extended move higher, a close back above 0.6600 and the focus would turn back to 0.6900/0.7000.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6425(AUD836m). Upcoming Close Strikes : 0.67500(AUD1.27b July 2), 0.6600(AUD907m July3).

- AUD/JPY - Today's range 94.15 - 94.54, it is trading currently around 94.25. Choppy price action as the pair establishes a range between 92.00 - 96.00. Should risk build on this move, focus could turn back to the 96.00 area.

Fig 1: AUD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

NZD: Asia Wrap - NZD/USD Looking Towards 0.6100 And Then Beyond

The NZD/USD had a range of 0.6052 - 0.6078 in the Asia-Pac session, going into the London open trading around 0.6070, +0.23%. NZD has drifted back to its highs albeit in a very quiet Asian session. US Equity futures have opened strongly in Asia printing new all-time highs, ESU5 +0.4%, NQU5 +0.5% after Canada rescinds its digital services tax.

- CFTC Data shows Asset Managers have cut their shorts and are now beginning to build a long in NZD +12195, the Leveraged community maintained their short that had just been added to -11981.

- NEW ZEALAND Business Activity & Confidence Up, But Still Off Cycle Highs: The New Zealand ANZ business activity and confidence measures rose in June. On activity we moved back to 40.9, from 34.8 in May, while confidence rebounded to 46.3, from 36.6 prior. The improvement in June follows a move lower in these headline indices since the end of Q1.

- A huge bounce from sub 0.5900 and the NZD has now established a foothold above 0.6000, with the USD breaking lower the NZD/USD looks to be building for a potential break higher of its own. A clear break of 0.6100 could provide the momentum to begin a larger move higher, initially targeting the 0.6400 area.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5850(NZD404m July 1), 0.5800(649m July2)

- AUD/NZD range for the session has been 1.0764 - 1.0799, currently trading 1.0770. The cross is struggling to get any momentum for now. It looks to be in a 1.0750 - 1.0850 range for now as it awaits a catalyst to provide some clearer direction.

Fig 1: NZD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: June Delivers Strong Returns Across the Region.

As the June comes to a close, major bourses have delivered good returns in June, despite the trade war and Iran-Israel conflict. China's major bourses enjoyed gains of 2-5% as Taiwan and the KOSPI were the biggest winners for the major bourses. News filtered through over the weekend that top negotiators from Japan and India have remained in Washington for further talks on trade deals, signs the market has taken as positive following the S&P closing at a record on Friday.

- The Hang Seng was one of the few decliners, down -0.42% today yet remains up +3.8% for June. The CSI300 is flat today and up +2.1% for the month whilst Shanghai Comp gained +0.20% and is up +2.50% for the month. The Shenzhen Comp was the best performer of the major bourses up +0.73% and up +5.10% for the month.

- The TAIEX in Taiwan fell -0.6% today but remains over +14% higher over the month as record inflows continued and the currency surges.

- The KOSPI gained +0.96% today and since the election (and promised new budget) has performed strongly delivering +14.3% in June.

- The FTSE Malay KLCI is flat today and up +1.30% for the month.

- The Jakarta Composite is up +0.26% today and one of the few fallers for the month, losing ground by -3.2%

- The FSTE Straits Times in Singapore is flat and up +1.80% for the month and the PSEi in the Philippines is up +0.40% and +1.46% for June.

- The NIFTY 50 is having a weak start to Monday down -0.35% yet remains up +3.3% for the month.

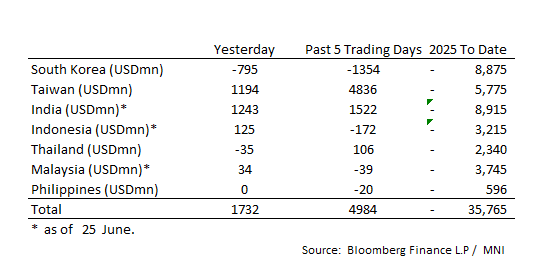

ASIA STOCKS: Taiwan Inflows Continue as India Follows

Taiwan has $5.1bn of Inflows in Four Trading Days.

- South Korea: Recorded outflows of -$795m Friday, bringing the 5-day total to -$1,354m. 2025 to date flows are -$8,875. The 5-day average is -$271m, the 20-day average is +$110m and the 100-day average of -$87m.

- Taiwan: Had inflows of +$1,194m Friday, with total inflows of +$4,836 m over the past 5 days. YTD flows are negative at -$5,775. The 5-day average is +$967m, the 20-day average of +$256m and the 100-day average of -$45m.

- India: Had inflows of +$1,243m as of the 26th, with total inflows of +$1,522m over the past 5 days. YTD flows are negative -$8,915m. The 5-day average is +$304m, the 20-day average of +$51m and the 100-day average of -$21m.

- Indonesia: Had inflows of +$125 as of the 26th with total outflows of -$172m over the prior five days. YTD flows are negative -$3,215m. The 5-day average is -$34m, the 20-day average -$20m and the 100-day average -$30m.

- Thailand: Recorded outflows of -$35m yesterday, with inflows totaling +$106m over the past 5 days. YTD flows are negative at -$2,340m. The 5-day average is +$21m, the 20-day average of -$32m and the 100-day average of -$21m.

- Malaysia: Recorded inflows as of +$34m as of 26th, totaling -$39m over the past 5 days. YTD flows are negative at -$3,745m. The 5-day average is +$2m, the 20-day average of -$23m and the 100-day average of -$21m.

- Philippines: Recorded no flows Friday, with net outflows of -$20m over the past 5 days. YTD flows are negative at -$596m. The 5-day average is -$4m, the 20-day average of -$18m the 100-day average of -$5m.

- WTI finished last week down -12.56% and Brent down -12.00% but has steadied today with modest rises.

- WTI is up +0.23% at US$65.21 bbl, having opened at $65.15.

- Brent is up +0.39% at $67.63 having opened at $67.33.

- The move lower last week for WTI sees it trade below all major moving averages with the nearest being the 50-day EMA at US$65.55

- BBG reports that Money managers boosted short-only bets on the WTI global benchmark by 35,743 lots to 114,848 lots, the biggest gain since last June, in the week ended June 24, according to figures from ICE Futures Europe.

- OPEC+ are again looking at options for further increases in supply according to reports over the weekend. Eight key OPEC+ nations have agreed on 411,000 barrel-a-day increases in each of the previous three months, and several delegates are ready to consider the same hike again for August.

- President Trump has hinted at sanctions relief for Iran if 'they can be peaceful' and US Energy Secretary Wright suggested the US administration is looking to spread 'commerce not conflict.'

Gold Set for Worst Month of 2025

- Gold edged modestly higher in the Asia trading day, gaining +0.15% to US$3,279.45.

- The gains weren't enough to extinguish the losses for the month and bullion remains down -0.30% for June and facing its first monthly loss of 2025.

- Gold traders will eye closely the US data this week for further indications for interest rates as the input into gold's next move.

- Gold has traded below the 50-day EMA of $3,289.72. The first times this year bullion has fallen below the 50-day EMA.

- China's biggest gold and copper producer Zijin Mining Group is to buy a gold project in Kazakhstan for US$1.2bn.

- The Official PMIs followed the familiar theme of recent releases with the PMI manufacturing in mild contraction and the PMI non-manufacturing barely holding in expansion.

- The PMI Manufacturing print of +49.7 was the third successive print below 50. Output and New orders rose relative to last month whilst employment declined.

- The PMI Non-manufacturing print of 50.5 was a modest improvement on last month's release of 50.3 whist New orders up whilst employment was down.

- This is the first full month of data since the agreement between Beijing and Washington to a halt to the trade war.

CHINA: Country Wrap: US Identifies TikTok Buyer

- President Donald Trump said he has identified a buyer for the US operations of TikTok, the social media app owned by Chinese company ByteDance Ltd., but he won’t provide details for two weeks. (source BBG)

- China Securities Journal reports that China may sell ultra long special bonds to aid growth. Cash raised from the bonds may be used to fund the government’s program of subsidizing corporate and household purchases of new equipment and home goods, said Tao Chuan, chief economist at Minsheng Securities Research Institute, according to the report (source China Securities Journal)

- The Official PMIs followed the familiar theme of recent releases with the PMI manufacturing in mild contraction and the PMI non-manufacturing barely holding in expansion. The PMI Manufacturing print of +49.7 was the third successive print below 50. Output and New orders rose relative to last month whilst employment declined. The PMI Non-manufacturing print of 50.5 was a modest improvement on last month's release of 50.3 whist New orders up whilst employment was down. This is the first full month of data since the agreement between Beijing and Washington to a halt to the trade war. (source MNI )

- The Hang Seng was one of the few decliners, down -0.42% today yet remains up +3.8% for June. The CSI300 is flat today and up +2.1% for the month whilst Shanghai Comp gained +0.20% and is up +2.50% for the month. The Shenzhen Comp was the best performer of the major bourses up +0.73% and up +5.10% for the month.

- Yuan Reference Rate at 7.1586 Per USD; Estimate 7.1704

- Bonds have traded in a very tight range all month with the CGB 10yr stuck between 1.64%-1.67% and finishing at 1.65%

INDIA: Country Wrap: States to Issue 2.8tn in July-Sept - RBI

- India’s finance ministry has asked the banks to focus on lending to small and medium enterprises and also to agriculture the secretary at the Department of Financial Services, told reporters in New Delhi Friday. (source BBG)

- Indian states will issue bonds worth 2.87 trillion rupees ($33.6 billion) in the July to September quarter, the Reserve Bank of India said in statement on Friday. (source RBI)

- India’s trade team has extended its stay in Washington to iron out differences as the two sides look to clinch a deal before a July 9 deadline when higher US tariffs are set to kick in, people familiar with the matter said. The in-person negotiations were initially supposed to run through June 27 but were extended by a day, raising hopes of an interim trade deal, said the people, who asked not to be identified as the discussions are private. (source BBG)

- The NIFTY 50 is having a weak start to Monday down -0.35% yet remains up +3.3% for the month.

- The rupee is relatively unchanged this morning at 85.50 and remains down for the month by -0.15%.

- Bonds have leaked higher in yield this month with the 10YR +8bps higher at 6.31%

SOUTH KOREA: Country Wrap: Mortgage Loan Caps Announced

- On the 27th, the government announced unprecedented special measures, including a limit of 600 million won on mortgage loans (main mortgage) in the metropolitan area and regulated areas and a 70% strengthening of the first-ever mortgage loan ratio (LTV). This is due to the judgment that the overheating of housing prices in Seoul can no longer be seen. (source MAEIL)

- As the supplementary budget bill (extra budget) was drawn up twice this year, the "deficit debt" to be paid back by national taxes exceeded 900 trillion won. Deficit debt accounted for more than 70% of the total national debt. According to the National Assembly Budget Office's "Analysis of the Second Supplementary Budget in 2025" on the 30th, the national debt will increase to 130.6 trillion won this year due to the formation of the second supplementary budget. Compared to last year's settlement, it will increase by 125.4 trillion won in a year. (source MAEIL)

- The increase in household loans this month was close to 7 trillion won, the report showed. It has been on the rise for five consecutive months. It is attributed to the fact that apartments in the Gangnam area of Seoul and the "Ma Yongseong" (Mapo, Yongsan, and Seongdong-gu) area have continued to "disappear" with new reported prices every day, and the number of people who want to get mortgage loans (main loans) in a hurry ahead of the implementation of the third phase of the stress total debt repayment ratio (DSR) in July. (source MAEIL)

- The KOSPI gained +0.96% today and since the election (and promised new budget) has performed strongly delivering +14.3% in June.

- The Won had a very strong day gaining +0.94% to 1,348.35 and is up +2.2% for the month.

- Bonds enjoyed lower yields across the curve with the 5-year the best performer. The 10Yr is at 2.82% is modestly higher in yield over the month, having traded in tight ranges.

ASIA FX: USD/KRW Slumps Into Month/Quarter End, USD/TWD Holding Above 29.00

In North East Asia FX, the USD has softened against CNH and KRW, while USD/TWD has struggled for fresh downside after last week's test sub 29.00. USD/HKD remains close to 7.8500, with shorter dated Hibor rates off highs from last week.

- USD/CNH was last near 7.1600, very close to session lows (7.1599). We had a weaker USD/CNY fixing, under 7.1600, which is fresh multi month lows back to Nov last year. The official PMIs for June were also a touch above market forecasts, even if manufacturing stayed in contraction. Downside focus in USD/CNH is likely to be a renewed test of last week's low of 7.1525. A clean break sub 7.1500 could ultimately see the 7.1000 region targeted.

- Spot USD/KRW is testing sub 1350 at the time of writing. We were last around 1348, up close to 1% in KRW terms (levels last seen in Oct last year). Month/quarter end factors may be in play, although this hasn't benefiting TWD today. The Kospi is up around 0.70%, putting the index near 3080, off recent highs, but still up strongly for the month. Offshore investors have sold local shares so far today. Spill over from lower USD/JPY levels (testing sub 144.00) is likely aiding the won.

- USD/TWD spot has crept higher, last back close to 29.19. This is up modestly from Friday closing levels. Focus will remain for this pair on another fresh test 29.00 (lows last Friday were at 28.91).

- Spot USD/HKD is little changed, last near 7.8500, the top end of the peg band.

ASIA FX: USD Weaker As Month/Quarter End Approaches, Trade Talks In Focus

In South East Asia FX, the bias has been for a weaker USD, with PHP and MYR the best performers in spot terms at this stage. IDR has lagged, losing ground modestly against the USD as we approach month/quarter end. Focus remains on trade talks with the US for a number of countries as the expiration date for Trump's tariff pause approaches.

- USD/PHP has continued to track lower, the pair now back sub all of its key EMA support points, the 50-dau at 56.43 breached today. We were last at 56.35, significantly paring month to date losses for the PHP. Downside focus is likely to rest around 56.00 if we see further weakness in oil/energy prices. The Philippines central bank earlier announced its expectations for the 2025 balance of payments deficit. The updated forecast calls for a larger deficit at $6.3bn versus $4bn previously guided, due to amongst other factors, ongoing tariff related risks. This hasn't impacted FX sentiment though.

- USD/THB is back to 32.55/60, still up from recent lows 32.335 seen last week in the pair. We remain sub all key EMAs. Earlier we had May industrial production, which rose 1.88% which was close to expectations. Thailand Finance Minister Pichai Chunhavajira is travelling to the US this evening for trade talks.

- USD/IDR is a little higher, last near 16230, but sit close to recent lows just under 16200. Headlines crossed earlier that Indonesia would relax import rules for 10 commodities, while it also offered the US to invest with Danantara in the critical minerals space within the country (via BBG). These steps are forming part of trade talks with the US.

- USD/MYR is back under 4.2200, up around 0.30% in MYR terms for the session. May lows in the pair came just under 4.2000 in terms of potential downside targets in the pair.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 30/06/2025 | 0600/0800 | ** | Retail Sales | |

| 30/06/2025 | 0600/0800 | ** | Import/Export Prices | |

| 30/06/2025 | 0600/0800 | ** | Retail Sales | |

| 30/06/2025 | 0600/0700 | *** | GDP Second Estimate | |

| 30/06/2025 | 0600/0700 | * | Quarterly current account balance | |

| 30/06/2025 | 0700/0900 | ** | KOF Economic Barometer | |

| 30/06/2025 | 0800/1000 | ** | M3 | |

| 30/06/2025 | 0800/1000 | *** | Bavaria CPI | |

| 30/06/2025 | 0800/1000 | *** | North Rhine Westphalia CPI | |

| 30/06/2025 | 0800/1000 | *** | Baden Wuerttemberg CPI | |

| 30/06/2025 | 0830/0930 | ** | BOE Lending to Individuals | |

| 30/06/2025 | 0830/0930 | ** | BOE M4 | |

| 30/06/2025 | 0830/1030 | ECB de Guindos At IADG Conference | ||

| 30/06/2025 | 0900/1100 | *** | HICP (p) | |

| 30/06/2025 | 1200/1400 | *** | HICP (p) | |

| 30/06/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 30/06/2025 | 1400/1000 | Atlanta Fed's Raphael Bostic - MNI Connect | ||

| 30/06/2025 | 1430/1030 | ** | Dallas Fed manufacturing survey | |

| 30/06/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 30/06/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 30/06/2025 | 1600/1200 | *** | USDA Acreage - NASS | |

| 30/06/2025 | 1600/1200 | ** | USDA GrainStock - NASS | |

| 30/06/2025 | 1700/1300 | Chicago Fed's Austan Goolsbee | ||

| 30/06/2025 | 1900/2100 | ECB Lagarde Opening Remarks At Sintra Forum | ||

| 01/07/2025 | 2300/0900 | ** | S&P Global Manufacturing PMI (f) | |

| 01/07/2025 | 2301/0001 | * | BRC Monthly Shop Price Index | |

| 01/07/2025 | 2350/0850 | *** | Tankan | |

| 01/07/2025 | 0030/0930 | ** | S&P Global Final Japan Manufacturing PMI | |

| 01/07/2025 | 0145/0945 | ** | S&P Global Final China Manufacturing PMI | |

| 01/07/2025 | 0630/0830 | ** | Retail Sales | |

| 01/07/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 01/07/2025 | 0740/0940 | ECB de Guindos Chairs Sintra Panel | ||

| 01/07/2025 | 0745/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 01/07/2025 | 0750/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 01/07/2025 | 0755/0955 | ** | Unemployment | |

| 01/07/2025 | 0755/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 01/07/2025 | 0800/1000 | ** | ECB Consumer Expectations Survey | |

| 01/07/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 01/07/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (Final) | |

| 01/07/2025 | 0840/1040 | ECB Elderson Chairs Sintra Panel | ||

| 01/07/2025 | 0900/1100 | *** | HICP (p) | |

| 01/07/2025 | 1040/1240 | ECB Schnabel Chairs Sintra Panel | ||

| 01/07/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 01/07/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 01/07/2025 | 1330/1430 | BOE Bailey On Panel At Sintra Conference | ||

| 01/07/2025 | 1330/0930 | Fed Chair Jerome Powell | ||

| 01/07/2025 | 1330/1530 | ECB Lagarde On Sintra Panel | ||

| 01/07/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (final) |