MNI EUROPEAN MARKETS ANALYSIS: US Data In Focus Later

- The USD has largely held Monday's gains, with aggregate moves in Tuesday trade modest so far. Some USD/Asia pairs are playing catch up though.

- US yields are down a touch, while equity sentiment is mostly negative in the region. Month end and the Aug 1 trade deadline remain in focus. US-China talks continue in Stockholm today.

- Later preliminary June US trade, May house prices, July consumer confidence and June JOLTS job openings are released. There is also preliminary Q2 Spanish GDP.

MARKETS

US TSYS: Asia Wrap - Yields Drift Lower In A Quiet Session

The TYU5 range has been 110-25+ to 110-28+ during the Asia-Pacific session. It last changed hands at 110-27+, up 0-03 from the previous close.

- The US 2-year yield has shifted lower trading around 3.914%, down 0.01 from its close.

- The US 10-year yield has edged lower trading around 4.402%, down 0.01 from its close.

- The 10-year yield has moved back towards its pivot within the wider range 4.10% - 4.65%, decent supply was seen around 4.30/35% first up. A decent bounce was seen off this support but the move has failed to follow through above 4.40% for now. The Data this week should hopefully provide more clarity going forward.

- Nick Timiraos on X: ”Fed officials expect they will need to resume lowering interest rates eventually—they just aren’t ready to do it this week. The questions dividing them center on what evidence they need to see first, and whether waiting for that clarity turns out to be a mistake.”

- “The Fed was united when officials paused cuts this year after tariffs raised fears of renewed inflation. But with tariff-related price hikes proving milder than feared and signs that hiring may be softening, officials are now fractured into three camps over whether to resume cuts.”

- “The focus will be whether Powell offers any hint of a September rate cut in his press conference Wednesday afternoon, and whether in the coming days and weeks his colleagues begin laying the groundwork for a cut at their next gathering.”

- Data/Events: Advanced Goods Trade Balance, FHFA House Price Index, S&P Corelogic, JOLTS, Conf. Board Consumer Confidence, Dallas Fed Services Activity.

JGBS: Modestly Richer, Strong 2Y Auction, BOJ Starts Two-Day Meeting Tomorrow

JGB futures are modestly stronger, +8 compared to the settlement levels.

- Today, the local calendar will be empty apart from 2-year supply.

- The 2-year bond auction showed strong results today. The low price printed stronger than the Bloomberg-surveyed forecast of 100.09, while the cover ratio increased to 4.4665x from 3.9028x. The auction tail also narrowed compared to last month.

- The Japan Times via BBG - "In an annual white paper on Tuesday the government underlined the need to take all possible measures to realize wage increases that outpace inflation. In an annual white paper on Tuesday the government underlined the need to take all possible measures to realize wage increases that outpace inflation."

- Cash US tsys are ~1bp richer in today's Asia-Pac session after yesterday's modest sell-off. Wednesday's FOMC announcement is widely expected to be a steady rate outcome.

- Cash JGBs are 1-2bps richer apart from the 30-year which is 1bp cheaper. The benchmark 2-year yield is 1.5bps lower at 0.825% versus the cycle high of 0.890%.

- Swaps are mixed, with rates flat to 1bp lower.

- Tomorrow, the local calendar will be empty ahead of the BOJ Policy Decision on Thursday.

AUSSIE BONDS: The Wait Is Over, Q2 CPI Tomorrow Followed By FOMC

ACGBs (YM +1.5 & XM +1.0) are slightly stronger after a subdued data-light session.

- The focus of this week will be tomorrow's Q2 CPI data, which is expected to show the underlying trimmed mean measure making further progress towards the band midpoint of 2.5%. Bloomberg consensus is forecasting a 0.7% q/q rise, bringing the annual rate to 2.7% after 0.7% & 2.9% in Q1. This is slightly higher than the RBA's May Q2 forecast of 2.6%. Services developments will also be monitored. The RBA is expected to cut rates 25bp on August 12.

- Cash US tsys are ~1bp richer in today's Asia-Pac session after yesterday's modest sell-off. Wednesday's FOMC announcement is widely expected to be a steady rate outcome. It’s virtually unanimous that there will be two dissents in favour of a cut at this meeting, with Gov Waller widely expected to do so and Gov Bowman also likely (among analysts who expressed an opinion on this).

- Cash ACGBs are 1-2bps richer with the AU-US 10-year yield differential at -8bps.

- The bills strip is slightly stronger, with pricing flat to +2.

- RBA-dated OIS pricing is softer across meetings today. A 25bp rate cut in August is given an 89% probability, with a cumulative 59bps of easing priced by year-end.

- The AOFM plans to sell A$1200mn of the 2.75% 21 June 2035 bond on Friday.

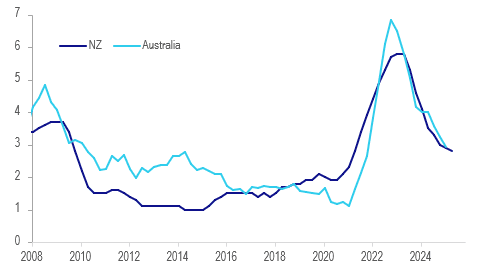

AUSTRALIA: NZ Q2 Core CPI Suggests Small Moderation In Australia

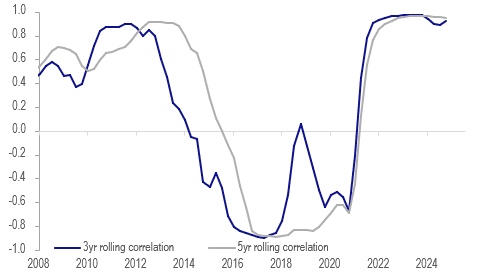

With Australia’s Q2 CPI data released on Wednesday, it is worth looking at NZ developments given the high correlation between the two countries’ inflation rates. With Australia’s headline CPI impacted by government electricity rebates, it is hard to infer any trends. However, the trimmed mean has a 3-year rolling correlation of around 90% with the RBNZ’s measure of core. The two were in line in Q1 at 2.9% and NZ’s Q2 outcome of 2.8% suggests that Australia’s may also post a small decline. This result would be above the RBA’s May Q2 forecast of 2.6% though.

Australia vs NZ underlying inflation y/y%

- NZ-Australia services CPIs also have a correlation of around 90% and in Q2 NZ’s picked up to 4.7% y/y from 4.2%. Q2 seasonally sees an increase in the quarterly rate in services but it would have to be above 1.0% q/q in Australia for the annual rate also to pick up. However, NZ non-tradeables inflation moderated 0.3pp to 3.7% y/y in Q2.

- Both services and non-tradeables in NZ continue to run above Australia’s, as has been the case since mid-2023.

- RBA Governor Bullock noted that in the monthly CPI data durable goods prices were a bit higher. NZ’s goods inflation was steady at 1.4% y/y in Q2. The 3-year rolling correlation between Aus-NZ goods inflation has picked up recently to around 95%.

Australia-NZ core CPI y/y% correlations

Source: MNI - Market News/LSEG/RBNZ

AUSTRALIA: Q2 Core Inflation Expected To Be 0.1pp Above RBA Forecast At 2.7%

Q2 CPI prints Wednesday and will be monitored closely given that the RBA relies on this series with the monthly version not yet complete (due to take place on November 26). Headline inflation continues to be distorted by federal & state government electricity rebates and so attention will remain on the underlying trimmed mean. Bloomberg consensus expects it to rise 0.7% q/q and for the annual rate to ease to 2.7% y/y from Q1’s 2.9%. The RBA’s May forecast was for 2.6% y/y and so a print close to this would likely result in an August cut but steady around Q1 may add doubt.

- Most analysts reporting to Bloomberg are around consensus at 2.6-2.7% y/y but forecasts range from 2.5-2.8% and the quarterly rate 0.5-0.8%. In terms of the major local banks, NAB and Westpac are in line with consensus, CBA expects 0.7% q/q but the annual rate to rise to 2.8%, while CBA has a slightly lower quarterly increase of 0.6% but annual inflation still 2.7%.

- Services inflation will continue to be watched as a measure of domestically-generated pressures. After being sticky through 2024, core services moderated to 3.3% y/y in Q1 from 4.2%.

- Q2 headline CPI is forecast to rise 0.8% q/q and 2.2% y/y after 0.9% q/q and 2.4% y/y in Q1. The RBA projected 2.1% y/y in May. CBA and NAB are in line with consensus, ANZ is forecasting 0.8% q/q & 2.1% y/y but Westpac is higher with 0.9% q/q & 2.3% y/y.

- Monthly June data are also released Wednesday and headline inflation is expected to be steady at 2.1% with forecasts ranging from 2.1% to 2.5%. ANZ and CBA are in line with expectations, NAB is lower at 2% and Westpac higher at 2.3%.

BONDS: NZGBS: Closed At Bests But Only Modestly Richer

NZGBs closed at session bests, 2bps richer across benchmarks.

- The NZ-US 10-year yield differential finished 3bps tighter at +15bps.

- Swap rates closed 2bps lower.

- RBNZ dated OIS pricing closed little changed across meetings. 21bps of easing is priced for August, with a cumulative 35bps by November 2025.

- The local calendar will feature the release of ANZ business confidence for July tomorrow. It continues to point to a gradual recovery in the economy. Cost and price components remain elevated, and inflation expectations are at 2.7% off their low.

- ANZ July consumer confidence is out on Friday. It rose sharply in June to 98.8, the highest this year, but still off December's 100.2. Rate cuts, which take time to be reflected in mortgage payments, have helped improve households' financial situations and reduced the time to buy component.

- June building permits will also be printed on Friday. They rose 10.4% m/m in May, and indicators suggest that the construction sector is recovering.

- On Thursday, the NZ Treasury plans to sell NZ$275mn of the 4.50% May-30 bond and NZ$175mn of the 4.25% May-34 bond.

FOREX: Asia FX Wrap - The USD Correction Could Have More To Go

The BBDXY has had a range of 1207.45 - 1208.74 in the Asia-Pac session, it is currently trading around 1208, +0.05%. The USD’s slide lower finally stalled at the back end of last week and some profit-taking was seen. Yesterday's US-EU trade deal was seen as a big loss for the European Union and this has provided the USD bounce with further tailwinds. There is lots of event risk coming up this week and we are heading into month-end so some caution is warranted, this could potentially see some more paring back of USD shorts. Today is corporate month-end and this could also add to some short-term USD demand putting further pressure on the shorts.

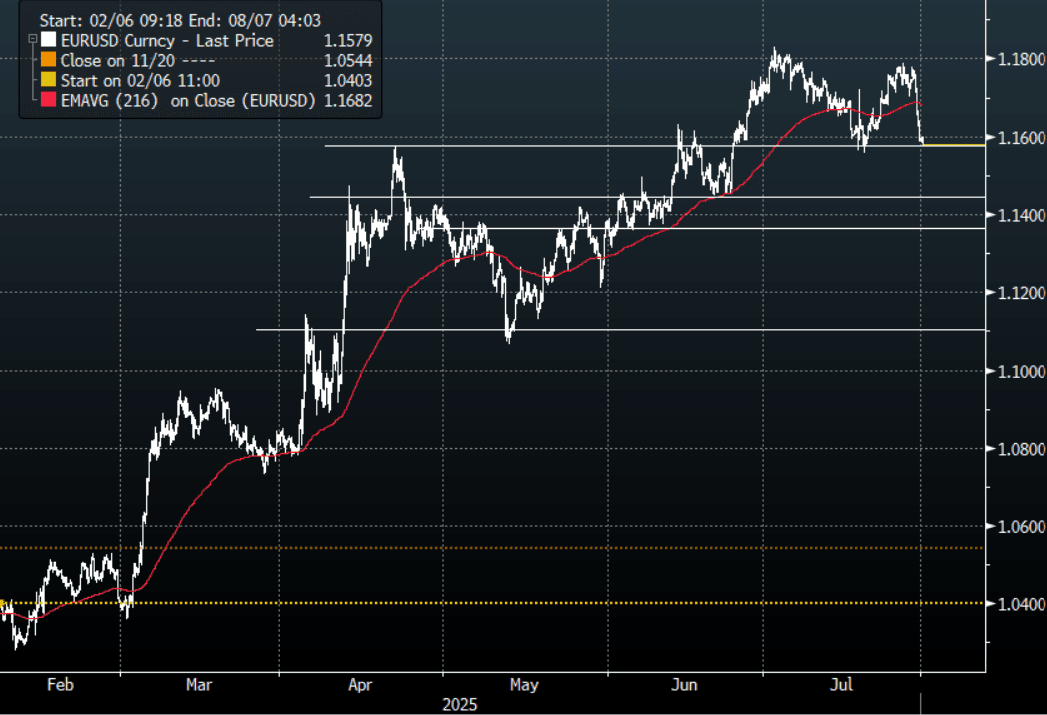

- EUR/USD - Asian range 1.1575 - 1.1599, Asia is currently trading 1.1580. The pair saw some heavy selling putting in a top towards 1.1800 for now. The price looked a little stretched in the short term, and with the USD making a recovery the EUR is set for a correction of sorts. First support around 1.1550 then the more important 1.1350/1.1450 area where I would expect demand first up.

- GBP/USD - Asian range 1.3337 - 1.3362, Asia is currently dealing around 1.3340. This pair looks like it is now breaking lower indicating a deeper correction. Support seen now back towards 1.3100/1.3200 and look for supply now on bounces back towards 1.3500.

- USD/CNH - Asian range 7.1775 - 7.1839, the USD/CNY fix printed 7.1511, Asia is currently dealing around 7.1800. Sellers should be around on bounces while price holds below the 7.2000 area and the PBOC manages the fix lower. Above 7.2000 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.15%, Gold $3311, US 10-Year 4.40%, BBDXY 1208, Crude oil $66.59

- Data/Events : Spain GDP & Retail Sales, EZ ECB 1&3 Year CPI Expectations, France Total Jobseekers

Fig 1: EUR/USD Spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

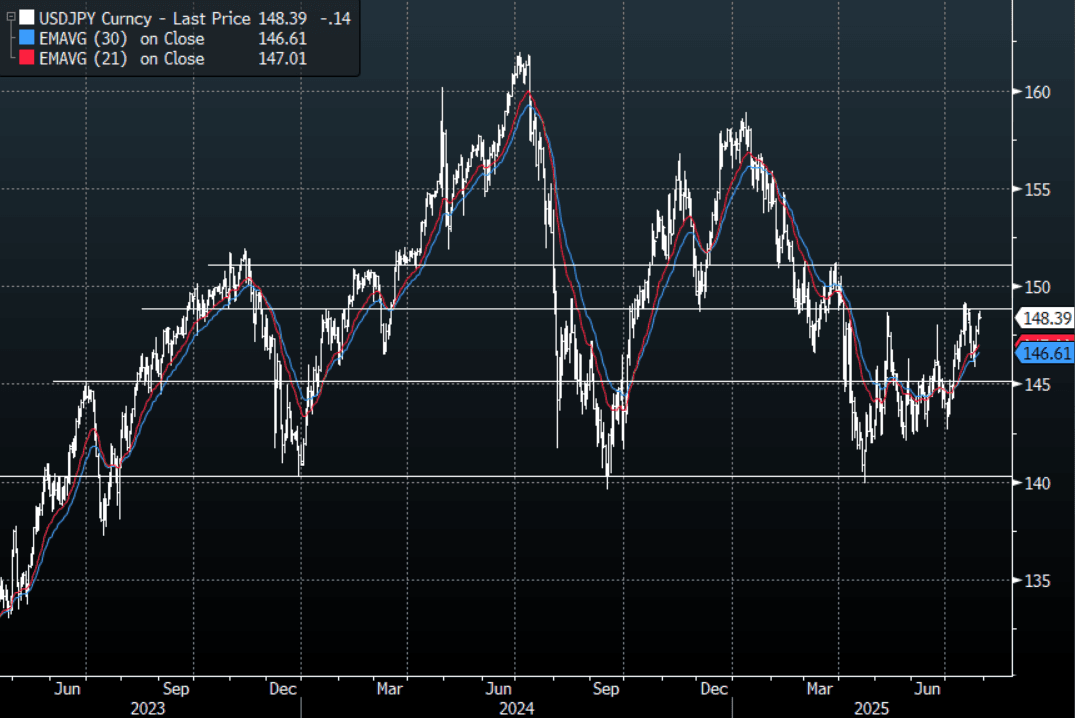

JPY: Asia Wrap - USD/JPY Consolidates On A 148 Handle, Eyes July Highs

The Asia-Pac USD/JPY range has been 148.29 - 148.71, Asia is currently trading around 148.45, -0.05%. USD/JPY continued to build on its momentum higher as the USD shorts reduce risk heading into an important week for risk. Corporate month-end today will add to the headwinds for the USD shorts. A move back above the highs for July would turn the focus towards the pivotal 151.00/152.00 area.

- The Japan Times via BBG - “In an annual white paper on Tuesday the government underlined the need to take all possible measures to realize wage increases that outpace inflation. In an annual white paper on Tuesday the government underlined the need to take all possible measures to realize wage increases that outpace inflation.”

- "X-BOJ DEPUTY GOVERNOR NAKASO: DOLLAR TO RETAIN SUPREMACY AS KEY GLOBAL CURRENCY BUT 'CRACKS' APPEARING AS INVESTORS DIVERSIFY INTO OTHER CURRENCIES. BOJ LIKELY TO RESUME INTEREST RATE HIKE IT RESTORES CONFIDENCE THAT ECONOMY, INFLATION WILL MOVE IN LINE WITH PROJECTIONS. BOJ MUST BE VIGILANT TO UPSIDE RISKS TO INFLATION AS RISING FOOD PRICES COULD LEAD TO OVERSHOOT IN INFLATION EXPECTATIONS" RTRS

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.65($823m).Upcoming Close Strikes : 149.00($1.16b July 30), 147.00($1.52b Aug 1), 146.00($1.43b Aug 1) - BBG.

- CFTC data shows Asset managers surprisingly added slightly to their JPY longs +72326( Last +71610), while leveraged funds have slightly reduced their newly built short JPY position -11571(Last -12606).

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

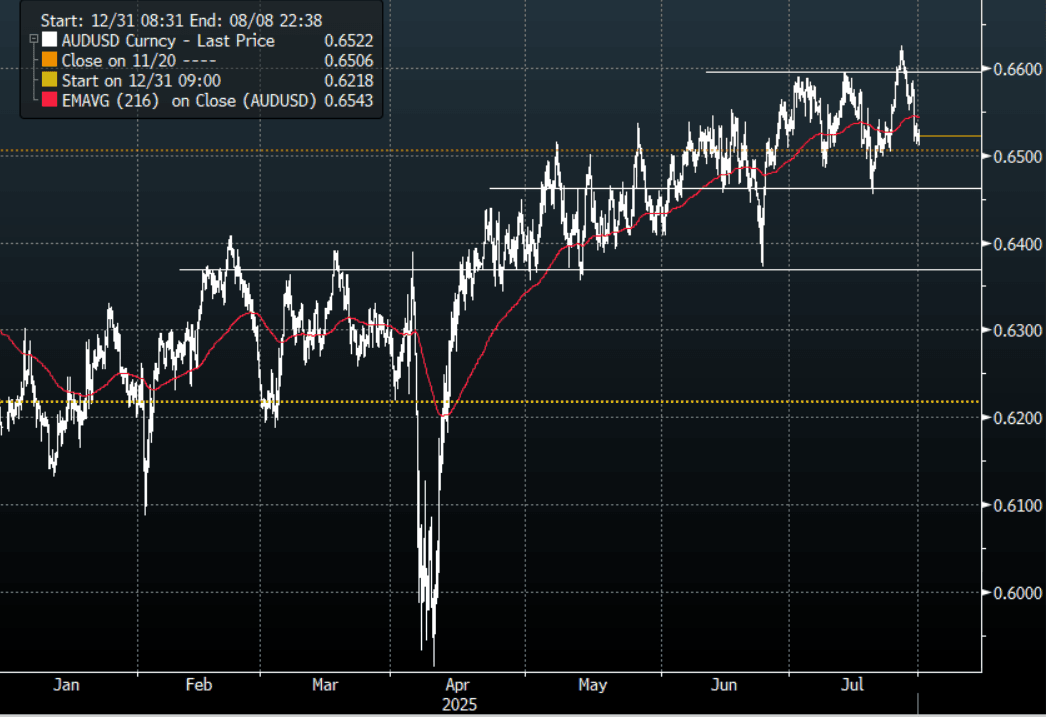

AUD: Asia Wrap - AUD/USD Trades Heavy, Looking Towards Q2 CPI Tomorrow

The AUD/USD has had a range of 0.6512 - 0.6530 in the Asia- Pac session, it is currently trading around 0.6520, -0.02%. The pair could not hold onto its early gains yesterday and slid lower as the USD bounced strongly across the board. The pair failed to gain any momentum above 0.6600 last week and now awaits a very busy calendar this week which could have meaningful implications for risk. Locally the Australian Q2 CPI tomorrow will be closely watched and could provide a catalyst for some movement. Worth keeping in mind it is corporate month-end today and this could see some further headwinds for USD shorts. First support around 0.6450 then the more important 0.6350 area.

- AUSTRALIA: Q2 Core Inflation Expected To Be 0.1pp Above RBA Forecast At 2.7%. Q2 CPI prints Wednesday and will be monitored closely given that the RBA relies on this series with the monthly version not yet complete (due to take place on November 26). Headline inflation continues to be distorted by federal & state government electricity rebates and so attention will remain on the underlying trimmed mean. The RBA’s May forecast was for 2.6% y/y and so a print close to this would likely result in an August cut but steady around Q1 may add doubt.

- CBA Warns Higher CPI Print Could Keep RBA Cautious. A 2.8% print could “be a somewhat awkward 0.2ppt above” the RBA’s latest forecast, but CBA would still expect a 25bp cut on August 12 but see the “decision as not as clear cut as current market pricing suggests”.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD968m), 0.6400(AUD323m). Upcoming Close Strikes : 0.6550(AUD1.01b July30), 0.6600(AUD1.38b July 31), 0.6465(AUD1.01b July31) - BBG

- CFTC Data shows Asset managers added a decent clip to their shorts -53959(Last -38267), the Leveraged community reduced their own shorts to -12010(Last -20048).

- AUD/JPY - Asia-Pac range 96.68 - 96.95, Asia is trading around 96.80. The pair could not hold above 97.00 yesterday. The support between 95.00 - 96.00 held very well last week and the pair is looking to regain its momentum for a move higher. The event-risk coming up this week could provide some short-term headwinds.

Fig 1: AUD/USD spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

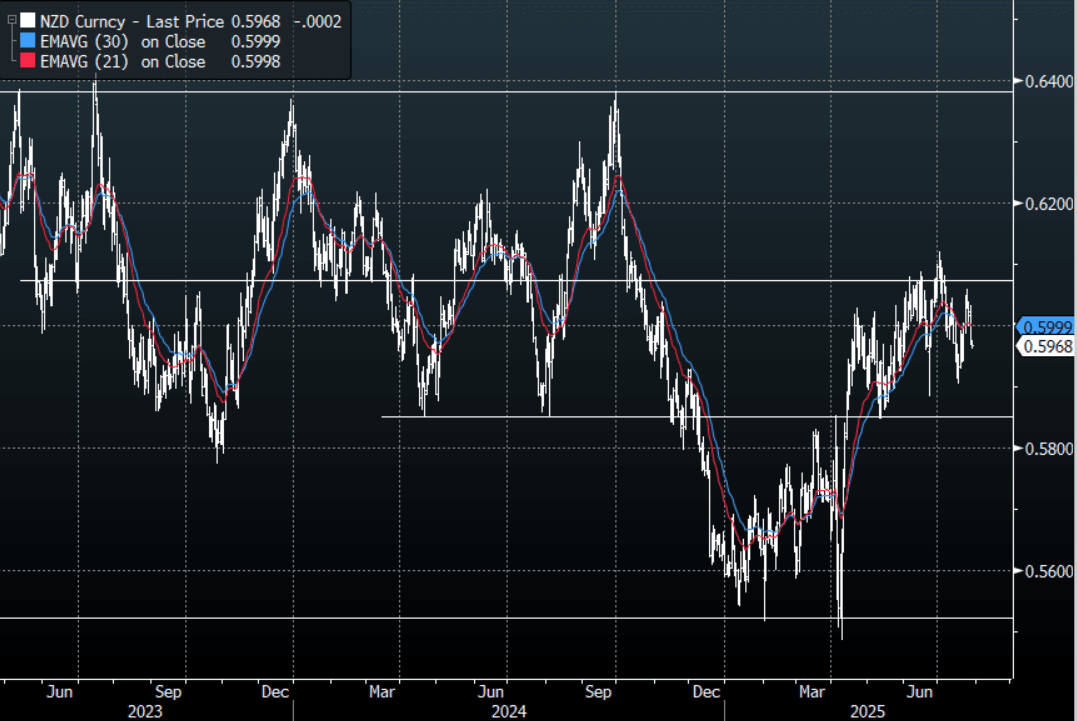

NZD: Asia Wrap - NZD/USD Fails Above 0.6000, Trades Heavy Into Month-End

The NZD/USD had a range of 0.5961 - 0.5976 in the Asia-Pac session, going into the London open trading around 0.5965, -0.08%. The pair could not hold onto its early gains yesterday and slid lower as the USD bounced strongly across the board. There is lots of event risk coming up this week and we are also heading into the corporate month-end today so there could be an extra demand for USD’s further pressuring the USD shorts. Support now seen back towards the 0.5850/0.5900 area.

- "NEW ZEALAND JUNE JOB ADS FALL 2.6% M/M: BNZ" - BBG

- "Job ads index fell 2.6% m/m following a revised 2% decline in May. Drops 2.8% y/y. After a year of relative stability, ads are again on a downwards trajectory: BNZ. “Consistent with the decline in job ads, we expect total employment fell modestly and the unemployment rate climbed to 5.3%” in 2q.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6000(NZD395m July 30), 0.5965(NZD424m July 31). - BBG

- CFTC Data shows Asset Managers again reduced their newly built longs in NZD +5034(Last +8192), the Leveraged community added slightly to their shorts last week -7328(Last -6744).

- AUD/NZD range for the session has been 1.0912 - 1.0930, currently trading 1.0928. Dips back to 1.0850/1.0900 should continue to find support as the pair tries to build momentum to move higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Sentiment Mostly Weaker Ahead Of Key Event Risks

Most regional Asia Pac markets are down in the first part of Tuesday trade. Losses aren't large, but outside of South Korea and Malaysia, trends are negative throughout the region. This follows and overnight session where US markets modestly outperformed EU weakness. So far today, US equity futures are modestly higher, with Nasdaq futures slightly outperforming. This comes ahead of month end late this week.

- Earlier remarks from US Commerce Secretary Lutnick stated that Trump is considering a few deals before the Aug 1 deadline, he will then decide on the unilateral tariff rate. Lutnick stated that an extension of trade truce was likely in terms of the current meetings under with China officials. Trump also pushed back on the idea he was pursuing a summit with China President Xi.

- The China CSI 300 is off a touch, but still close to recent highs. The HSI is down around 1%, but still above the 25300 level. Japan markets are also weaker, the Topix off close to 0.85%. Proximity to earnings outcomes and the Fed decision/data is being cited as a headwind for these markets.

- Taiwan's Taiex is down around 0.85% as well, after a strong run higher in recent weeks. The Kospi is bucking these trends, up nearly 0.60% and firmly above the 3200 level. Earlier we had headlines of corporate tax increases and changes to the capital gains tax, but these shifts have been flagged in the local media prior to today, which may be limiting the market impact.

- In South East Asia, most markets are down, except for Malaysia. Losses are modest though at this stage. Thailand markets have returned, unable to build on recent positive momentum. Thailand has accused Cambodia of violating the recent ceasefire agreement, while a meeting between the countries respective militaries has been postponed.

ASIA STOCKS: Positive Inflow Trends Remain For South Korea & Taiwan

Recent trends remained in place from an equity flow standpoint in EM Asia markets. Inflow momentum remains positive for both the South Korea and Taiwan markets, albeit with slightly better inflow momentum into South Korean stocks yesterday. Generally positive trends for global tech stocks are likely aiding sentiment, with the MSCI IT index closing at record highs yesterday. Samsung's report on a chip deal to supply Tesla also likely aided the South Korean inflow story.

- Earlier new wires reports this morning indicate that South Korea will raise the corporate tax rate back to 2022 levels, while the eased threshold for stock market capital gains tax will also be reversed. These measures have been spoken about recently in the onshore media, so shouldn't surprise the market too much. The Kospi is tracking lower in the first part of dealing today, back under the 3200 level.

- At the end of last week, Indian flow momentum remained negative. India comfortably has the largest YTD outflows in the region.

- Elsewhere aggregate flows were quite modest to start the week. Thailand markets return today after yesterday's break.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 331 | 1339 | -5999 |

| Taiwan (USDmn) | 220 | 1499 | 1915 |

| India (USDmn)* | -164 | -368 | -9172 |

| Indonesia (USDmn) | 3 | 6 | 3608 |

| Thailand (USDmn)* | -8 | 273 | -1951 |

| Malaysia (USDmn) | -24 | -33 | -2887 |

| Philippines (USDmn) | -3 | 4 | -619 |

| Total (USDmn) | 354 | 2720 | -15105 |

| * Data Up To July 25 |

Source: Bloomberg Finance L.P./MNI

OIL: Crude Holds Gains As Uncertainty Rises Over US Action Against Russia

Oil has held onto most of Monday’s gains. It has trended gradually lower through the APAC session though with WTI now down 0.1% to $66.64/bbl, close to the intraday low, after reaching $67.09 early in trading. Brent is 0.1% lower at $69.96/bbl after a high of $70.28. They rose around 2.8% yesterday following US President Trump saying he will bring forward the deadline for an end to hostilities in Ukraine. If effective, the measures he has proposed against Russia, including on purchasers of its crude, could impact global oil supplies.

- Trump said he would bring the ceasefire deadline forward to 10-12 days from July 28. He appears to have lost patience with Russian President Putin saying he’s “not so interested in talking any more” after the latter has said one thing and done another. Trump said that he’ll likely make an announcement Tuesday. The original deadline was September 2.

- With OPEC meeting on August 3 to decide its output target for September and sanctions & trade remaining in focus, attention remains on fundamentals. US industry-based inventory data is released later Tuesday and will be monitored for signs of weakness in demand.

- Later preliminary June US trade, May house prices, July consumer confidence and June JOLTS job openings are released. There is also preliminary Q2 Spanish GDP.

Gold In Narrow Range Ahead Of Key Events This Week

Gold has been range trading during today’s APAC session, holding Monday’s loss, as markets wait for key events taking place this week. Wednesday’s FOMC decision is a particular focus but so too are trade talks, US Q2 GDP and July payrolls on Wednesday and Friday respectively. Bullion is 0.1%lower at $3312.2/oz after falling to a low of $3308.15 followed by a high of $3320.95. The moderately higher US dollar and yields have been pressuring gold.

- US-China talks will continue today. US commerce secretary Lutnick expects that there will be a 90-day extension of the tariff lull. Korea, Thailand and Brazil are working on agreements before the August 1 deadline.

- Bloomberg reported on research from Fidelity stating the possibility that gold could reach $4000/oz by end-2026 driven by Fed rate cuts, weaker greenback and continued central bank buying.

- Silver is down 0.2% to $38.10. It has been also been in a narrow range between $38.198 and $38.047.

- Equities are mixed with the S&P e-mini up 0.1% and KOSPI +0.5% but Hang Seng down 1.0% and Nikkei -0.9%. Oil prices are slightly lower with WTI -0.2% to $66.58/bbl. Copper is down 0.4%.

- Later preliminary June US trade, May house prices, July consumer confidence and June JOLTS job openings are released. There is also preliminary Q2 Spanish GDP.

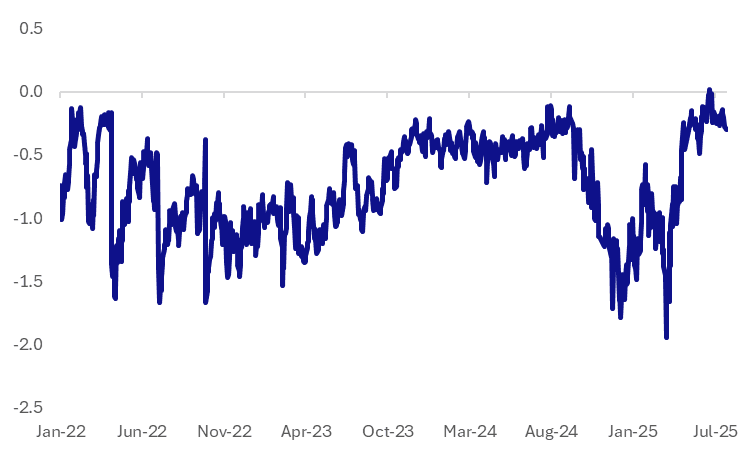

SGD NEER Off Recent Highs, But Still Close To Top End Of Policy Band

The most likely outcome from tomorrow's MAS policy meeting outcome is an unchanged decision, or further easing, which could take the NEER slope back to flat. The sell-side consensus is for no change tomorrow, while the chart below plots the SGD NEER as a percent deviation from the top end of the band (per Goldman Sachs estimates). The elevated level of the NEER relative to the top end of the band suggests some downside risks if we see an MAS easing tomorrow.

- Insofar as the NEER position relative to band extremes gives us a sense of market expectations around the MAS policy meeting outcome, it could be argued the market isn't expecting a dramatic shift at tomorrow's policy announcement.

- At the January 2025 meeting, the NEER was -1.3% from the top end of the band the day before the decision, while in April it was close to -1%. At both of those meetings the MAS eased. Currently we sit around -0.30% from the top end of the band, albeit off recent highs.

- Of course, broader USD weakness, along potential inflows into Singapore in recent months (around the de-dollarization theme) have also aided the SGD and likely boosted it within the policy band range.

- For spot USD/SGD, we sit near 1.2870 in latest dealings, which is close to the 50-day EMA resistance point. Further north is the 100-day, close to 1.2980. Recent lows rest just under 1.2750 for the pair.

Fig 1: SGD NEER - % Deviation From Top End Of The Band (Goldman Sachs)

Source: Goldman Sachs/Bloomberg Finance L.P./MNI

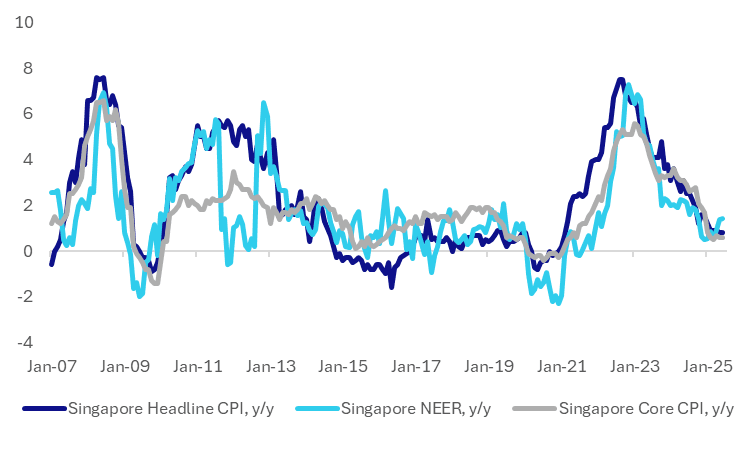

SINGAPORE: MAS Seen On Hold Tomorrow, But Likely To Be A Close Call

The MAS meeting outcome for July will be released tomorrow morning at 8am local time. The sell-side consensus is for now change, although some forecasters expect the central bank to ease further. BBG noted: "Fourteen of 19 economists in a Bloomberg survey forecast the Monetary Authority of Singapore will maintain its settings on Wednesday." (see this link for more details). Our bias is for the central bank to hold policy settings steady, after the central bank eased earlier this year in Jan and April. Still, it is likely to be a close call between on hold and further easing.

- The case for further easing rests with the benign inflation backdrop, coupled with risks to the growth outlook, particularly on the trade side. The first chart below plots the trends in headline and core inflation against the y/y change in the SGD NEER (source MAS).

- Inflation prints have been very modest in recent outturns. Data up to June showed headline at 0.8%y/y, while core was at 0.6%y/y, both unchanged from May readings and slightly below market forecasts. At face value, the +1.4%y/y rise in the NEER looks too firm for such inflation trends.

- At the last policy meeting, the central bank noted: "MAS Core Inflation is now forecast to average 0.5–1.5% in 2025, down from 1.0–2.0% in the January 2025 MPS." Recent inflation outcomes are very much consistent with the outlook from April, if not slightly lower .

Fig 1: Singapore Inflation Trends & SGD NEER Y/Y

Source: Bloomberg Finance L.P./MAS/MNI

- On the growth side, Singapore avoided a technical recession by posting firmer than expected growth in Q2. The advance estimates showed growth up 1.4%q/q, versus 0.8% forecast. The Q1 fall was -0.5%.

- Better exports helped the economy, while construction was also firmer in Q2. There is much uncertainty around the H2 outlook though, particularly on the trade front, given higher tariff levels are coming in for many key global economies/regions.

- At the last meeting the MAS stated on growth: "For 2025 as a whole, Singapore’s GDP growth is expected to slow to 0.0–2.0% from 4.4% last year. "

- At the margin, the central bank may take some comfort from the worst of the possible trade scenarios on tariffs being avoided for now.

- This, along with the economy bouncing nicely in Q2, may see the MAS comfortable to remain on hold tomorrow, albeit still with an eye to ease further.

INDIA: Country Wrap: Trade Negotiations with US Facing Hurdles

- India's trade deal negotiations with the US face hurdles as the White House shifts its demands, seeking a comprehensive Phase 1 agreement before any signing. Trump's focus on a single overall tariff figure, like the EU's 15%, complicates matters given India's higher tariff structure. Securing win-win opportunities and addressing Trump's commercial agenda are crucial for progress. (source EC Times)

- The Reserve Bank of India will withdraw excess liquidity from the system through a three-day variable rate reverse repurchase auction. States are due to sell INR300b ($3.5b) of bonds at a weekly auction. (source RBI )

- The RBI appears to be conducting the biggest FX intervention in the region, but official data actually show more limited buying. The RBI is continuing to build FX reserves and maintain currency competitiveness and has also managed to reduce its net short dollar forward position from its peak in February of $88b to $65b by end-May (including forwards with maturity of over 1 year), suggesting some ongoing dollar demand” (source BBG)

- The NIFTY 50 fell into yesterday's close to finish down -0.6% and has opened flat in this morning's trade.

- The Rupee is down in line with regional trends, lower by -0.20% to 86.84.

- Bonds are opening better bid with the 10yr at 6.36%, from last night's close of 6.37%

SOUTH KOREA: Country Wrap: Finance Minister in Washington on Trade Talks

- The presidential office said Monday the United States has been pressing South Korea to further open its agricultural and livestock markets in trade negotiations ahead of the tariff deadline, while Seoul is working to minimize concessions. Woo Sang-ho, senior presidential secretary for political affairs, made the remarks as South Korea continues talks with Washington to avert the 25 percent reciprocal tariffs before the Aug. 1 deadline set by the Donald Trump administration. "It is true that the U.S. side is exerting very strong pressure in the tariff negotiations, particularly in the agricultural and livestock sectors," Woo said in a briefing. "The government is striving to minimize concessions in order to protect domestic industries as much as possible." (source Yonhap)

- Finance Minister Koo Yun-cheol will hold high-level trade talks with his U.S. counterpart in Washington later this week, the finance ministry said Monday, as the Aug. 1 deadline for tariff negotiations approaches. Koo will depart Tuesday for the U.S. capital, where he will hold talks with U.S. Treasury Secretary Scott Bessent on Thursday (local time), just one day before the United States is expected to resume hefty tariff enforcement on South Korean goods. The minister had originally been slated to attend a "2+2" meeting last week with Trade Minister Yeo Han-koo, along with Bessent and U.S. Trade Representative Jamieson Greer. However, the talks were postponed due to scheduling conflicts of Bessent. (source Yonhap)

- The Kospi is bucking weaker regional trends, up nearly 0.60% and firmly above the 3200 level. Earlier we had headlines of corporate tax increases and changes to the capital gains tax, but these shifts have been flagged in the local media prior to today, which may be limiting the market impact.

- The Won is weaker again today in line with regional trends, off by -0.15% to 1,391.30

- The KTB curve has rallied again today with yield 1-2bps lower. KTB 10 yr at 2.83% (following yesterday's close of 2.84%)

CHINA: Country Wrap: Manufacturing Trade with Europe Growing

- China's manufacturing hub enhances economic and trade exchanges with Europe as the growing popularity of products from Guangdong in Europe is underpinned by strengthening China-Europe ties, a well-developed international logistics network, and increasingly diversified economic and trade cooperation. (source XINHUA)

- China has recently accelerated the integration of sci-tech innovation with industrial innovation, demonstrating remarkable achievements in pursuing high-quality development. * The secret behind the innovation boom lies in China's robust industrial ecosystem, which is built on a policy framework to improve relevant services and help translate patents into products. * Going forward, China will strengthen the principal position of enterprises in sci-tech innovation, thereby creating a stronger synergy between scientific and industrial innovation. (source XINHUA)

- The China CSI 300 is off a touch, but still close to recent highs. The HSI is down around 1%, but still above the 25300 level. Japan markets are also weaker, the Topix off close to 0.85%. Proximity to earnings outcomes and the Fed decision/data is being cited as a headwind for these markets.

- Yuan Reference Rate at 7.1511 Per USD; Estimate 7.1909

- The yield on the CGB 10yr has inched up to 1.73% with bond futures lower for the seventh day out of eight.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 29/07/2025 | 0600/0800 | Flash Quarterly GDP Indicator | ||

| 29/07/2025 | 0700/0900 | *** | GDP (p) | |

| 29/07/2025 | 0800/1000 | ** | ECB Consumer Expectations Survey | |

| 29/07/2025 | 0830/0930 | ** | BOE Lending to Individuals | |

| 29/07/2025 | 0830/0930 | ** | BOE M4 | |

| 29/07/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 29/07/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 29/07/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 29/07/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 29/07/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 29/07/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 29/07/2025 | 1400/1000 | *** | Conference Board Consumer Confidence | |

| 29/07/2025 | 1400/1000 | *** | JOLTS jobs opening level | |

| 29/07/2025 | 1400/1000 | *** | JOLTS quits Rate | |

| 29/07/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 29/07/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 29/07/2025 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note | |

| 30/07/2025 | - | Bank of Japan Meeting | ||

| 30/07/2025 | 0130/1130 | *** | CPI inflation | |

| 30/07/2025 | 0130/1130 | *** | CPI Inflation Monthly | |

| 30/07/2025 | 0530/0730 | *** | GDP (p) | |

| 30/07/2025 | 0530/0730 | ** | Consumer Spending | |

| 30/07/2025 | 0600/0800 | ** | Retail Sales | |

| 30/07/2025 | 0600/0800 | ** | Retail Sales | |

| 30/07/2025 | 0600/1400 | ** | MNI China Money Market Index (MMI) | |

| 30/07/2025 | 0700/0900 | ** | Economic Tendency Indicator | |

| 30/07/2025 | 0700/0900 | *** | HICP (p) | |

| 30/07/2025 | 0700/0900 | ** | KOF Economic Barometer | |

| 30/07/2025 | 0800/1000 | *** | GDP (p) | |

| 30/07/2025 | 0800/1000 | *** | GDP (p) | |

| 30/07/2025 | 0800/1000 | ECB Wage Tracker | ||

| 30/07/2025 | 0900/1100 | * | Consumer Confidence, Industrial Sentiment | |

| 30/07/2025 | 0900/1100 | *** | EMU Preliminary Flash GDP | |

| 30/07/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 30/07/2025 | 1215/0815 | *** | ADP Employment Report | |

| 30/07/2025 | 1230/0830 | *** | GDP / PCE Quarterly | |

| 30/07/2025 | 1230/0830 | *** | Treasury Quarterly Refunding | |

| 30/07/2025 | 1345/0945 | *** | Bank of Canada Policy Decision |