MNI EUROPEAN MARKETS ANALYSIS: US CPI In Focus Later

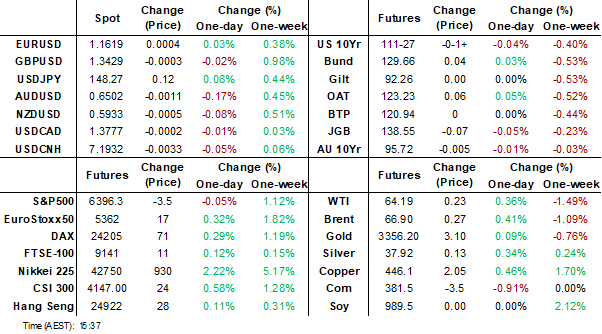

- The RBA cut rates as expected by 25bps, taking the policy rate to 3.60%. The RBA Board stated that “labour market conditions remain a little tight” compared to July’s “conditions remain tight”. Market reaction has been fairly limited, with the AUD down slightly, while OIS is also off a touch.

- In the equity space, Japan markets outperformed, while trends were mostly steadier elsewhere. As widely expected, the US-China tariff trade truce was extended.

- US July CPI data are forecast to show both core and headline ticking up 0.1pp to 3.0% and 2.8% respectively (see Hidden PDF) and will be monitored for signs of any tariff impact. A higher-than-expected print could pressure oil as demand concerns would increase. The market has around an 85% chance of a rate cut for the Fed’s September meeting.

- July US NFIB small business optimism, real earnings and budget data are also released, as well as UK labour data and euro area/German August ZEW sentiment. The Fed’s Barkin and Schmid speak on the economy.

MARKETS

US TSYS: Asia Wrap - Market Eyes CPI, Very Quiet Asian Session

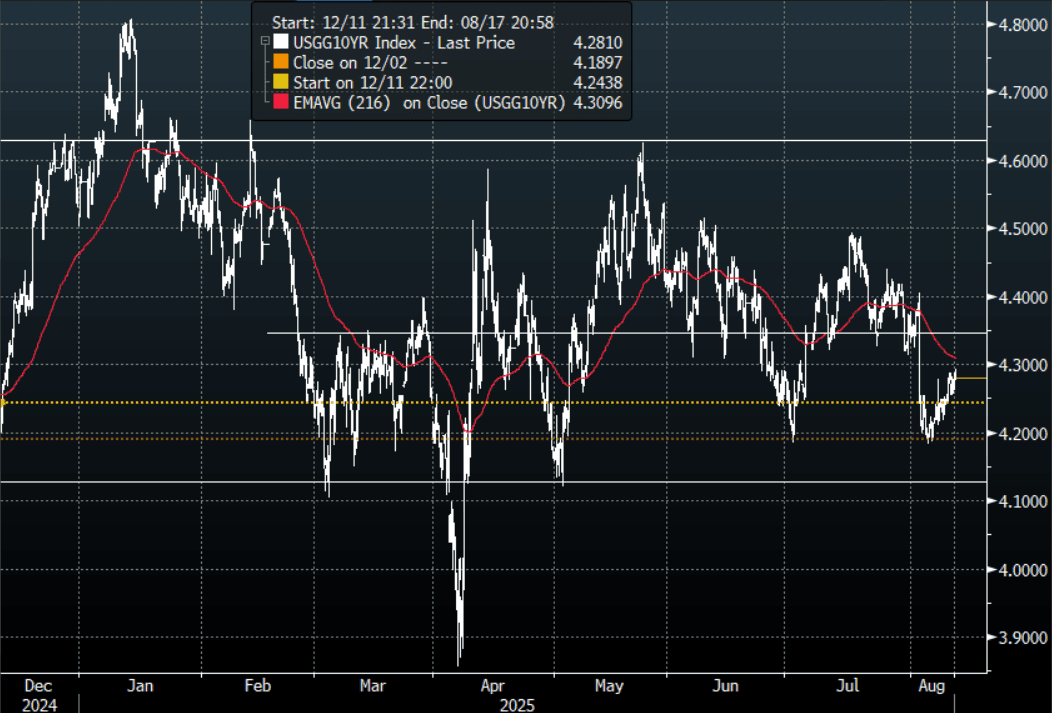

The TYU5 range has been 111-23 to 111-26 during the Asia-Pacific session. It last changed hands at 111-25, down 0-03+ from the previous close. All eyes on the US CPI tonight to confirm if there any signs of inflation taking hold.

- The US 2-year yield is trading around 3.768%.

- The US 10-year yield is trading around 4.283%.

- The 10-year yield had a powerful move lower in reaction to the NFP data, breaking below its 4.30% pivot within the wider range 4.10% - 4.65%. This now turns momentum lower in yields and you could expect buyers of treasuries on bounces back towards 4.30/35% now looking to initially test the 4.10% area.

- MNI US CPI Preview: High Early Bar To September Fed Hold. The CPI report for July is released on Tuesday Aug 12, at 0830ET. Consensus sees core CPI inflation at a seasonally adjusted 0.3% M/M in June and unrounded analyst estimates broadly echo this with a median 0.32% M/M. It would mark a further acceleration from 0.23% M/M in June and 0.13% M/M in May for its fastest pace since January, with the latest firming seen coming from core goods inflation doubling to 0.4% M/M.

- Truflation on X: “July BLS CPI FORECAST: 2.8% YoY. Tariffs are biting, the labor market is cooling, and consumers are wobbling, pointing to slower growth. Could this signal upside risks to inflation? July highlights, goods prices accelerating as tariffs pass through; services cooling (but still supported by wage growth). Biggest upward contributors: Education +0.7% MoM (+2.9% YoY) · Utilities +0.6% (+4.6%) · Health +0.5% (+3.0%) · Alcohol & Tobacco +0.6% (+3.1%). Biggest downward contributors: Food −0.6% MoM (+2.7% YoY) · Housing −0.5% (+0.8% YoY)

- Data/Events: NFIB Small Business Optimism, CPI, Federal Budget Balance

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Slightly Cheaper Ahead Of US CPI, PPI & 5Y Supply Tomorrow

JGB futures are weaker but off lows, -9 compared to the settlement levels.

- Cash US tsys are little changed in today's Asia-Pac session ahead of today's US CPI data.

- (MNI) The CPI report for July is released on Tuesday Aug 12, at 0830ET. Consensus sees core CPI inflation at a seasonally adjusted 0.3% M/M in June and unrounded analyst estimates broadly echo this with a median 0.32% M/M. It would mark a further acceleration from 0.23% M/M in June and 0.13% M/M in May for its fastest pace since January, with the latest firming seen coming from core goods inflation doubling to 0.4% M/M.

- (Bloomberg) -- Bond investors betting on a Federal Reserve interest rate cut next month face a potential roadblock: inflation. July's consumer price index, due on Tuesday, will give traders clues on how President Donald Trump's tariffs are affecting costs. Economists surveyed by Bloomberg expect the annual core inflation rate to rise to 3%, the highest since February.

- Cash JGBs are showing a modest sell-off across benchmarks, led by the 30-year. The benchmark 10-year yield is 0.9bp higher at 1.499% versus the cycle high of 1.616%.

- Swap rates are flat to 1bp higher, with a steepening bias.

- Tomorrow, the local calendar will see PPI and Machine Orders data alongside 5-year supply.

AUSSIE BONDS: RBA Cuts As Expected, Limited Reaction

ACGBs (YM -0.5 & XM -1.0) are moderately richer after the RBA cut the cash rate by 25bps to 3.60%.

- The Board noted that inflation continues to moderate toward the 2–3% range. Trimmed mean inflation fell to 2.7% and headline inflation to 2.1% in the June quarter. Domestic demand is gradually recovering, household incomes have risen, and labour market conditions, though easing, remain tight.

- With 75bps of cuts this year, the Board remains cautious but ready to respond to shifts in global or domestic conditions, maintaining its focus on price stability and full employment.

- Cash ACGBs are 1-2bps richer after the RBA decision, with the AU-US 10-year yield differential at -2bps.

- Swap rates are 2-4bps lower after the decision, with the 3s10s curve steeper.

- The bills strip has richened since the decision but sits flat on the day.

- RBA-dated OIS pricing is flat to 3bps softer across meetings after the decision, mid-2026 leading. A 25bp rate cut in August was given a 97% probability today. A cumulative 36bps of easing priced by year-end.

- Tomorrow, the local calendar will see the Q2 Wage Price Index.

- The AOFM plans to sell A$1200mn of the 4.25% 21 December 2035 bond tomorrow and A$1000mn of the 2.75% 2 1 November 2029 bond on Friday.

RBA Cuts, Labour Market Now Only “A Little Tight”

The RBA made the unanimous decision to cut rates 25bp to 3.60% today as expected. There was a change in the statement language on the labour market. It also presented updated staff forecasts, which given the economy had developed close to the May expectations showed few major changes. The inflation trajectory is unchanged despite a lower cash rate assumption over 2026, which the Board reiterated showed a “gradual easing path”. With the extension of the forecasts to Q4 2027, core inflation now reaches the mid-point of the band.

- The Board stated that “labour market conditions remain a little tight” compared to July’s “conditions remain tight”. “Tight” was removed from the paragraph on the lagged impact of policy on decision making. “The labour market remains strong” was changed to “labour market conditions easing slightly” in the penultimate paragraph of today’s statement.

- Trimmed mean inflation continues to be expected to be at 2.6% in Q4 2025 and then stay there until Q4 2027 when it reaches 2.5%. Q2 2025 was 0.1pp higher than forecast in May at 2.7%. Headline also moderates towards 2.5% as government rebates drop out.

- Q4 2025 GDP growth was revised down 0.4pp to 1.7% driven by lower public demand expectations. Export growth has also been revised down in 2025.

- The unemployment rate projections were unchanged with it reaching 4.3% and then staying there. Employment growth was revised higher in the near-term and was then little changed. Wages growth was revised slightly lower. Productivity was revised down in 2027 with it only briefly at 1%.

- There was little change to trading partner GDP projections despite the Board saying “there is a little more clarity on the scope and scale of US tariffs” suggesting that the “more extreme outcomes” should be “avoided”.

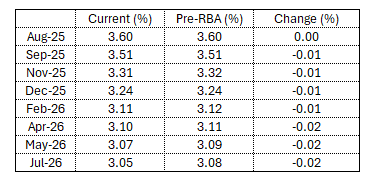

STIR: RBA Dated OIS Slightly Softer After RBA Cuts 25bps

RBA-dated OIS pricing is flat to 2bps softer across meetings after the decision, with mid-2026 leading.

- A 25bp rate cut in August was given a 97% probability.

- A cumulative 36bps of easing priced by year-end.

Figure 1: RBA-Dated OIS – Current Vs. Pre-RBA

Source: Bloomberg Finance LP / MNI

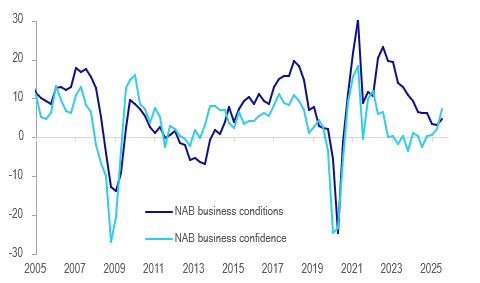

AUSTRALIA DATA: Business Outlook May Have Turned

NAB’s measure of business confidence can be volatile but it has been trending higher since April and printed at 7 in July up from 5 in June and -2 in March signalling an improvement in how firms see the outlook. Business conditions moderated to 5, but are still above every month this year except June, which was revised down 2 points to 7. The activity components moderated in July but generally remained at levels above May.

Australia NAB business confidence vs conditions

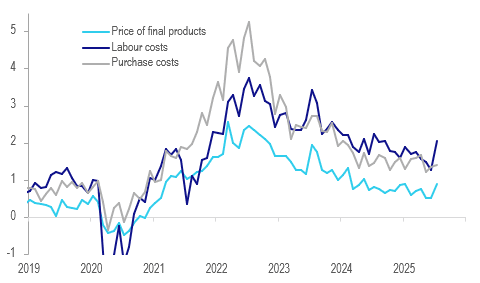

- The July price/cost components of the survey were consistent with other indicators suggesting that disinflation may have stabilised. Labour costs rose 2.1% 3m/3m but this measure usually picks up in July due to wage increases, including the minimum wage, scheduled for the July 1 start to the financial year. But prices of final products rose 0.9% 3m/3m, highest in over a year, and retail prices were up 1.1%. Purchase costs increased 1.4%, the highest in 3-months.

- After picking up to 3.6 in June, employment moderated back to 1.4 in July below the 2.7 series average. It has been trending down signalling lower labour demand. July jobs data print on Thursday and consensus is forecasting a 25k increase and 0.1pp drop in the unemployment rate to 4.2%.

- Forward orders continued to hover around neutral at -0.2 in July after +0.2 but above the -3.3 average of the last 24 months. Exporters sales were weak at -3.6 following June’s -3.1.

Australia NAB business prices/costs 3m/3m%

Source: MNI - Market News/LSEG

BONDS: NZGBS: Subdued Session Ahead Of US CPI Data

NZGBs closed little changed after trading in narrow ranges on a data-light day.

- Cash US tsys are little changed in today's Asia-Pac session ahead of today's US CPI data.

- (MNI) The CPI report for July is released on Tuesday Aug 12, at 0830ET. Consensus sees core CPI inflation at a seasonally adjusted 0.3% M/M in June and unrounded analyst estimates broadly echo this with a median 0.32% M/M. It would mark a further acceleration from 0.23% M/M in June and 0.13% M/M in May for its fastest pace since January, with the latest firming seen coming from core goods inflation doubling to 0.4% M/M.

- Swap rates are unchanged.

- With the next RBNZ meeting approaching (August 20), this week contains a number of high frequency releases that the MPC monitors and should give a sense for how the economy began Q3.

- July card spending is out tomorrow and while it is off its lows, growth has remained soft. There could be some payback in the month following the 0.5% m/m rise in June.

- RBNZ dated OIS pricing is unchanged across meetings. 23bps of easing is priced for August, with a cumulative 40bps by November 2025.

- On Thursday, the NZ Treasury plans to sell NZ$200mn of the 3.00% Apr-29 bond and NZ$250mn of the 2.75% Apr-37 bond.

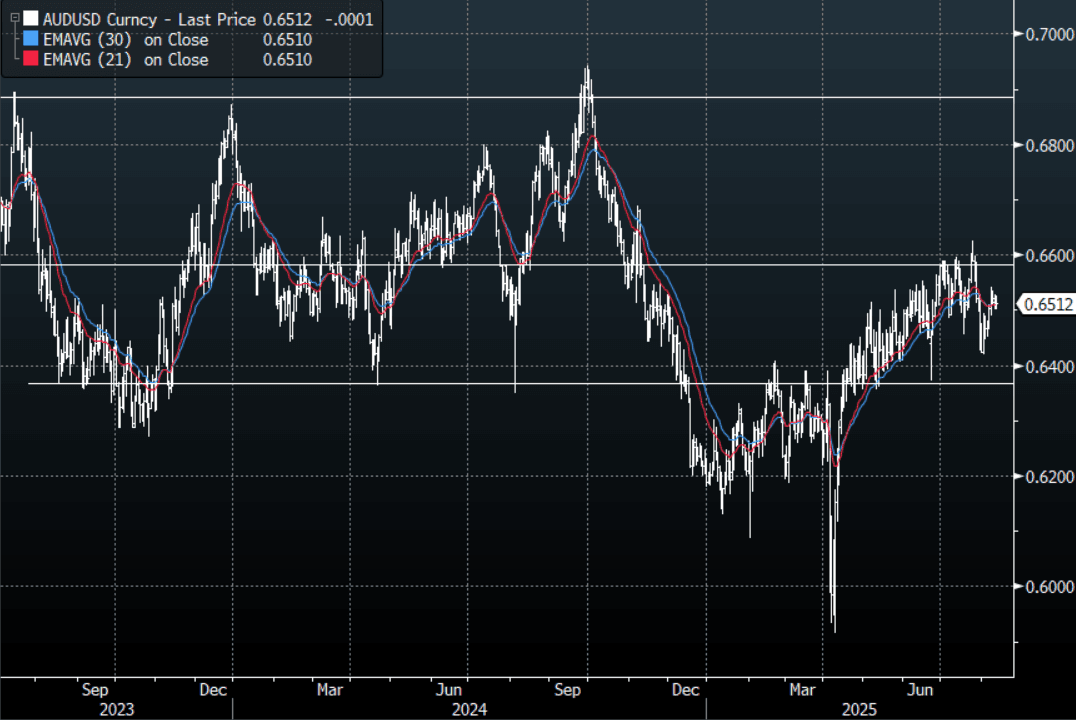

AUD: Asia Wrap - AUD Dips In Reaction To Cut, Focus Turns To Press Conference

The AUD/USD has had a range of 0.6500 - 0.6526 in the Asia- Pac session, it is currently trading around 0.6510, -0.05%. Risk has traded a little higher in our session, E-minis +15%, NQU5 +0.15%. The AUD/USD has moved a couple of spreads lower in reaction to the RBA cutting rates by 25bps. Focus will now turn to the press conference, then the US CPI tonight.

- “ RBA Says: Will Be Attentive to Data, Evolving Assessment of Risks, Sees Risk Households, Firms Delay Spending, Policy Well Placed to Respond Decisively to Global Factors, Forecasts Assume Trade Concerns Weigh on Aust. Inflation, Trade Policy Expected to Have Adverse Effect on Global Eco.” - BBG

- "Australian Consumer Confidence Dn 1.3 Pts Last Week - ANZ Roy Morgan" - DJ

- AUSTRALIA DATA: Business Outlook May Have Turned. NAB’s measure of business confidence can be volatile but it has been trending higher since April and printed at 7 in July up from 5 in June and -2 in March signalling an improvement in how firms see the outlook. Business conditions moderated to 5, but are still above every month this year except June, which was revised down 2 points to 7. The activity components moderated in July but generally remained at levels above May.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6565(AUD908m). Upcoming Close Strikes : 0.6575(AUD646m Aug 13), 0.6600(AUD1.25b Aug 14) - BBG

- CFTC Data shows Asset managers added to their shorts -60729(Last -49183), the Leveraged community added very slightly to their own shorts -13997(Last -13823).

- AUD/JPY - Asia-Pac range 96.37 - 96.83, Asia is trading around 96.60. The pair has bounced nicely and is testing its first resistance around the 96.50 area. There should be sellers around here initially, a sustained break below 94.50/95.00 is needed to signal a deeper move lower or a break above 97.50 would reinstate the momentum higher.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

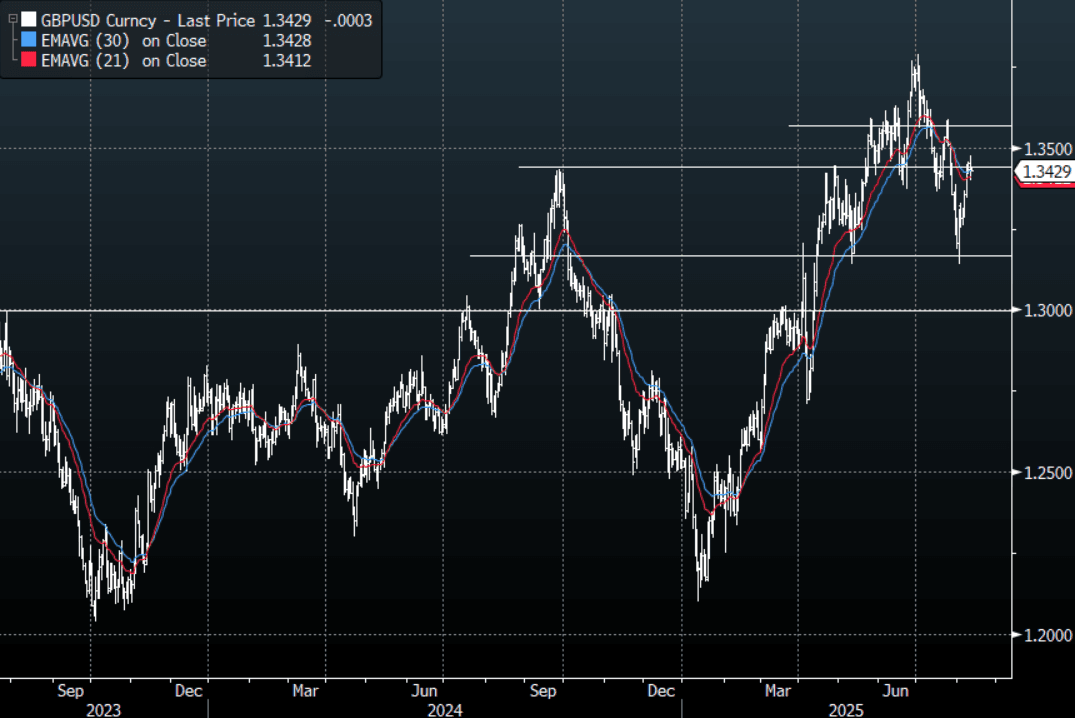

FOREX: Asia FX Wrap - USD Treads Water Ahead Of CPI

The BBDXY has had a range of 1206.70 - 1207.69 in the Asia-Pac session, it is currently trading around 1207, -0.10%. The USD bounced in the N/Y Session as some shorts pared back their exposure as we look toward the US CPI tonight. A sustained break back below 1198 points to a retest of the lows, and a bounce back towards 1220/1230 should probably be faded initially. Where the CPI comes in tonight will determine which level gets tested.

- EUR/USD - Asian range 1.1610 - 1.1625, Asia is currently trading 1.1620. The pair has bounced nicely off the important 1.1300/1.1400 area. The market has stalled at its first attempt to challenge the resistance around the 1.1700 area. Having moved away from 1.1700 the US CPI tonight will determine if we have another go at it.

- GBP/USD - Asian range 1.3426 - 1.3440, Asia is currently dealing around 1.3430. The pair bounced nicely off the 1.3100/1.3200 support area. Sellers saw the move higher stall just above 1.3450 and the US CPI will have a say in if that is now the top in the short-term.

- USD/CNH - Asian range 7.1895 - 7.1965, the USD/CNY fix printed 7.1418, Asia is currently dealing around 7.1930. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.07%, Gold $3352, US 10-Year 4.283%, BBDXY 1207, Crude Oil $64.18

- Data/Events : EZ Zew Survey, Germany Zew Survey/Current Account Balance

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

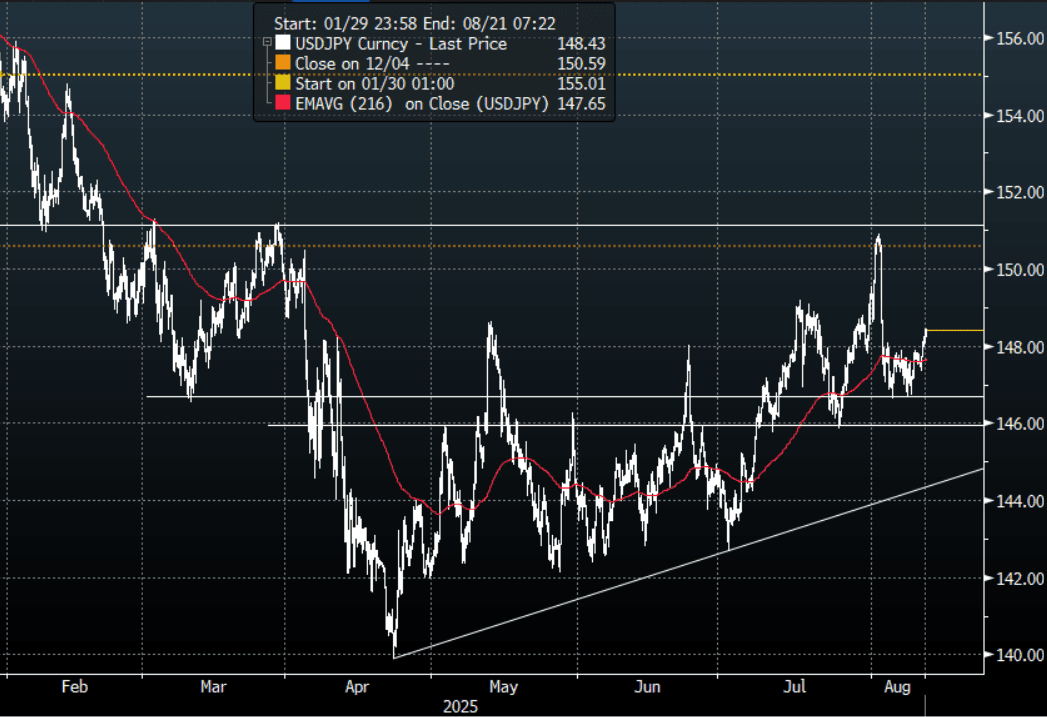

JPY: Asia Wrap - USD/JPY Probes Above 148 As Shorts Pared Back Into US CPI

The Asia-Pac USD/JPY range has been 148.05 - 148.45, Asia is currently trading around 148.45, +0.19%. USD/JPY is probing above 148.00 as the market pares back on some USD’s shorts going into the US CPI tonight. Price is holding above the support area between 146.00/147.00, a move sub 145.00 is needed to turn momentum lower once more, until then the 145.00-151-00 range should dominate. US CPI tonight will determine which end of the range is tested.

- MNI US CPI Preview: High Early Bar To September Fed Hold. The CPI report for July is released on Tuesday Aug 12, at 0830ET. Consensus sees core CPI inflation at a seasonally adjusted 0.3% M/M in June and unrounded analyst estimates broadly echo this with a median 0.32% M/M. It would mark a further acceleration from 0.23% M/M in June and 0.13% M/M in May for its fastest pace since January, with the latest firming seen coming from core goods inflation doubling to 0.4% M/M.

- (Bloomberg) -- Bond investors betting on a Federal Reserve interest rate cut next month face a potential roadblock: inflation. July’s consumer price index, due on Tuesday, will give traders clues on how President Donald Trump’s tariffs are affecting costs. Economists surveyed by Bloomberg expect the annual core inflation rate to rise to 3%, the highest since February.

- Options : Close significant option expiries for NY cut, based on DTCC data: 147.30($878m), 146.00($597m).Upcoming Close Strikes : 147.00($1.01b Aug 13), 150.25($1.47b Aug 13) - BBG.

- CFTC data shows asset managers reduced their JPY longs +60532( Last +75119), leveraged funds slightly reduced their newly built short JPY position -29308(Last -31280).

Fig 1 : USD/JPY Spot H2 Chart

Source: MNI - Market News/Bloomberg Finance L.P

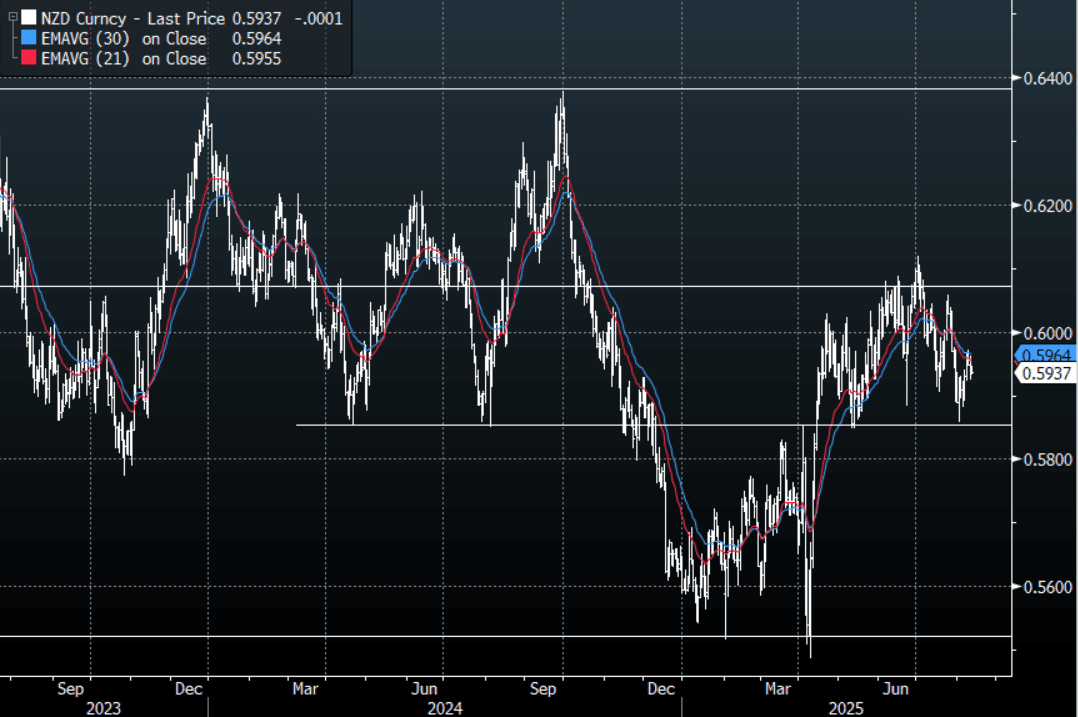

NZD: Asia Wrap - NZD/USD Consolidating On A 0.59 Handle, Awaits US CPI

The NZD/USD had a range of 0.5933 - 0.5946 in the Asia-Pac session, going into the London open trading around 0.5935, -0.05%. Risk has traded a little higher this morning, E-minis +0.10%, NQU5 +0.10%. NZD/USD bounced nicely off its 0.5850 support last week but depending on your view I would suspect sellers could return on any bounce back toward 0.6000/0.6050. For the moment firmly back in the 0.5850-0.6100 range looking for a catalyst to break and give clearer direction. The US CPI tonight might hopefully clear the picture a little.

- (Bloomberg) -- Australia’s dollar is expected to lag behind its New Zealand counterpart as their economies and central bank policies diverge, according to a Barclays note. Dovish risks are higher for the RBA as Australia’s economy slows, a currency strategist at Barclays writes in a note. On the other hand New Zealand’s growth is gaining momentum and inflation has rebounded. Aussie is also vulnerable to slower global growth and weakness in the Chinese economy.

- (Bloomberg) - Shipments from China, the US’s second-largest source of imports, started drying up noticeably in the lead-up to the Aug. 11 deadline to avoid re-imposing massive reciprocal tariffs. The drop-off may add to investors’ nervousness over whether equities can extend this year’s surge in the face of President Trump’s trade war.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5825(NZD300m Aug 14). - BBG

- CFTC Data shows Asset Managers have cut their longs completely and started to rebuild a short in the NZD -1811(Last +3903), the Leveraged community added to their shorts slightly -6778(Last -6250).

- AUD/NZD range for the session has been 1.0964 - 1.0983, currently trading 1.0980. The Cross continues to trade sideways after stalling towards the 1.1000 area once more. The range looks to be 1.0850-1.1000 for now.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Japan markets Outperform, Aided By Earnings

In the equity space, the major indices are mostly in the green at this stage. Japan benchmarks are the standout, while gains are more modest elsewhere. US Equity futures are a touch higher, after modest cash losses in Monday US trade. The focus is on the US CPI print later. A decent upside surprise is likely needed to derail a Fed cut in September.

- For Japan markets, the Topix is up a further +1.7%, while the NKY 225 is around +2.7%, trading at fresh record highs. Cited catalysts have been tariff related relief (that Japan avoided a worse case scenario), while better earnings in the tech space are another positive. The Topix information and communication sub index is up around 2.7% at this stage. Markets were also out yesterday, so some catch up may be in play.

- In China and Hong Kong markets are higher, although more so for China. The CSI 300 is up around 0.6%, while the HSI is just in positive territory. There has been some drag from the HSI tech sub index.

- The Taiex is up a touch, while the South Korean Kospi is close to flat. The Kospi was up in early trade, but the South Korean Presidential Office denied earlier onshore media reports around a potentially favorably stock capital gains tax ruling.

- In South East Asia, Indonesian stocks are up strongly, last +1.3%. Thailand and Singapore are down modestly.

- In Australia, the ASX 200 is close to flat as markets await the RBA decision in a few minutes. The central bank is widely expected to cut rates by 25 bps.

ASIA STOCKS: Malaysian Consecutive Outflow Days Stretch Back To July 25

Equity inflow momentum was mixed yesterday, with tech sensitive markets offering contrasting viewpoints. South Korea saw positive momentum, but Taiwan saw outflows. For Taiwan this followed very strong inflow momentum last Thursday, but since then momentum has stalled somewhat, albeit remaining positive for the 5-day rolling sum period. The Taiex looks to be establishing itself above the 24000 level. Recent data outcomes have been positive in terms of export growth for July up 42%y/y. The local authorities did note yesterday that if the current 20% tariff rate is maintained that growth could be cut by 0.1-0.36%.

- In South Korea, yesterday's inflows ended a run of two consecutive days of outflows. The past 5-days of inflows are running at a more modest +$500mn. Onshore media reported on stocks capital gain tax: "The official at Lee’s office told DongA that the current 5b won threshold is likely to be maintained as ruling party has stated its position" (see this link, via BBG for more details).

- Indian inflows returned at the end of last week but not enough to shift the 5-day rolling sum into positive territory.

- Indonesian inflows remained positive. In contrast, Malaysia saw further outflows, which now stretch back to July 25th in terms of consecutive outflow days seen. Still, the local Malaysian bourse has tracked higher since the start of August.

- Thailand markets were closed yesterday and return tomorrow.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 196 | 510 | -4859 |

| Taiwan (USDmn) | -153 | 1408 | 4419 |

| India (USDmn)* | 323 | -855 | -12028 |

| Indonesia (USDmn) | 52 | 122 | -3693 |

| Thailand (USDmn)* | 3 | 122 | -1696 |

| Malaysia (USDmn) | -24 | -243 | -3220 |

| Philippines (USDmn) | 7 | 12 | -617 |

| Total (USDmn) | 405 | 1075 | -21695 |

| * Data Up To Aug 8 |

Source: Bloomberg Finance L.P./MNI

OIL: Crude Range Trading Ahead Of Key Events Later Tuesday

Oil prices are slightly higher today ahead of US July CPI data, industry-reported US inventories, and EIA and OPEC monthly reports out later. Moves so far this week signal some stabilisation as the market watches the outcomes of the week’s events, which also include Friday’s Trump-Putin meeting on Ukraine.

- WTI is up 0.3% to $64.17/bbl after rising to $64.22 and then falling to $63.90 – a narrow range. Brent is also 0.3% higher at $66.83/bbl and has traded between $66.92 and $66.60.

- Trump said that Friday is more of a “feel-out meeting” and that he will report back to Ukrainian/European leaders afterwards. So it remains some time before the easing of sanctions on Russia can be considered.

- The 90-day extension of the current US-China trade stance to November 9 has calmed markets concerned that an escalation in trade tensions would weigh on growth and especially energy demand.

- US July CPI data are forecast to show both core and headline ticking up 0.1pp to 3.0% and 2.8% respectively (see Hidden PDF) and will be monitored for signs of any tariff impact. A higher-than-expected print could pressure oil as demand concerns would increase. The market has around an 85% chance of a rate cut for the Fed’s September meeting.

- July US NFIB small business optimism, real earnings and budget data are also released, as well as UK labour data and euro area/German August ZEW sentiment. The Fed’s Barkin and Schmid speak on the economy.

GOLD: Market Now Watching US CPI After Trump Clarified Gold’s Tariff Status

After falling 1.6% on Monday, gold prices are 0.3% higher at $3350.7/oz during Tuesday’s APAC session following US President Trump’s post that “Gold will not be Tariffed!”, although this is yet to be formally announced. The market had been concerned following a customs ruling that certain gold imports would face duties, which would have impacted the smooth functioning of the market. Attention now turns to July US CPI data out later today and will be monitored for signs of higher tariffs being passed on.

- Gold reached a high of $3357.48 early in the session, below initial resistance at $3409.2, 8 August high.

- Silver is also higher up 0.7% to $37.88, close to the intraday high but continuing to trade below initial resistance at $39.655.

- Equities are generally stronger with the S&P e-mini up 0.1%, Nikkei +2.5% but the Hang Seng is flat. Oil prices are up with WTI +0.3% to $64.14/bbl. Copper is 0.6% higher.

- US July CPI data are forecast to show both core and headline ticking up 0.1pp to 3.0% and 2.8% respectively (see Hidden PDF). A higher-than-expected print would pressure gold prices. The market has around an 85% chance of a rate cut for the Fed’s September meeting, which would support bullion.

- July US NFIB small business optimism, real earnings and budget data are also released, as well as UK labour data and euro area/German August ZEW sentiment. The Fed’s Barkin and Schmid speak on the economy.

THAILAND: MNI BoT Preview-Aug 2025: May Wait For New Governor

- Hidden PDF

- Given that inflation is below the Bank of Thailand’s (BoT) 1-3% target band and growth is lacklustre and lending continues to contract, 14/23 analysts surveyed by Bloomberg are forecasting a 25bp rate cut to 1.5% on August 13.

- However, there are also numerous reasons for it to be on hold, thus it is a close call. A new governor takes over from October 1, Vitai, and he is considered to be dovish. With policy seen as accommodative and already low it may want to retain policy space especially given elevated domestic and global uncertainties.

- If rates are left at 1.75%, it will be a dovish hold and there is likely to be at least one 25bp cut in one of the two BoT meetings left in 2025.

CHINA: County Wrap: US Tariff Pause for 90 Days

- President Donald Trump extended a pause of sky-high tariffs on Chinese goods for another 90 days into early November, stabilizing trade ties between the world’s two largest economies. Trump signed an order extending the truce through Nov. 10, deferring a tariff hike set for Tuesday. The de-escalation first took effect when the US and China agreed to reduce tit-for-tat tariff hikes and ease export restrictions on rare earth magnets and certain technologies. (source BBG)

- US President Donald Trump signed an executive order extending a tariff truce with China by another 90 days, a White House official said on Monday, hours before trade truce between Washington and Beijing was due to expire on Tuesday. (source China Daily)

- Three major Chinese financial institutions have announced coordinated measures to simplify account-opening procedures for overseas central banks and similar institutions, in a move aimed at optimizing China’s bond market. The key institutions will no longer require a compliance commitment statement for account openings under both the Bond Connect and settlement agency models, according to official statements

- The changes are expected to improve efficiency and convenience for foreign central banks and monetary authorities, while further advancing the internationalization of China’s bond market, Securities Times reports (source BBG)

- China and Hong Kong markets are higher, although more so for China. The CSI 300 is up around 0.6%, while the HSI is just in positive territory. There has been some drag from the HSI tech sub index.

- Yuan Reference Rate at 7.1418 Per USD; Estimate 7.1905

- The modest bout of weakness in the bond market continued and has seen the CGB10yr move higher to 1.73%.

SOUTH KOREA: Country Wrap: KDI Keeps GDP Forecast at 0.8%

- South Korea's state-run economic think tank on Tuesday kept at 0.8 percent its growth outlook for the local economy this year, citing persistent weakness in construction investment. The latest projection by the Korea Development Institute (KDI) is unchanged from its May forecast but still marks a sharp downgrade from the 1.6 percent estimate issued in February. For 2026, the institute said the economy is projected to grow 1.6 percent, also unchanged from three months earlier. "While consumption and export forecasts were revised upward for this year, the downward adjustment in construction investment led us to maintain the overall growth forecast," the KDI said. (source Yonhap)

- Bond issuance in South Korea fell from a month earlier in July on a drop in government and special bond issues, data showed. The value of bonds sold last month stood at 84 trillion won (US$60.4 billion), down 4.6 trillion won from the previous month, according to the data from the Korea Financial Investment Association (KOFIA). By type, government bond issuance fell by the largest margin of 8.7 trillion won in the one-month period to 26.2 trillion won. (source Yonhap)

- The KOSPI was the regional laggard today as one of the few fallers of the major bourses down -0.20%

- The Won is the best regional performer today up +0.17% to 1,389.15 bouyed by the China news.

- Bonds are weak with yields higher across the curve by 1-2bps. KTB 10yr is at 2.80% (from yesterday's close of 2.78%).

INDIA: Country Wrap: CPI Expected to Be Weak

- Later today India releases its CPI for July and market expectations are for a drop to it's lowest print since 2019. Against a June result of +2.10%, the forecast for July from economists is +1.40% due to a high base effect. In 2024 India experienced a dramatic rise in food prices, particularly vegetables and July's prices will be compared against that high base. RBI Governor Sanjay Malhotra was quoted recently saying, "CPI inflation for the current year 2025-26 is now projected at 3.1%. This is down from 3.7% that we had earlier projected in June." According to the RBI Governor, headline CPI inflation declined for the eighth consecutive month, reaching a 77-month low of 2.1% in June. At this stage, that seems overly optimistic and hence could provide further downward pressure on rates. The market seems not prepared for this given the swaps market pricing in little change in rates over a 12 - month time horizon. As monsoon season kicks off in India, a period that delivers most of the annual rainfall, market observers will be monitoring the impact particularly with regard to vegetable production. (source MNI)

- The Indian government indicated on Monday that it remained hopeful about negotiating a bilateral trade agreement with the United States despite recent turbulence. US President Donald Trump had imposed a 25% levy against Indian imports at the beginning of August — vowing to add an additional 25% later this month for its continued purchase of Russian oil. Officials have suggested that the Narendra Modi-led government is now working on support measures to insulate exporters in certain sectors from the full impact of the tariffs. (source Financial Express)

- The NIFTY 50 is flat this morning as it nears the 100-day EMA of 24,590.

- The Rupee is flat at 87.62 in a lackluster start to the trading day.

- Bonds are modestly better ahead of the CPI later with the IGB 10yr at 6.43% (-1bp)

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 12/08/2025 | 0600/0700 | *** | Labour Market Survey | |

| 12/08/2025 | 0600/0700 | *** | Labour Market Survey | |

| 12/08/2025 | 0600/0700 | *** | Labour Market Survey | |

| 12/08/2025 | 0600/0700 | *** | Labour Market Survey | |

| 12/08/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 12/08/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 12/08/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 12/08/2025 | 1100/1200 | BOE APF Quarterly Report | ||

| 12/08/2025 | - | *** | Money Supply | |

| 12/08/2025 | - | *** | New Loans | |

| 12/08/2025 | - | *** | Social Financing | |

| 12/08/2025 | 1230/0830 | * | Building Permits | |

| 12/08/2025 | 1230/0830 | *** | CPI | |

| 12/08/2025 | 1230/0830 | *** | CPI | |

| 12/08/2025 | 1230/0830 | *** | CPI | |

| 12/08/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 12/08/2025 | 1400/1000 | Richmond Fed's Tom Barkin | ||

| 12/08/2025 | 1430/1030 | Kansas City Fed's Jeff Schmid | ||

| 12/08/2025 | 1600/1200 | *** | USDA Crop Estimates - WASDE | |

| 12/08/2025 | 1800/1400 | ** | Treasury Budget | |

| 13/08/2025 | 0130/1130 | *** | Quarterly wage price index | |

| 13/08/2025 | 0600/0800 | *** | HICP (f) | |

| 13/08/2025 | 0700/0900 | *** | HICP (f) | |

| 13/08/2025 | 1100/0700 | ** | MBA Weekly Applications Index |