MNI EUROPEAN MARKETS ANALYSIS: Solid 10yr Auction Aids JGBs

- BoJ Governor Ueda stated rate hikes are still on the table, even amidst all the uncertainty. The 10yr JGB auction was solid, with futures stronger, +10 compared to settlement levels.

- USD/JPY is slightly higher, as most majors have weakened versus the USD. AUD has underperformed. Partial indicators point to soft domestic demand in tomorrow's Q1 GDP release for Australia.

- Later the Fed’s Goolsbee, Cook and Logan appear. May euro area HICP, US April JOLTS job openings and final April US orders print.

MARKETS

US TSYS: Asia Wrap - Yields A Little Lower

The TYU5 range has been 110-16 to 110-20+ during the Asia-Pacific session. It last changed hands at 110-20, up 0-05 from the previous close.

- The US 2-year yield has drifted lower, dealing around 3.93%, down 0.01 from its close.

- The US 10-year yield has drifted lower, trading around 4.4316%, down 0.1 from its close.

- (Bloomberg) - “Traders are buying into the stagflation narrative, with Monday’s economic reports setting the tone for a week that culminates in the May jobs report. Against that backdrop, the path of least resistance is a steeper yield curve.”

- “The Fed can proceed with rate cuts if uncertainty around trade policy is resolved, Austan Goolsbee said, adding that recent data showed “surprisingly little impact so far.” Lorie Logan said risks to inflation and employment are balanced, implying the central bank can remain patient.”(BBG)

- AFR - “JPMorgan chief executive Jamie Dimon on Friday night predicted that a crack in the bond market is “going to happen” - and it will scare the pants off everyone.”

- The 10-year has bounced nicely off its support around 4.35/40%. Yields need to hold above this area to continue to build for a move higher.

- Data/Events : Factory Orders, Durable Goods Orders, JOLTS.

JGBS: 10Y Auction Result Sparks Rally, BoJ Ueda Speech Later Today

JGB futures are stronger, +10 compared to settlement levels, after gapping higher following a strong 10-year auction.

- The 10-year JGB auction delivered a low price above expectations, according to the Bloomberg dealer poll. Moreover, the cover ratio increased to 3.6627x from 2.5440x, and the tail shortened to 0.01, the shortest since March 2023, from 0.18.

- BoJ Governor Ueda, speaking in parliament, emphasised that trade uncertainties remain extremely high and are unlikely to ease even after tariff issues are resolved. He noted that the BoJ's baseline economic scenario could change significantly due to external conditions.

- He also said the BoJ will review its bond tapering plans at the next policy meeting on June 17, taking into account feedback from bond market participants.

- Note as well Governor Ueda will speak later today at 4:50pm local time.

- Cash US tsys are ~1bp richer in today's Asia-Pac session after yesterday's sell-off.

- Cash JGBs are 1bp cheaper to 2bps richer across benchmarks, with the belly leading. The benchmark 10-year yield is 2.3bps lower on the day at 1.490%.

- Swap rates are flat to 1bp lower.

- Tomorrow, the local calendar will see Jibun Bank Composite and Services PMIs.

AUSSIE BONDS: Little Changed, RBA Minutes Highlight Uncertainty

ACGBs (YM flat & XM -1.0) are little changed after dealing in narrow ranges in today’s Sydney session.

- Cash US tsys are ~1bp richer in today's Asia-Pac session after yesterday's sell-off. Today’s US calendar will see Factory Orders, Durable Goods Orders and JOLTS. Non-Farm Payrolls are due on Friday.

- Cash ACGBs are little changed with the AU-US 10-year yield differential at -15bps.

- The May meeting RBA minutes confirmed that staying on hold, 25bp and 50bp rate cuts were discussed. It appears that not only is there considerable uncertainty regarding the outlook but that the Board prefers to remain cautious and move “predictably”, as a result, it cut by the widely expected 25bp, which was also assumed in its updated staff projections. Given not just global uncertainties but also around the level of monetary restrictiveness and tightness in the labour market, another cut in July is not fixed and will be highly data and event-dependent.

- The bills strip is slightly mixed, with pricing -1 to +1.

- Tomorrow, the local calendar will see Q1 GDP, with the market expecting +0.4% q/q and +1.5% y/y.

- The AOFM plans to sell A$800mn of the 1.50% 21 June 2031 bond on Friday.

AUSTRALIA DATA: Net Exports Detracted From Q1 Growth

Not only was the current account deficit larger than expected but Q4 was revised significantly wider, but that meant that it narrowed in Q1. It was $14.7bn in Q1 after $16.3bn in Q4. Net exports detracted 0.1pp from growth while the 0.2pp contribution in Q4 was revised down to a 0.1pp detraction.

- The Q1 improvement in the current account was due to a smaller net income deficit as lower coal prices resulted in less dividends paid to overseas investors. The primary income deficit narrowed $2.2bn to $19.4bn.

- The goods & services surplus narrowed $0.2bn to $5.2bn due to a widening in the services deficit. Exports rose 1.9% q/q while imports picked up 2.2% q/q.

Australia current account $bn

Source: MNI - Market News/ABS

- Goods exports rose 2.9% q/q but were down 2.4% y/y. The quarterly increase was driven by non-monetary gold (volumes & prices rose) and rural goods, while non-rural posted its fifth consecutive quarterly decline. Services fell 1.7% q/q but were up 7% y/y.

- The ABS noted that the Q1 shipment of gold to the US was larger than the total of the last four years, as producers aimed to beat US tariffs. Excluding gold, total goods exports would have declined 1% q/q due to disruptions to coal production and lower prices.

- Merchandise imports were up 3.1% q/q & 2.7%y/y with consumer goods +0.3% q/q and intermediate +7.1% q/q, due to a pickup in fuel prices, but capital down 1.1% q/q, consistent with weak investment. Services fell 0.5% q/q as overseas travel became less popular.

- The terms of trade appear to have stabilised with Q1 +0.1% q/q, second straight increase, to drive an improvement in the annual rate to -4.0% from -4.6%. Export prices rose 2.8% q/q with both goods and services higher, while import prices increased 2.6% q/q driven by goods with services little changed.

Australia terms of trade indices

Source: MNI - Market News/ABS

RBA: Board Wanted To Move “Predictably” In May, July Data & Event Dependent

The May meeting minutes confirmed that staying on hold, 25bp and 50bp rate cuts were discussed. It appears that not only is there considerable uncertainty regarding the outlook but that the Board prefers to remain cautious and move “predictably”, as a result it cut by the widely expected 25bp, which was also assumed in its updated staff projections. Given not just global uncertainties but also around the level of monetary restrictiveness and tightness in the labour market, another cut in July is not fixed and will be highly data and event dependent.

- Rates were cut by 25bp as that was assumption in the forecasts brought underlying inflation close to the band mid-point, the “progress made on inflation”, the “slightly softer outlook for domestic consumption”, global developments would like slow Australian growth, it was “predictable” and would leave room to respond to events.

- The Board decided to limit the move to 25bp because Australian data was yet to show any “adverse impact on domestic demand” from global events, concerns about Australia’s supply-side including productivity, “two-sided” uncertainty over the degree of labour market tightness, impact of a demand recovery on profit margins, trade policy outcomes and effects on global supply chains are still unknown, and it would be difficult to unwind “too rapid” easing.

- The arguments to hold policy included that the stance of current policy is not judged “very restrictive”, headline inflation would rise again when electricity rebates ended, “labour and product markets remained relatively tight”, case to wait and see how global trade policy evolved and there were currently “few observable effects on the Australian economy”.

- Domestic developments on their own warranted monetary policy easing, while global developments “strengthened the case”. The combination of the two is likely to be important for the rate outlook.

BONDS: NZGBS: Twist-Steepener After Long Weekend

After the long weekend, NZGBs closed showing a twist-steepener, with benchmark yields 1bp lower to 4bps higher.

- Cash US tsys are ~1bp richer in today's Asia-Pac session after yesterday's sell-off. Today’s US calendar will see Factory Orders, Durable Goods Orders and JOLTS. Non-Farm Payrolls are due on Friday.

- (Bloomberg) - "Traders are buying into the stagflation narrative, with Monday's economic reports setting the tone for a week that culminates in the May jobs report. Against that backdrop, the path of least resistance is a steeper yield curve."

- "The Fed can proceed with rate cuts if uncertainty around trade policy is resolved, Austan Goolsbee said, adding that recent data showed "surprisingly little impact so far." Lorie Logan said risks to inflation and employment are balanced, implying the central bank can remain patient."(BBG)

- Swap rates closed 2bps lower to 3bps higher, with a steepener 2s10s curve.

- RBNZ dated OIS pricing closed little changed across meetings. 7bps of easing is priced for July, with a cumulative 30bps by November 2025.

- Tomorrow, the local calendar will be empty.

- On Thursday, the NZ Treasury plans to sell NZ$200mn of the 3.00% Apr-29 bond, NZ$200mn of the 4.50% May-35 bond and NZ$50mn of the 5.00% May-54 bond.

NEW ZEALAND: Terms Of Trade Rises Again, Strong Export Volume Growth

While the Q1 merchandise terms of trade rose less than expected at 1.9% q/q, it was the fifth straight monthly increase after it was up 3.2% in Q4. Statistics NZ notes that the softer kiwi “contributed” to higher export and import prices. Export volumes rose solidly for the second straight quarter boosted by dairy products and should be a positive in Q1 GDP when it is released on June 19.

NZ terms of trade y/y%

- Export prices rose 7.1% q/q to be up 17.2% y/y boosted by a 10.5% q/q increase in dairy prices and 7.2% q/q in meat, while import prices were up 5.1% q/q & 6.2% y/y. Consumer goods import prices rose 3.5% q/q to be up 5.5% y/y after 1.7% y/y in Q4. This is the highest annual rate since Q2 2023 and likely added to CPI inflation.

- The services terms of trade rose 4.2% q/q but was still down 7.3% y/y after -7.4% y/y in Q4. Services export prices rose 3.2% q/q & 3.8% y/y, while imports fell 0.8% q/q but were still up 12.1% y/y.

- Merchandise export volumes rose 4.7% q/q in Q1 driven by a 7% q/q jump in dairy products.

- Goods import volumes fell 2.5% q/q to be up 2.0% y/y down from Q4’s 5.8% y/y reflecting continued weak domestic demand. Consumer goods imports rose a moderate 0.2% q/q but annual growth eased to 2.5% from 5.9%.

NZ import prices vs CPI y/y%

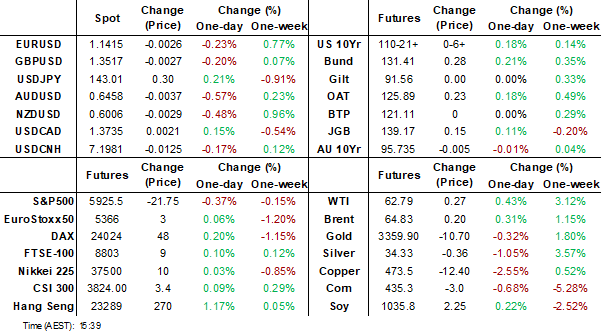

FOREX: Asia FX Wrap - USD Bounces in Asia

The BBDXY has had a range of 1207.93 - 1211.32 in the Asia-Pac session, it is currently trading around 1210. Robin Brooks on X: “Today's Dollar fall is worrying. It mirrors Dollar weakness in early April, when the Dollar (black) fell even as interest differentials of the US vis-à-vis the G10 (blue) were stable(see graph below). That kind of decoupling of the Dollar from rate differentials is unusual and a worrying sign.” https://x.com/robin_j_brooks/status/1929653605440606282

- EUR/USD - Asian range 1.1416 - 1.1455, Asia is currently trading 1.1420. EUR has drifted lower during the Asian session as US stock futures trade weaker. Dips should continue to find support, the demand back towards 1.1200 proved to be solid last week.

- GBP/USD - Asian range 1.3515 - 1.3559, Asia is currently dealing around 1.3520. The GBP is attempting another run higher but is struggling to gain any momentum on a 1.3500 handle. Look for an opportunity to buy again back towards the 13300/3400 area if seen.

- USD/CNH - Asian range 7.2016 - 7.241, the USD/CNY fix printed 7.1869. Asia is currently dealing around 7.1985. Sellers should be around on bounces while price holds below the 7.2500 area.

- Cross asset : SPX -0.42%, Gold $3361, US 10-Year 4.43%, BBDXY 1210, Crude oil $62.81

Data/Events : Spain Unemployment, Italy Unemployment, EC CPI

Fig 1: DXY vs 2Y2Y FWD Rate

Source - Robin Brooks via X

JPY: Asia USD/JPY Wrap - Ueda Puts the Brakes On The Move Lower, For Now ?

The Asia-Pac USD/JPY range has been 142.38 - 143.27, Asia is currently trading around 143.10. USD/JPY has had an unexpected bounce in our session as the BOJ Governor pushes back on being forced to raise rates.

- (Dow Jones) via BBG - “The yen weakens against most other G-10 and Asian currencies in the morning session on possible dovish signs in BOJ Gov. Ueda's comments earlier. Ueda said that uncertainty, including on trade policy outlook, remains high and could remain so even after the tariffs are determined. Ueda said the central bank isn't predetermining rate decisions and won't push for rate increases just to make room for future rate cuts.”

- Bank of Japan Governor Ueda, speaking in parliament, said the BoJ will review its bond tapering plans at the next policy meeting on June 17, taking into account feedback from bond market participants. Additionally, he pointed out that sharp movements in long-term yields could influence short-term rates.

- BOJ GOV UEDA: MINUTES OF BOJ'S MEETING WITH BOND MARKET PLAYERS SHOWED MANY THOUGHT IT WAS IMPORTANT FOR BOJ TO CONTINUE TAPERING BOND BUYING WHILE STRIKING BALANCE BETWEEN FLEXIBILITY AND PREDICTABILITY" RTRS

- The market seems very confident of a move lower in USD/JPY but with positioning quite large now we have seen the risk of pullbacks increase. Resistance around the 146.00 area held perfectly and the JPY bulls would be quite relieved as well as vindicated by the price action.

- The USD is looking like it is about to start another leg lower. A break below 142.00 in USD/JPY and all eyes will once again turn to the pivotal 140.00 area. Sellers should emerge on a bounce back towards the 144.00 area now.

Options : Close significant option expiries for NY cut, based on DTCC data: 143.00($450m). Upcoming Close Strikes : 140.00($1.89b June 5), 140.00($1.13b June 6).

Fig 1 : USD/JPY Spot Hourly Chart

Source: MNI - Market News/Bloomberg

NZD: Asia Wrap - NZD/USD Struggling To Hold Above 0.6000

The NZD/USD had a range of 0.6011 - 0.6055 in the Asia-Pac session, going into the London open trading around 0.6015. The NZD has failed to hold onto its gains above 0.6050 and drifted lower all day. The move lower has been a reaction to weaker Chinese data and US Equity futures trading poorly in our session. The Bulls will be hoping demand can keep it on a 0.6000 handle to build for another attempt.

- China's May CAIXIN PMI contracted in May, surprising forecasters. May's result of +48.3 was materially down from +50.4 in March and a surprise to market surveys predicting a rise to +50.7.

- NEW ZEALAND: Terms Of Trade Rises Again, Strong Export Volume Growth. While the Q1 merchandise terms of trade rose less than expected at 1.9% q/q, it was the fifth straight monthly increase after it was up 3.2% in Q4. Statistics NZ notes that the softer kiwi “contributed” to higher export and import prices. Export volumes rose solidly for the second straight quarter boosted by dairy products and should be a positive in Q1 GDP when it is released on June 19.

- The NZD is attempting to break out its recent range, the hawkish slant from the RBNZ last week only saw a slight paring back of short positions. Should the NZD sustain a clear break back above 0.6050 you could see some of these reduced even further.

- The support back towards 0.5850 has held very well, and while this continues to hold expect buyers to be around on dips. A clear break above 0.6050 could provide the spark for the next leg higher.

- CFTC Data showed Asset managers maintaining their shorts, while the leveraged community pared back only a little of the decent short they had initiated the week before.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6100(NZD375m). Upcoming Close Strikes : 0.5900(NZD401m June 4)

AUD/NZD range for the session has been 1.0727 - 1.0770, currently trading 1.0755. A top looks in place now just above 1.0900, the market will have been looking for a more dovish tone from the RBNZ last week and AUD/NZD could now see supply on bounces. The sell zone is back towards 1.0825/50 with the first target being around 1.0650.

Fig 1: NZD/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg

AUD: Asia Wrap - Fails At 0.6500 Once More

The AUD/USD has had a range of 0.6464 - 0.6500 in the Asia- Pac session, it is currently trading around 0.6465. The AUD has again failed towards the 0.6500 area, the move lower has been a reaction to weaker Chinese data and US Equity futures trading poorly in our session.

- China's May CAIXIN PMI contracted in May, surprising forecasters. May's result of +48.3 was materially down from +50.4 in March and a surprise to market surveys predicting a rise to +50.7.

- RBA: Board Wanted To Move “Predictably” In May, July Data & Event Dependent. The May meeting minutes confirmed that staying on hold, 25bp and 50bp rate cuts were discussed. It appears that not only is there considerable uncertainty regarding the outlook but that the Board prefers to remain cautious and move “predictably”, as a result it cut by the widely expected 25bp, which was also assumed in its updated staff projections

- The AUD has struggled to hold onto its overnight gains and has underperformed in the crosses as US Equity futures stay under pressure in the Asian session.

- Expect buyers to continue to be around on dips while the support in the AUD holds, a close back below 0.6300/50 would start to challenge the newly formed uptrend, a sustained break above 0.6550 and the move higher could begin to accelerate.

- Today's price action suggests the range of 0.9350 - 0.9550 is set to persist for a little longer.

AUD/JPY - Today's range 92.49 - 92.86, it is trading currently around 92.55. Range looks 92.00 - 94.00 for now, a sustained break sub 91.50/92.00 will bring focus back to towards the lows again.

Fig 1: AUD/USD spot Hourly Chart

Source: MNI - Market News/Bloomberg

ASIA STOCKS: China Up on Stimulus Hopes, Elsewhere Mixed

As China returns from a break yesterday, an unexpected weak CAIXIN manufacturing PMI drove markets higher as investors speculate about the potential for further policy intervention. With Korea closed, all eyes were on China's major bourses with some of the beaten down EV related stocks having a better day in Hong Kong (BYD +1.7%, Li Auto +6.4%)

- With the Hang Seng leading the way with a rise of +1.13%, onshore bourses performed also with the CSI300 +0.48%, the Shanghai Composite +0.48% and Shenzhen up +0.57%.

- The FTSE Malay KLCI returned after being closed yesterday to be down by -0.32% and mark six successive days of falls.

- The Jakarta Composite did very little and hovered around where it opened after its biggest fall in four weeks yesterday.

- The FTSE Straits Times in Singapore is down -0.03% whilst the PSEi in the Philippines is up +0.45%.

- The NIFTY 50 is in line for three straight days of fall, losing ground by -0.20% today.

ASIA STOCKS: Flows Reverse for Taiwan and India

After an exceptional period of inflows into the major markets, it appears that this trend has stalled for now as constant daily flows are interrupted with outflows, with Taiwan and India the latest to experience a significant outflow.

- South Korea: Recorded inflows of +$172m yesterday, bringing the 5-day total to +$265m. 2025 to date flows are -$11,205. The 5-day average is +$53m, the 20-day average is +$53m and the 100-day average of -$112m.

- Taiwan: Had outflows of -$1,885m as yesterday, with total outflows of -$2,332m over the past 5 days. YTD flows are negative at -$12,778. The 5-day average is -$466m, the 20-day average of +$222m and the 100-day average of -$134m.

- India: Had outflows of -$585m as of the 30th, with total inflows of +$50m over the past 5 days. YTD flows are negative -$10,528m. The 5-day average is +$10m, the 20-day average of +$87m and the 100-day average of -$113m.

- Indonesia: Had outflows of -$172m as of yesterday, with total outflows of -$45m over the prior five days. YTD flows are negative -$2,898m. The 5-day average is -$9m, the 20-day average +$9m and the 100-day average -$31m.

- Thailand: Recorded outflows of -$47m as of 29th, outflows totaling -$84m over the past 5 days. YTD flows are negative at -$1,755m. The 5-day average is -$17m, the 20-day average of -$2m and the 100-day average of -$18m.

- Malaysia: Recorded outflows of -$107m as of the 30th, totaling -$240m over the past 5 days. YTD flows are negative at -$3,424m. The 5-day average is -$56m, the 20-day average of +$8m and the 100-day average of -$24m.

- Philippines: Saw inflows of +$8m yesterday, with net outflows of -$259m over the past 5 days. YTD flows are negative at -$515m. The 5-day average is -$52m, the 20-day average of -$13m the 100-day average of -$5m.

OIL: Crude Holds Onto Gains As Supply Worries Fade

Oil prices have held onto Monday’s 3.7% gains and continued to trade higher during today’s APAC session. WTI is up 0.4% to around $62.80/bbl but off the intraday high of $63.25, but continues to trade above the 50-day EMA at $62.47 opening up key resistance at $65.82. Brent is 0.3% higher at $64.82 but down from today’s peak of $65.34, just above initial resistance at $65.31. The USD index is up 0.1%.

- The fading prospect of an easing in sanctions on Russia or Iran has supported oil prices. The potential increase in supply was a concern at a time of output normalisation from OPEC.

- While OPEC announced another 411kbd production increase from July, many of the group’s members have little spare capacity with Saudi the main one who can boost output, which it may choose not to do. The impact of normalisation may not be as much as feared if many in OPEC end up underproducing quotas.

- Also on the supply side, fires in Alberta have threatened oil production resulting in around 350kbd or 7% of Canadian output being shut down, according to Bloomberg. The closures impact heavy crude which is currently in short supply due to seasonal maintenance.

- With the significant uncertainty created by US trade announcements in recent months, data is being scrutinised for observable effects on activity. For oil, US inventory data is being monitored for signs of demand slippage and how the driving season is progressing. The industry-based data is out today with the official EIA on Wednesday.

- Later the Fed’s Goolsbee, Cook and Logan appear. May euro area HICP, US April JOLTS job openings and final April US orders print.

GOLD: Bullion Gives Up Some Gains As US Dollar Strengthens

After rising 2.8% to $3381 on Monday, gold prices are down 0.6% to $3361.9, holding just below initial resistance at $3365.9, 23 May high, during today’s APAC trading. They reached a high of $3392.2 early in the session but have trended lower since reaching a trough of $3359.91 as the US dollar strengthened (USD BBDXY +0.2%), but trade and geopolitical risks remain present with talks on a number of fronts ongoing.

- Australia’s ABS reported that Q1 shipments of gold to the US were larger than the total of the last four years, as producers aimed to beat US tariffs.

- Regional equities are mixed with the Hang Seng up 1.1%, Straits Times flat and Nifty 50 down 0.3% and S&P e-mini -0.4%. Other commodities are mixed with silver down 1.8% to $34.14, copper -2.5% but WTI up 0.5%. US yields are little changed.

- Later the Fed’s Goolsbee, Cook and Logan appear. May euro area HICP, US April JOLTS job openings and final April US orders print.

CHINA: CAIXIN PMI Unexpectedly Contracts

- China's May CAIXIN PMI contracted in May, surprising forecasters.

- May's result of +48.3 was materially down from +50.4 in March and a surprise to market survey's predicting a rise to +50.7

- May's result was the worst since Q3 2022.

- Output fell sharply to +47.5 vis +51.6 in April for the lowest reading since late 2022 and new orders fell from the month prior.

- The outcome reverses seven consecutive months of expansion and speaks to the uncertainty created from the US-China trade war.

SOUTH KOREA: Country Wrap: Korean's to Vote

- Korean markets were closed today due to the presidential election. If you haven't already seen it, take a look at the excellent piece from our political risk team.

https://my.mnimarkets.com/article/17efcc2c-fd8d-4f27-9492-6ccccff910a2-1748602114087

- Yonhap reporting that interest in this election is strong. Five hours after the polls opened at 6 a.m., 18.3 percent, or some 8.1 million, of the 44.39 million eligible voters had cast their ballots at 14,295 polling stations, according to the National Election Commission (NEC). Voter interest was keen in the snap election, as 34.74 percent of the registered voters had already cast their ballots in the early voting held on Thursday and Friday, the second-highest figure since early voting was introduced in 2014. (source Yonhap)

https://en.yna.co.kr/view/AEN20250602004952315?section=national/politics

- Maeil Business Paper reporting that the Electoral Commission is saying that as at 1PM today, voter turn out for this election when compared to 1pm for the last is nearly 1% higher. (source MAEIL)

https://www.mk.co.kr/en/politics/11333304

- Korea's market have largely been in a positive mood ahead of the election. The markets have endured multiple shocks from the martial law through to impeachment for President Yoon to the dominant semi-conductor stocks melting down as tariffs were announced by the US. The KOSPI cratered -13% over the April announcement of tariffs yet has recovered since. From the 9 April low, the KOSPI is up +17.71% and at 2,698 sits above the 5-year average. During that same period 1Q GDP printed at -0.2% and the BOK cut rates. The Won over that time has had an equally volatile period. Around the time of the tariff announcement the Won was trading at 1,377 only to widen to 1,420 (representing a 3.10% decline) and then recover back to 1,377 today. Bonds have equally exhibited an increase in volatility over that time. KTB 3yr ended March at 2.57%, rallying to 2.25% and today is back at 2.35%. KTB 10yr ended March at 2.78%, rallying to 2.56% and is back now at 2.79%. (source MNI Market News)

MALAYSIA: Country Wrap: PMIs Continue to Disappoint

- Malaysia's May PMI Manufacturing saw a modest improvement from March, whilst continuing to point to contraction. May PMI printed at +48.8, from +48.6 prior and continues the theme of modest contraction. The last PMI above 50 was in August 2022. Output rose to +48.5 from +47.4 and new orders were higher than last month.

- Despite this contraction, the Malaysian economy is expected to grow +4.5%-+5.5% in 2025 (source MNI Market News)

- Malaysia made a strong economic showing at Expo 2025 Osaka as the nation secured RM4.68 billion in potential investments from Japan, the Malaysian Investment Development Authority (MIDA) said. This figure represents a major milestone, accounting for 56.9% of the RM7.39 billion in total investments attracted under Malaysia’s Expo participation. (source Business Today)

- The FTSE Malay KLCI returned after being closed yesterday to be down by -0.32% and mark six successive days of falls.

- The ringgit is off to a strong start for the week, gaining +.15% at 4.25

- MGS 10YR at 3.59%

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 03/06/2025 | 0630/0830 | *** | CPI | |

| 03/06/2025 | 0700/0300 | * | Turkey CPI | |

| 03/06/2025 | 0900/1100 | *** | HICP (p) | |

| 03/06/2025 | 0900/1100 | ** | Unemployment | |

| 03/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 03/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 03/06/2025 | 0915/1015 | BOE Bailey, Breeden, Dhingra, Mann At TSC | ||

| 03/06/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 03/06/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 03/06/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/06/2025 | 1400/1000 | *** | JOLTS jobs opening level | |

| 03/06/2025 | 1400/1000 | *** | JOLTS quits Rate | |

| 03/06/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/06/2025 | 1645/1245 | Chicago Fed's Austan Goolsbee | ||

| 03/06/2025 | 1700/1300 | Fed Governor Lisa Cook | ||

| 03/06/2025 | 1930/1530 | Dallas Fed's Lorie Logan | ||

| 04/06/2025 | 2300/0900 | * | S&P Global Final Australia Services PMI | |

| 04/06/2025 | 2300/0900 | ** | S&P Global Final Australia Composite PMI | |

| 04/06/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 04/06/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 04/06/2025 | 0130/1130 | *** | Quarterly GDP | |

| 04/06/2025 | 0700/0900 | ** | Industrial Production | |

| 04/06/2025 | 0715/0915 | ** | S&P Global Services PMI (f) | |

| 04/06/2025 | 0715/0915 | ** | S&P Global Composite PMI (final) | |

| 04/06/2025 | 0745/0945 | ** | S&P Global Services PMI (f) | |

| 04/06/2025 | 0745/0945 | ** | S&P Global Composite PMI (final) | |

| 04/06/2025 | 0750/0950 | ** | S&P Global Services PMI (f) | |

| 04/06/2025 | 0750/0950 | ** | S&P Global Composite PMI (final) | |

| 04/06/2025 | 0755/0955 | ** | S&P Global Services PMI (f) | |

| 04/06/2025 | 0755/0955 | ** | S&P Global Composite PMI (final) | |

| 04/06/2025 | 0800/1000 | ** | S&P Global Services PMI (f) | |

| 04/06/2025 | 0800/1000 | ** | S&P Global Composite PMI (final) | |

| 04/06/2025 | 0830/0930 | ** | S&P Global Services PMI (Final) | |

| 04/06/2025 | 0830/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 04/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 04/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 04/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 04/06/2025 | 1215/0815 | *** | ADP Employment Report | |

| 04/06/2025 | 1230/0830 | Atlanta Fed's Raphael Bostic | ||

| 04/06/2025 | 1345/0945 | *** | Bank of Canada Policy Decision | |

| 04/06/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 04/06/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI |