MNI EUROPEAN MARKETS ANALYSIS: Risk Appetite Improves Further

- Risk appetite has stayed on the front foot from an equity standpoint, with Trump expressing optimism around US-China trade talks (albeit with clear focus points).

- China Q3 GDP slowed, while Sep activity figures were mixed. Housing remains a drag, but broader macro spill over has been limited today. NZ Q3 CPI was close to market and RBNZ expectations as well.

- As expected,Japan's LDP and Ishin parties are forming a coalition, which should pave the way for Takaichi to become the new PM. Yen has rebounded from lows, aided by hawkish remarks from BoJ board member Takata.

- Later the ECB’s Schnabel speaks while the Fed is in its media blackout ahead of the 29 October decision. The ongoing US government shutdown continues to impact public sector data releases. August euro area current account and construction and Canada’s Q3 BoC business survey print.

MARKETS

US TSYS: UST 10-Yr Re-Establishes Recent Range

A day of consolidation for bonds after last week's Fed Comment induced rally. TYZ5 is down -02 at 113-12+ as what seems cooling trade tensions give equity markets a boost. TYZ5 maintains its position above all major moving averages, the nearest being the 20-day EMA at 113-01.

- The US 2-Yr ended last week down -5bps at 3.45% having now traded below 2024 lows and has backed up to 3.47% in the Asia trading day.

- The US 5-Yr ended last week down -3bps at 3.59% with the break below 3.60% possibly indicating the resetting of recent ranges, but has edged higher back to 3.60% today.

- The US 10-Yr finished last week at 4.01% unable to hold below 4.00%. The 4.00% - 4.20% range has held of late and whilst the 10-Yr closed at 3.97% Thursday, ultimately as risk sentiment improved moderately, it was unable to hold below and reset recent ranges. It has inched higher again today to be at 4.02%

- The US 30-yr finished last week at 4.60%, a decline of -2bps, having briefly dipped below 4.60% Thursday. 4.60% does not appear to be a particularly strong technical for the 30-Yr at this stage and it has drifted higher to 4.61%. The driver for long end yields in the first part of the week is most likely to come from any improvements in sentiment as the concerns on US banks dissipates.

JGBS: Cheaper As Market Digests New LDP/Ishin Coalition, Hawkish BOJ Takata

JGB futures are sharply weaker, -50 compared to settlement levels, and at session lows after digesting the formed coalition between the LDP and Ishin, which should deliver the PM position to LDP leader Takaichi.

- Takaichi is generally seen as a negative for local bonds (given her pro-growth/monetary loose comments in the past), while being positive for equities.

- Ishin stated: "*YOSHIMURA: DON'T HAVE TIMELINE ON ZERO CONSUMPTION TAX ON FOOD" - BBG, so it may take a little time for fresh policies to emerge.

- BoJ's Takata stated that now is the time to adjust policy rates further, and the inflation target is more or less achieved. Takata voted for a rate hike at the last policy meeting, but this wasn't the majority viewpoint. At this stage, only 6bps of hike risks are priced by the market for the end Oct meeting.

- Cash US tsys are ~1bp cheaper in today's Asia-Pac session after Friday's modest sell-off.

- Consistent with the above developments, cash JGBs are 2-3bps cheaper across benchmarks out to the 10-year but flat to 1bp richer beyond. The benchmark 10-year yield is 3.8bps higher at 1.669% versus the cycle high of 1.70%.

- Swap rates are 1-3bps higher.

- Tomorrow, the local calendar will see Tokyo Condominiums for Sale and Machine Tool Orders data alongside 10-year CT supply.

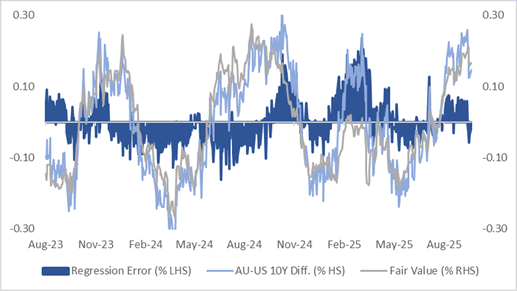

AUSSIE BONDS: Cheaper But Narrow Ranges On Data-Light Day

ACGBs (YM -5.0 & XM -5.5) are weaker after holding in tight ranges in today’s data-light session.

- Cash ACGBs are 5bps cheaper with the AU-US 10-year yield differential at +13bps. At +13bps, the differential has narrowed from recent wides but remains in the top half of the ±30bps range that has prevailed since November 2022.

- A simple regression of the 10-year yield differential against the AU-US 1-year forward 3-month swap rate (1Y3M) differential over the past two years suggests the current spread is -2bps versus fair value.

- The bills strip is -3 to -6.

- RBA-dated OIS pricing is firmer across meetings today. A 25bp rate cut in November is given a 72% probability, with a cumulative 24bps of easing priced by year-end (based on an effective cash rate of 3.60%).

- The local data calendar is fairly quiet through the course of this week, with October's preliminary PMIs out on Friday, with the RBA's Bullock also speaking that day.

- This week, the AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond on Tuesday, A$900mn of the 2.75% 21 June 2035 bond on Wednesday and A$800mn of the 2.75% 21 November 2029 bond on Friday.

Figure 1: AU-US Cash 10-Year Yield Differential (%)

Source: Bloomberg Finance LP / MNI

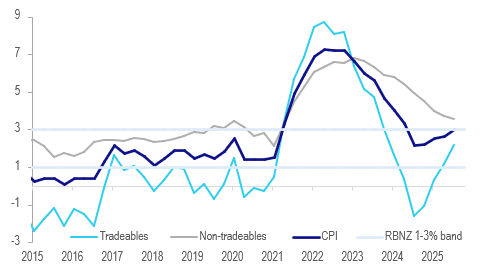

NEW ZEALAND: Q3 CPI Close To Expectations, November Easing Looks Likely

Q3 CPIs are unlikely to derail any further easing at the 26 November RBNZ meeting after the 50bp this month. Headline rose 1% q/q bringing annual inflation to 3.0% y/y from 2.7%, the top of the RBNZ’s target band but there had been fears that it could go above. Domestically-driven non-tradeables were slightly higher than the RBNZ expected at 1.1% q/q but the annual rate at 3.5% was in line. Its measure of core will print today at 1500 NZDT/1300 AEDT.

NZ CPI y/y%

- Core inflation remained well within the band with CPI ex food, energy and vehicle fuel rising 0.8% q/q & 2.5% y/y down from 2.7%.

- The 1% q/q jump in inflation was the largest in two years but is expected to be temporary as it was driven by a 8.8% q/q rise in local authority rates contributing 28% of the quarterly rise, this is measured once a year in Q3, a 12.2% q/q increase in vegetable prices contributed 15% and meat 4% q/q contributed 9.4%. There were offsets from pharmaceuticals (-4.4% q/q) and snacks (-1.8% q/q).

- The important non-tradeables inflation moderated to 3.5% in Q3 from 3.7%, the lowest since Q2 2021 and in line with the RBNZ’s August forecast. Electricity and council rates made the largest contributions while pharmaceuticals and real estate provided a partial offset.

- Tradeables has turned after troughing at -1.6% y/y in Q3 2024 it rose 2.2% y/y in Q3 2025 after Q2’s 1.2%, as the RBNZ expected.

- Goods prices are trending higher rising 2.1% y/y in Q3 after 1.4% while services inflation remains elevated it moderated in Q3 to 4.4% y/y from 4.7% but still higher than Q1’s 4.2%.

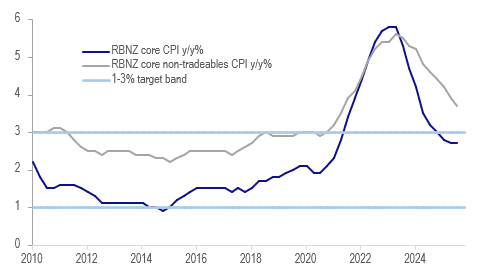

NEW ZEALAND: Measures Of Core Inflation Within RBNZ’s Band

While headline CPI inflation hit the top of the RBNZ’s 1-3% target band in Q3, underlying inflation remained within it but at the upper end. The RBNZ’s own measure of core from its sector factor model was stable at 2.7% y/y in Q3, remaining at the lowest since Q1 2021, while Statistics NZ’s CPI ex food, energy and vehicle fuel moderated 0.2pp to 2.5% y/y. While the RBNZ would like to see core inflation moderate further, it is likely to be reassured that non-tradeables moderated.

- Domestically-driven non-tradeables underlying inflation moderated 0.2pp to 3.7% y/y, the lowest since Q2 2021, whereas tradeables picked up 0.3pp to 1.0% y/y, highest since Q1 2024.

- The 10% trimmed mean rose 0.3pp to 2.6% y/y but 30% was stable at 2.1% y/y, close to the target mid-point.

- The next key inflation-related data are Q3 wages/labour market on 5 November followed by RBNZ Q4 inflation expectations on 11 November. The RBNZ wants to ensure that the recent uptick in price pressures isn’t feeding through to expectations.

NZ core CPI y/y%

Source: MNI - Market News/RBNZ

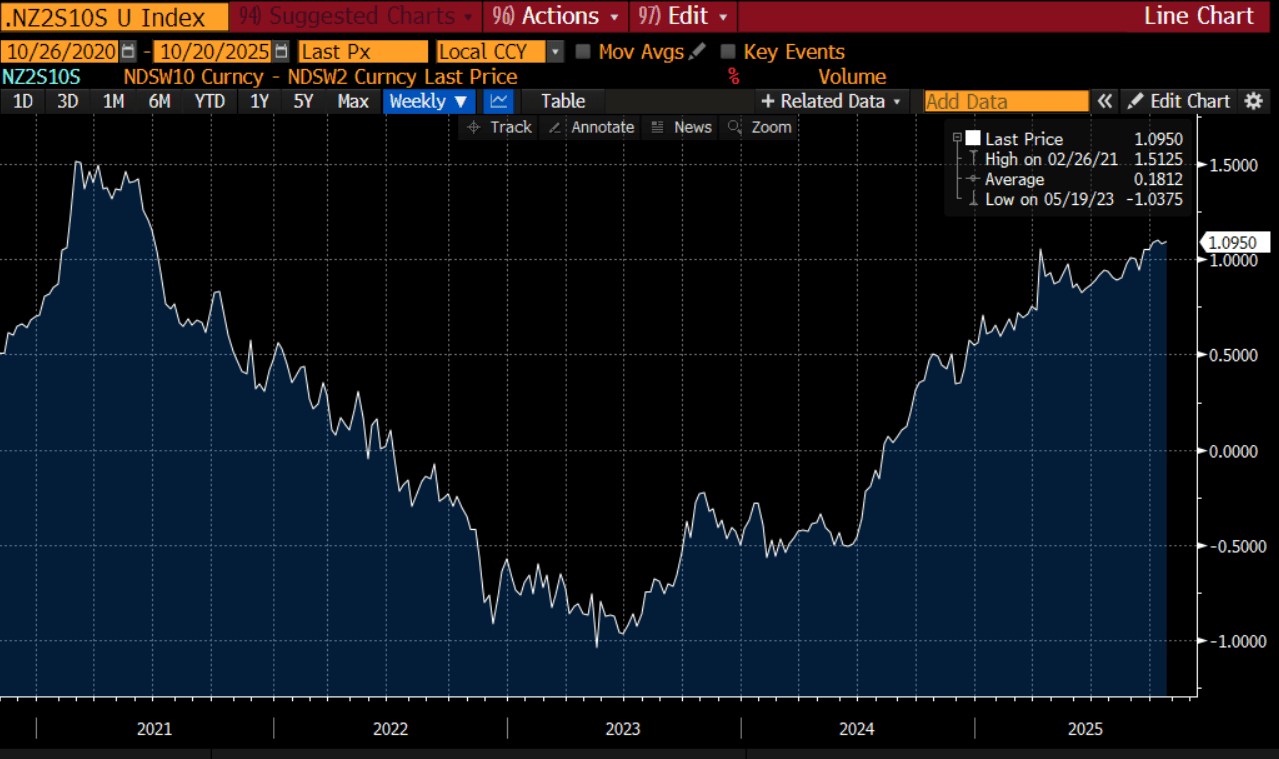

BONDS: NZGBS: Cheaper With 2s10s Swap Curve At Cycle Highs After Q3 CPI

NZGBs closed 2-4bps cheaper, with a steeper curve after today’s Q3 CPI data.

- While headline CPI inflation hit the top of the RBNZ’s 1-3% target band in Q3, underlying inflation remained within it but at the upper end. The RBNZ’s own measure of core from its sector factor model was stable at 2.7% y/y in Q3, remaining at the lowest since Q1 2021, while Statistics NZ’s CPI ex food, energy and vehicle fuel moderated 0.2pp to 2.5% y/y. While the RBNZ would like to see core inflation moderate further, it is likely to be reassured that non-tradeables moderated.

- Accordingly, Q3 CPIs are unlikely to derail any further easing at the 26 November RBNZ meeting after the 50bp this month.

- RBNZ dated OIS pricing is little changed across meetings. 26bps of easing is priced for November, with a cumulative 36bps by February 2026.

- Swap rates closed 2-4bps higher, with the 2s10s curve around cycle highs. (see chart)

- Tomorrow, the local calendar will see Trade Balance data

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond, NZ$175mn of the 4.25% May-36 bond and NZ$50mn of the 5.00% May-54 bond.

Bloomberg Finance LP

FOREX: USD/JPY Off Highs, 20-day EMA Downside Test Eyed

The USD has drifted a little lower in the first part of Monday dealings, with risk appetite mostly positive in the equity space (US futures building on gains from late last week, which has reduced safe have related flows. Trump comments set the stage for US-China trade talks, a key focus point for broader risk trends, with soybean purchases and rare earths key focus point. Still, Trump expressed optimism around scope for deals. USD/JPY spiked above 151.00 in early trade, with Takaichi all but now confirmed as the new PM (with LDP clinching a coalition agreement with minor party Ishin), but we sit lower now. NZD/USD has drifted a little higher, Q3 CPI was close to market and RBNZ expectations.

- The BBDXY index was last around 1207.20/25, so within recent ranges. USD/JPY has been the G10 focus point for most of today. Earlier highs were at 150.21, but we are back at 150.60/65 in latest dealings.

- Hawkish remarks from BOJ board member Takata have helped yen at the margins, which arguably weren't a surprise to the market, but still highlight BOJ hiking risks. Takaichi is generally seen as a negative for the yen, local bonds (given her pro growth/monetary lose comments in the past), while being positive for equities. Still, earlier comments from Takaichi and her advisors indicated they didn't intend to excessively weaken the yen, which along with Takaichi odds of being PM being elevated at the end of last week, may be limiting yen fallout so far today.

- For USD/JPY we remain above the 20-day EMA, near 150.15, but a clean break lower could see 148.93 targeted (the 50-day EMA).

- NZD/USD is a little higher at 0.5735/40, unable to test recent highs around 0.5760 so far. The Q3 CPI was close to expectations, but likely rules out a 50bps cut at the Nov policy meeting (25bps is currently priced).

- AUD/USD is close to 0.6500, little changed on the day in what is a quiet data week.

- SEK is up around 0.40% to 9.4130/35, although liquidity will be lighter for this pair in Asia Pac. The general risk on tone in the equity space, is a SEK positive.

- Looking ahead, the ECB’s Schnabel speaks while the Fed is in its media blackout ahead of the 29 October decision. The ongoing US government shutdown continues to impact public sector data releases. August euro area current account and construction and Canada’s Q3 BoC business survey print.

OIL: WTI Below Initial Support, Prices Pressured By Slower China Growth

Oil prices have moved in a narrow range during today’s APAC session with WTI falling 0.4% to $57.30/bbl, below initial support at $57.50, 30 May low, opening $54.89, 5 May low. Brent is down 0.4% to $61.07/bbl holding above round number support at $60.00. Crude found support on Friday from a more positive US-China trade outlook but fundamentals remain poor with supply increasing and demand softening. The USD index is flat.

- While Q3 China GDP was stronger than expected at 4.8% y/y, it was below the 5% target and Q2’s 5.2%. Also September property and investment data remained weak. Since China is the largest oil importer, the strength of its demand is important especially as the market’s focus is on expected record excess supply in 2026.

- US-China trade negotiations continue this week and Trump’s comments signal that there should be an agreement.

- In terms of geopolitics, attention is on Ukraine again with meetings due to take place including possibly between Trump and Putin. Ukraine hit an important southern Russian gas processing facility on the weekend which resulted in it stopping inbound flows.

- Later the ECB’s Schnabel speaks while the Fed is in its media blackout ahead of the 29 October decision. The ongoing US government shutdown continues to impact public sector data releases. August euro area current account and construction and Canada’s Q3 BoC business survey print.

Gold Prices Range Trading As US-China Talks Take Place This Week

Gold prices are slightly higher during today’s APAC trading after falling on Friday. Optimism that US-China trade talks will be successful in reaching an agreement put downward pressure on bullion early in the session with it falling to $4219.14/oz but it then recovered approaching $4270. It is now up 0.3% to around $4264.3 despite a slightly higher 2-year US yield and flat USD index.

- US-China trade negotiations continue this week and Trump’s comments signal that there should be an agreement.

- Gold has benefited from safe haven flows related to ongoing uncertainty related to the US government shutdown, the fiscal outlook and credit risks. US regional banks’ reports will be scrutinised for emerging problems related to risky lending.

- HSBC sees additional investment flows into gold and notes that prices could reach $5000/oz next year, according to Bloomberg.

- Silver is 0.5% higher at $52.19 after falling to $51.286 and then rebounding to $52.289. It fell over 4% on Friday and like gold it remains in overbought territory.

- Equities are rallying with the S&P e-mini is up 0.3%, Hang Seng up 2.4% and KOSPI +1.3%. Oil prices are lower with Brent down 0.3% to $61.11/bbl. Copper is 1.7% higher.

- Later the ECB’s Schnabel speaks while the Fed is in its media blackout ahead of the 29 October decision. The ongoing US government shutdown continues to impact public sector data releases. August euro area current account and construction and Canada’s Q3 BoC business survey print.

ASIA STOCKS: HSI Nears the 50-day EMA as China US Tensions Simmer

- Friday's losses did not follow into Monday with major bourses delivering solid gains, with some trading through key technical levels.

- The Hang Seng lost -2.5% on Friday and has regained that today, trending above the 50-day EMA . At 25,877 above now is the 20-day EMA of 26,137 which it has trended above for most of the period from May. China stocks had a day of data releases and GDP moderated as expected, whilst Industrial Production surprised to the upside following on from better than expected exports reported last week. The CSI 300 has rebounded also though only by +0.80% as it tries to break back above the 20-day EMA. Easing trade tensions supported China's stocks as US President Trump said that 'much higher tariffs threatened wouldn't be sustainable', as a new round of talks between the two countries is about to start.

- The NIKKEI was the star yet again today roaring up +2.9% reaching another new all time high of 48,956. The cooling of the US China tensions added to the news that the LDP is likely to sign a new coalition deal with the Innovation Party, with pro-stimulus candidate Sanae Takaichi now on track to be the next Prime Minister.

- Not to be outdone by its neighbour in Japan, the KOSPI is up +1.43% to reach yet another new high of 3,801 today.

- Having suffered at the hands of US trade tensions with focus on its purchase of Russian oil, the NIFTY 50 continues its turnaround story up 200pts in morning trading to reach a new all time high of 25,913.

ASIA STOCKS: South Korea & India Inflows Positive, Taiwan Still Lagging

Outside of outflows from Taiwan, net equity inflows were mostly positive to end last week. South Korea and India were the standouts in terms of inflows in the past week, while Taiwan saw further profit taking on recent inflow momentum. Focus for these markets will remain on broader equity trends, with markets stabilizing towards the end of last week, aided by US President Trump dialing down rhetoric in relation to the 100% tariff threat against China. South Korea officials also noted substantial progress was made in talks with the US from late last week. Both the Kospi and Taiex have had solid starts to the week. Taiwan inflows may be drawn back in if the Taiex continues to rally, although year to date inflows remain higher compared to South Korea.

- In India, Trump remarked earlier that India will continue to face high tariff levels if it doesn't restrict oil imports from Russia. India markets are out to start the week, but the Nifty finished strongly last week.

- In SEA we saw inflows into Indonesia, but mostly outflows elsewhere. Indonesia is the only economy with a positive 5-day sum of inflows.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 348 | 569 | 3572 |

| Taiwan (USDmn) | -924 | -2857 | 6745 |

| India (USDmn)* | 245 | 968 | -16267 |

| Indonesia (USDmn) | 183 | 118 | -3113 |

| Thailand (USDmn) | -64 | -159 | -3099 |

| Malaysia (USDmn)* | -3 | -183 | -4130 |

| Philippines (USDmn) | -4 | -15 | -710 |

| Total (USDmn) | -219 | -1556 | -17002 |

| * Data Up To Oct 16 |

Source: Bloomberg Finance L.P./MNI

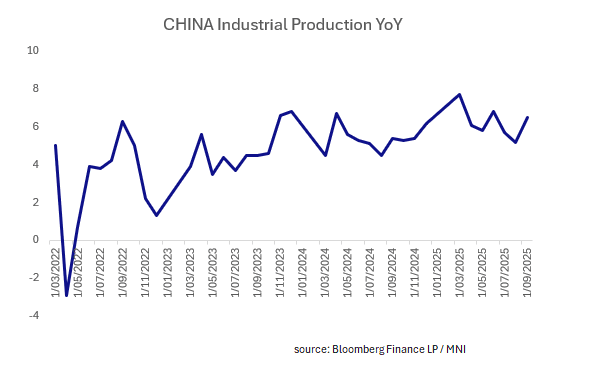

CHINA: A Moderation of 3Q GDP as Industrial Production Accelerates

- China's third quarter GDP rose +4.8% YoY, above estimates of +4.7%

- Following both Q1 and Q2 GDP releases being firmer than expected, it was anticipated that third quarter would be lower.

- The seasonally adjusted QoQ result topped expectations at +1.1%, from +0.8% and Year to Date remained above 5% at 5.2%

- The largest data surprise was Industrial Production which snapped back above it's 3-year average and at 6.5%, consistent with the better than expected exports reported earlier this month.

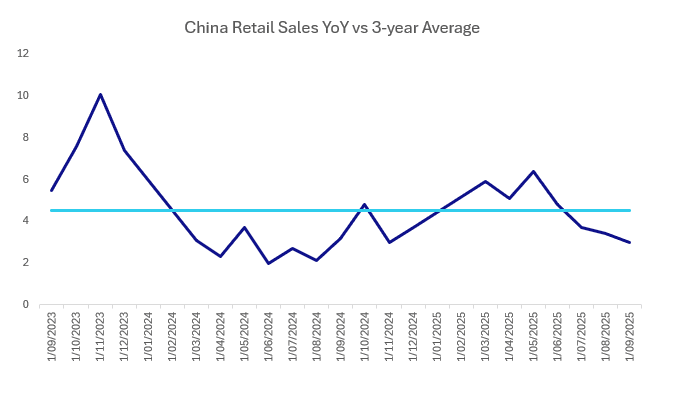

- Forecasts for policy changes from the 4th Plenum emphasize a focus on the consumer and as retail sales in September continued to splutter, the likelihood of this grows.

- Retail sales remains below the 3-Yr average expansion of 4.5% at 3.0% today, as domestic demand falters. This data does not capture golden week where by all accounts travel and service related expenditure was up.

- Markets have reacted positively to the releases with the CSI 300 jumping after the releases. Government bond's reaction has been more reserved witht he 10-Yr giving back some of last week's gains with yields higher by +1bp to t 1.84%

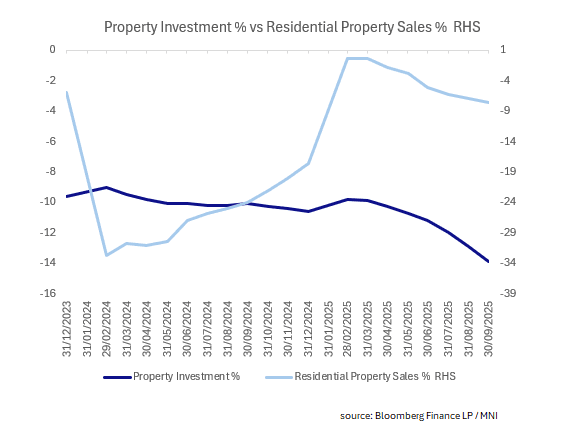

CHINA HOUSING: Adjustment Continues as Investment and Sales Fall Further

- Whilst the decline in property prices is a glaring reflection of the plight of the sector, the activity led data is more telling.

- September's Property Investment YTD release declined further to -13.9% for a sixth successive month of increasing declines.

- New home sales value declined 7.6% YoY Ytd to CNY5.53tn with a 5.6% decline in sales area whilst construction fell 18.9% YoY YTD.

- Residential property sales and been on an improving (albeit still negative) up to March, het has fallen month on month since with September's decline of -7.6% the largest decline this year.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 20/10/2025 | 0600/0800 | ** | PPI | |

| 20/10/2025 | 0800/1000 | ** | EZ Current Account | |

| 20/10/2025 | 0800/1000 | ECB Schnabel at Macroeconomics and Finance Conference | ||

| 20/10/2025 | 0900/1100 | ** | EZ Construction Output | |

| 20/10/2025 | 0900/1100 | *** | EZ GDP 4th (Final) | |

| 20/10/2025 | 1230/0830 | * | Industrial Product and Raw Material Price Index | |

| 20/10/2025 | 1400/1600 | ECB Schnabel Panel at Macroeconomics and Finance Conference | ||

| 20/10/2025 | 1430/1030 | ** | BOC Business Outlook Survey | |

| 20/10/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 20/10/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 21/10/2025 | 0600/0700 | *** | Public Sector Finances | |

| 21/10/2025 | 0700/0900 | ECB Lane at Macroeconomics and Finance Conference | ||

| 21/10/2025 | 0900/1100 | * | government debt | |

| 21/10/2025 | 0900/1100 | * | government deficit | |

| 21/10/2025 | 0900/1000 | BOE Saporta Fireside Chat at Islamic Development Bank | ||

| 21/10/2025 | 1030/1130 | BOE Bailey & Breeden on Private Markets at Financial Services Regulation Committee | ||

| 21/10/2025 | 1100/1300 | ECB Lagarde Keynote at Norges Bank Climate Conference | ||

| 21/10/2025 | 1230/0830 | *** | CPI | |

| 21/10/2025 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 21/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index |