MNI EUROPEAN MARKETS ANALYSIS: Oil Edges Up Amid Sanction Risk

- US Tsy futures sit a touch softer, with no cash trading today with Japan markets out. The USD is down against most of the G10 but mixed against Asia FX.

- China August activity data was weaker than forecast with fixed asset investment only up 0.5% ytd y/y. Market impact has been negligible though, with China equities continuing to rise.

- Oil prices have trended higher in today’s APAC trading after rising over last week. Further sanctions on Russia are being discussed by the EU and US but President Trump has said that NATO needs to stop importing Russian crude (Turkey and Hungary are the main ones} before he’ll impose further restrictions.

- Later US September Empire manufacturing and July euro area trade print. The ECB’s Lagarde and Schnabel speak.

MARKETS

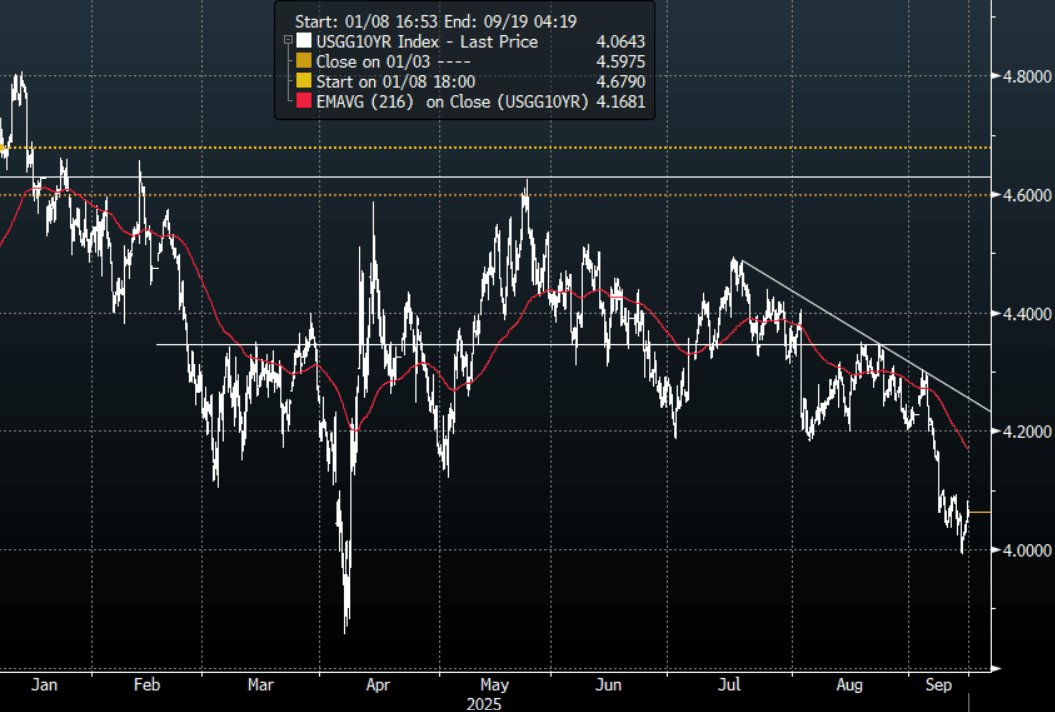

US TSYS: Asia Wrap - Futures Edge Lower On A Japanese Holiday

The TYZ5 range has been 113-02 to 113-07 during the Asia-Pacific session. It last changed hands at 113-05+, down 0-03+ from the previous close.

- 10-Year Yields found some supply around 4.00% and have retraced a little as the market looks towards the FOMC this week. The first buy-zone is now back towards the 4.20% area where I suspect decent demand should return initially. A sustained break through 4.00% is needed for the focus to then turn towards the 3.80% area.

- Alexander Stahel on X: “The market is now pricing in a fairly political Fed that’s going to overease. That’s the concept that seems the danger. Fed Funds at 4.375; market pricing in 3 for the long run projection. Anyway, 25bps this week seems a given. But we then need a machine gun of cuts.”

- RenMac on X: “Fed Should Go 50… But Likely Won’t – Neil Dutta”

- (Bloomberg) -- The Congressional Budget Office now expects higher inflation and unemployment this year and slower economic growth, after taking into account President Donald Trump’s tax law, tariffs and lower net immigration.

- Bob Elliott X: “Fed looks set to ignore a near 3% core PCE print as they transition to cutting. While the Fed can ignore this reality, households can't. The continued price pressures are set to curtail their real spending ahead.”

- Data/Events: Empire Manufacturing

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE BONDS: Weak Start To The Week, Jobs On Thurs

ACGBs (YM -3.0 & XM -6.0) are weaker and hovering near session lows on a relatively subdued session.

- There has been no cash US tsy trading today with Japan out. TYZ5 is moderately cheaper.

- Cash ACGBs are 3-6bps cheaper with the 3/10 curve steeper.

- The bills strip is flat to -4 across contracts with a steepening bias.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in September is given a 9% probability, with a cumulative 28bps of easing priced by year-end.

- Today, the local calendar was empty ahead of an RBA Hunter's Fire-Side Chat tomorrow.

- The focus this week, however, will be on Thursday's August jobs data. Employment is forecast to rise 21k after July's +24.5k with the unemployment rate expected to remain at 4.2%. It will also be important to monitor underemployment, the split between full-time & part-time and hours worked. The RBA is currently expected to leave rates unchanged on September 30 as it waits for Q3 CPI on October 29.

- This week, the AOFM plans to sell A$1200mn of the 4.25% 21 December 2035 bond on Wednesday and A$1000mn of the 1.00% 21 December 2030 bond on Friday.

BONDS: NZGBS: Closed Cheaper Ahead Of A Busy Week Of Local Data

NZGBs closed 2-4bps cheaper, with the 2/10 curve steeper.

- Swap rates closed 1-3bp higher.

- (Bloomberg) “Economic activity is expected to pick up over the second half of 2025 but there is uncertainty surrounding the pace of recovery, the Treasury Dept. says in its Fortnightly Economic Update released Monday in Wellington.”

- The focus of the week will be on Thursday’s Q2 GDP data release. Bloomberg consensus is in line with the RBNZ’s August forecast of -0.3% q/q bringing the annual rate to flat after declining 0.7% y/y in Q2. 25bp rate cuts are expected at both the October 8 and 26 November meetings.

- August monthly price series including food, electricity, rent, petrol and travel print on Tuesday. Food price inflation has been picking up. There is a risk that Q3 CPI inflation exceeds the 3% top of the RBNZ’s target band. The bank is forecasting 3% for the quarter.

- On Wednesday, Q3 current account data is out and the deficit is expected to narrow to 4.8% of GDP but with it widening to $2.7bn from $2.32bn in Q2.

- There is also Westpac Q3 consumer confidence on Wednesday.

- RBNZ dated OIS pricing closed little changed across meetings. 22bps of easing is priced for October, with a cumulative 40bps by November 2025.

FOREX: Yen Buying A Feature Las Week, USD Mostly Sold Elsewhere - Per CFTC

In the week ending Sep 9 (last Tuesday) the bias from the CFTC FX positioning update was to sell the USD. The standout last week was JPY buying. In the leveraged space, we saw +17.3k of JPY buying, which cut the outright short to under 50k. On the asset manager side, net longs were added to by +8.8k. This comes as broader USD sentiment remains softer amid rising Fed easing expectations. Still, USD indices, while softer, haven't broken definitely lower (the BBDXY remains above July lows, last near 1198.3). For USD/JPY, last Tuesday (which was the CTCF reference period), marked the recent low point for USD/JPY with the pair unable to test back under 147.00 since then.

- EUR/USD longs were added to in both the leveraged and asset manager space. GBP trends were mixed, little change in leveraged positioning, while asset managers cut pound shorts.

- For the AUD, we saw leveraged investors cut back on shorts, as AUD/USD consolidated above 0.6600. Still, asset managers were happy to maintain shorts.

- Elsewhere, aggregate positioning shifts weren't large, with NZD seeing largely offsetting flows between leveraged investors and asset managers. For CAD, modest selling was evident, adding to existing outright shorts.

Table 1: CFTC Positioning Change & Outright Position By Major Currency

| Leveraged Contracts | Asset manager Contracts | |||

| Weekly Change | Outright Position | Weekly Change | Outright Position | |

| JPY | 17323 | -49591 | 8812 | 87239 |

| EUR | 7020 | 8837 | 3649 | 408764 |

| GBP | -288 | 21012 | 9522 | -70426 |

| AUD | 6779 | -5081 | -2308 | -68333 |

| NZD | -2159 | -1874 | 2006 | -3121 |

| CAD | -1371 | -47670 | -757 | -65033 |

| CHF | -1584 | 48 | -1980 | -42307 |

| MXN | -5594 | 28997 | 2328 | 37671 |

Source: CFTC/Bloomberg Finance L.P./MNI

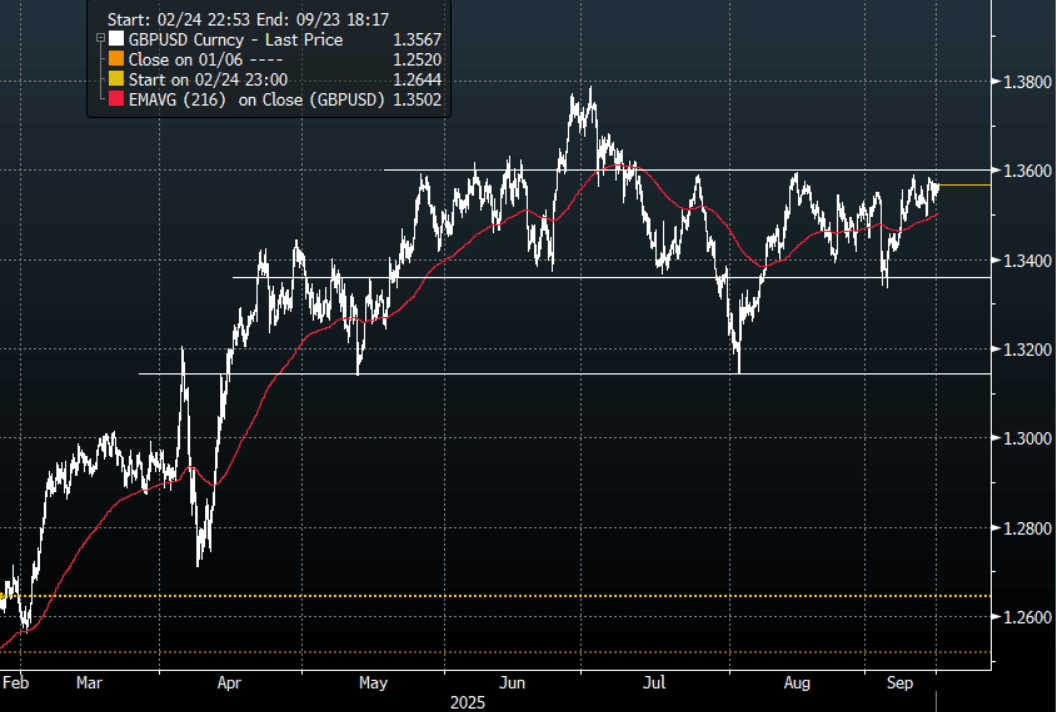

FOREX: Asia FX Wrap - Can The USD Break Lower Before FOMC ?

The BBDXY has had a range of 1197.50 - 1199.03 in the Asia-Pac session; it is currently trading around 1197, -0.05%. The USD could not follow through on Friday and remains frustratingly above its recent support. A sustained break below 1197/1195 is needed to regain the momentum lower and retest the year's lows towards 1180 where demand should return initially. A break sub 1180 would be extremely bearish, should the USD start another leg lower it would have big implications for FX and potentially see a lot of the recent ranges in G10 broken. With the FOMC approaching we might see the ranges continue until the market hears what Powell has to say about the potential new rate cutting cycle the market is pricing in.

- EUR/USD - Asian range 1.1722 - 1.1748, Asia is currently trading 1.1730. The pair consolidated Friday night. EUR is still within its wider 1.1350-1.1850 range with a bias to the topside.

- GBP/USD - Asian range 1.3549 - 1.3568, Asia is currently dealing around 1.3565. The pair is back in the middle of its recent 1.3350-1.3650 range, but price action suggests it may be looking to retest the range highs.

- USD/CNH - Asian range 7.1197 - 7.1272, the USD/CNY fix printed 7.1056, Asia is currently dealing around 7.1200. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.10%, Gold $3644, US 10-Year 4.064%, BBDXY 1198, Crude Oil $63.06

- Data/Events : Germany Wholesale Price Index, Italy Trade Balance, EZ Trade Balance

Fig 1: GBP/USD Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

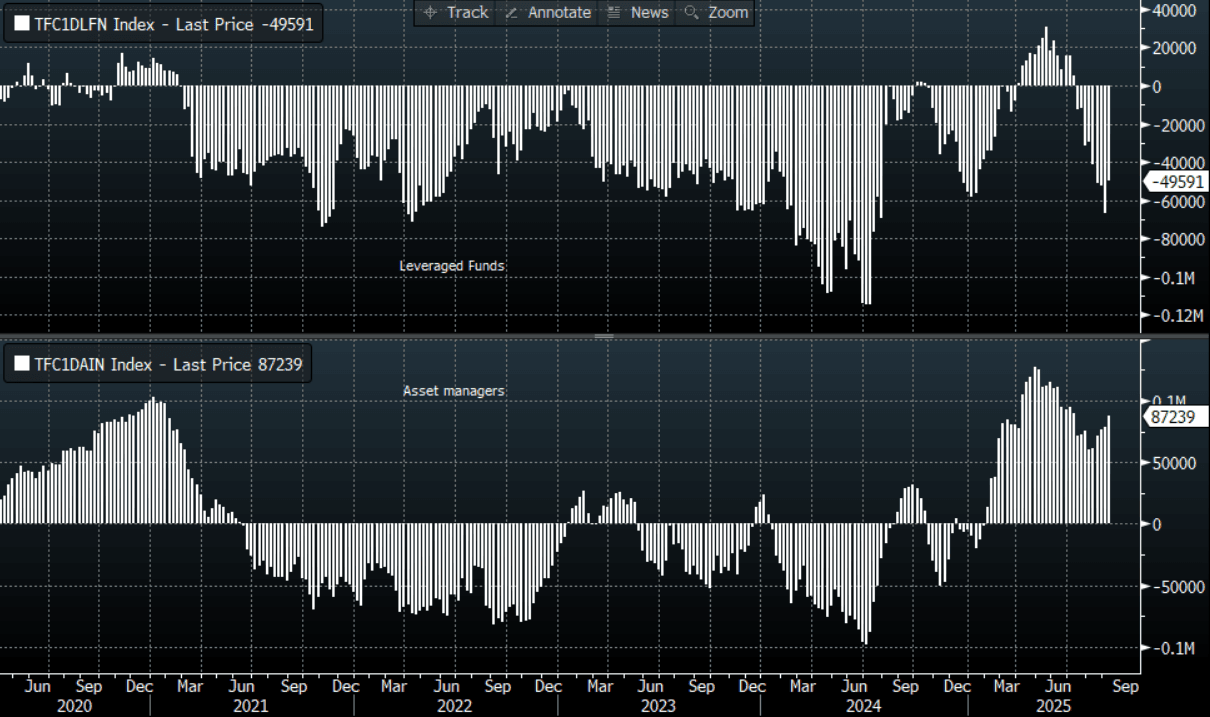

JPY: Asia Wrap - USD/JPY Trading Sideways On A 147 Handle

The USD/JPY range has been 147.37 - 147.79 in the Asia-Pac session, it is currently trading around 147.40, -0.20% on a Japanese holiday. USD/JPY continues to trade sideways with no clear trend. The price remains in the middle of its recent 146-149 range, and we need a convincing break to see a clearer direction again. CFTC data shows leveraged funds paring back some of their short JPY position last week but remain core short, looking for this support to continue to hold. A move back below 145/146 is needed to potentially start seeing these positions being flushed out.

- MNI INTERVIEW: Powell Won't Signal String Of Fed Cuts-Lockhart. Federal Reserve Chair Jerome Powell will justify next week’s widely expected interest rate cut by citing rising downside risks to employment but refrain from signaling a string of cuts beyond September because the Fed must also contend with inflation heading in the wrong direction, former Atlanta Fed President Dennis Lockhart told MNI.

- "JAPAN'S HAYASHI TO ANNOUNCE ENTRY IN LDP RACE TOMORROW: NIKKEI" - BBG

- "TAKAICHI LEADS LDP RACE AT 29%, KOIZUMI AT 25% IN YOMIURI POLL" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 150.00($1.04b).Upcoming Close Strikes : 146.00($1.41b Sept 16), 150.00($1.49b Sept 16), 145.70($1.22b Sept 17) - BBG.

- CFTC data shows last week asset managers again added to their JPY longs again as they look to rebuild their position +87239( Last +78427), leveraged funds reduced their short position perhaps losing confidence the support will continue to hold -49591(Last -66914).

Fig 1 : JPY CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia Wrap - AUD/USD Consolidates Around 0.6650

The AUD/USD has had a range of 0.6641 - 0.6662 in the Asia- Pac session, it is currently trading around 0.6660, +0.20%. US Equities traded sideways as the market turned its focus towards the FOMC this week and what the potential upcoming cutting cycle could look like. The AUD consolidates around 0.6650, trying to find the momentum it needs to accelerate above this pivotal area. Should the USD break and extend lower we could see the AUD gain momentum above 0.6650/0.6700 and potentially target levels back towards 0.6900/0.7000. The price action suggests dips will be supported for now as we await confirmation of this potential break higher, the first buy-zone is back towards the 0.6550 area.

- Bloomberg - “Aussie to Extend March Higher as Shorts Bail, Yuan Climbs. AUD/USD is pressing into a higher range, fueled by yuan strength, looming Fed cuts and leveraged shorts scrambling to cover. Net Aussie shorts are the smallest since November last year, and on the present course are likely to turn into longs with the FOMC to provide a dovish rate cut this week.”

- MNI BRIEF: China's August Investment Slows To Five-year Low. China’s fixed-asset investment growth decelerated to 0.5% y/y in the Jan–Aug period from the previous 1.6%, marking the slowest pace since Aug 2020 and missing an expectation of 1.5%, National Bureau of Statistics data showed Monday.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6500(AUD309m). Upcoming Close Strikes : 0.6600(AUD794m Sept 18) - BBG

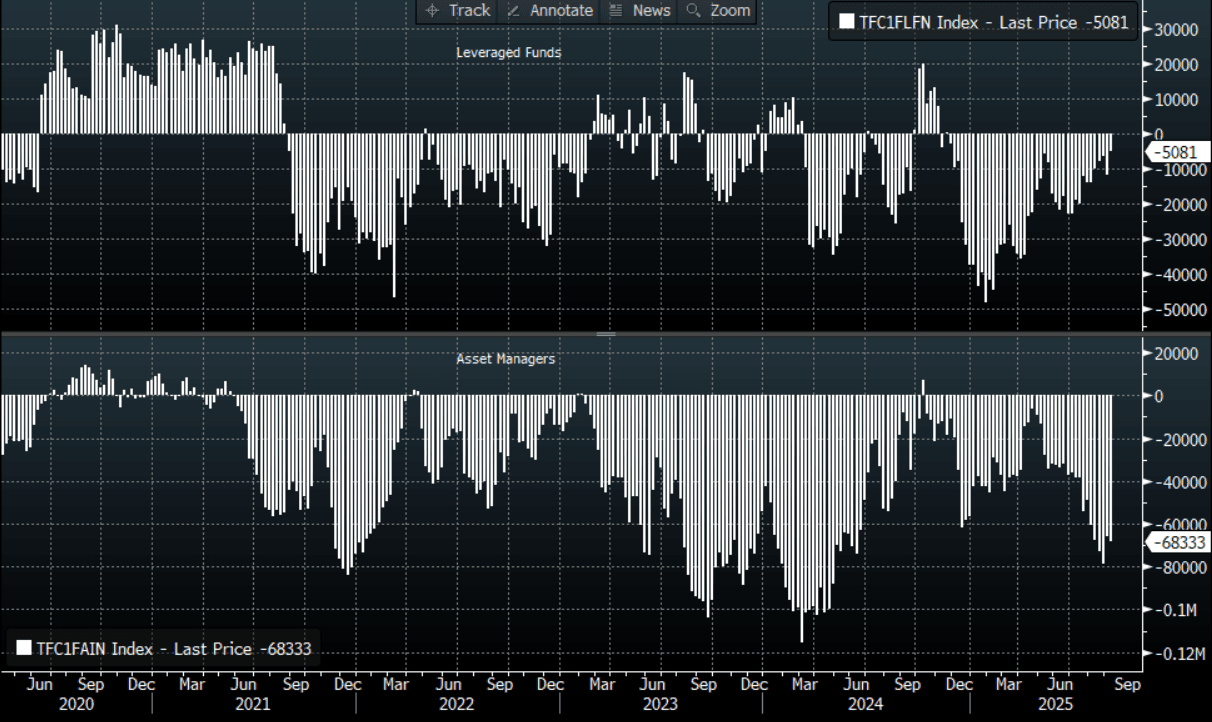

- CFTC Data last week shows Asset managers slightly increasing their shorts -68333(Last -66025), the Leveraged community pulled back the shorts they had just started to rebuild -5081(Last -11860).

- AUD/JPY - Asia-Pac range 98.06 - 98.27, Asia is trading around 98.20. The pair consolidated its gains on Friday night, turning the focus back towards the 99.00/100.00 area. Dips back towards 96.50/97.00 should be expected to be supported now first up.

Fig 1: AUD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

NZD: Asia Wrap - NZD/USD Doing Some Work Below 0.6000

The NZD/USD had a range of 0.5947 - 0.5966 in the Asia-Pac session, going into the London open trading around 0.5965, +0.20%. US Equities traded sideways as the market turned its focus towards the FOMC this week and what the potential upcoming cutting cycle could look like. The NZD topped out just below 0.6000 as momentum higher stalled. The USD though is still looking vulnerable, which continues to support the NZD. A close back above 0.6000 would negate any semblance of the downward pressure it was exhibiting, but for those that have a bearish view this remains a decent entry point to express that. We might have to wait for the FOMC to get some clarity as CFTC Data shows positions are light with conviction obviously low.

- (Bloomberg) -- New Zealand’s services industry contracted for an 18th straight month in August, suggesting that an economic rebound in the third quarter could be more sluggish than expected. Reserve Bank Governor Christian Hawkesby said last week that early indicators of third-quarter activity gave him confidence of an economic rebound, and he reiterated that policymakers’ central projection is that the Official Cash Rate will be cut to 2.5% by the end of the year

- "NZ TREASURY SEES UNCERTAINTY OVER PACE OF 2H ECONOMIC RECOVERY, NZ TREASURY COMMENTS IN FORTNIGHTLY ECONOMIC UPDATE" - BBG

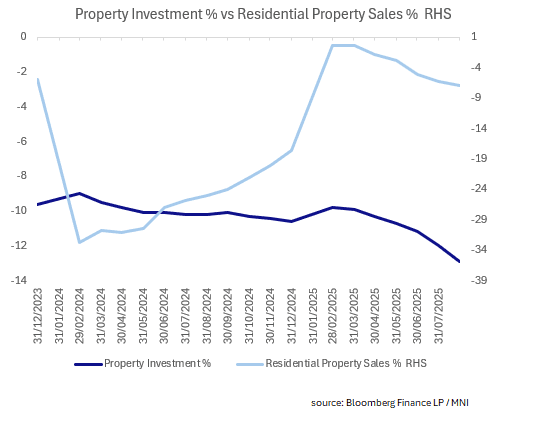

- China Weak Property Data Continues: Property Investment YTD YoY and Residential Property Sales YoY declined more than expected in August. Property Investment YTD YoY fell -12.9%, its largest monthly decline. It has not recorded a positive monthly result since March 2022. Residential Property Sales YoY declined -7.0% in August, the worst result for 2025. It has not recorded a positive monthly result since July 2023.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5825(NZD1.01b Sept 17), 0.5900(NZD860m Sept 17), 0.6250(NZD427m Sept 17) - BBG

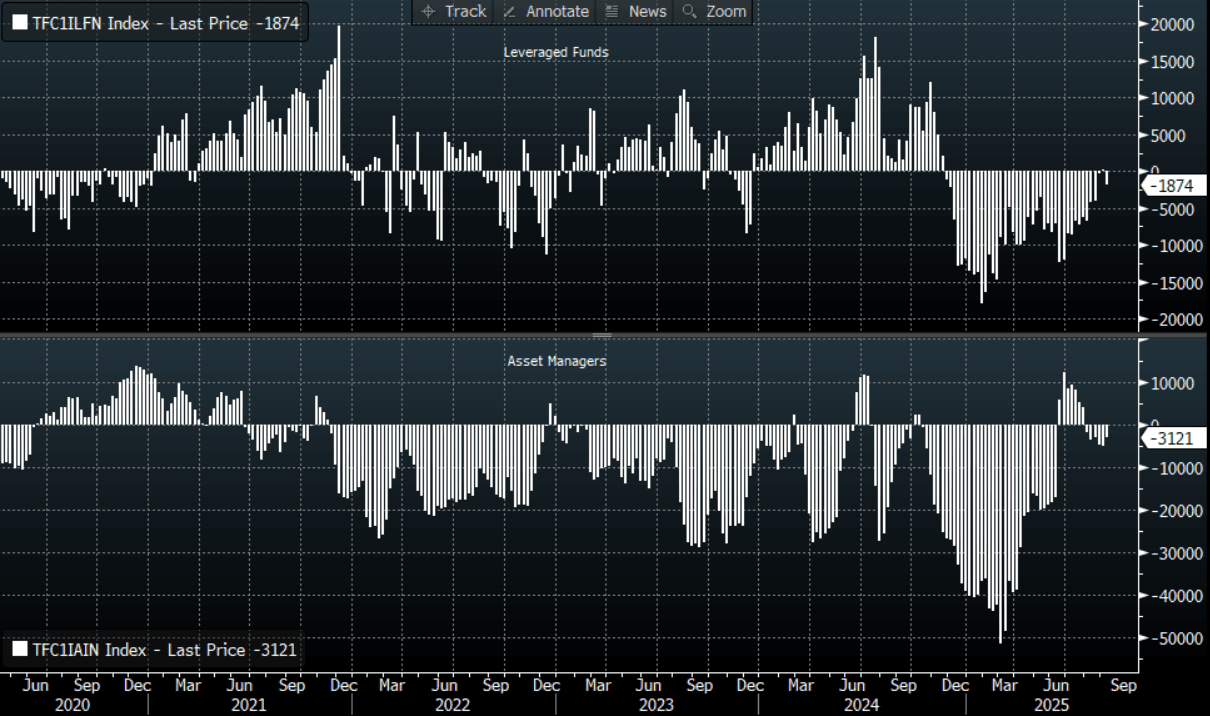

- CFTC Data of last week shows Asset Managers added slightly to their new short position in the NZD -5127(Last -4743), the Leveraged community have completely exited their short and have turned a fraction long +285(Last -225)..

- AUD/NZD range for the session has been 1.1150 - 1.1176, currently trading 1.1175. The Cross is consolidating above 1.1100, dips back towards 1.1000/1.1050 should be supported now. A break above the multiple highs towards the 1.1200 area is needed to regain the momentum higher.

Fig 1: NZD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: China Kicks off the Week with Strong Gains

Following strong opposition from investors, the Korean government's policy to lower the capital gains tax threshold for equity investors has finally been dumped, marking the first major about face for the new government. The NIKKEI is closed today for a public holiday, having closed Friday at new highs. The focus for investors for the week ahead will be the Federal Reserve meeting this week as markets globally hope for a rate cut.

- The major bourse in China are off to a good start this week, with the Hang Seng up +0.30%, the CSI 300 +0.85%, Shanghai up +0.22% and Shenzhen up +0.65% on a day when economic data shows the economy continues to expand.

- The KOSPI is up on the taxation news, by +0.50%.

- The TAIEX in Taiwan one of the few decliners, down -0.20%.

- The Jakarta Composite is up +0.75%

- The NIFTY 50 is opening with modest falls of -0.05%.

ASIA STOCKS: South Korea Records Best Inflow Day Since Mid 2024, As Kospi Surges

Friday delivered strong inflows for both South Korea and Taiwan. South Korea saw over $1.1bn in net inflows, which was the strongest inflow day since mid-June last year. It also bought the 5-day sum of net inflows to over $3bn. The Kospi has surged to fresh record highs, pushing through the 3400 level in the first part of trade today. Onshore media is reporting that the government won't go through with plans to lower the threshold for stock capital gains (with original plans being this would be lowered to 1bn won form the current 5bn won). Such a step was suggested by President Lee last week, so today's outcome is unlikely to surprise the market much.

- For Taiwan, the 5-day sum of net inflows remained very elevated last week at +$5.6bn. Broader tech sentiment rallied last week, while the onshore Taiex index is just off record highs. Chip/AI demand sentiment remains firm.

- Elsewhere, outflow momentum from Indonesia slowed to nearly flat on Friday. Still, we had decent outflows the week of just over $400mn. This week we have the BI decision, where no change is expected. It will be a focus point though given the new FinMin has a strong pro-growth stance.

- The see-saw nature of Indian flows continued, while other markets saw little net aggregate shifts in terms of flows.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 1165 | 3034 | -2299 |

| Taiwan (USDmn) | 910 | 5606 | 7405 |

| India (USDmn)* | -387 | 188 | -15524 |

| Indonesia (USDmn) | -2 | -401 | -3728 |

| Thailand (USDmn) | -24 | -66 | -2552 |

| Malaysia (USDmn)* | 25 | -2 | -3808 |

| Philippines (USDmn) | 5 | -3 | -727 |

| Total (USDmn) | 1693 | 8357 | -21233 |

| * Data Up To Sep 11 |

Source: Bloomberg Finance L.P./MNI

OIL: Crude Trends Higher As Sanction Risk The Focus

Oil prices have trended higher in today’s APAC trading after rising over last week. WTI is up 0.5% to $63.03 following a peak of $63.13 earlier, while Brent is 0.5% higher at $67.33 after reaching $67.43. Current geopolitical risks are having the opposite effect to supply/demand fundamentals with a large market surplus expected in 2026. The USD index is slightly lower.

- Further sanctions on Russia are being discussed by the EU and US but President Trump has said that NATO needs to stop importing Russian crude (Turkey and Hungary are the main ones} before he’ll impose further restrictions. US Treasury Secretary Bessent said that the G7 should also place duties on countries buying Russian oil.

- Ukrainian attacks on Russian energy infrastructure continued over the weekend.

- China’s August data was generally softer than consensus expected but it didn’t worry oil prices.

- The key event this week is the Fed’s 17 September decision. With a 25bp rate cut widely expected, attention will be on the tone of comments from Chair Powell to gauge the outlook for policy.

- Later US September Empire manufacturing and July euro area trade print. The ECB’s Lagarde and Schnabel speak.

Gold Slightly Higher As Awaits Direction From The Fed This Week

Gold prices are off today’s low of $3626.66/oz to be up slightly at $3644.5. It reached a high of $3646.93. It has found support from a slightly lower US dollar. The key event for bullion this week will be Wednesday’s Fed decision (a 25bp cut is widely expected), the accompanying comments and Chair Powell’s tone. The outlook for Fed policy is likely to drive direction.

- Gold continues to trade below the 9 September high of $3674.3 but it remains in a clear bull cycle. Initial support is at $3579.7, 8 September low.

- Silver is up 0.2% to $42.27 off the intraday high of $42.314. The trend remains bullish with the metal exceeding resistance at $42.173 today opening $42.323. The 20-day EMA is at $39.986.

- Equities are generally stronger with the S&P e-mini up 0.1% and CSI 300 +0.9% but ASX down 0.2%. Oil prices are higher with WTI +0.6% to $63.06/bbl. Copper is up 0.3%.

- Later US September Empire manufacturing and July euro area trade print. The ECB’s Lagarde and Schnabel speak.

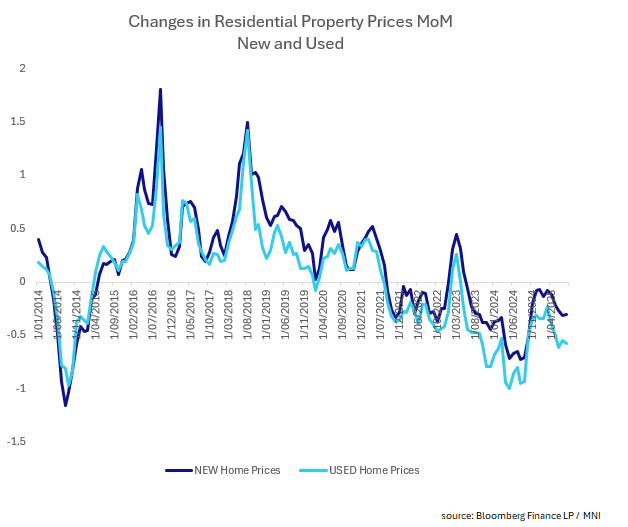

CHINA: No Surprises from House Prices in August

- New and used house prices continued to decline in August, with used home prices down more than July.

- New home prices declined -0.30% , from -0.31% in July.

- The last month that recorded a positive print was May 2023.

- Used home prices declined -0.58%, from -0.55% in July.

- The last month that recorded a positive print was April 2023.

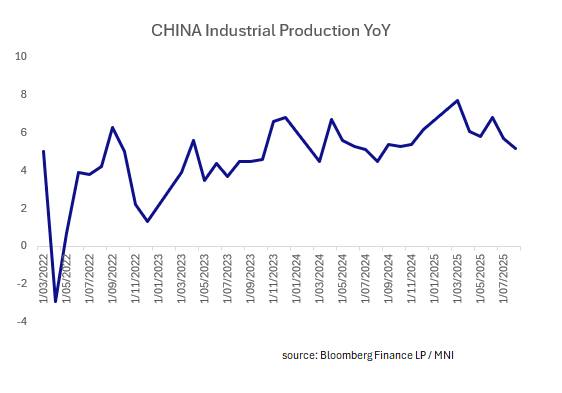

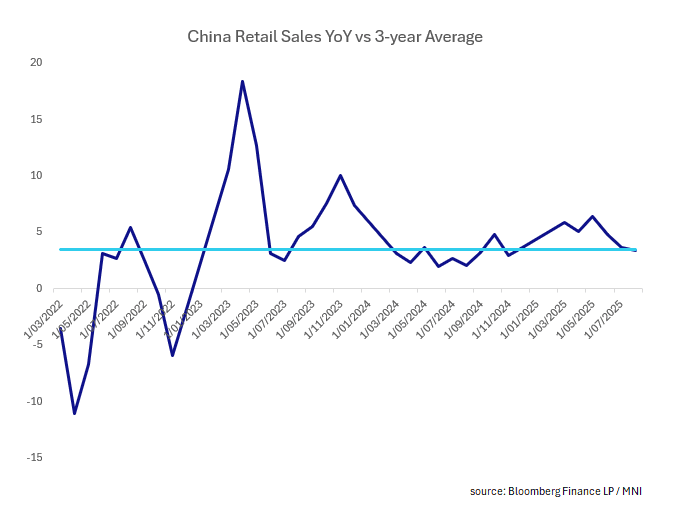

CHINA: Key Data Stable in August

- Multiple data releases today pointed to a very modest slowing in the economic expansion in China.

- Retail sales expanded +3.4% for August, below expectations of +3.8% and prior month of +3.7%.

- Industrial Production YoY expanded +5.2%, missing expectations of +5.6% and below the prior month of +5.7%.

- Investments in Fixed Assets Ex Rural YTD YoY rose a mere +0.5% from +1.6% in July.

China's moderation is following a better than expected first half, with the data showing a likely return to expectations rather than anything worrying.

CHINA: Weak Property Data Continues

- Property Investment YTD YoY and Residential Property Sales YoY declined more than expected in August.

- Property Investment YTD YoY fell -12.9%, its largest monthly decline. It has not recorded a positive monthly result since March 2022.

- Residential Property Sales YoY declined -7.0% in August, the worst result for 2025. It has not recorded a positive monthly result since July 2023.

- Recently Shenzhen announced measures to support the property prices and bring their policies in line with Beijing and Shanghai. The announcements as of September 6 included easing of home purchase restrictions for non residents, removal of home purchase limits and lowering down payment requirements.

INDIA: Country Wrap: PM Announces Spending Package

Market Summary: he NIFTY 50 is opening with modest falls of -0.05%, after finishing last week with gains of +1.50%. The Rupee is flat Monday at 88.26 and bonds are softer with the 10-Yr at 6.49%

- Prime Minister Narendra Modi announced and inaugurated projects worth 163 billion rupees ($1.85b) during his visit to the north-eastern states of Meghalaya and Manipur on Saturday. Modi inaugurated development works and kicked off projects worth 90b rupees across railways, roadways and energy in Mizoram, according to a government release. Announced projects worth 73b rupees in Manipur, according to another release (source PM's office)

- The Consumer Price Index (CPI)-based retail inflation in August rose to 2.07% from earlier 1.61% in July, data by the Ministry of Statistics and Programme Implementation (MoSPI) said on Friday. It said the food inflation for August stood at -0.69%, rising 107 basis points compared to July. Corresponding inflation rates for rural and urban areas are -0.70% and -0.58%, respectively. Food inflation in rural areas was at -1.74% in August. It increased for urban areas from -1.90% during the same period last month. (source Asia News)

SOUTH KOREA: Country Wrap: CGT Changes Dropped

Market Summary: The KOSPI is up on the taxation news, by +0.50%, following last week's strong gains. The Won is up +0.42% to 1,387.80 but remains weaker over the last five trading days. Bonds are seeing steeper curves with the KTB 10-Yr up at 2.84%

- Taiwan is expected to overtake Korea in per capita GDP this year, data showed Sunday. The reversal after 22 years is explained by Korea’s weakening growth momentum coupled with Taiwan’s rise as a technological and economic powerhouse in the global economy. (source Korea Times)

- The government has decided to keep the threshold for capital gains tax on stock holdings at the current level of 5 billion won ($3.6 million), Finance Minister Koo Yun-cheol said Monday. (source Korea Times)

ASIA FX: TWD Softer, USD Weaker Elsewhere, China Data Misses Ignored

In NEA markets, the bias, outside of TWD, has been for softer USD levels.

- USD/CNH is still holding above 7.1200, but largely ignored a softer round of August data from earlier. The data pointed to softer activity trends in the month, with retail sales and IP slowing further in y/y terms, while fixed asset investment was up only 0.5% ytd y/y. House prices also continued to fall in August. Offset has come from a firmer equity market backdrop, with tech continuing to lead. The USD/CNY fix remains above 7.1000 and until we break lower, this may cap USD/CNH downside.

- Spot USD/KRW has fallen around 0.35%, last near 1388. This keeps us within recent ranges, although the won lagged broader USD softness last week. Local equities are up, pushing to fresh highs above 3400. Earlier headlines crossed that the government wouldn't go ahead with plans to lower the stock market capital gains threshold, but such a move was spoken about last week by President Lee. Focus remains on US-South Korea trade talks, with South Korea worried about the $350bn investment pledge impact on FX markets.

- Spot USD/TWD is slightly higher, but holding under 30.30 at this stage, wedged between key EMAs. The pair has consolidated has the recent run lower, while onshore equities have also stalled around recent highs.

- Spot USD/HKD has tested sub 7.7750, fresh lows back to the first half of May. USD/HKD looks to be running a little ahead of softer US-HK yield differentials, but the wedge isn't large.

ASIA FX: USD/Asia Pairs Edge Higher In SEA, But Recent Ranges Holding

In South East Asia FX markets, trends have been modestly skewed towards USD gains, but aggregate moves have been modest so far. PHP has lost around 0.30%, while THB and IDR are off a close to 0.10%. Malaysian markets are out today, while USD/SGD has edged down a little.

- USD/PHP is back close to 57.30, up +0.30% from end Friday levels. This keeps us within recent ranges, with earlier Sep highs just above 57.50. EMAs are all lower than current spot levels with the 100-day back close to 56.97. BSP Governor Remolona expressed concern around the PHP slide late last week. Central bank resolve could be tested if we re-visit the 57.50/55 region. On the data front, July remittances growth was a touch below forecasts, printing 3.0%y/y (against 3.2% projected and 3.7% prior).

- USD/IDR is has drifted a little higher, the pair last near 16400. This is sub recent highs around 16500, when market sentiment was tested post the replacement of the FinMin. Still, BI has stated a 16300 target for the currency in recent weeks.

- USD/THB was firmer in the first part of trade, but after getting to highs of 31.81 we now sit back at 31.74, less than 0.10% weaker in baht terms. Focus remains on efforts to decouple THB from gold price moves.

- USD/SGD is back at 1.2815, down slightly for the session, which is line with the majors ticking up against the USD. This pair has been supported sub 1.2800 since the start of August.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 15/09/2025 | 0900/1100 | * | Trade Balance | |

| 15/09/2025 | 1130/1330 | ECB Schnabel At EIB Chief Econ Meeting | ||

| 15/09/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 15/09/2025 | 1230/0830 | ** | Wholesale Trade | |

| 15/09/2025 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 15/09/2025 | 1300/0900 | * | CREA Existing Home Sales | |

| 15/09/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 15/09/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 15/09/2025 | 1810/2010 | ECB Lagarde at Institut Montaigne Paris | ||

| 15/09/2025 | - | FOMC Meetings with S.E.P. | ||

| 16/09/2025 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 16/09/2025 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 16/09/2025 | 0600/0700 | *** | Labour Market - Payrolls & Claimants | |

| 16/09/2025 | 0600/0700 | *** | Labour Market - Payrolls & Claimants | |

| 16/09/2025 | 0800/1000 | *** | HICP (f) | |

| 16/09/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 16/09/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 16/09/2025 | 0900/1100 | ** | EZ Industrial Production | |

| 16/09/2025 | 1215/0815 | ** | CMHC Housing Starts | |

| 16/09/2025 | 1230/0830 | *** | CPI | |

| 16/09/2025 | 1230/0830 | *** | Retail Sales | |

| 16/09/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 16/09/2025 | 1230/0830 | *** | Retail Sales | |

| 16/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 16/09/2025 | 1315/0915 | *** | Industrial Production |