MNI EUROPEAN MARKETS ANALYSIS: Israel-Iran Truce Agreed

- Oil prices fell sharply following the announcement of a ceasefire between Iran and Israel early in the session. They have recovered somewhat during the day but remain down following Monday’s sharp drop. The end to the war is due at 0800 AEST Wed/2300 BST Tues/1800 EDT Tues.

- With fears of a broader Middle East conflict softening, risk markets rebounded today with the major equity bourses in the region leading the way with gains up +1.5%-+2.5%.

- The BBDXY has extended lower again in early Asian trading after President Trump's announcement of a ceasefire, BBDXY -0.30%. The price action overnight was very revealing and points to a market that is very quick to reinstate USD shorts with conviction high for a move lower.

MARKETS

US TSYS: Asia Wrap - Yields Edge Lower

The TYU5 range has been 111-06 to 111.10+ during the Asia-Pacific session. It last changed hands at 111-09+, down 0-05 from the previous close.

- The US 2-year yield has edged lower trading around 3.85%, down 0.01 from its close.

- The US 10-year yield has edged lower trading around 4.34%, down 0.01 from its close.

- (Bloomberg) -- “There's also the likelihood that bonds need to hear a dovish tone from Fed Chair Powell before they can make serious gains. Powell’s two days of Congressional testimony starts in the US session later today and he will be grilled about the potential for interest-rate cuts as soon as July”

- Bob Elliott on X: “A Broad Slowdown In US Hard Data. In recent weeks hard data across nearly every sector of the US economy has shown slowing, suggesting a broad-based weakness that is far from priced into current market expectations.”

- The 10-year yield attempted to break below its 4.30% support overnight, it failed on its first attempt but a sustained move back below there would likely see the move pick up momentum. 10-year yields would need to get back above 4.45/4.50% again to alleviate this downward pressure.

- Data/Events: Philadelphia Fed Non-Man Activity, Current Account Balance, FHFA House Price Index

JGBS: Little Changed, Mixed Results For 20Y Supply, BoJ SoO Tomorrow

JGB futures are weaker, down 10 ticks from settlement levels, but have retraced some of the earlier cheapening seen in the Tokyo afternoon session following the release of today’s 20-year auction results.

- The 20-year JGB auction delivered mixed results across key metrics. The low price underperformed dealer forecasts, according to a Bloomberg poll. However, the cover ratio increased to 3.1007x (highest since March) from 2.5007x in the previous auction, and the auction tail shortened dramatically to 0.28 from 1.14 – the longest since 1987.

- Cash US tsys are ~1bp richer in today's Asia-Pac session. Later today, Fed Chairman Powell gives the semi-annual policy testimony and is expected to be questioned on the unchanged stance. Also, the Fed’s Hammack, Williams, Kashkari, Collins and Barr speak. Today's US calendar: Philadelphia Fed Non-Man Activity, Current Account Balance, FHFA House Price Index.

- Cash JGBs are little changed across benchmarks out to the 10-year and 1bp richer beyond. The benchmark 20-year yield is 1.3bps lower at 2.346% after today's supply.

- Swap rates are flat to 1bp higher.

- Tomorrow, the local calendar will see PPI Services and Coincident/Leading Index data alongside BoJ Summary of Opinions (June MPM) and a speech from BoJ Board Tamura.

AUSSIE BONDS: Richer, Narrow Ranges, May CPI Tomorrow

ACGBs (YM +4.0 & XM +5.5) are trading stronger, but ranges have been relatively narrow on a data-light day.

- "Oil extended declines and US futures gained after Donald Trump said that Israel and Iran had agreed to a tentative ceasefire. Iran's foreign minister said no agreement has been made but that it would halt fighting if Israel stops." (BBG)

- Cash US tsys are ~1bp richer in today's Asia-Pac session. Today’s US calendar: Philadelphia Fed Non-Man Activity, Current Account Balance, FHFA House Price Index.

- Cash ACGBs are 4-6bps richer with the AU-US 10-year yield differential at -18bps.

- May CPI data is due tomorrow. Consensus expects it to ease to 2.3% y/y from 2.4%. Trimmed mean ticked up to 2.8% y/y in April and has been around 2.7-2.8% since December, suggesting a stalling in disinflation. The next RBA meeting is July 7-8.

- The bills strip is flat to +4, with late whites/early reds outperforming.

- RBA-dated OIS pricing is slightly softer across meetings today. A 25bp rate cut in July is given an 85% probability, with a cumulative 76bps of easing priced by year-end.

- The AOFM plans to sell A$1000mn of the 3.50% 21 December 2034 bond tomorrow.

BONDS: NZGBS: Closed Richer But Off Bests After A Data-Light Session

After a data-light session, NZGBs closed marginally off session bests, 3-4bps richer.

- Nevertheless, NZGBs underperformed their $-bloc counterparts, with the NZ-US and NZ-AU 10-year yield differentials closing 2-3bps wider.

- Cash US tsys are ~1bp richer in today's Asia-Pac session.

- (Bloomberg) -- ANZ Bank now sees New Zealand house prices rising 2.5% in 2025, less than the previous projection of 4.5%. Sales volumes have stabilised around their long-run average, but rising demand has been met with an ample supply of new listings. Indicators of the balance between housing supply and demand continue to drift sideways, leading to a forecast downgrade.

- Production collected for processing in May was 104.1m kg milk solids, up 8% y/y.

- Swap rates closed 4-5bps lower, with the 2s10s curve flatter.

- RBNZ dated OIS pricing closed flat to 4bps softer across meetings, with the 2026 meeting leading. 4bps of easing is priced for July, with a cumulative 30bps by November 2025.

- Tomorrow, the local calendar will see trade balance data for May.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 3.00% Apr-29 bond, NZ$175mn of the 4.50% May-35 bond and NZ$50mn of the 1.75% May-41 bond.

FOREX: Asia FX Wrap - Market Very Quick To Resell The USD

The BBDXY has had a range of 1203.92 - 1207.36 in the Asia-Pac session, it is currently trading around 1204. The BBDXY has extended lower again in early Asian trading after President Trump's announcement of a ceasefire, BBDXY -0.30%. The price action overnight was very revealing and points to a market that is very quick to reinstate USD shorts with conviction high for a move lower. (Bloomberg) - The PBOC set the strongest yuan fixing since November, but it also signaled a reluctance to allow strong gains. The fixing also came in slightly above the estimate for the first time since June 13. This adds to the view that China is acceding to a sustained, gradual appreciation in its currency, as well as emphasizing the broader theme of USD weakness.”

- EUR/USD - Asian range 1.1575 - 1.1610, Asia is currently trading 1.1605. EUR support back towards 1.1450 proved solid once more and the swift turnaround in the USD has seen the EUR going into the London session above 1.1600. While the USD remains on the back foot the EUR will continue to find demand on dips.

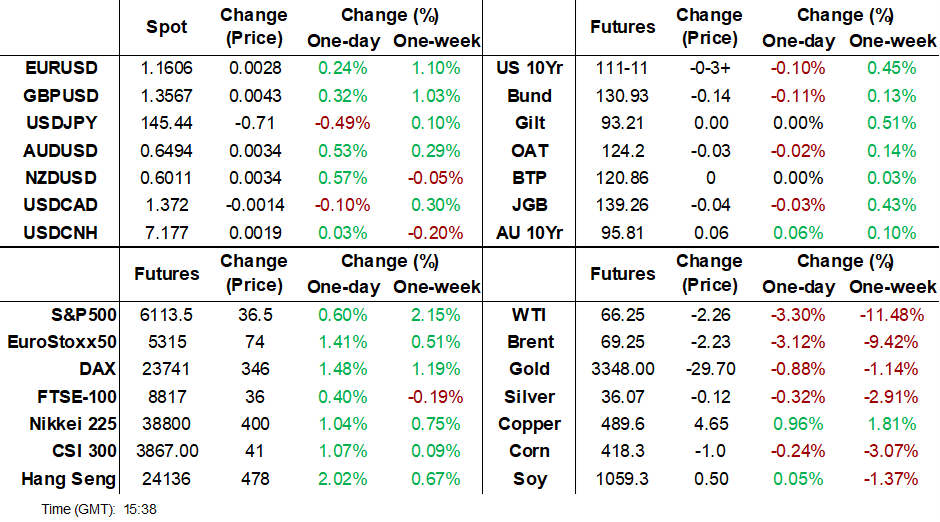

- GBP/USD - Asian range 1.3506 - 1.3566, Asia is currently dealing around 1.3560. The GBP again found solid demand around its 1.3400 support and is now back to testing its previous highs back towards 1.3600 looking for the momentum to carry it through its weekly pivot.

- USD/CNH - Asian range 7.1704 - 7.1797, the USD/CNY fix printed 7.1656. Asia is currently dealing around 7.1780. Sellers should be around on bounces while price holds below the 7.2500 area and the PBOC manages the fix lower.

- Cross asset : SPX +0.55%, Gold $3350, US 10-Year 4.34%, BBDXY 1204, Crude oil $66.65

- Data/Events : Ger IFO

Fig 1: GBP/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: Asia Wrap - USD/JPY Follows The Move Lower In Oil

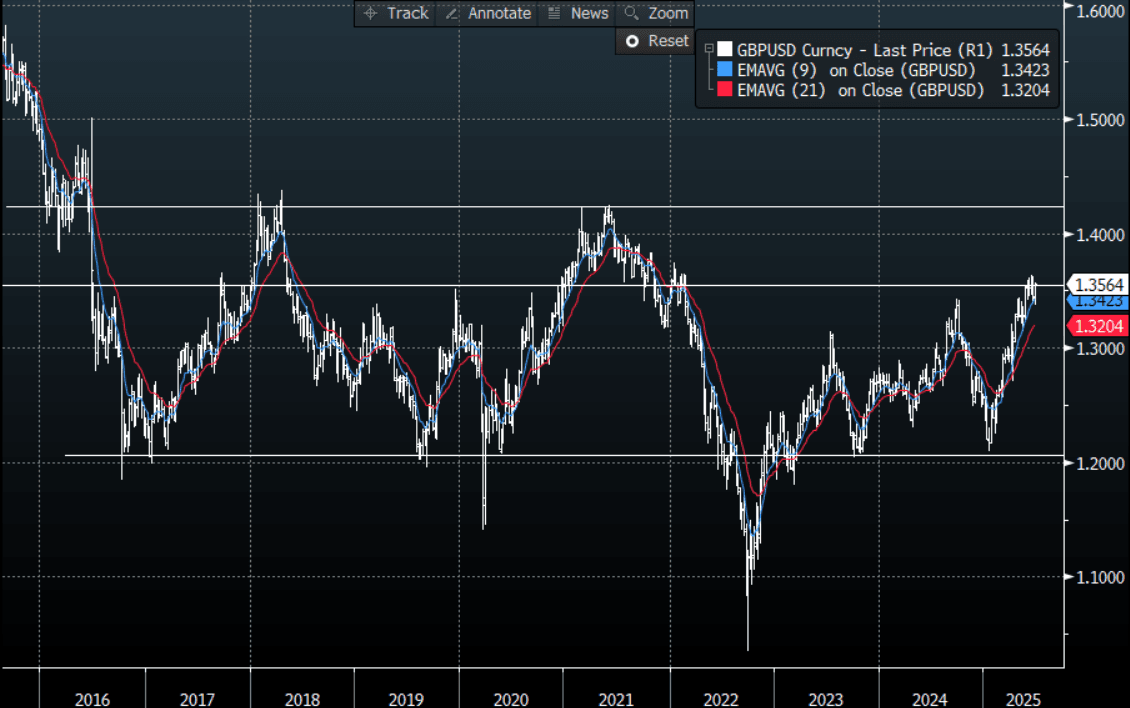

The Asia-Pac USD/JPY range has been 145.30 - 146.15, Asia is currently trading around 145.45, -0.50%. USD/JPY continues to extend lower in Asia as it follows the capitulation in oil longs, which have reacted to the announcement of a ceasefire in the Middle East. The market is very quick to re-instate its USD shorts.

- (Bloomberg) -- The Bank of Japan shrank its balance sheet by 2.3% to 716.1 trillion yen in the past 10 days.

- Mixed Demand Metrics For 20Y Auction: Overall though today's result is likely to be seen as better than the performance observed in the 30-year JGB auction earlier this month.

- "AKAZAWA: STILL WORKING ON TIMING FOR NEXT ROUND OF TRADE TALKS" - BBG

- There would have been some paring back of JPY longs on the break above 147.00 overnight but the reversal from above 148.00 shows how quickly the market is to reinstate these positions.

- An ugly daily shadow points to a potential top being in place now, first support back towards 144.50/145.00.

- Price now back in a wider 142.00 - 148.00 range, I am not sure that the brief spike higher would have seen positioning altered too much and the long JPY trade is still alive and well.

- Options : Close significant option expiries for NY cut, based on DTCC data: 145.00($582m).Upcoming Close Strikes : 144.50($1.34b June 25), 143.00($1.41b June 26)

- CFTC data shows Asset managers maintained their already extensive JPY longs, while leveraged funds have pared back their own longs that had just begun to be rebuilt.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia Wrap - AUD/USD Extends Gains, Eyes 0.6550

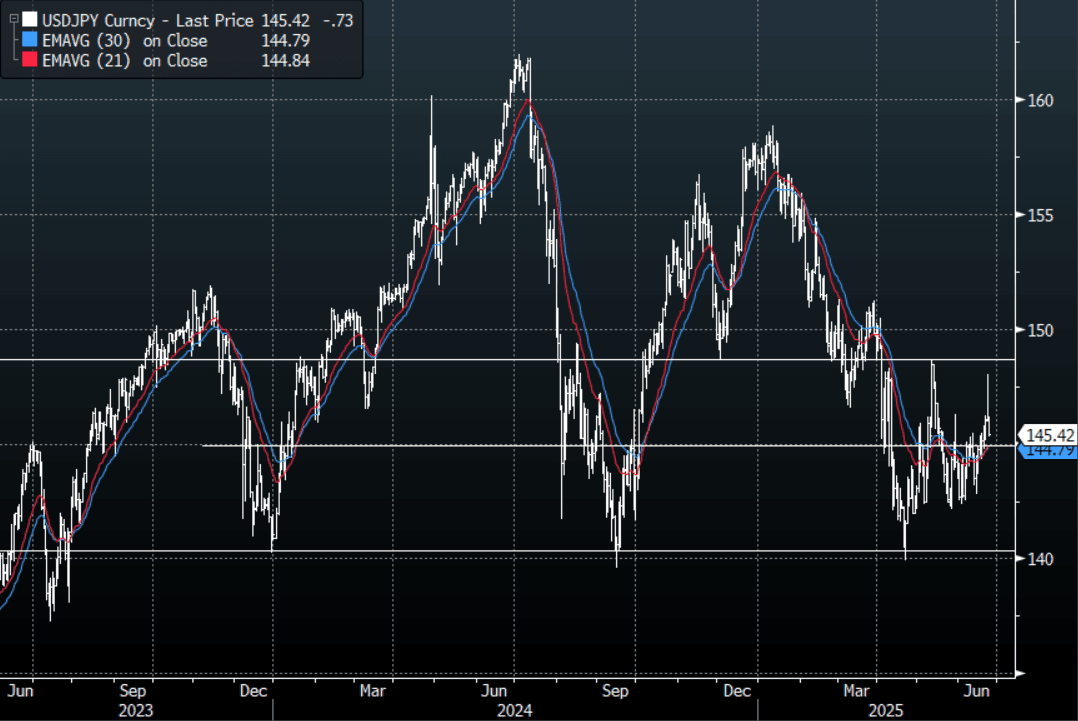

The AUD/USD has had a range of 0.6454 - 0.6497 in the Asia- Pac session, it is currently trading around 0.6490. The AUD has remained better bid throughout the Asian session, +0.45%. The market is shrugging off headlines of explosions and missiles still heading in either direction and focusing wholly on the ceasefire announced by President Trump. The market was very quick to re-sell USD’s across the board and now the AUD is back within striking distance of 0.6550 again.

- "TRUMP SPOKE DIRECTLY WITH NETANYAHU ON CEASEFIRE AGREEMENT, TRUMP THANKS QATAR EMIR FOR HELPING BROKER ISRAEL-IRAN TRUCE"

- “Oil extended declines and US futures gained after Donald Trump said that Israel and Iran had agreed to a tentative ceasefire. Iran’s foreign minister said no agreement has been made but that it would halt fighting if Israel stops.”(BBG)

- From looking vulnerable and on the verge of a collapse, down around 1.2% at one point then ending positive on the day is quite the feat.

- The AUD/USD bounced hard off its support and is now back to potentially testing the top end of its range.

- Price remains in the wider 0.6350 - 0.6550 range for now. After failing to break lower and risk looking like it can extend higher can the AUD have another go trying to break above the 0.6550 area ?

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6500(AUD1.41b June 26), 0.6450(AUD553m June 26).

- CFTC Data shows Asset managers maintaining their shorts, the Leveraged community though again added to their shorts.

- AUD/JPY - Today's range 94.26 - 94.56, it is trading currently around 94.35. Choppy price action as the pair establishes a range between 92.00 - 96.00. Should risk build on this move, focus could turn back to the 96.00 area.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

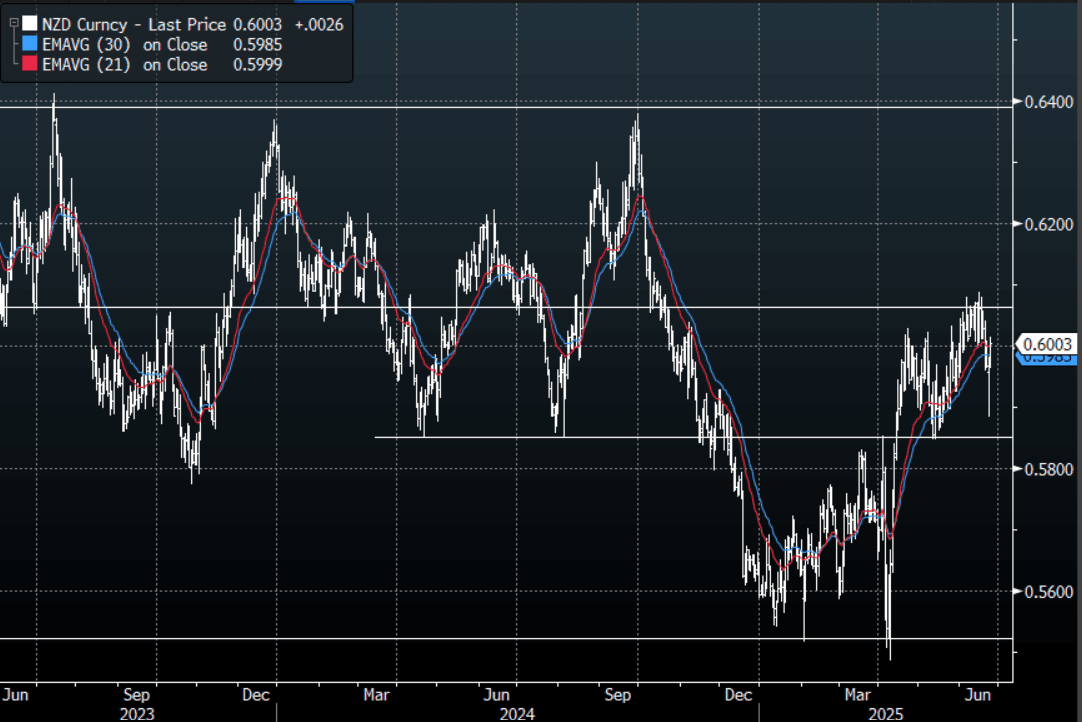

NZD: Asia Wrap - NZD Back Above 0.6000

The NZD/USD had a range of 0.5963 - 0.6014 in the Asia-Pac session, going into the London open trading around 0.6005. The NZD has remained well supported all through the Asian session, +0.50%. With the USD back under pressure the NZD very quickly finds itself back on a 0.6000 handle, looking to build momentum for a test of the 0.6100 area.

- "NZ TREASURY: MAINTAINING ECONOMY MOMENTUM MAY BE CHALLENGING" - BBG

- “Among Group-of-10 commodity currencies, the Kiwi “is the only energy importer and most vulnerable if Middle East oil supply is impacted more severely,” wrote Bank of America.”

- A huge bounce from sub 0.5900 and we are again breaking back above the 0.6000 area this morning.

- Technically while the support around 0.5850 holds in NZD/USD it is still in an uptrend, this held perfectly overnight and should risk build on from this then focus will turn once gain back to 0.6050/0.6100.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5690(NZD621m June 25)

- CFTC Data showed Asset managers paring back their shorts slightly once more over the week, the leverage community did likewise.

- AUD/NZD range for the session has been 1.0798 - 1.0817, currently trading 1.0805. The cross is struggling to get any momentum back above 1.0800 for now, it needs to hold above here and start extending higher to put a higher low in place. The longer it fails to extend the higher the chances it begins to drift lower again, a break sub 1.0750 will see downward momentum return.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Major Bourses Lead Stocks Higher

With fears of a broader Middle East conflict softening, risk markets rebounded today with the major equity bourses in the region leading the way with gains up +1.5%-+2.5%.

- In China, the Hang Seng led the way rising +1.95% today for its biggest one day gain this month. The CSI 300 followed it higher, rising by +1.09% whilst the Shanghai Comp rose +1.00% and the Shenzhen Comp up +1.53%.

- The TAIEX in Taiwan is very strong, gaining +1.9%.

- Korea's KOSP was a standout today rising +2.6% for its strongest gain in three weeks and more than erasing yesterday's losses.

- The FTSE Malay KLCI hardly moved today, and didn't join in the rally falling just -0.02%

- The Jakarta Composite was strong rising +1.18%

- The FTSE Straits Times in Singapore is up +0.49% whilst the PSEi in the Philippines is up +1.49%

- The NIFTY 50 is up +0.94% in morning trade following yesterday's loss of -0.56%

OIL: Crude Risk Premium Unwinding As Focus Returns To Fundamentals

Oil prices fell sharply following the announcement of a ceasefire between Iran and Israel early in the session. They have recovered somewhat during the day but remain down following Monday’s sharp drop. The end to the war is due at 0800 AEST Wed/2300 BST Tues/1800 EDT Tues. Iran’s military action was due to stop at 0500 BST and Israel’s at 1100 BST. US President Trump has warned that the truce shouldn’t be violated.

- WTI is down 3.2% to $66.34/bbl to be 10.1% lower this week. It fell to $64.38 early in the session, just below support at $64.51, 50-day EMA. Brent is -2.8% to $69.48/bbl off today’s trough of $68.23, above the 50-day EMA at $67.99. The USD index is down 0.3%.

- The Iran-Israel conflict worried markets that supply could be severely impacted especially if Israel attacked Iranian oil infrastructure or Iran disrupted shipping in the Strait of Hormuz. Despite the ceasefire being in its early hours, markets seem reassured and oil’s geopolitical risk premium is unwinding.

- Attention is now likely to return to demand and supply issues stemming from trade disputes and OPEC output normalisation – they hold their next meeting on July 6 to decide August output. A market surplus is generally expected this year and next. US industry-based inventory data is out today.

- Later Fed Chairman Powell gives the semi-annual policy testimony and is expected to be questioned on the unchanged stance. Also the Fed’s Hammack, Williams, Kashkari, Collins and Barr speak. ECB President Lagarde appears as well as de Guindos and Lane.

- In terms of data, US June Philly non-manufacturing, Q1 current account, April house prices, June consumer confidence & Richmond Fed business sentiment are released. Germany’s June Ifo survey and Canada’s May CPI also print.

GOLD: Bullion Falls As Risk Sentiment Improves

Gold prices fell to $3333.34/oz following US President Trump’s announcement of a ceasefire followed by an end to the Iran-Israel war as geopolitical risks eased. They are currently down 0.6% to $3349.2 and off the low, which briefly pierced initial support at $3338.8.

- The end to the war in due at 0800 AEST Wed/2300 BST Tues/1800 EDT Tues. Iran’s military action was due to stop at 0500 BST but Israel reported more missiles at 0515 BST.

- With stronger risk sentiment dominating today, gold is not finding support from the weaker US dollar and lower US yields. The BBDXY USD is down 0.3%.

- Equities have rallied with the S&P e-mini up 0.6% and Hang Seng +2%. Oil prices are down with WTI -2.8% to $66.56/bbl as the geopolitical risk premium unwinds. Copper is 0.9% higher.

- Silver has trended higher and is currently up 0.2% at $36.16 off the intraday low of $35.61 reached early in the session. It is now down 0.4% over the last week but technicals suggest this is corrective and a bull wave remains in play. Initial support is at $35.49 and resistance at $37.32.

- Later Fed Chairman Powell gives the semi-annual policy testimony and is expected to be questioned on the unchanged stance. Also the Fed’s Hammack, Williams, Kashkari, Collins and Barr speak. ECB President Lagarde appears as well as de Guindos and Lane.

- In terms of data, US June Philly non-manufacturing, Q1 current account, April house prices, June consumer confidence & Richmond Fed business sentiment are released. Germany’s June Ifo survey and Canada’s May CPI also print.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 24/06/2025 | 0800/1000 | *** | IFO Business Climate Index | |

| 24/06/2025 | 0800/0900 | BOE Bailey At Gold Standard Conference | ||

| 24/06/2025 | 0845/1045 | 2025 Budget Press Conference | ||

| 24/06/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 24/06/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 24/06/2025 | 0930/1030 | BOE Green On CB Balance Sheet Mgmt | ||

| 24/06/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 24/06/2025 | 1115/1315 | ECB de Guindos At XLII APIE seminar | ||

| 24/06/2025 | 1230/0830 | *** | CPI | |

| 24/06/2025 | 1230/0830 | * | Current Account Balance | |

| 24/06/2025 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 24/06/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 24/06/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 24/06/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 24/06/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 24/06/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 24/06/2025 | 1300/1500 | ECB Lagarde Accepts De Sanctis Award "Europa" | ||

| 24/06/2025 | 1315/0915 | Cleveland Fed's Beth Hammack | ||

| 24/06/2025 | 1335/1435 | BOE Ramsden At Barclays-CEPR MonPol Forum | ||

| 24/06/2025 | 1355/1555 | ECB Lane Keynote At Barclays-CEPR MonPol Forum | ||

| 24/06/2025 | 1400/1000 | *** | Conference Board Consumer Confidence | |

| 24/06/2025 | 1400/1000 | ** | Richmond Fed Survey | |

| 24/06/2025 | 1400/1000 | Fed Chair Jay Powell | ||

| 24/06/2025 | 1400/1500 | BOE Bailey At Lords Econ Affairs Committee | ||

| 24/06/2025 | 1540/1640 | BOE Pill At Gold Standard Conference | ||

| 24/06/2025 | 1550/1650 | BOE Breeden At UK Finance Digital Innovation Summit | ||

| 24/06/2025 | 1630/1230 | New York Fed's John Williams | ||

| 24/06/2025 | 1700/1300 | * | US Treasury Auction Result for 2 Year Note | |

| 24/06/2025 | 1805/1405 | Boston Fed's Susan Collins | ||

| 24/06/2025 | 2000/1600 | Fed Governor Michael Barr | ||

| 25/06/2025 | 2301/0001 | * | Brightmine pay deals for whole economy | |

| 24/06/2025 | 0015/2015 | Kansas City Fed's Jeff Schmid | ||

| 25/06/2025 | 0130/1130 | *** | CPI Inflation Monthly | |

| 25/06/2025 | 0600/1400 | ** | MNI China Money Market Index (MMI) | |

| 25/06/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 25/06/2025 | 0700/0900 | ** | PPI | |

| 25/06/2025 | 0700/0900 | *** | GDP (f) | |

| 25/06/2025 | 0845/0945 | BOE Lombardelli At BOE MonPol Conference | ||

| 25/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 25/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 25/06/2025 | 0900/1000 | BOE Pill On Panel At BOE MonPol Conference | ||

| 25/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 25/06/2025 | 1230/1330 | BOE Lombardelli Chairs Riksbank's Breman Speech At BOE MonPol Conf |