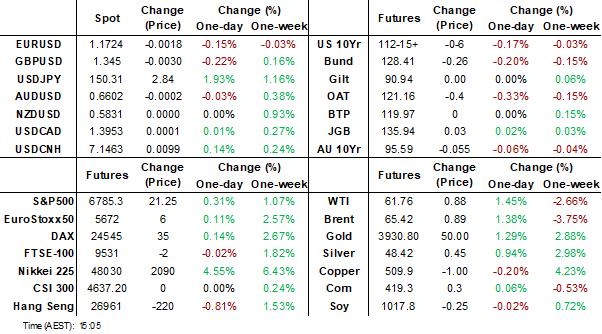

MNI EUROPEAN MARKETS ANALYSIS: Gold Bull Trend Continues

- Japan markets have moved notably today, following the surprise LDP election win from Sanae Takaichi over the weekend (odds of her victory were very low on Friday). USD/JPY has surged through 150.00, as BoJ hiking odds have fallen (Takaichi has been a critic of BoJ hikes in the past). The JGB yield curve is steeper, but local equities have surged.

- The data calendar has been very light with China and South Korea still out, while most of Australia was also out today.

- Gold has surged to fresh record highs, while oil is also up post the weekend OPEC+ meeting.

- The Fed’s Schmid speaks later on the economy and monetary policy, and also the ECB’s Lagarde, Lane and de Guindos appear. August euro area retail sales print.

MARKETS

US TSYS: Futures Lower, 10yr Might See Buyers Re-engage Around 4.20%

US Tsy futures hold weaker across the board 10yr last at 112-16+, -05. We remain above the 50-day EMA support point (112-12+) for 10yr futures, which will be watch on any further extension lower. The Sep move through this support zone proved to be a false break. The US Tsy cash curve has had a steepening bias, +56.5bps last. Spill over from a sharp steepening in the cash JGB curve (after Takaichi surprised and won the LDP leadership battle).

- Outside of government shutdown news, with seemingly little progress made over the weekend, focus will remain on what can be gleaned from private sector surveys/economy wide anecdotes. Focus later today may be on Trump administration government job lay offs.

- For US 10yr outright, we remain within recent ranges, last 4.14%, with broader 4.00-4.10% ranges holding. Buyers might re-emerge on any move back toward 4.20%, given on-going signs around labour market softness (with the Fed's Jefferson highlighting on Friday the jobs market is softening across a range of indicators) and how the Fed composition may change as we progress through 2026. Still, with elevated inflation pressures it is unlikely to be a sharp break lower on the downside, rather a steady grind.

- Looking ahead, there is no data scheduled or Fed speakers for Monday. Tuesday's Trade Balance & Import/Export data suspended due to the Gov shutdown. US Treasury supply kicks off Monday with $84B 13W & $75B 26W bill auctions (1130ET).

JGBS: Curves Steeper, But Sub Recent Highs, 30yr Debt Auction Tomorrow

All the action today has away from the 10yr JGB, which has been fairly steady, last near 1.67%. The front end is weaker, back end firmer in yield terms as markets have moved to price in less BoJ hike risks, as well greater fiscal uncertainty. The 2/10s curve was last +76.5bps, +4.5bps for the session, while the 2/30s was +239bps, up 17bps.

- We noted earlier after the initial adjustment to Takaichi's victory, sentiment may stabilize and await cabinet announcements and early policy outcomes before taking the curve to fresh highs. The early Sep high for 2/30s was +245bps. The 30yr outright was last 3.30%, the 40yr 3.53%, while the 2yr was near 0.91%.

- These moves have largely been mirrored in the swap space, although yield moves haven't been as large at the back end (with JGBs likely more susceptible to fiscal policy concerns).

- BoJ tightening risk has fallen dramatically for Oct, with just 6bps of tightening priced in against recent highs of 17bps, as Takaichi stated the government and BoJ should be coordinated on economic policy. Takaichi has been a critic of BoJ hikes in the past (but her rhetoric wasn't as strong during this most recent LDP leadership campaign).

- JGB futures are back to flat, last 135.93, +.02, but well off earlier highs of 136.53.

- Note tomorrow, we get on the data front, Aug Household spending prints. Greater focus will be on 30yr dent auction, the first test for the new Takaichi regime.

BONDS: All Eyes On RBNZ On Wednesday, Mkt Close To Split On 25 or 50bps Cut

NZGB yields have shown a steepening bias as Monday's session has unfolded, consistent with US and JGB moves. The 2/10s curve was last +150bps, close to fresh highs since April of this year. Local news flows has been light, with all eyes on the RBNZ outcome this Wednesday. While it is widely expected to cut rates further, economists are split between a 25bp and 50bp move. 10 out of the 25 analysts surveyed by Bloomberg are forecasting the larger reduction. The announcement won’t be accompanied by updated forecasts or a press conference (they are scheduled for November), but post-meeting speaking events should be announced this week.

- The 2yr swap rate is holding under 2.50%, so near recent cycle lows. A more dovish RBNZ this week is likely to see the market target a move into the 2.00-2.25% region. Moves back towards 2.75% may be faded on any hawkish surprise. The bias around 2yr swap still appears skewed lower until NZ growth is on a firmer footing. Market pricing per OIS RBNZ dated contracts show an implied rate of 2.67% for Wednesday's meeting, versus the current policy rate of 3.00% (so around 131% of a 25bps moved priced in), whilst the terminal rate into 2026 sits close to 2.25%, which is where we have been close to in recent weeks.

- The 2yr government bond yield was last around 2.72%, little changed today, while the 10yr is back above 4.22%, +2bps firmer. Both benchmarks remain within recent ranges.

NEW ZEALAND: RBNZ Forecast To Cut But By How Much?

The focus of the week is firmly on Wednesday’s RBNZ decision. While it is widely expected to cut rates further, economists are split between a 25bp and 50bp move. 10 out of the 25 analysts surveyed by Bloomberg are forecasting the larger reduction. The announcement won’t be accompanied by updated forecasts or a press conference (they are scheduled for November), but post-meeting speaking events should be announced this week.

- In terms of data, the key Q3 Quarterly Survey of Business Opinion (QSBO) is released on Tuesday. It should give an indication of how weak the recovery is and as a result possibly impact the size of rate cut projections ahead of Wednesday’s RBNZ decision.

- In terms of surveys, there is also BusinessNZ’s PMI for September. It showed manufacturing stagnating in August with the PMI at 49.9 but the Q3 average was 51.3 up from Q2’s 50.0. While August output and employment were below the breakeven 50-level, forward-looking new orders rose to 55.2, the highest since March 2022.

AUSTRALIA: RBA’s Bullock Before Senate On Friday, Consumer Sentiment Tuesday

In a quiet week RBA Governor Bullock’s appearance before the Senate Economics Committee on Friday and Westpac October consumer confidence on Tuesday will be the highlights.

- RBA Governor Bullock and Assistant Governor Kent will answer questions from the Senate Economics Committee for the supplementary 2025-2026 budget at 0900 AEDT on Friday. Bullock appeared before the lower house before the 30 September decision to hold rates and so the decision as well as its inflation concerns are likely to be examined.

- Tuesday’s October Westpac consumer sentiment survey would have been taken during the week of the 30 September RBA decision and given rates were unchanged, the pre- and post-meeting breakdown will be of interest. Confidence fell 3.1% to 95.4 in September as economic and unemployment expectations deteriorated.

- ANZ September job ads also print on Tuesday. The series appears to have stabilised with it rising 1.75% y/y in August, the fastest since January 2023.

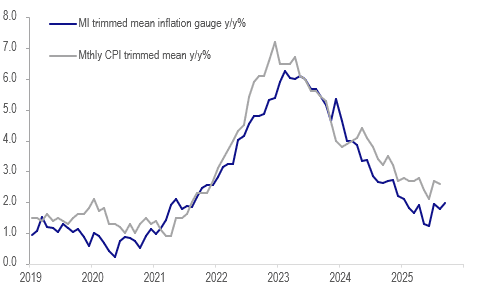

- Melbourne Institute inflation expectations for October are released on Thursday. Q3 was in line with Q2 at 4.4%. Any breaks below 4% have been short-lived. On Monday, MI’s September inflation gauge for both headline and trimmed mean rose 0.2pp, another sign of stalling disinflation.

AUSTRALIA DATA: Data Continue To Signal Stall In Disinflation

The Melbourne Institute’s inflation gauge for September picked up 0.2pp to 3.0% with Q3 averaging 2.9% up slightly from Q2’s 2.8%. It also has a trimmed mean measure which also rose 0.2pp to 2% in September to be 1.9% in Q3 up from Q2’s 1.5% and may be trending higher again. Monthly CPI inflation is also higher over Q3 and RBA Governor Bullock sounded cautious last week as the central bank is concerned that there are signs a few key components are rising, especially market services which have also been sticky overseas. The key quarterly CPI data are released 29 October and are likely to determine the outcome of the 4 November RBA meeting.

Australia trimmed mean inflation y/y%

FOREX: USD/JPY Testing Above 150.00, Options Volumes See 151-155.00 Strikes

Yen weakness has been the standout today, with USD/JPY breaking above 150.0, off 1.75% so far today for the session. The surprise Takaichi election win from Saturday's LDP leadership race has driven sentiment (with market odds of her victory very low on Friday per Polymarket). BoJ tightening risk has fallen dramatically for Oct just 6bps of tightening priced in against recent highs of 17bps), with Takaichi stating the government and BoJ should be coordinated on economic policy. Takaichi has been a critic of BoJ hikes in the past (but her rhetoric wasn't as strong during this most recent LDP leadership campaign).

- For USD/JPY technicals, a clean break above 150.00, will see focus shift to 150.92, the Aug 1 high and key resistance.

- Positioning focus will rest with asset managers and whether they go back a short position (with leveraged contracts already net short). Asset managers were last net long to the tune of +79.3k.

- The 1 month risk reversal is highs last -0.30, fresh highs back to 2022. So far today we have seen close to $7.4bn in options volumes go through in USD/JPY (63% of total volumes per DTCC on BBG). The larger volume transactions have been skewed towards USD/JPY calls with strikes in 151-155.00 region.

- USD/JPY looks too high relative to US-JP rate differentials, but further position adjustments could still play out in the near term.

- Elsewhere, EUR/USD is back slightly lower at 1.1720/25, with French politics likely to come back into focus.

- The kiwi has outperformed the G10 today with NZDUSD up 0.1% to 0.5836, close to the intraday high at 0.5840, helped by stronger US equity futures even though the NZX was lower.

- AUDUSD fell to 0.6582 in early trading as USDJPY rose following news that Japan’s conservative Takaichi won the LDP leadership. The pair has recovered to be up 0.1% to 0.6609, close to the intraday high of 0.6612, aided by better risk appetite with equities generally stronger. The USD index is 0.3% higher. BBDXY last near 1204.25.

ASIA STOCKS: Japan Stocks To Fresh Record High On Takaichi Victory

Japan stocks have surged in the aftermath of Takaichi winning the LDP leadership battle. The combination of Takaichi's pro growth/dovish BoJ backdrop has seen local bourses post sharp gains. The NKY 225 is up 4.5%, while the Topix has gained nearly 2.9%. Elsewhere US equity futures have ticked higher but remain just short of recent highs. The US government shutdown drags on, while Monday focus may rest with the Trump administrations government job cut announcements (reportedly expected to be in the thousands). China and South Korean markets remain closed. Much of Australia is also out, although the ASX200 is still trading (down modestly).

- Japan indices, now at fresh record highs, have been aided by the weaker yen trend (we are approaching the 150.00 level), with the Topix transport gaining 2.8%. The bank sub index has lagged though, as BoJ hiking expectations have been pared, this sub index down 2.5%. Fiscal concerns under the new Takaichi regime are yet to impact broader sentiment (although the potential for pro growth from higher government borrowing/spending is a market positive). Also note offshore investors have mostly been net sellers in recent week of local stocks, so they may be coming back into the market as we break higher.

- Elsewhere Hong Long markets are weaker, but this follows a strong run higher recently. The HSI off around 0.75%.

- In South East Asia, Philippines losses have been evident. The PCOMP down a further 0.80% at the time of writing. We are still above recent lows (sub 6000), but earlier headlines from the Stock Exchange CEO noted the challenges facing the market amid near term political instability/corruption probes. (via BBG). Offshore investors have been net sellers of local stocks so far in Oct.

OIL: Crude Relief Rally After Restrained OPEC Output Decision

Oil prices are higher during Monday’s APAC session after falling sharply last week. The move higher appears to be a relief rally following OPEC’s decision to increase November’s output 137kbd in line with October’s rise. There had been fears that it could have been substantially higher as the IEA is forecasting a record market surplus in 2026. WTI is up 1.6% to $61.85/bbl, close to the intraday high, and Brent is 1.5% higher at $65.48, after reaching $65.52. The USD index is up 0.3%.

- According to Bloomberg there were some dissenting views with Russia arguing that prices needed to be supported and Algeria that demand could weaken but Saudi arguing for a larger target increase.

- The group is trying to regain market share but most members have limited spare capacity except Saudi Arabia, and so the impact of output decisions on physical supply is unclear.

- The Fed’s Schmid speaks later on the economy and monetary policy, and also the ECB’s Lagarde, Lane and de Guindos appear. August euro area retail sales print.

Gold Makes Another New High On Elevated US Uncertainty

Gold has traded above round-number resistance at $3900/oz for most of Monday’s APAC session and has also broken above resistance at $3909.4, a Fibonacci projection. Today’s rally has resulted in another record high being reached at $3926.61. Bullion is currently 1.0% higher at $3926.3 helped by the ongoing US government shutdown with no near-term resolution apparent and the uncertainty it creates around the economy. This is outweighing the stronger US dollar (BBDXY +0.3%) and unchanged yields.

- Gold has benefited from safe-haven flows from the government shutdown as it not only weighs on US activity but also delays key data releases. Both are likely to make monetary policy decisions difficult as the outlook is even less clear. The market has almost 50bp of easing priced in by end 2025. Another senate vote to resolve the impasse will be held Monday.

- The prospect of further US rate cuts as well as uncertainty around the government shutdown and Fed independence mean that gold continues to make new highs and approach $4000/oz.

- Silver is up 01.0% to $48.47 after a high of $48.38, above resistance at 48.232. It fell to $47.962 early in the session.

- The S&P e-mini is up 0.3% and Nikkei +4.5% but ASX down 0.2%. A number of Asian markets are closed today. Oil prices are higher with WTI +1.5% to $61.81/bbl. Copper is down 0.3%.

- The Fed’s Schmid speaks later on the economy and monetary policy, and also the ECB’s Lagarde, Lane and de Guindos appear. August euro area retail sales print.

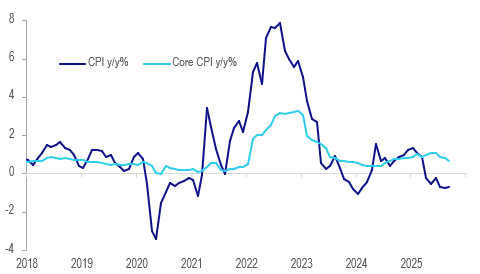

THAILAND: Rate Cut Likely On Weak Growth & Disappointing September CPI

September Thai inflation was lower than expected with headline printing at -0.7% y/y after -0.8% and core at +0.65% y/y following August’s +0.8%. The Bank of Thailand decision is announced Wednesday, the first with new pro-growth Governor Vitai, and it is widely forecast to cut rates 25bp to 1.25%. The soft September CPI print along with lacklustre growth reinforces those expectations.

- Core inflation was its lowest in just over a year despite 100bp of easing begun in October 2024 as domestic growth remains weak. Government energy subsidies and lower food prices from good harvests pushed headline into negative territory where it has been for six straight months.

- Consumer data have generally been soft with August with consumer confidence falling to its lowest since December 2022, July private consumption down 0.3% y/y and August tourist arrivals contracting 12.8% y/y. Q2 real consumption growth slowed to 2.1% y/y from 2.5%. Recent political instability has been unhelpful but the new government is looking at ways to support households although it has also promised new elections.

- There was downward pressure on core inflation from clothing, housing, and personal & medical care.

Thailand CPI y/y%

Source: MNI - Market News/LSEG

ASIA FX: USD/Asia Higher, Spill Over Evident From Weaker Yen

The bias has been for higher USD/Asia pairs, with spill over from the spike in USD/JPY levels in play. China and South Korean markets remain out until the second half of the week, which will be limiting liquidity and interest in these markets. USD/CNH spot was last above 7.1400 (off around 0.10%, versus yen's 1.85% fall), while the 1 month USD/KRW NDF had risen to above 1409/10, around 0.30% weaker than end NY closing levels. We are just short of recent highs for the 1 month contract.

- The JPY/KRW cross (based off the 1 month NDF level) is back to 9.4100, sharply down from earlier Oct highs above 9.5300. Dips in this cross have mostly been supported back toward 9.3500 since early Aug.

- Spot USD/KRW and USD/JPY have an historical correlation of around 45% (last 12 months), second highest in the region after USD/SGD, USD/JPY correlation (66%). USD/SGD was last around 1.2925 up 0.30%, short of end Sep highs around 1.2950. The MAS policy meeting outcome is due soon (BBG has the release window from now until the 14th of Oct, which is next Tuesday)

- Elsewhere, USD/THB is off earlier highs the pair last around 32.35 (down 0.10% for the session). September Thai inflation was lower than expected with headline printing at -0.7% y/y after -0.8% and core at +0.65% y/y following August’s +0.8%. The Bank of Thailand decision is announced Wednesday, the first with new pro-growth Governor Vitai, and it is widely forecast to cut rates 25bp to 1.25%.

- USD/PHP is back above 58.00 off around 0.40%, with Philippines stocks down close to 1%. We are still above recent lows (sub 6000), but earlier headlines from the Stock Exchange CEO noted the challenges facing the market amid near term political instability/corruption probes. (via BBG). USD/IDR has crept above 16610, down 0.20% om IDR terms.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 06/10/2025 | 0700/0900 | ** | Industrial Production | |

| 06/10/2025 | 0700/0900 | ** | Unemployment | |

| 06/10/2025 | 0715/0915 | ECB de Guindos Speech at Diario Expansion | ||

| 06/10/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 06/10/2025 | 0730/0930 | *** | HCOB France Construction PMI | |

| 06/10/2025 | 0800/1000 | ECB Lane Keynote at ECB MonPol Conference | ||

| 06/10/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 06/10/2025 | 0900/1100 | ** | EZ Retail Sales | |

| 06/10/2025 | 1500/1600 | BOE Bailey Keynote at Scotland Global Investment Summit | ||

| 06/10/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 06/10/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 06/10/2025 | 1700/1900 | ECB Lagarde at ECON Hearing, European Parliament | ||

| 06/10/2025 | 2100/1700 | Kansas City Fed's Jeff Schmid | ||

| 07/10/2025 | 2330/0830 | ** | Household spending | |

| 07/10/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 07/10/2025 | 0645/0845 | * | Foreign Trade | |

| 07/10/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 07/10/2025 | 1230/0830 | ** | Trade Balance | |

| 07/10/2025 | 1230/0830 | ** | Trade Balance | |

| 07/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index |