MNI EUROPEAN MARKETS ANALYSIS: Fed In Focus Later

- Broader USD moves and US Tsy yields have been modest so far today, as the market awaits the FOMC later. JGB futures are stronger, +9 compared to the settlement levels, after today’s 20-year auction.

- On the data front, the Westpac Leading index in Australia signaled slowing growth. In NZ, there was a sharp narrowing in the Q2 YTD current account deficit as a share of GDP with it printing at 3.7% after 4.2% and the peak in Q4 2022 of 9%.

- Later the focus is on the Fed (see MNI Fed Preview) but there are also August US housing starts/permits, August UK/euro area CPIs and the Bank of Canada decision (forecast to cut 25bp). In addition to Powell and BoC Governor Macklem, ECB President Lagarde and Board member Cipollone also speak today.

MARKETS

US TSYS: Quiet Session, Looking Toward FOMC

The TYZ5 range has been 113-15 to 113-18+ during the Asia-Pacific session. It last changed hands at 113-17+, down 0-00+ from the previous close.

- The US 2-year yield is trading 3.503%.

- The US 10-year yield has edged lower trading around 4.022%, down 0.01 from its close.

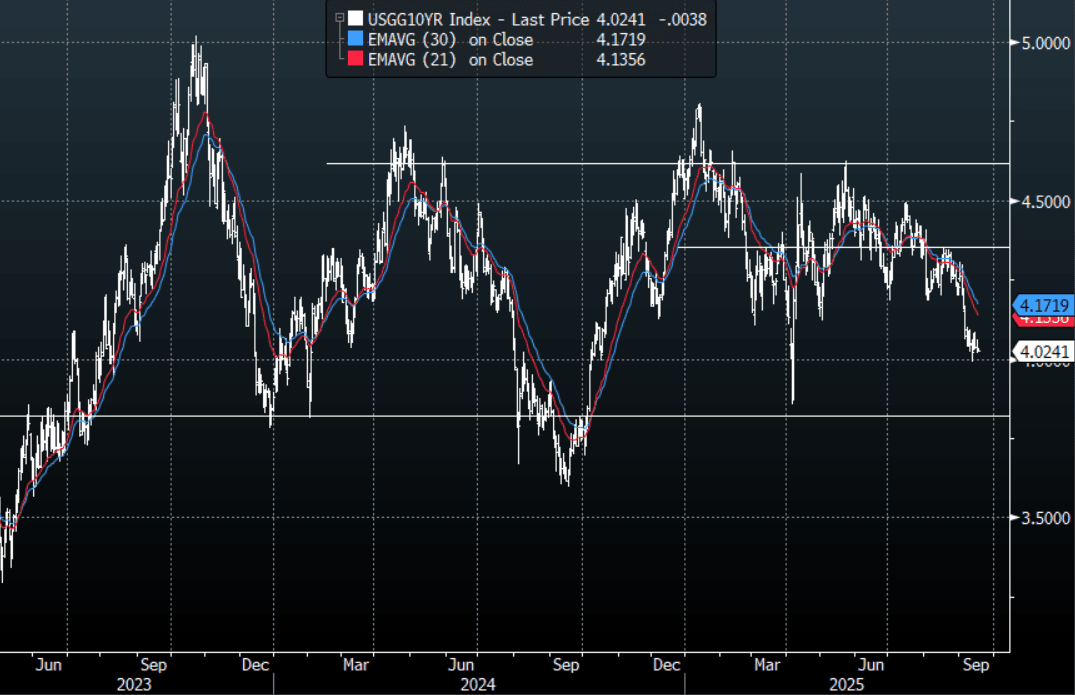

- 10-Year Yields continue to do work just above 4.00% as the market looks towards the FOMC tomorrow morning. The first buy-zone is now back towards the 4.20% area where I suspect decent demand should return initially. A sustained break through 4.00% is needed for the focus to then turn towards the 3.80% area. The market does seem confident and is pricing in a dovish outcome, the risk is Powell does not deliver.

- Luke Gromen on X: “The weaker the USD gets, the better the LT UST auctions get. It is taking a bit more USD downside to get good auctions than it used to, it seems. Where things get more interesting is when the lagged impact of the weaker USD begins to show up in inflation readings. Let's watch.”

- Nick Timiraos on X: “The Fed is expected to cut rates by 25 bps on Wednesday, with all eyes on how many officials pencil in three cuts for the year, implying consecutive cuts in October and December. A walkup to an FOMC meeting unlike any in recent memory.”

- Data/Events: MBA Mortgage Applications, Housing Starts, FOMC Rate Decision

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Market Strengthens After 20Y Auction, Japan's Exports Hit By Tariffs

JGB futures are stronger, +9 compared to the settlement levels, after today’s 20-year auction.

- The 20-year JGB auction delivered solid results across key metrics. The low price outperformed dealer forecasts, which were set at 97.80 according to a Bloomberg poll. Moreover, the cover ratio jumped to 3.9974x from 3.0853 in the previous outing and the auction tail shortened to 0.10 from 0.13.

- MNI Brief: Japan's exports fell for a fourth straight year-on-year decline in August, down 0.1% after July's 2.6% drop, as shipments of automobiles and iron, and steel products were hit by U.S. tariffs.

- Cash US tsys are little changed in today's Asia-Pac session ahead of today's FOMC decision.

- Nick Timiraos on X: "The Fed is expected to cut rates by 25 bps on Wednesday, with all eyes on how many officials pencil in three cuts for the year, implying consecutive cuts in October and December. A walk-up to an FOMC meeting unlike any in recent memory."

- Cash JGBs are little changed across benchmarks apart from the benchmark 20-year yield, which is 1.5bps lower at 2.651%.

- Swap rates are 1bp lower to 1bp higher, with a flattening bias. Swap spreads are mixed.

- Tomorrow, the local calendar will see Core Machine Orders and Tokyo Condominiums for Sale. The BoJ also starts its 2-day policy meeting.

JAPAN DATA: Exports Down Y/Y But Above Forecast, US Exports Down 13.8%y/y

Japan headline Aug trade figures were mixed. Exports were -0.1%y/y, against a -2.0% forecast (-2.6% was the July outcome). On the import side, we fell -5.2%y/y, against a -4.1% forecast and -7.4% prior outcome. The trade deficit was -¥242.5bn, against a -¥512.6bn forecast, while July's print was -¥118.4bn. In seasonally adjusted terms the trade deficit was -¥150.1bn, which was also better than forecast, but sub recent cycle highs for the balance (+¥166.5bn in Feb).

- Tariff impact was seen, with exports to the US down -13.8%y/y. To the EU exports rose 5.5%y/y, while to China exports were down a modest -0.5%y/y. The trade surplus Japan has with the US narrowed to ¥324bn. In Feb this year the surplus was at ¥918.5bn.

- Automobile exports fell 7.9% in August, the fifth consecutive decline following an 11.4% fall in July. Iron and steel exports dropped 14.9%, easing from July’s 21.0% fall. Auto exports to the US fell by 28.4%.

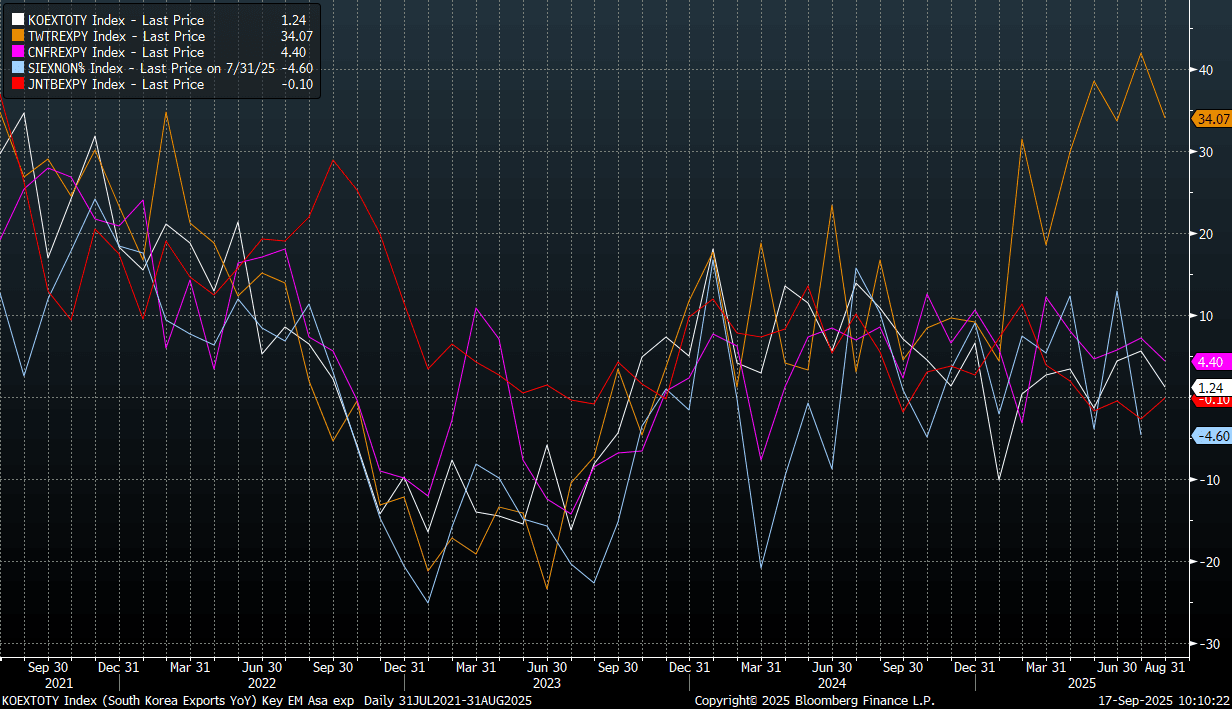

- Export growth for Japan was down in y/y terms for the fourth straight month. The chart below shows export growth for key Asian economies (Japan is the red line). Outside of Taiwan, which is the standout, the trends are broadly similar, albeit with China and South Korea managing to maintain positive y/y growth in recent months.

Fig 1: Key Asian Economy Export Growth Trends - Y/Y

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Subdued Session Ahead Of The FOMC Decision

ACGBs (YM +0.5 & XM flat) are little changed on a data-light session

- Westpac's lead index signalled slowing growth in August with the 6-month annualised rate turning negative (-0.16% down from July's +0.11%) for the first time since September 2024.

- Cash ACGBs are little changed with the AU-US 10-year yield differential at +19bps.

- The latest round of ACGB Dec-35 supply saw the weighted average yield print 0.26bp through prevailing mids (per Yieldbroker). However, today’s cover ratio fell dramatically to 2.1583x from 3.2417x. The AOFM plans to sell A$1000mn of the 1.00% 21 December 2030 bond on Friday.

- The bills strip is slightly weaker.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in September is given a 9% probability, with a cumulative 28bps of easing priced by year-end (based on an effective cash rate of 3.60%).

- Tomorrow, the local calendar will see August jobs data. Employment is forecast to rise 21k after July's +24.5k, with the unemployment rate expected to remain at 4.2%. It will also be important to monitor underemployment, the split between full-time & part-time and hours worked. The RBA is currently expected to leave rates unchanged on September 30 as it waits for Q3 CPI on October 29.

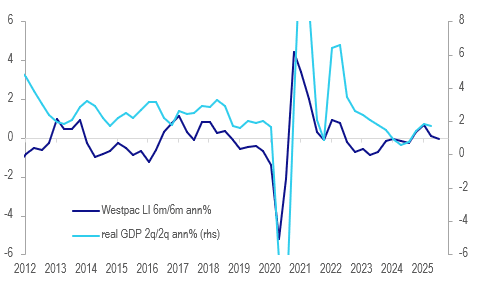

AUSTRALIA DATA: Westpac Lead Indicator Signals Slower Growth

Westpac’s lead index signalled slowing growth in August with the 6-month annualised rate turning negative (-0.16% down from July’s +0.11%) for the first time since September 2024. Almost all variables have eased over the last 6 months. It is signalling that growth on a 2q/2q basis could slow over the coming quarters.

Australia growth outlook %

Source: MNI - Market News/LSEG

- Westpac is forecasting Australian GDP growth of 1.9% in 2025 up from 2024’s 1.3% with it returning to trend next year. Its Card Tracker suggests that private consumption slowed over Q3 to early September. It expects the RBA to be on hold in September but then ease 25bp in November and twice more in 2026.

- Westpac consumer unemployment expectations has been the largest contributor to the moderation in the lead index over the last half year. It rose 4.6% in September’s consumer sentiment survey to the highest in a year and just under the series average. Thus it and confidence (-3.1% m/m Sept) are likely to continue to weigh in the next lead index.

- Commodity prices in AUDs, Westpac consumer sentiment and dwelling approvals also contributed to the moderation. Hours worked, the yield spread and US IP also made slight negative contributions with only Australian equities positive.

BONDS: NZGBS: Closed With A Modest Bull-Steepener

NZGBs closed showing a moderate curve steepener, with benchmark yields 1-3bps lower.

- (Bloomberg) Inflation-adjusted New Zealand existing home sales average price NSA fell 3.2% in August from the same period last year, according to Bloomberg calculations using official data.

- Cash US tsys are little changed in today's Asia-Pac session ahead of today’s FOMC decision.

- Nick Timiraos on X: "The Fed is expected to cut rates by 25 bps on Wednesday, with all eyes on how many officials pencil in three cuts for the year, implying consecutive cuts in October and December. A walk-up to an FOMC meeting unlike any in recent memory."

- Swap rates closed flat to 2bps lower, with a steeper 2s10s curve.

- RBNZ dated OIS pricing closed slightly softer across meetings. 23bps of easing is priced for October, with a cumulative 42 bps by November 2025.

- The focus tomorrow will be on the Q2 GDP data release. Bloomberg consensus is in line with the RBNZ's August forecast of -0.3% q/q, bringing the annual rate to flat after declining 0.7% y/y in Q2. 25bp rate cuts are expected at both the October 8 and 26 November meetings.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond and NZ$225mn of the 4.25% May-34 bond.

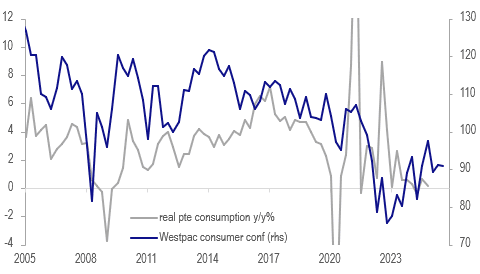

NEW ZEALAND: Households Pessimistic, Rate Refixing Should Help Going Forward

Q3 Westpac consumer confidence moderated to 90.9 from 91.2, remaining well below the series average and firmly in pessimistic territory where it has been for four years. Rate cuts have helped to support it but 250bp of easing has done little to boost sentiment as the labour market remains tough and housing market weak. Confidence is signalling only a soft improvement in real consumption growth currently.

- The 25bp rate cut on August 20 with the signal of two more by year end was included in Westpac’s survey period. Not all of the 250bp has fed through to all mortgage holders. The RBNZ said in August that “about half of existing mortgages are expected to re-fix onto lower rates over the next six months”, which should help consumer confidence going forward. It reiterated that monetary policy lags are “long and variable”.

- There was a 0.5 point rise in the present conditions index driven by better finances but expectations deteriorated 0.7 points. The expected financial situation fell 4.1 points to 3.3, below the 10-year average of 4.8. 42% of respondents said their finances had deteriorated over the last year with only 17% saying they had improved.

- Households are still not keen to buy a major item with the “good time to buy” index down 1.1 points to -10.6, well below the 10-year average of +9.0.

- The economic outlook was mixed with a pick up in the 1-year ahead assessment but a slight decline 5-years ahead.

NZ consumer outlook

Source: MNI - Market News/LSEG

NEW ZEALAND: Q2 GDP Forecast At -0.3% q/q But Some Locals Expect A Deeper Drop

Q2 GDP prints on Thursday, 18 September and Bloomberg consensus is forecasting it to contract 0.3% q/q in line with the RBNZ’s projection in August. The goods-producing sector was particularly weak over the quarter. The central bank said that activity stalled in Q2 driven by weaker business and consumer sentiment following the US’ announcement of higher tariffs. Chief Economist Conway noted that the data in July signalled that the recovery looks to have continued in Q3.

- The RBNZ expects growth to recover in H2 with Q3 forecast at +0.3% q/q and Q4 +0.8% q/q. However, weak Q2 growth, the lacklustre recovery and continued deterioration of the labour market mean that it is expected to cut rates 25bp at both its October and November meetings, in line with its projections.

- Analyst estimates for Q2 GDP are in a broad range between +0.1% q/q and -0.5% q/q.

- A number of the local banks’ expect it to print below consensus while Kiwibank and ASB are in line. ANZ and Westpac are forecasting GDP to contract 0.4% q/q while BNZ expects -0.5% q/q before it rises 0.7% in Q3.

- In terms of Q2 data released, merchandise export volumes fell 3.7% q/q while imports rose 4.2% suggesting a negative net export contribution to expenditure-based GDP.

- Manufacturing volumes fell 2.9% q/q in Q2 after rising 2.4% and the construction sector likely remained soft with building volumes down 1.8% q/q after an upwardly-revised +1.3%.

- BNZ notes that producers are being pressured by higher energy costs, weak demand and competition from imports. It also expects the public and forestry sectors to be soft.

- On a more positive note, Q2 real retail sales rose 0.5% q/q, the third consecutive quarter of growth.

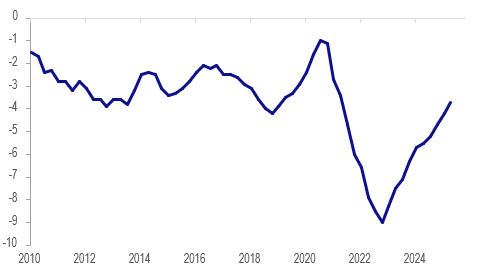

NEW ZEALAND: Current Account Deficit Lowest In 4 years

There was a sharp narrowing in the Q2 YTD NZ current account deficit as a share of GDP with it printing at 3.7% after 4.2% and the peak in Q4 2022 of 9%. Q1 was revised sharply lower at $0.709bn (nsa) and 4.2% of GDP from $2.324bn and 5.7%. The deficit in Q2 widened marginally to $0.97bn (nsa) but seasonally adjusted it narrowed $0.7bn driven by a smaller primary income deficit.

NZ current account YTD % GDP

- The seasonally adjusted deficit at $3.45bn and the share of GDP at 3.7% were the lowest in four years.

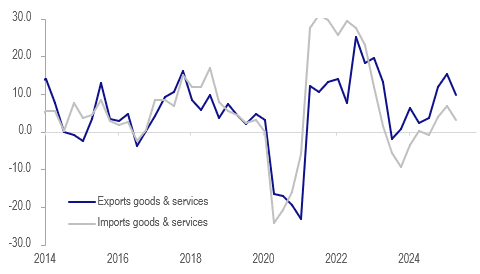

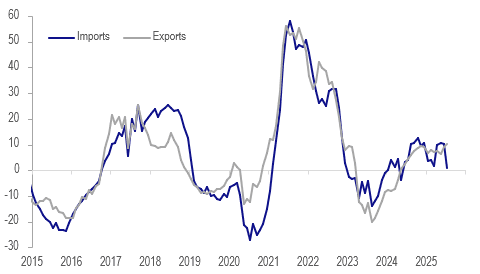

- The goods and services deficit widened slightly to $818mn with exports outpacing imports up 9.8% y/y compared to 3.1% y/y. However, services imports rose 9.6% y/y with exports up 5.3%. Goods shipments were robust +11.7% y/y while imports rose only 0.5% y/y, showing weak discretionary spending.

- The goods deficit was little changed at $128mn while services widened to $690mn.

- The primary deficit narrowed by $1bn to $2.3bn due to New Zealanders earning more on overseas investments. Also companies with international subsidiaries earned more.

NZ goods & services trade y/y%

Source: MNI - Market News/LSEG

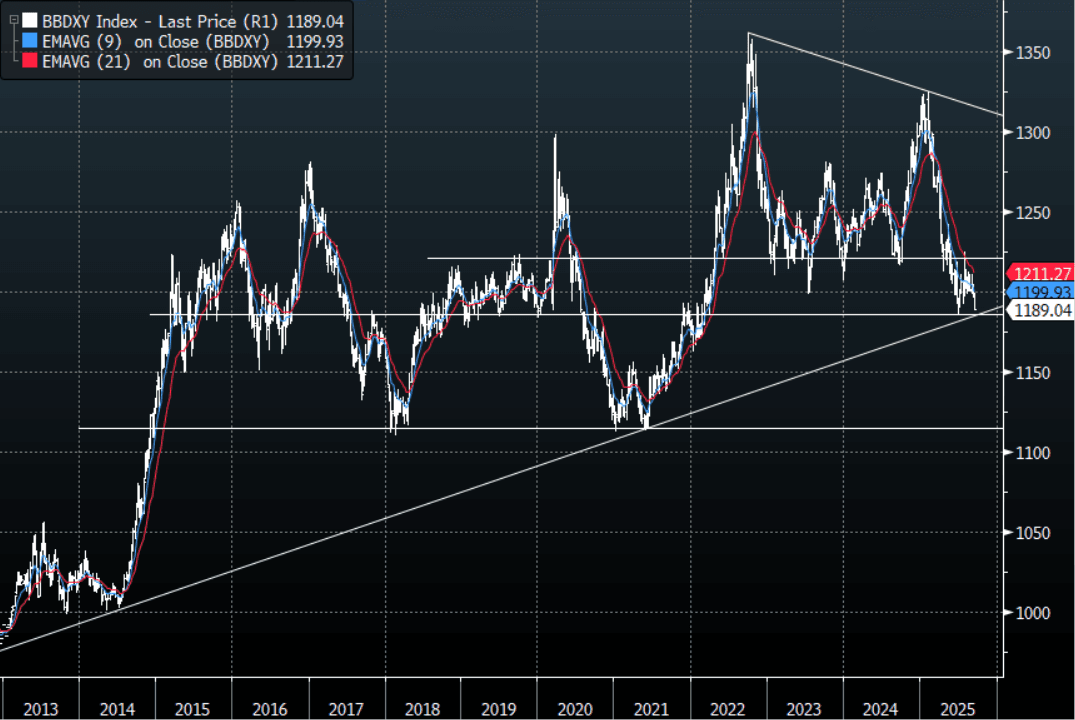

FOREX: Asia FX Wrap - The Market Is Going Into The FOMC Short USD's

The BBDXY has had a range of 1187.79 - 1189.50 in the Asia-Pac session; it is currently trading around 1189, +0.02%. The USD’s move lower gained pace overnight breaking below its recent support around 1195/97, first target is the year's lows back towards 1180. A sustained break below 1180 would be extremely bearish, should the USD start another leg lower it would have big implications for FX and potentially see a lot of the recent ranges in G10 broken. The market is clearly going into the FOMC short the USD so there is some obvious danger of disappointment, but if the market gets the dovish cut it's looking for the USD could be poised for its next big leg lower.

- EUR/USD - Asian range 1.1851 - 1.1873, Asia is currently trading 1.1855. The pair is making new highs heading into the FOMC as the USD breaks down. Should this break be sustained after the FOMC the first target is 1.2000 then the 1.2200/2300 area.

- GBP/USD - Asian range 1.3639 - 1.3659, Asia is currently dealing around 1.3645. The pair is probing the top-end of its recent 1.3350-1.3650 range, price action suggests it may be looking to break these highs and reassert its momentum higher. A sustained break above 1.3650 will initially target the year's highs just below 1.3800, through here it would open a move back to the 1.4200/1.4300 area.

- USD/CNH - Asian range 7.1004 - 7.1077, the USD/CNY fix printed 7.1013, Asia is currently dealing around 7.1050. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX -0.05%, Gold $3681, US 10-Year 4.024%, BBDXY 1189, Crude Oil $64.43

- Data/Events : EZ CPI

Fig 1: BBDXY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

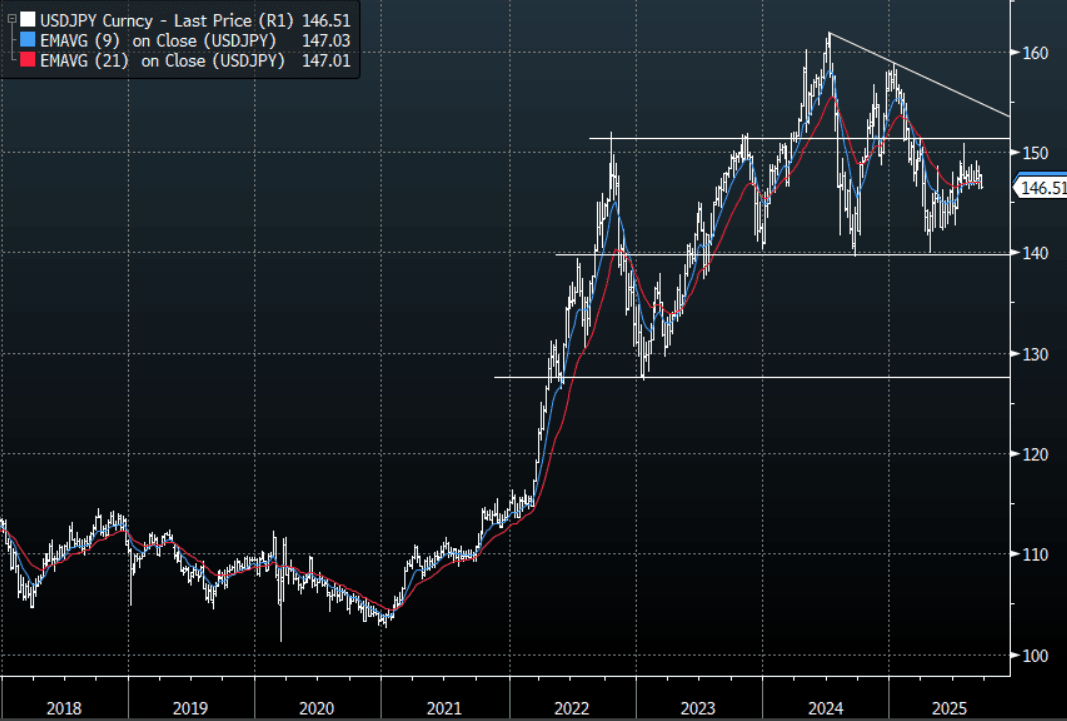

JPY: Asia Wrap - USD/JPY Pressing 146.00 Support Into FOMC

The USD/JPY range has been 146.21 - 146.61 in the Asia-Pac session, it is currently trading around 146.50, +0.03%. USD/JPY came under pressure overnight as the USD trades very heavy heading into the FOMC. The price is now just above the support of its recent 146-149 range, and we need a convincing break to see a clearer direction again. CFTC data shows leveraged funds paring back some of their short JPY position last week but remain core short, looking for this support to continue to hold. A move back below 145/146 is needed to potentially start seeing these positions being flushed out. Can the FOMC or the BOJ this week be that catalyst ?

- (Bloomberg) -- “RBC BlueBay Asset Management has taken a long yen position, betting that Japan’s political transition and a possible Bank of Japan rate hike in October could drive further strength in the currency. BlueBay’s chief investment officer Mark Dowding said the firm would also consider shifting to “go long duration” if Shinjiro Koizumi wins the LDP leadership race, and the BOJ follows through with a rate hike.”

- "Japan’s GPIF is making its first direct investment in domestic alternative assets." - BBG

- MNI Brief: Japan Aug Exports Post 4th Straight Drop: Japan’s exports fell for a fourth straight year-on-year decline in August, down 0.1% after July’s 2.6% drop, as shipments of automobiles and iron, and steel products were hit by U.S. tariffs. The data is unlikely to prompt the BOJ to alter its view that exports remain broadly flat as a trend.

- Solid Demand Metrics For 20Y Auction: The 20-year JGB auction delivered solid results across key metrics. The low price outperformed dealer forecasts, which were set at 97.80 according to a Bloomberg poll. Moreover, the cover ratio jumped to 3.9974x from 3.0853 in the previous outing and the auction tail shortened to 0.10 from to 0.13

- Options : Close significant option expiries for NY cut, based on DTCC data: 145.70($1.22b), 146.85($861m), 148.00($567m). Upcoming Close Strikes : 145.00($1.48b Sept 19), 146.40($797m Sept 19) - BBG.

Fig 1 : USD/JPY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

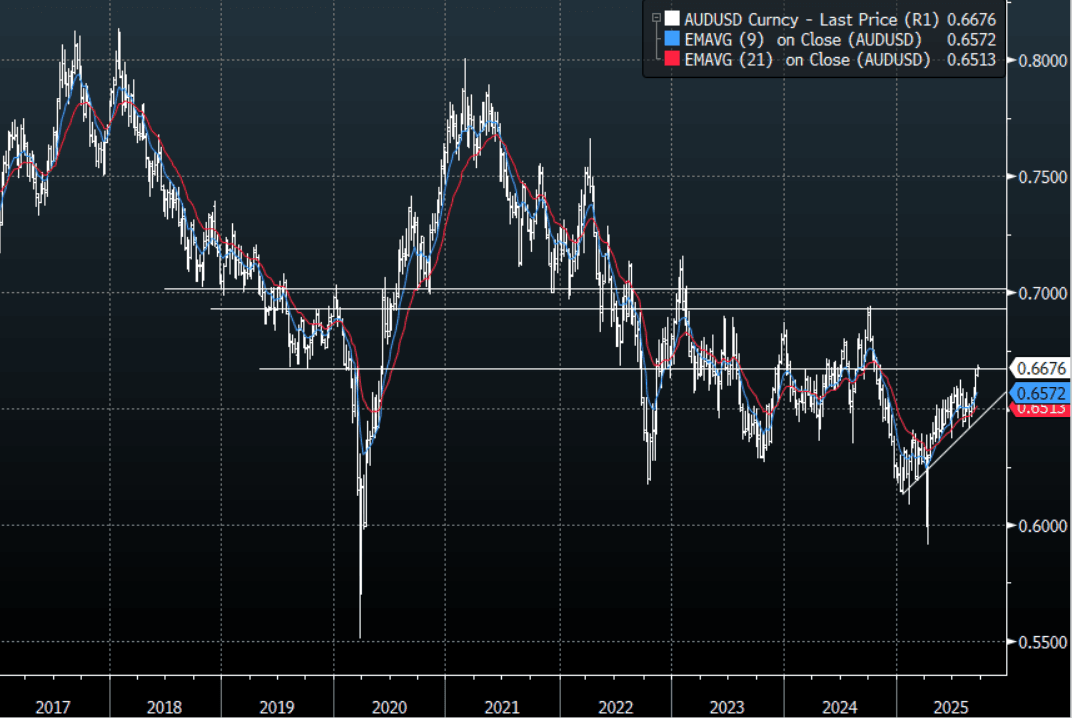

AUD: Asia Wrap - AUD/USD Pressing Resistance Heading Into FOMC

The AUD/USD has had a range of 0.6672 - 0.6690 in the Asia- Pac session, it is currently trading around 0.6675, -0.15%. US stocks finally paused for a breath ahead of the FOMC, but the USD can’t catch a break and looks to be breaking lower even before the market hears from Powell. The AUD continues to be supported and grinds higher. How the USD reacts after the FOMC will be key as the market has already priced in some significant negativity. If the USD can follow through with this move then we could see the AUD gain momentum above 0.6650/0.6700 and potentially target levels back towards 0.6900/0.7000. The price action suggests dips will be supported for now as we await confirmation of this potential break higher, the first buy-zone is back towards the 0.6550 area.

- MNI AU: Unchanged Unemployment Rate Expected On Thursday, Analysts Split. August labour market data are released on Thursday and remain a point of focus. Employment is forecast to rise 21k after July’s +24.5k with the unemployment rate expected to remain at 4.2%. It will also be important to monitor underemployment, the split between full-time & part-time and hours worked. The RBA is currently expected to leave rates unchanged on September 30 as it waits for Q3 CPI on October 29.

- MNI - Westpac Lead Indicator Signals Slower Growth: Westpac’s lead index signalled slowing growth in August with the 6-month annualised rate turning negative (-0.16% down from July’s +0.11%) for the first time since September 2024. Almost all variables have eased over the last 6 months. It is signalling that growth on a 2q/2q basis could slow over the coming quarters.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6650(AUD457m). Upcoming Close Strikes : 0.6600(AUD894m Sept 18), 0.6750(AUD1.16b Sept 19) - BBG

- AUD/JPY - Asia-Pac range 97.79 - 97.96, Asia is trading around 97.80. The pair’s move higher has finally stalled towards 98.50. Dips back towards 96.50/97.00 should be expected to be supported now first up.

Fig 1: AUD/USD spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

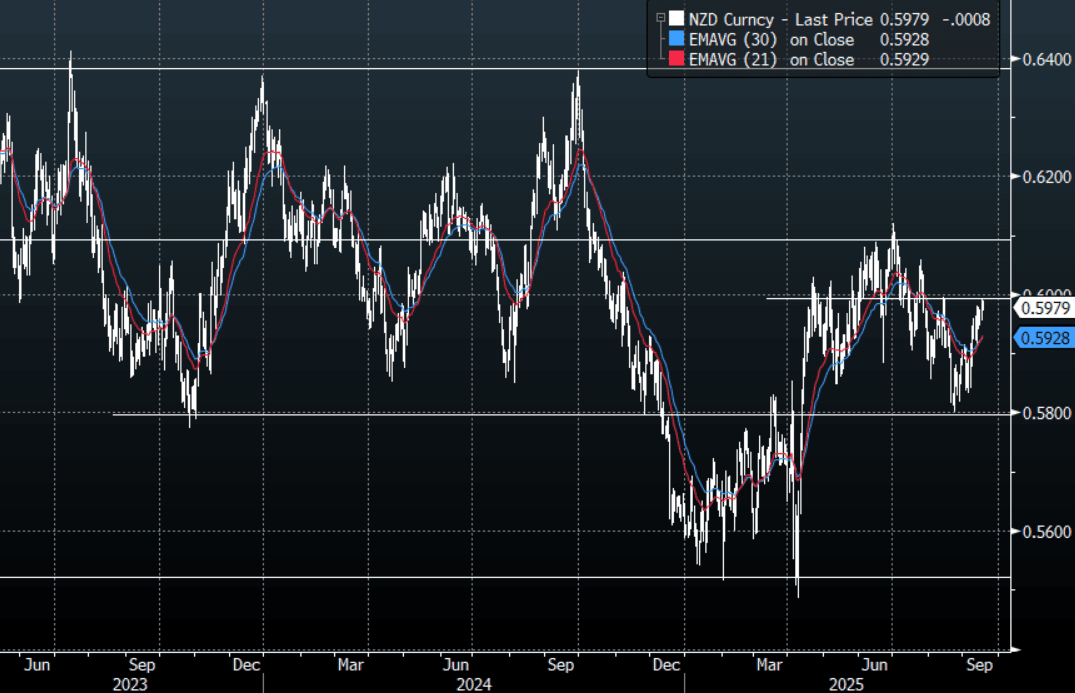

NZD: Asia Wrap - NZD/USD Stalls ahead Of 0.6000

The NZD/USD had a range of 0.5975 - 0.5990 in the Asia-Pac session, going into the London open trading around 0.5980, -0.10%. US stocks finally paused for a breath ahead of the FOMC, but the USD can’t catch a break and looks to be breaking lower even before the market hears from Powell. The USD continues to extend lower, which is supporting the NZD. A close back above 0.6000 would negate any semblance of the downward pressure it was exhibiting, but for those that have a bearish view this remains a decent entry point to express that, the FOMC tomorrow morning could be the catalyst needed for a clearer direction.

- MNI AUS - NZ Q2 GDP Forecast At -0.3% q/q But Some Locals Expect A Deeper Drop. Q2 GDP prints on Thursday, 18 September and Bloomberg consensus is forecasting it to contract 0.3% q/q in line with the RBNZ’s projection in August. The goods-producing sector was particularly weak over the quarter. The central bank said that activity stalled in Q2 driven by weaker business and consumer sentiment following the US’ announcement of higher tariffs. Chief Economist Conway noted that the data in July signalled that the recovery looks to have continued in Q3.

- "NZ’s Willis Says Economic Growth Is Picking Up After 2q stutter, acknowledges GDP report is expected to show 2q contraction" - BBG

- MNI AUS - “Current Account Deficit Lowest In 4 years: There was a sharp narrowing in the Q2 YTD NZ current account deficit as a share of GDP with it printing at 3.7% after 4.2% and the peak in Q4 2022 of 9%. Q1 was revised sharply lower at $0.709bn (nsa) and 4.2% of GDP from $2.324bn and 5.7%. The deficit in Q2 widened marginally to $0.97bn (nsa) but seasonally adjusted it narrowed $0.7bn driven by a smaller primary income deficit.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5825(NZD1.01b Sept 17), 0.5900(NZD860m Sept 17), 0.5935(NZD537m Sept 18) - BBG

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: KOSPI Off Recent Highs As China's Rally Continues

Having touched a new high of 3,449 yesterday, the KOSPI is off today on profit taking and positioning shifts ahead of the FED. As China rallied, Japan fell also in all round what was a mixed day across the region.

- All of China's major bourses are up with the Hang Seng leading the charge. The HSI is up +1.41%, the CSI 300 +0.60%, Shanghai +0.40% and Shenzhen up +0.82%.

- The Nikkei yesterday touched a new high of 44,902 and is lower by -0.05% today.

- The TAIEX in Taiwan is down -0.63%, having reached a new high of 25,629 yesterday.

- The FTSE Malay KLCI has been closed for two days and is up +0.20% Wednesday.

- The Jakarta Comp hit new highs of 7,982 today as it rallied +0.30%.

- The NIFTY 50 is up +0.33% after yesterday finishing higher by +0.68%

ASIA STOCKS: South Korea and Taiwan Inflow Surge Resumes

South Korea, along with Taiwan, were the standouts from an offshore equity flow standpoint yesterday. After a slower inflow backdrop on Monday, inflows surged yesterday amid both buoyant global and local equity market trends. The Kospi and the Taiex both rose over 1% to fresh cycle highs in Tuesday trade. Overnight saw softness, particularly in EU stocks, but the SOX positive momentum continued. Near term focus will rest with the Fed tone, particularly Fed Chair Powell's outlook for further rate cuts in terms of timing and size, post a likely easing later on Wednesday US time.

- For South Korea, via BBG: "Top net-buying by foreign investors: Samsung Electronics, Doosan Enerbility, SK Hynix, HJ Shipbuilding, Hanwha Aerospace", whilst Taiwan's inflows for Sep to date are now above $8bn, close to fresh cycle highs.

- Elsewhere, flows trends were mixed. India reverted back to modest outflows on Monday, while the 5-day sum is moderately positive.

- Indonesia saw small outflows yesterday, with today's BI decision coming into focus. Onshore demonstrations may also unfold today.

- Thailand saw better inflows yesterday, but the 5 day sum remains close to flat. Also note, Malaysian markets return today.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 1145 | 3677 | -1007 |

| Taiwan (USDmn) | 864 | 4663 | 8413 |

| India (USDmn)** | -38 | 266 | -15447 |

| Indonesia (USDmn) | -23 | -52 | -3687 |

| Thailand (USDmn) | 39 | 15 | -2503 |

| Malaysia (USDmn)* | 55 | 53 | -3753 |

| Philippines (USDmn) | -1 | -2 | -736 |

| Total (USDmn) | 2041 | 8621 | -18720 |

| * Data Up To Sep 12 | |||

| * Data Up To Sep 15 |

Source: Bloomberg Finance L.P./MNI

OIL: Crude Holding Gains Ahead Of Fed & EIA Data

Crude has held onto most of this week’s gains trending only slightly lower during today’s APAC session. WTI is down 0.1% to $64.45/bbl after a low of $64.37 but it reached $64.67 early in the session. Brent is 0.1% lower at $68.38/bbl, close to the intraday low. The USD index is little changed ahead of the Fed decision later on Wednesday.

- A dovish Fed is likely to be good for oil prices as rate cuts should support energy demand, as long as it doesn’t sound worried about the growth outlook.

- Oil prices have been supported this week by concerns that measures taken against Russia, including Ukrainian attacks on its energy infrastructure, and conflict in the Middle East could impact supplies.

- The EU is discussing further restrictions to reduce Russia’s energy revenues including sanctions on Chinese and Indian companies that facilitate imports from Russia. EC President von der Leyen said that the EU is looking into fast tracking the end of energy imports from Russia after the US said it needs to stop.

- Industry data showed a large US crude stock drawdown. The official EIA data is out later today and with the IEA forecasting a record market surplus in 2026, this data will be monitored for signs of a rising inventory trend.

- Later the focus is on the Fed (see MNI Fed Preview) but there are also August US housing starts/permits, August UK/euro area CPIs and the Bank of Canada decision (forecast to cut 25bp). In addition to Powell and BoC Governor Macklem, ECB President Lagarde and Board member Cipollone also speak today.

Gold Lower Ahead Of Today’s Fed Decision

Gold prices are down moderately during today’s APAC session after reaching a new high of $3703.07/oz on Tuesday and ahead of the Fed decision later. They are currently down 0.2% to $3681.1 after rising to $3695.39 and then falling to $3674.45. The US dollar is slightly higher and yields little changed as markets wait for Fed Chair Powell’s comments and the updated forecasts as a 25bp rate cut is widely expected.

- Silver is underperforming gold today by a large margin. It is down 1.3% to $42.00 off the intraday low of $41.792, above the 20-day EMA at $40.432. It was trading around $42.60 early in the session.

- Equities are mixed with the S&P e-mini and Nikkei down slightly, KOSPI -0.6% but Hang Seng up 1.4% and CSI 300 +0.6%. Oil prices are slightly lower with WTI -0.1% to $64.43/bbl. Copper is down 0.6%.

- Later the focus is on the Fed (see MNI Fed Preview) but there are also August US housing starts/permits, August UK/euro area CPIs and the Bank of Canada decision (forecast to cut 25bp). In addition to Powell and BoC Governor Macklem, ECB President Lagarde and Board member Cipollone also speak today.

INDONESIA: BI On Hold But Likely To Retain Easing Bias

Indonesia is widely expected to keep rates at 5% today with only 2 out of 38 analysts surveyed by Bloomberg forecasting a 25bp cut (see MNI BI Preview). Bank Indonesia (BI) holds monthly meetings and so has space to be cautious given its focus on FX stability and that it intervened to defend the rupiah in recent weeks following political instability and the replacement of respected Finance Minister Indrawati. However with signs of weakening growth and moderating inflation, it will keep its easing bias.

- Headline inflation moderated 0.1pp to 2.3% y/y in August with lower transportation inflation offsetting higher food driven by rice prices. Core moderated to 2.2% y/y from 2.3%, the lowest since October, reflecting softer domestic demand.

- Both measures are now below the mid-point of BI’s 1.5-3.5% target band but in August the central bank said that it is “confident” that inflation will remain within the corridor this year and next with inflation expectations anchored, spare capacity, effects from digitalisation and “managed imported inflation”.

Indonesia CPI y/y%

Source: MNI - Market News/LSEG

- The August S&P Global PMI showed an increase in manufacturers’ cost inflation due to the stronger USD which was passed on to customers driving selling price inflation to its highest since July 2024.

- Economic data since the August meeting have been mixed. Consumer confidence fell to its lowest in almost three years. Weak household sentiment is signalling a slowdown in consumption in Q3.

- July merchandise exports were robust rising 9.9% y/y with shipments to key destinations China and the US robust but also to the rest of ASEAN and the EU. In contrast, imports fell 5.9% y/y, a tentative signal of weak domestic demand.

- The S&P Global manufacturing PMI returned to positive territory with both domestic and export orders growing.

Indonesia merchandise exports vs imports y/y% 3-mth ma

Source: MNI - Market News/LSEG

INDIA: Country Wrap: Market Not Expecting from RBI in October

Market Summary: The NIFTY 50 is up +0.33% after yesterday finishing higher by +0.68% as the Rupee is the best regional performer, up +0.33% to 87.77. Bonds remain quiet with the IGB 10-Yr at 6.47%, -1bp today.

- Bankers have ruled out a rate cut by the Reserve Bank of India (RBI) in the upcoming monetary policy review in October, but expect one more cut during the current financial year. (source Money Control)

- PM Narendra Modi reiterated India's consistent support for peaceful resolution of Ukraine conflict and early restoration of peace and stability in a phone conversation with his Denmark counterpart Mette Frederiksen, as they discussed issues of regional and global significance. According to an Indian readout, Frederiksen reaffirmed Denmark's strong support for conclusion of a mutually beneficial India-EU Free Trade Agreement (FTA) at the earliest, and for success of AI Impact Summit to be hosted by India in 2026. (source: Times of India)

SOUTH KOREA: Country Wrap: BOK says Rates Can't Fix Housing Crisis

Market Summary: The KOSPI - having touched a new high of 3,449 yesterday, the KOSPI is off today on profit taking and positioning shifts ahead of the FED. The Won is flat at 1,379.55 and bonds modestly lower in yield. KTB 10-Yr is at 2.81%.

- Financial authorities are accelerating efforts to delist underperforming companies to further boost the stock market, with the benchmark KOSPI having surpassed a record 3,400 points, according to the Korea Exchange (KRX) Tuesday. (source Korea Times)

- The central bank chief said Tuesday that interest rate policy alone cannot control real estate prices, and the bank seeks to stabilize the housing market by preventing an oversupply of liquidity. (source Korea Times)

INDONESIA: Country Wrap: Govt to Change BI Mandate

Market Summary: The Jakarta Comp hit new highs of 7,982 today as it rallied +0.30% whilst IDR was up +0.07 to 16,428. Bonds are strong with the curve steepening. The 10-Yr is -1.5bp lower at 6.32% .

- INDONESIAN lawmakers are weighing changes at the central bank that include a broader mandate and a lower bar for removing senior officials, heightening investor concerns about the monetary authority’s independence. (source Business Times Singapore)

- Indonesian Finance Minister Purbaya who took office a week ago after the ousting of his predecessor, defended plans to dramatically stimulate the economy against concerns they could undermine the country’s hard-won fiscal standing. (source BBG)

ASIA FX: USD Steady In NEA, USD/CNY Fix Holds Above 7.1000

In North East Asia markets, FX trends have been relatively steady. Markets await the Fed outcome later, particularly in terms of the outlook, as the next risk point for broader dollar risks.

- USD/CNH rose to 7.1077 after the USD/CNY fix remained set above 7.1000. We have since drifted lower but have been unable to test sub 7.1000 so far today. CNH has lagged softer USD trends of late, maintaining a low beta to dollar falls. EUR/CNH sits off Tuesday highs, last near 8.4200.

- Spot USD/KRW rose to 1382.15 in the first part of trade, but sits back close to 1379.5 in latest dealings, little changed for the session. Local equities are down 0.80% so far today, after a strong run higher recently. Offshore investors are also modest net sellers after strong inflows yesterday, which may be curbing USD/KRW downside today at the margins.

- USD/TWD spot tested under 30.00 in the first part of dealings, but there was no follow through. We were last close to 30.04, down only modestly for the session. Like South Korea, Taiwan equities are lower today after hitting fresh cycle highs yesterday. Taiwan offshore inflows have also been very strong in Sep to date, with potentially some pause taking place ahead of the key event risk in terms of the Fed outcome.

UP TODAY (TIMES GMT/LOCAL

| Date | GMT/Local | Impact | Country | Event |

| 17/09/2025 | 0600/0800 | ** | Unemployment | |

| 17/09/2025 | 0600/0700 | *** | Consumer inflation report | |

| 17/09/2025 | 0730/0930 | ECB Lagarde at ECB Annual Research Conference | ||

| 17/09/2025 | 0800/1000 | ECB Cipollone At Associazione Bancaria Italiana EC Meeting | ||

| 17/09/2025 | 0900/1100 | *** | EZ HICP Final | |

| 17/09/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 17/09/2025 | 1115/1315 | ECB Cipollone Speaks at Netherlands Central Bank Resilience Conference | ||

| 17/09/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/09/2025 | 1230/0830 | *** | Housing Starts | |

| 17/09/2025 | 1230/0830 | *** | Housing Starts | |

| 17/09/2025 | 1345/0945 | *** | Bank of Canada Policy Decision | |

| 17/09/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 17/09/2025 | 1430/1030 | BOC press conference | ||

| 17/09/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 17/09/2025 | 1800/1400 | *** | FOMC Statement | |

| 18/09/2025 | 2245/1045 | *** | GDP | |

| 18/09/2025 | - | NorgesBank Meeting | ||

| 18/09/2025 | - | Bank of Japan Meeting | ||

| 18/09/2025 | 2350/0850 | * | Machinery orders | |

| 18/09/2025 | 0130/1130 | *** | Labor Force Survey | |

| 18/09/2025 | 0710/0910 | ECB Lagarde Video Message at Women Leadership Summit | ||

| 18/09/2025 | 0800/1000 | *** | Norges Bank Rate Decision | |

| 18/09/2025 | 0800/1000 | ** | EZ Current Account | |

| 18/09/2025 | 0800/1000 | ECB de Guindos at MNI Connect Event | ||

| 18/09/2025 | 0900/1100 | ** | EZ Construction Output | |

| 18/09/2025 | 0945/1145 | ECB Schnabel Chairs Panel at ECB Research Conference | ||

| 18/09/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 18/09/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 18/09/2025 | 1230/0830 | *** | Jobless Claims | |

| 18/09/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 18/09/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index |