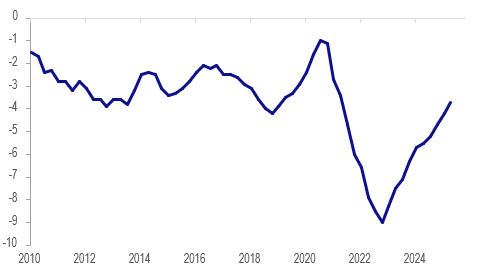

NEW ZEALAND: Current Account Deficit Lowest In 4 years

There was a sharp narrowing in the Q2 YTD NZ current account deficit as a share of GDP with it printing at 3.7% after 4.2% and the peak in Q4 2022 of 9%. Q1 was revised sharply lower at $0.709bn (nsa) and 4.2% of GDP from $2.324bn and 5.7%. The deficit in Q2 widened marginally to $0.97bn (nsa) but seasonally adjusted it narrowed $0.7bn driven by a smaller primary income deficit.

NZ current account YTD % GDP

- The seasonally adjusted deficit at $3.45bn and the share of GDP at 3.7% were the lowest in four years.

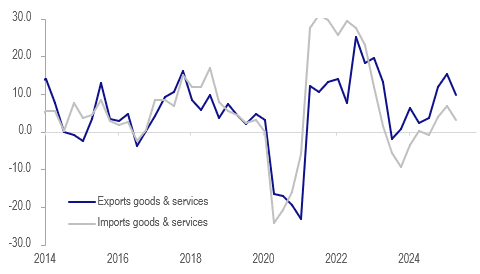

- The goods and services deficit widened slightly to $818mn with exports outpacing imports up 9.8% y/y compared to 3.1% y/y. However, services imports rose 9.6% y/y with exports up 5.3%. Goods shipments were robust +11.7% y/y while imports rose only 0.5% y/y, showing weak discretionary spending.

- The goods deficit was little changed at $128mn while services widened to $690mn.

- The primary deficit narrowed by $1bn to $2.3bn due to New Zealanders earning more on overseas investments. Also companies with international subsidiaries earned more.

NZ goods & services trade y/y%

Source: MNI - Market News/LSEG

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Cheaper With US Tsys, Light Local Calendar

ACGBs (YM -3.5 & XM -4.5) are weaker after US tsys bear-steepened on Friday, with yields 2-5bps higher.

- There was no particular event or headline that stood out, but recent whiffs of stagflation (following on from Thursday's hot producer price report) and follow-through from European long-end weakness (partly on fiscal concerns) appeared to weigh.

- While July retail sales appeared solid in our view (and led to a slight upgrade to the Atlanta Fed's GDPNow est for Q3), the August prelim UofM survey was decidedly stagflationary with weaker sentiment and higher inflation expectations, while industrial production was uninspiring and import price inflation was a little firmer than expected despite lower revisions.

- Cash ACGBs are 3-4bps with the AU-US 10-year yield differential at -5bps.

- The bills are -1 to -4, with the strip steeper.

- RBA-dated OIS pricing is slightly firmer across meetings today. A 25bp rate cut in September is given a 28% probability, with a cumulative 36 bps of easing priced by year-end.

- The local calendar will be empty today, ahead of Westpac Consumer Confidence tomorrow.

- This week, the AOFM plans to sell A$1500mn of the 1.25% 21 May 2032 bond on Wednesday and A$300mn of the 4.75% 21 June 2054 bond on Friday.

BONDS: NZGBS: Slightly Cheaper, RBNZ Policy Decision On Wednesday

In local morning trade, NZGBs are 1-2bps cheaper after US tsys bear-steepened on Friday, with yields 2-5bps higher.

- This week's calendar includes residential sector data (housing starts, homebuilder sentiment, existing home sales) and flash August PMI data as Friday’s keynote speech by Fed Chair Powell as part of the annual Jackson Hole symposium Aug 21-23.

- The July BNZ performance of services index rose to 48.9 in July from a revised 47.6 in June.

- The highlight of the week will be Wednesday’s RBNZ decision, where the MPC is likely to cut rates 25bp to 3% after pausing in July. It will also release updated forecasts, and Governor Hawkesby will hold a press conference. On Thursday, he will appear before a parliamentary committee to talk about the latest Monetary Policy Statement.

- Tuesday sees Q2 PPI output/input prices. They both rose strongly in Q1.

- July trade data print on Thursday. NZ has been running trade surpluses in recent months, helped by strong exports of primary produce and frontloading of exports to the US.

- Swap rates are 2bps higher.

- RBNZ dated OIS pricing is little changed across meetings. 23bps of easing is priced for this week, with a cumulative 42bps by November 2025.

OIL: Crude Lower Today As Market Waits For Monday’s US-Ukraine/Europe Meeting

Oil prices have started Monday’s trading lower after falling over a percent on Friday. There appears to have been some progress towards a peace deal for Ukraine. US President Trump meets with Ukraine’s President Zelenskyy and other European leaders on Monday to discuss the results of his talks with Russia’s President Putin, which the market is now focusing on. The Europeans are likely to be particularly interested in the details of the US’ offered security guarantee.

- WTI fell 1.3% to $63.14/bbl on Friday to be down 1.2% on the week and 8.8% in August. It has started today’s trading around $62.65, close to Friday’s low. It remains above initial support at $61.94, 13 August low. Initial resistance is at $70.96.

- Brent was down $66.13/bbl to be -0.7% last week and -7.8% this month. It fell to a trough of $65.73 and is currently trading below that at $65.62 but is still above the bear trigger at $65.06, 30 June low. Initial resistance is at $72.89.

- Russia is apparently offering to hold its frontlines in Kherson and Zaporizhzhia in exchange for the Donbas. US special envoy Witkoff said that the US/European security guarantee could “effectively offer Article-5 like language” (NATO), as reported by the BBC. Ukraine has to hold a referendum though to agree to changes to its territory.

- The IEA and US EIA both increased the expected size of 2026’s oil surplus. Negotiations on a peace for Ukraine is opening the possibility of an easing of sanctions on Russia which could add to global supply and so oil prices have been falling. However, if Russia is unreasonable or walks away then sanctions will be extended including punitive tariffs on those who buy its fuel which could impact supplies.