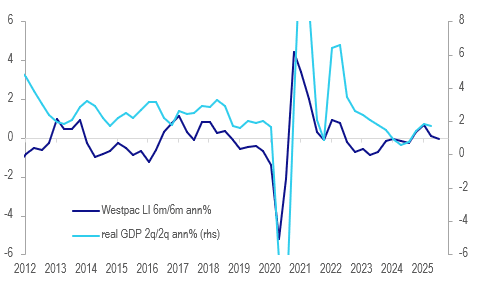

AUSTRALIA DATA: Westpac Lead Indicator Signals Slower Growth

Westpac’s lead index signalled slowing growth in August with the 6-month annualised rate turning negative (-0.16% down from July’s +0.11%) for the first time since September 2024. Almost all variables have eased over the last 6 months. It is signalling that growth on a 2q/2q basis could slow over the coming quarters.

Australia growth outlook %

Source: MNI - Market News/LSEG

- Westpac is forecasting Australian GDP growth of 1.9% in 2025 up from 2024’s 1.3% with it returning to trend next year. Its Card Tracker suggests that private consumption slowed over Q3 to early September. It expects the RBA to be on hold in September but then ease 25bp in November and twice more in 2026.

- Westpac consumer unemployment expectations has been the largest contributor to the moderation in the lead index over the last half year. It rose 4.6% in September’s consumer sentiment survey to the highest in a year and just under the series average. Thus it and confidence (-3.1% m/m Sept) are likely to continue to weigh in the next lead index.

- Commodity prices in AUDs, Westpac consumer sentiment and dwelling approvals also contributed to the moderation. Hours worked, the yield spread and US IP also made slight negative contributions with only Australian equities positive.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: BBDXY - Holding Above 1200 To Start The Week

The BBDXY range Friday night was 1201.04 - 1204.31, Asia is currently trading around 1203. The USD drifted lower again going into the weekend back towards its support just below 1200. This is clearly the side the market is more comfortable trading. A sustained break below 1197/1195 is needed to regain the momentum lower and retest the year's lows.

- Robin Brooks on X: “The 12-month rolling sum of foreign flows into longer-term US assets reached an all-time high in June. That's well after all the chaos in April around "Liberation Day" and all the weirdness on Russia and China. Markets just don't care. They continue to see US "exceptionalism...”

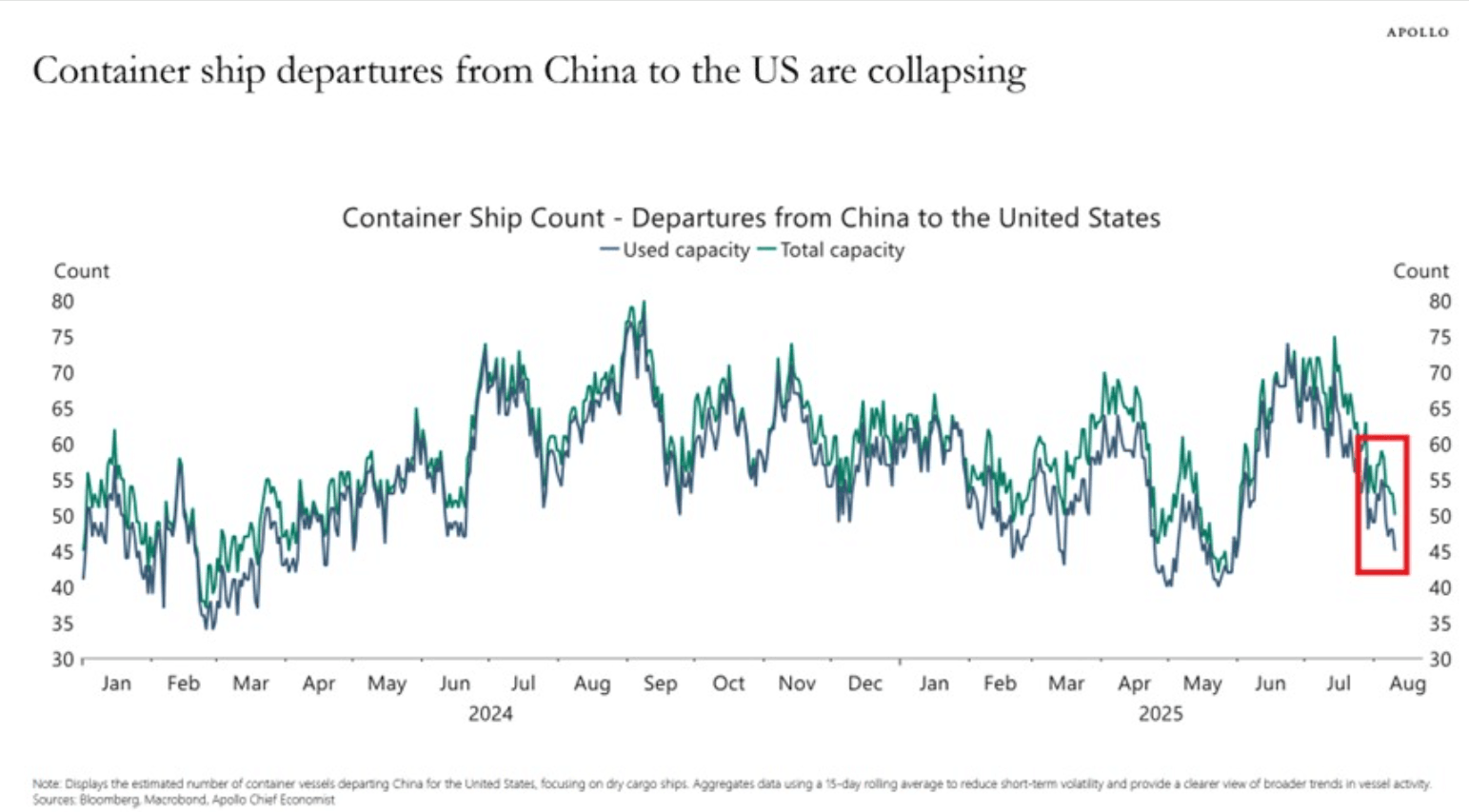

- The Kobeissi Letter on X: “Container shipping traffic from China to the US is falling again: The number of container ships departing from China to the US over the last 15 days has dropped to its lowest level since May. This is also one of the lowest readings in 2 years. Shipping volumes have declined by ~40% over the last month.This comes despite the ongoing US-China tariff truce, which was extended for another 90 days on Tuesday. US-China trade is slowing.” See Fig.1 Below.

- (Bloomberg) - The dollar’s increasingly strong ties to Treasury yields promise more volatility at a time when the path for interest rates has become a hotly-debated topic. The 30-day correlation between two-year yields and the Bloomberg Dollar Spot Index has steadily risen since April, when the relationship broke down as a backdrop of uncertainty over tariff policy focused minds on the greenback as the Sell America trade of choice.

- There is a broad consensus that the USD is set to embark on a decent move lower as the world reduces its exposure to the US and repatriates a lot of these flows. This consensus will also result in some decent short squeezes as a lot of the market is positioned the same way.

- Data/Events : New York Fed Services Business Activity, NAHB Housing Starts

Fig 1: Container Ship Count

Source: MNI - Market News/@KobeissiLetter/Apollo

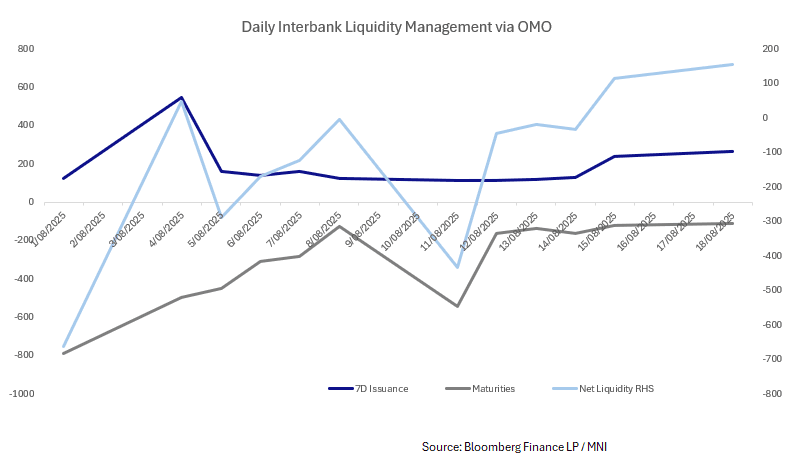

CHINA: Central Bank injects CNY154.5bn via OMO

- The PBOC issued CNY66.5bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY112bn.

- Net liquidity injects CNY154.5bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.42%, from prior close of 1.47%.

- The China overnight interbank repo rate is at 1.46%, from the prior close of 1.41%.

- The China 7-day interbank repo rate is at 1.45%, from the prior close of 1.49%.

AUSSIE BONDS: Holding Cheaper

ACGBs (YM -3.0 & XM -4.0) are weaker on a local data-light session.

- (AFR - Mark Trevarthen) “Having witnessed at close quarters the changing behaviour of bond markets across four decades now, it has become increasingly clear that Australia has matured into a high-quality destination, and the market is expanding to reflect this, not only through the broader range of corporates coming to the market to issue Australian dollar bonds, but also the wider investor base beyond Australian shores, with offshore participation in primary issuance and the secondary market increasing significantly in the past year.”

- Cash US tsys are ~1bp richer in today's Asia-Pac session after Friday's bear-steepener.

- Cash ACGBs are 3-4bps with the AU-US 10-year yield differential at -5bps.

- The bills are flat to -4, with the strip steeper.

- RBA-dated OIS pricing is slightly firmer across meetings today. A 25bp rate cut in September is given a 28% probability, with a cumulative 36bps of easing priced by year-end.

- The local calendar will be empty today, ahead of Westpac Consumer Confidence tomorrow.

- This week, the AOFM plans to sell A$1500mn of the 1.25% 21 May 2032 bond on Wednesday and A$300mn of the 4.75% 21 June 2054 bond on Friday.