MNI EUROPEAN MARKETS ANALYSIS: Eminis Eyeing Early April Highs

- Early focus was on positive trade headlines from both the US and China sides following weekend discussions in Switzerland. More details are expected to come out later today, but at this stage Eminis are up over 1.5%, while Nasdaq futures are near +2% higher.

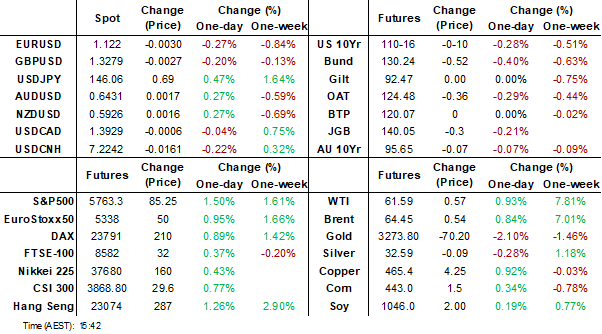

- The USD has risen against safe havens, although it has been fairly quiet post early moves. USD/JPY is holding above 146.00, while USD/CNH is lower but within recent ranges. Regional equity market sentiment is stronger, while gold is down, oil up.

- US Tsy yields have extended higher.

- Looking ahead, further trade details will be in focus, with US Tsy Secretary Bessent to talk at 9am Geneva time.

MARKETS

US TSYS: Asia Wrap - Yields Extend Higher

TYM5 has traded lower within a range of 110-15+ to 110-19+during the Asia-Pacific session. It last changed hands at 110-19, down 0-07 from the previous close.

- The US 2-year yield is higher, dealing around 3.91%, up 0.02 from its close.

- The US 10-year yield is higher, dealing around 4.40%, up 0.02 from its close.

- (Bloomberg) -- “Hedge funds aggressively added to net short positioning in 10-year note futures, while asset managers boosted longs in the sector in the week up to May 6, CFTC data shows.”

- Several regional small and medium-sized banks in China have lowered deposit interest rates in a bid to further reduce funding costs, according to Securities Daily. Following the adjustment, interest rates on certain banks’ three- and five-year medium- to long-term deposits have fallen below 2%. Analysts anticipate this downward trend will persist, citing ongoing pressure from narrowing interest rate spreads, the report said.

- Yields have all moved higher this morning as risk bounces on US-China officials citing 'substantial progress' made from weekend trade talks held in Switzerland.

- The 10-year Yield range seems to be 4.10% - 4.5%, price has bounced nicely off the 4.25/30 support, target back towards the top end of the range 4.45/50%.

- Data/Events : US CPI Tomorrow

JGBS: Sell-Off Pared But Bear-Steepener Remains, BoJ SoO Tomorrow

JGB futures are weaker, -29 compared to the settlement levels, but above session lows.

- Today's heavy session aligns with weaker US tsys, which are trading 2-4bps cheaper in today's Asia-Pac session, as risk bounces on US-China officials citing 'substantial progress' made from weekend trade talks. US Treasury Secretary Bessent said that further details would be shared today.

- The US data calendar is light today, ahead of US CPI on Tuesday and Retail Sales on Thursday.

- Japan’s April economy watchers survey current condition index fell to 42.6, compared with the median estimate of 44.6.

- Japan’s bank deposits increased at the slowest pace since April 2007 as households seek to safeguard their assets from inflation. Deposits climbed 0.7% in April from a year earlier, decelerating for a third straight month.

- Cash JGBs are 1-6bps cheaper across benchmarks, with a steepening bias. The benchmark 10-year yield is 2.2bps higher at 1.391% versus the session high of 1.41%

- Swap rates are 2-4bps higher, with swap spreads mixed.

- Tomorrow, the local calendar will see BoJ Summary of Opinions (April MPM) and Money Stock data alongside 30-year supply.

AUSSIE BONDS: Heavy Session To Start Week, Risk-On Weighs

ACGBs (YM -6.0 & XM -6.5) are sharply cheaper and near Sydney session lows.

- This move aligns with weaker US tsys, which are trading 2-4bps cheaper in today's Asia-Pac session, as risk bounces on US-China officials citing 'substantial progress' made from weekend trade talks.

- US Treasury Secretary Bessent said there had been 'substantial progress' in the two days of talks with China and that further details would be shared today.

- The US data calendar is light today, ahead of US CPI on Tuesday and Retail Sales on Thursday.

- (Bloomberg) -- “Hedge funds aggressively added to net short positioning in 10-year note futures, while asset managers boosted longs in the sector in the week up to May 6, CFTC data shows.”

- Cash ACGBs are 5bps cheaper with the AU-US 10-year yield differential at -6bps.

- The bills strip is cheaper with pricing -2 to -5 (late whites leading).

- RBA-dated OIS pricing is flat to 5bps firmer today, leaving meetings 2-24bps firmer than levels before the release of Q1 CPI data on April 30.

- Tomorrow, the local calendar will see Westpac Consumer and NAB Business Confidence measures.

- AOFM plans to sell A$1200mn of the 3.50% 21 December 2034 bond on Wednesday and A$800mn of the 2.50% 21 May 2030 bond on Friday.

STIR: RBA Dated OIS Dec-25 Pricing 25bps Firmer Than Pre-CPI Level

RBA-dated OIS pricing is 2-24bps firmer across meetings than levels before the release of Q1 CPI data on April 30.

- Q1 headline and underlying inflation printed 0.1pp higher than expected, but the trimmed mean at 2.9% y/y was below the top of the RBA’s 2-3% target band for the first time since Q4 2021.

- The data was close to the RBA’s expectations and at this stage consistent with inflation sustainably remaining within the band. Thus, another 25bp rate cut to 3.85% is likely on May 20, assuming that easing is consistent with the RBA’s updated outlook.

- A 50bp rate cut in May is given a 2% probability (10% before the CPI data), with a cumulative 93bps (117bps before) of easing priced by year-end.

Figure 1: RBA-Dated OIS – Post-CPI Vs. Pre-CPI

Source: MNI - Market News / Bloomberg

BONDS: NZGBS: Closed At Cheaps With Focus On Trade Deals

NZGBs closed at session cheaps, with benchmark yields 3-4bps higher. NZ-US and NZ-AU 10-year yield differentials were little changed.

- With the domestic calendar empty, attention was focused abroad.

- Cash US tsys are trading 2-3bps cheaper in today's Asia-Pac session as risk bounces on US-China officials citing 'substantial progress' made from weekend trade talks held in Switzerland. US Treasury Secretary Bessent said there had been 'substantial progress' in the two days of talks with China and that further details would be shared today.

- “The Reserve Bank of New Zealand (RBNZ) is "well-placed" to offset the impact of the projected lower discretionary fiscal spending on aggregate demand as the effect of the government's fiscal consolidation is likely to be limited at the macroeconomic level, ANZ Research said in a budget preview report on Monday.” (per MTN via BBG)

- Swap rates closed 3-4bps higher.

- RBNZ dated OIS pricing closed slightly firmer across meetings. 25ps of easing is priced for May, with a cumulative 75bps by November 2025.

- Tomorrow, the local calendar will be empty ahead of Card Spending and Net Migration data on Wednesday.

FOREX: G10 Wrap - Risk Holds Gains From Asian Open

The BBDXY has had an Asian range of 1227.85 - 1229.76, Asia is currently trading around 1229. “China and the U.S. have agreed to establish a formal mechanism for economic and trade negotiations, with further details and a joint statement expected to be released on Monday, according to Xinhua News Agency. The high-level talks, held in Geneva over the weekend, were described as candid, in-depth, and constructive, with significant consensus reached and substantial progress made, Xinhua reported, citing China’s top trade negotiator, He Lifeng.” “Goldman expects the onshore yuan to strengthen to 7 per dollar in 12 months”(BBG). This is pretty significant considering only a month or 2 ago the thinking was USD/CNH would have to weaken considerably due to the tariffs. It also aligns with the broader view starting to gain traction that Usd/Asia could just be starting a bigger move lower.

- EUR/USD - Asian range 1.1193 - 1.1243, Asia is currently trading 1.1230. EUR/USD gapped 50/60 points lower on the open to test below 1.1200 in early trade, price is now testing longer-term support around 1.1200, a sustained break below here would then target 1.1000. The market is still expected to use dips as a buying opportunity.

- GBP/USD - Asian range 1.3262 - 1.3295, Asia is currently dealing around 1.3285. GBP dipped on the Asian open but has since clawed back most of its losses. GPB has found buyers back towards 1.3200, if this support breaks buyers are expected to return back towards 1.3000/3100.

- USD/JPY - Asian range 145.70 - 146.28, the Asia session is currently dealing around 145.85. The 146.00/1.4700 area remains the first area in which sellers should be eager to get involved, then the more important 149/151 area. Support seen back towards 1.4400.

- USD/CNH - Asian range 7.2198 - 7.2298, the USD/CNY fix printed 7.2066. Asia is currently dealing around 7.2250. Sellers capped the 7.2500 area on Friday, and would think any move back should again be met by supply. A move through this area targets 7.27/30.

- Cross asset : SPX +1.5%, Gold $3278, US 10-Year 4.40%, BBDXY 1229, Crude oil $61.37

- Data/Events : BOE’s Lombardelli, Greene, Mann and Taylor to speak.

Fig 1: USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg

FOREX: Antipodean Wrap - AUD & NZD Outperform

The S&P is up 1.4% this morning after gapping on thin liquidity at the Asian open. It has held these gains remarkably well for now, with these early Monday morning moves having a habit of failing. There seems to be a view that the outcome of these talks could have significant implications going forward as China now sees itself coming to the negotiating table as a peer and not as a subordinate. Hu Xijin, former Editor-in-Chief of the Global Times, remarked in a recent Weibo post: “China has achieved the most equal negotiation with the United States among all nations. The two sides had been at loggerheads, but their first official contact yielded substantial results—an unexpected turn of events. I believe this breakthrough is precisely the result of China’s readiness to stand firm and its unwavering commitment to principle.” See this X link for more details https://x.com/ShanghaiMacro/status/1921759301284376957

- AUD/USD - Asian range 0.6410 - 0.6432, the AUD is currently dealing around 0.6435. AUD has outperformed this morning especially in the crosses. Good demand was seen on Friday sub 0.6400, on the day this could continue to provide support. A break below 0.6300 needed to reverse direction.

- AUD/JPY - Asian range 93.40 - 93.99, price goes into London trading around 93.75. While the support around 92.00 holds, price is likely to continue testing the Weekly resistance seen between 94.00/96.00 where sellers should remerge.

- NZDUSD - Asian range 0.5910 - 0.5931, going into London trading around 0.5935. On the day there is potential for NZD to continue to outperform as the market digests an outcome from the talks that many thought not possible. First support is right here around the 0.5900 area but more importantly the support around 0.5800 needs to hold to keep the bulls in the drivers seat.

- AUD/NZD - Asian range 1.0833 - 1.0859, the Asian session is currently trading 1.0845. Sellers continue to provide headwinds for the cross just above 1.0850, a sustained move back above 1.0900 would negate the bearish trend.

Fig 1 : AUD/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg

ASIA STOCKS: Stocks by News from Geneva

Asia stocks have been in a positive mood today with gains across all major markets following positive noises coming out of the US China discussions. Chinese tech names have performed strongly whilst Pharma companies have struggled given President Trump's plans to reduce prescription costs on pharmaceuticals.

Overall markets were strong with gains of over 2% by some key bourses.

- China's key indexes were up strongly with the Hang Seng up +0.95%, the CSI 300 +0.60%, Shanghai +0.35% and Shenzhen up +1.05%

- The TAIEX in Taiwan is up +0.92% having enjoyed strong inflows over the last week.

- The KOSPI shrugged off poor economic data to rise +0.68%, following last week's gains.

- With Jakarta, Singapore and Malaysia closed.

- Having fallen last week on concerns as to the escalating conflict with Pakistan, India's NIFTY 50 is up strongly in morning trade rising by +2.90%

ASIA STOCKS: Taiwan’s Flows Continue

Taiwan has now enjoyed US$4bn of inflows in six successive trading days.

- South Korea: Recorded outflows of -$140m as of the 9th, bringing the 5-day total to +$52m. 2025 to date flows are -$12,044m. The 5-day average is +$10m, the 20-day average is -$74m and the 100-day average of -$134m.

- Taiwan: Had inflows of +$645m as of the 9th, with total inflows of +$2,744m over the past 5 days. YTD flows are negative at -$14,471. The 5-day average is +$549m, the 20-day average of +$213m and the 100-day average of -$163m.

- India: Had inflows of +$286m as of the 8th, with total inflows of +$1,657m over the past 5 days. YTD flows are negative -$10,609m. The 5-day average is +$331m, the 20-day average of +$188m and the 100-day average of -$123m.

- Indonesia: Had outflows of -$34m as of the 9th, with total outflows of -$198m over the prior five days. YTD flows are negative -$3,252m. The 5-day average is -$40m, the 20-day average -$57m and the 100-day average -$37m

- Thailand: Recorded outflows of -$44m as of the 9th, inflows totaling -$12m over the past 5 days. YTD flows are negative at -$1,616m. The 5-day average is -$2m, the 20-day average of -$14m the 100-day average of -$18m.

- Malaysia: Recorded outflows of -$10m as of 8th, totaling +$148m over the past 5 days. YTD flows are negative at -$2,511m. The 5-day average is +$30m, the 20-day average of +$13m and the 100-day average of -$30m.

- Philippines: Saw inflows of +$8m as of the 9th, with net inflows of +$31m over the past 5 days. YTD flows are negative at -$220m. The 5-day average is +$6m, the 20-day average of +$3m the 100-day average of -$3m.

- The idea that weekend talks between China and the US have made progress, has given a strong boost to many markets today including oil.

- WTI is up over +0.60% to add to last week's gain of +4.68%.

- The move this morning sees WTI break through the 20-day EMA of $61.06, with the next key level the 50-day EMA $63.96 to be trading at $61.41

- Brent is up this morning by +0.55%, following last week's gain of +4.27% to be touching the 20-day EMA of $64.34

- A trade war has the potential to materially detract from global growth and has been one of the contributing factor to gold being lower by more than 10% this year.

- After two days of negotiations in Geneva, US Treasury Secretary Scott Bessent and Trade Representative Jamieson Greer said that they was progress and would share more information on Monday, with the same positive sentiment echoed by their Chinese counterparts.

- Ongoing concerns about Iran's nuclear program sees US and Iran in dialogue and has potential to escalate if common ground can't be met.

- Ukraine's Volodymyr Zelenskiy is set to meet with Vladimir Putin in Istanbul on May 15 for direct negotiations, following a weekend of hectic diplomacy. The meeting is conditional on Russia beginning a 30-day ceasefire on Monday.

- In potential signs that relationships are shifting, Indonesia will cut its fuel imports from Singapore and source supplies from the US and Middle Eastern countries instead.

- Saudi Aramco's net income declined 4.6% to 97.5 billion riyals in the first quarter due to lower crude prices. The company's total dividend for the quarter fell to $21.36 billion, compared with $31 billion in the same three months of last year, which will add to the strain on the Saudi budget.

- House Republicans will include money to “begin” refilling the nation’s depleted strategic oil reserves as part of their massive bill to extend President Donald Trump’s tax cuts, a key committee chairman said in an op-ed published Sunday.

Gold Falls Again as Optimism Grows

- Gold started the week lower and is trading at US$3,281.41 in afternoon trade, a decline of 1.32%.

- This morning's move sees gold breach the 20-day EMA of $3,284.60 with the 50-day EMA below at $3,162.71.

- Evidence of trade talks and the somewhat easing of tensions has taken some of the safe haven bid out of gold this morning and given the strength of last week's performance, it is likely profit taking is behind this morning's move.

- US and China reported 'substantial' progress after two days of talks in Switzerland with markets looking for a de-escalation of a trade war that could materially lower global growth.

SOUTH KOREA: Early Trade Data Craters

- South Korea's first 10 days of trade data cratered in signs that the tariff war is having a severe impact.

- Following last month's result of +6.5%, imports for the first 10days of May contracted -15.9%

- Exports contracted -23.8% for the first 10days of May, following last month's result of +13.7%.

- Exports to China at $10.88b, +3.9% YoY

- Exports to US at $10.63b, -6.8% YoY

- Imports from China at $12.50b, +0.6% YoY

- Imports from US at $6.14b, +2.2% YoY

CHINA: Country Wrap: Progress Made in Discussions. No Details as Yet

- The US and China both reported “substantial progress” after two days of talks in Switzerland aimed at de-escalating a trade war, marking what Chinese Vice Premier He Lifeng called “an important first step” toward resolving differences. While neither side immediately announced specific measures on Sunday, He said the world’s two biggest economies agreed to create a mechanism for further talks, led by US Treasury Secretary Scott Bessent and himself. Bessent said the US would share details on Monday and He promised a joint statement. (source BBG)

- China has more space to roll out financial policies to support services consumption, as the world’s second-largest economy needs to further prioritize boosting demand in face of external shocks, reports the China Securities Journal, citing experts. (source BBG).

- China's key indexes were up strongly with the Hang Seng up +0.95%, the CSI 300 +0.60%, Shanghai +0.35% and Shenzhen up +1.05%

- Yuan Reference Rate at 7.2066 Per USD; Estimate 7.2441

- Bonds remain very steady with the CGB stationary at 1.63%

ASIA FX: USD/CNH Down On Trade Optimism, Little Follow Through, USD/KRW Higher

- The early bias in USD/Asia pairs was skewed to the downside, post positive trade meeting headlines between US-China. However, follow through has been limited, particularly for the likes of USD/KRW. Much of South East Asia has been out today, limiting liquidity in that part of the region.

- USD/CNH gaped lower at the open, but found support just under 7.2200 (we opened near 7.2400). Both the US and China sides had positive comments regarding the weekend trade talks in Switzerland. More details are expected from the US side today, while a joint statement is also expected to be issued. Focus will be on lowering tariff levels and how quickly a trade deal might be achieved. The USD/CNY fix came in lower, but remained within recent ranges. Onshore equities are up the CSI 300 gaining 0.65% to be above 3870.

- Spot USD/KRW fell sharply in the first part of trade, but found support ahead of the 1392 area. We last tracked above 1404, +0.45% above end Friday levels. This goes against the generally positive risk on tone seen in terms of equities. The Kospi is close to the 2600 level. So far in May, spot USD/KRW has been supported sub 1400, suggesting some underlying USD demand.

- Spot USD/TWD has edged down slightly today, last near 30.20/25, but remains very much within recent ranges. Like elsewhere its equity market is rising firmly today (Taiex up close to 1%).

- As noted above, SEA is mostly out today. The USD/INR 1 month NDF fell back under 85.00, up around 1% at one stage before stabilizing. Sentiment has been aided by a ceasefire between India and Pakistan holding for now.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 12/05/2025 | 0800/0900 | BOE Lombardelli At BOE Bank Watcher's Conference | ||

| 12/05/2025 | 1030/1130 | BOE Greene On Monetary policy outlook | ||

| 12/05/2025 | - | *** | Money Supply | |

| 12/05/2025 | - | *** | New Loans | |

| 12/05/2025 | - | *** | Social Financing | |

| 12/05/2025 | - | ECB's Cipollone At Eurogroup Meeting | ||

| 12/05/2025 | 1250/1350 | BOE Mann On Neutral Rate Of Interest | ||

| 12/05/2025 | 1425/1025 | Fed Governor Adriana Kugler | ||

| 12/05/2025 | 1430/1530 | DMO likely to publish FQ2 consultation agenda | ||

| 12/05/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 12/05/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 12/05/2025 | 1600/1200 | *** | USDA Crop Estimates - WASDE | |

| 12/05/2025 | 1600/1700 | BOE Taylor Fireside Chat With Ed Balls | ||

| 12/05/2025 | 1800/1400 | ** | Treasury Budget | |

| 13/05/2025 | 2301/0001 | * | BRC-KPMG Shop Sales Monitor | |

| 13/05/2025 | 0600/0700 | *** | Labour Market Survey | |

| 13/05/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 13/05/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 13/05/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 13/05/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 13/05/2025 | - | ECB's De Guindos At ECOFIN Meeting | ||

| 13/05/2025 | 1230/0830 | *** | CPI | |

| 13/05/2025 | 1255/0855 | ** | Redbook Retail Sales Index |