MNI EUROPEAN MARKETS ANALYSIS: China Nov Activity Data Softens

- USD/JPY is lower, after better Tankan survey data, while BoJ liaison points to solid 2026 wage growth. NZD/USD faltered, along with local rates, as the new RBNZ Governor noted financial conditions had tightened more than expected since the Nov policy meeting.

- China activity data for Nov was mostly below expectations, with retail sales slowing notably. Nov house prices also continued to fall. Still, asset market fallout has been limited.

- Looking ahead, we have the US Empire manufacturing survey out, along with further Fed speak (Miran and Williams).

MARKETS

US TSYS: Yields Grind Lower on Equity Weakness

US bond futures continued to add gains in the afternoon session with the 10-Yr up +04 to 112-09+. TYH6 is at the mid-point of the 100-day EMA of 112-14 and the 200-day EMA of 111-30 and will look to the array of data out over the coming days for the catalyst for the next move.

Cash was strong with the front end leading the rally as yields across the curve fell by up to -1.4bps.

- The 2-Yr is down -1.2bps to 3.512%

- The 5-Yr is down -1.2bps to 3.731%

- The 10-Yr is down -0.08bps to 4.178%

- The 30-Yr is down -0.2bps to 4.845%.

Other than equity market weakness, tonight markets will focus on Empire Manufacturing (exp 10.0 vs prior 18.7), preliminary PMIs for December, November CPI but the key event later in the week Non Farm Payrolls for November.

Tonight sees a US$86bn 13-week bill and a US$77bn 26-week bill auction.

JGBS: Mixed Performance To Start BOJ Decision Week, Hike 95% Priced

JGB futures are unchanged compared to settlement levels after a relatively subdued session.

- Expectations for a 25bp rate hike (from 0.50% to 0.75%) at the BOJ's December 18-19 meeting have strengthened over the past couple of weeks. Governor Ueda signalled earlier this month that the Bank may be ready to move, shortly after the yen fell to a 10-month low against the dollar, heightening concerns about imported inflation.

- Nearly two-thirds of analysts surveyed by Bloomberg expect the BOJ to lift rates roughly every six months from this month onward, with the median terminal rate for the cycle forecast at 1.25%. Markets now assign a 94% probability to a hike this week, with another increase priced in by September 2026.

- Cash US tsys are flat to 1bp richer.

- Cash JGBs are mixed across benchmarks, with yields 1bp higher (20-year) to 1.5bps lower (40-year). The benchmark 10-year yield is 0.4bp higher at 1.958% versus the cycle high of 1.98%.

- The swaps curve has twist-steepened, with rates 0.5bps lower to 2bps higher.

- Tomorrow, the local calendar will see S&P Global PMIs (Services & Composite) alongside an Auction for Enhanced-Liquidity 5-15.5 YR.

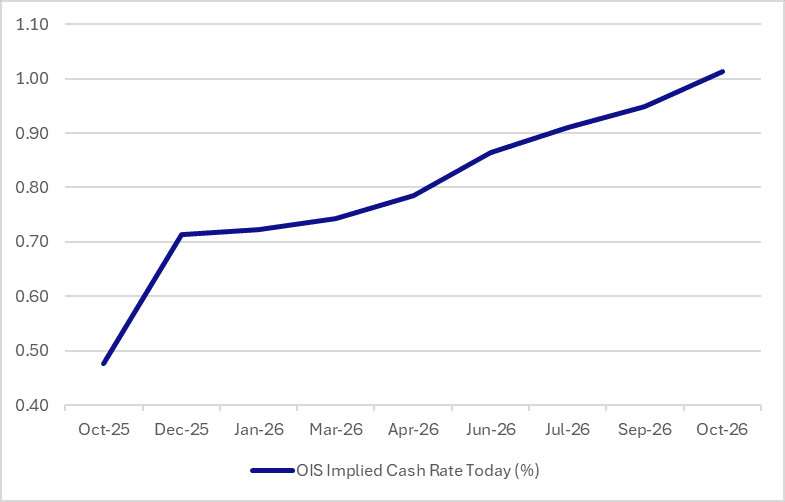

Figure 1: BOJ-Dated OIS

Source: Bloomberg Finance LP / MNI

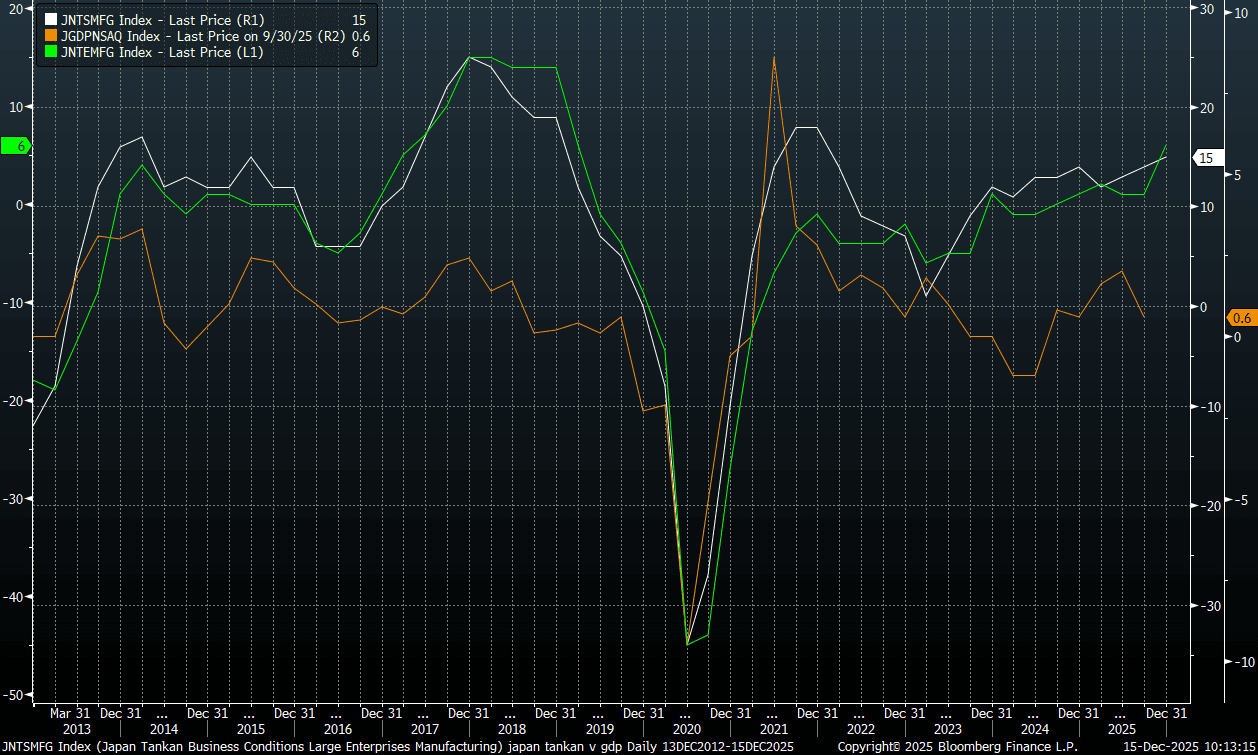

JAPAN DATA: Q4 Tankan Should Support Confidence In Outlook

The Q4 Tankan survey mostly met or exceeded market expectations. The headline index for large manufacturers printed at 15, which was also the market consensus, and versus 14 prior. The outlook was 15, above the 13 forecast and 12 prior reading. For large non-manufacturers we printed 34, versus 35 forecast and 34 prior. The capex outlook edged up to 12.6%, versus 12.5% prior and against a 12.1% forecast. The data, at face value, bodes well for a recovery in GDP y/y momentum, as well as the Capex outlook. It shouldn't impact BoJ thinking around an expected hike this week, but is likely to give renewed confidence into the 2026 outlook.

- Notably smaller manufacturing firms saw Q4 conditions rise to 6, well above the 2 expected and 1 prior. The Q4 outcome was the highest print since 2019. The outlook was also stronger than forecast at 2, (-1 projected).

- The chart below plots the large (the white line) and small (green line) manufacturing Tankan readings against Japan y/y GDP growth (the orange line).

- The BoJ noted that less trade uncertainty (while tariff impact was also less than feared), along with positive chip demand, as supporting the outlook. Weaker consumption, rising labour costs were cited as negatives, while retailers also voiced concerns over China-Japan relations.

- On the inflation side, on average, companies saw the annual consumer inflation rate at 2.4% in December, unchanged from September. Firms also expected sales prices to increase 4.3% three years ahead, unchanged from September, and 5.2% five years ahead, also unchanged from the previous survey. (via our Tokyo policy team).

Fig 1: Japan Tankan Trends & GDP Y/Y Growth

Source: Bloomberg Finance L.P./MNI

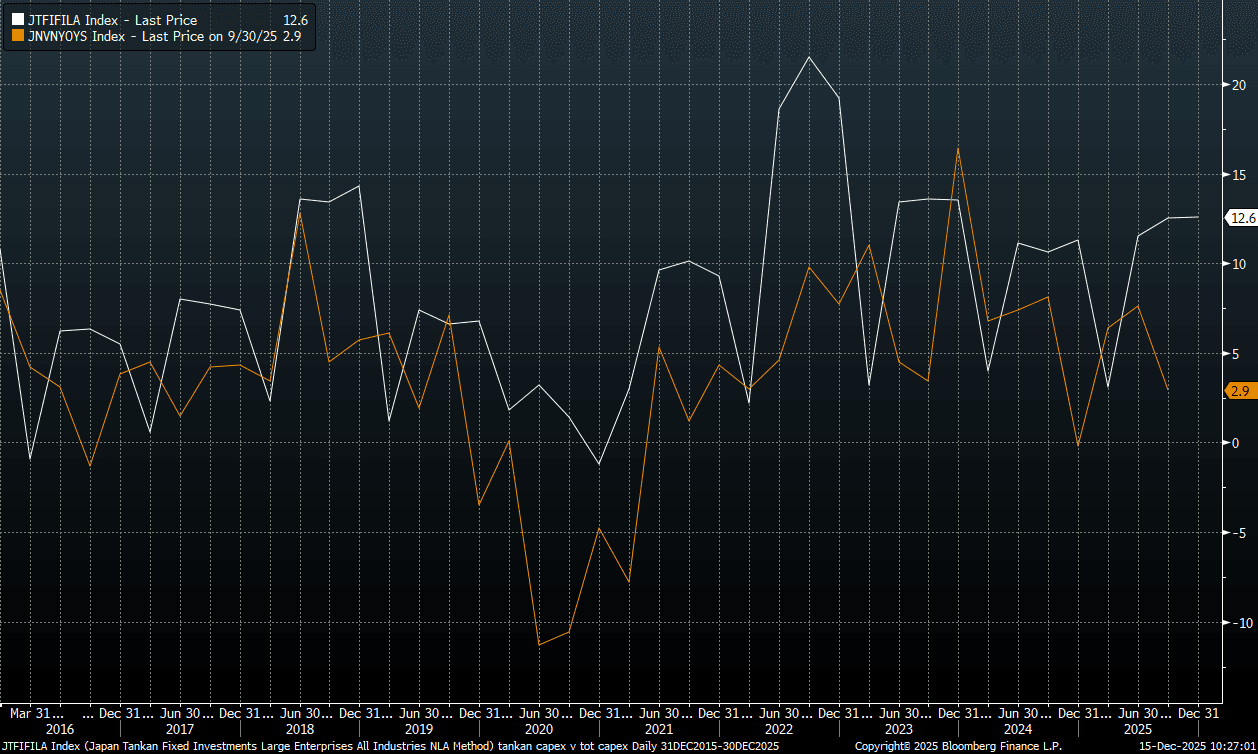

JAPAN DATA: Tankan Capex Intentions Nudged Higher, Well Above Long Run Average

The chart below plots the Tankan Q4 Capex outlook, which nudged up to 12.6%, versus actual capex spend (which eased back to 2.9% in Q3). Capex intension per the Tankan survey remain above long run averages and continue to suggest a resilient backdrop for this important driver of Japan growth. Capital expenditure plans by smaller firms are expected to rise 0.1% this fiscal year, revised up from -2.3% in September and also above the historical average.

Fig 1: Japan Tankan Capex Intentions & Actual Capex

Source: Bloomberg Finance L.P./MNI

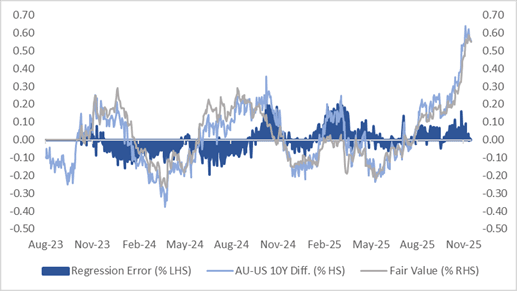

AUSSIE BONDS: AU-US 10Y Consolidates Range Break, Looks Fairly Priced

ACGBs (YM +2.0 & XM flat) are slightly stronger after a relatively subdued start to the week.

- Cash US tsys are flat to 1bp richer.

- Cash ACGBs have twist-steepened, with yields 3bps lower to 1bp higher. The AU-US 10-year yield differential is at +56bps. At this level, the differential sits just below its cycle high set earlier this month, the widest since mid-2022.

- December’s price action has consolidated the differential’s breakout above the ±30bps range that had prevailed since November 2022. This widening has occurred alongside a steady increase in market-implied expectations for the RBA cash rate.

- Indeed, a simple regression of the 10-year yield differential against the AU–US 1Y3M differential over the past two years suggests the current spread is around fair value.

- Bills pricing is +3 to +4.

- RBA-dated OIS pricing has softened 1-4bps today. Nevertheless, pricing continues to show tightening across all meetings, with the probability of a 25bp hike rising from 29% for February to 81% by June and 150% by December 2026.

- Tomorrow, the local calendar will see S&P Global PMIs (Services & Composite) and Consumer Confidence.

- The AOFM plans to sell A$1000mn of the 4.25% 21 October 2036 bond on Wednesday.

Figure 1: AU-US Cash 10-Year Yield Differential (%)

Source: Bloomberg Finance LP / MNI

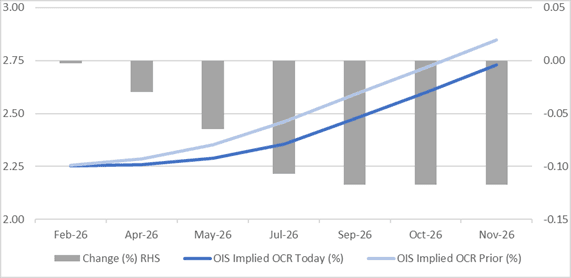

BONDS: NZGBS: Strong Rally As RBNZ Gov Pushes Back Vs Hike Expns

NZGBs closed showing a bull-steepener, with yields 5-9bps lower, after the market viewed comments from RBNZ Governor Anna Breman as a warning that market pricing was too hawkish.

- RBNZ Governor Anna Breman has pushed back against investor bets on an interest-rate hike next year, saying she expects the Official Cash Rate will remain unchanged for some time. “Financial market conditions have tightened since the November decision, beyond what is implied by our central projection for the OCR,” Breman said in a statement Monday in Wellington. “As always, we are closely monitoring wholesale market interest rates and their effect on households and businesses.”

- On a relative basis, NZGBs have outperformed their $-bloc counterparts, with the NZ-US and NZ-AU 10-year yield differentials 4-5bps lower. Today’s move has halted the sharp rebound in the NZ-AU differential following the recent RBNZ policy decision and guidance.

- Swap rates closed 1-5bps lower, with a steeper 2s10s curve.

- RBNZ-dated OIS pricing closed 12bps softer for late 2026 meetings. No tightening is priced for February, while November 2026 now assigns 48bps.

- Tomorrow, the local calendar will see Food Prices and Non-Resident Bond Holdings data alongside the Government’s Half-Year Fiscal Update.

Figure 1: RBNZ Dated OIS Current vs. Prior (%)

Bloomberg Finance LP

NEW ZEALAND: Services PMI Weakens Further, Remains Entrenched Sub 50.0

The New Zealand services PMI lost momentum for Nov, printing at 46.9, versus 48.4 in Oct. The index has remained sub 50.0 since the early parts of 2024, although we are above 2025 lows (44.2 seen in May). This comes after Friday's manufacturing PMI remained above 50.0, while card spending for Nov showed a firmer trend. Overall, the data reinforces the patchy nature of the current economic recovery in NZ, which is yet to establish a firm footing.

- In terms of the detail, the weakness was most prominent for the activity/sales index, which fell to 45.8 from 48.4, while the employment index printed at 46.4, from 48.6 in Oct.

- Via BBG: "Composite indicator for services and manufacturing suggests downside risk to growth expectations for early 2026": via BNZ.

RBNZ Governor - Financial Conditions Have Tightened More Than Expected

The RBNZ has released some remarks from new Governor Breman, as she is making several media appearances this week. The Governor states that the economy has evolved broadly in line with the conditions laid out in the Nov policy review: “We continue to see signs that growth is recovering after having stalled in the middle of this year. The labour market is still weak but is expected to recover as demand in the economy strengthens. We remain confident that annual headline consumers price index inflation will decline towards the 2 per cent target mid-point by the middle of next year.”

- She added that the OCR projections imply a slight risk of further easing, but: “However, if economic conditions evolve as expected the OCR is likely to remain at its current level of 2.25 per cent for some time.

- Interestingly, she added that: “Financial market conditions have tightened since the November decision, beyond what is implied by our central projection for the OCR,” Dr Breman says. As always, we are closely monitoring wholesale market interest rates and their effect on households and businesses. “Ahead of our next OCR decision in February, we will continue to assess incoming data, financial conditions, and global developments, and implications for New Zealand’s economic outlook and our medium-term inflation objective.” Dr Breman reiterated that monetary policy is not on a preset course. (via the RBNZ)

- NZD/USD is weaker in the aftermath of the comments, down 0.50% to sub 0.5780. The 2yr swap rate is off 5bps to be back under 2.79%.

FOREX: USD - BBDXY Struggles to Bounce, Is It Lagging ?

The BBDXY has had a range today of 1206.24 - 1207.71 in the Asia-Pac session; it is currently trading around 1206, -0.05%. The USD has failed to react to a weak close in US stocks or US yields in the long-end moving higher. Is it lagging or correctly seeing the moves as unconvincing that probably won’t follow through, or could it also be pricing in the potential Supreme Court decision that some believe is imminent. On the day look for initial resistance again back towards the 1208-1209 area and above here the more important 1212-1214 area where sellers should remerge. Support is in the 1204/05 area; a move below here would target 1198-1200.

- EUR/USD - Asian range 1.1729-1.1745, Asia is currently trading 1.1735. The pair is trading sideways trying to hold onto its gains above 1.1700. On the day, first support is toward 1.1705-1720 initially, if this does not hold, look for demand to then return in the 1.1660-1.1680 area.

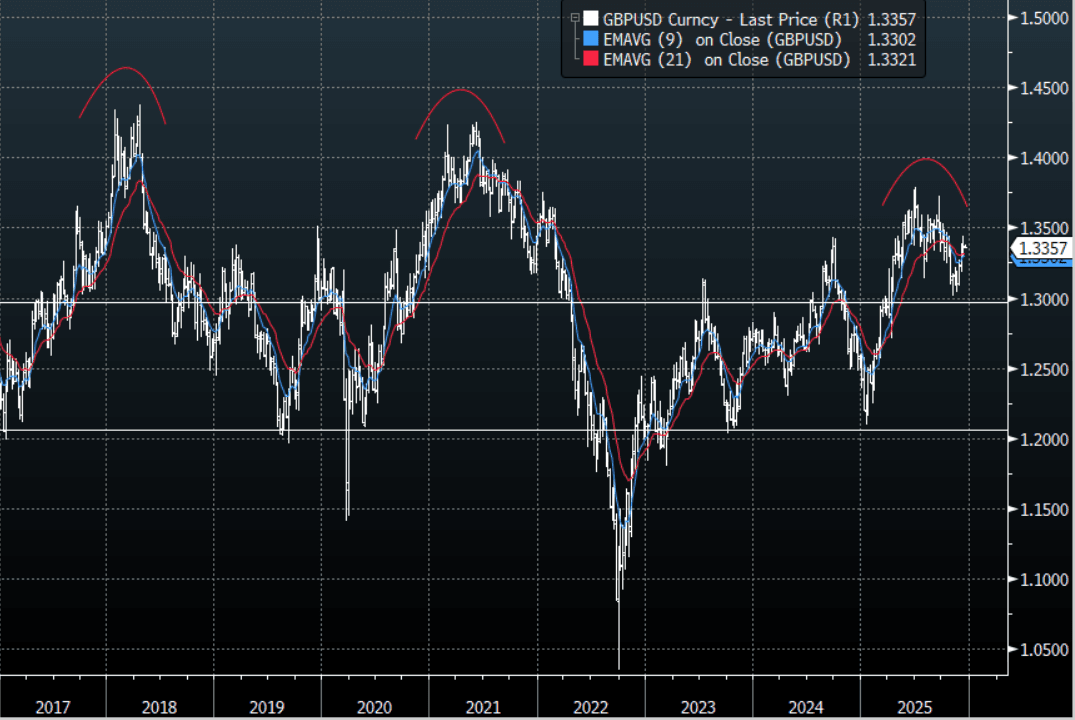

- GBP/USD - Asian range 1.3355-1.3381, Asia is currently dealing around 1.3360. The pair stalled above 1.3400 at the end of last week. On the day GBP has initial support around the 1.3325-1.3345 area, if this does not hold look for a pullback to the more important 1.3250/80 area. I continue to watch for signs of GBP potentially topping out.

- Cross asset : SPX +0.20%, Gold $4330, US 10-Year 4.176%, BBDXY 1206, Crude Oil $57.74

- Data/Events : Germany Wholesale Price Index MoM/Bloomberg Dec. Germany Economic Survey, France Bloomberg Dec. France Economic Survey, Spain Bloomberg Dec. Spain Economic Survey, EZ Bloomberg Dec. Eurozone Economic Survey

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

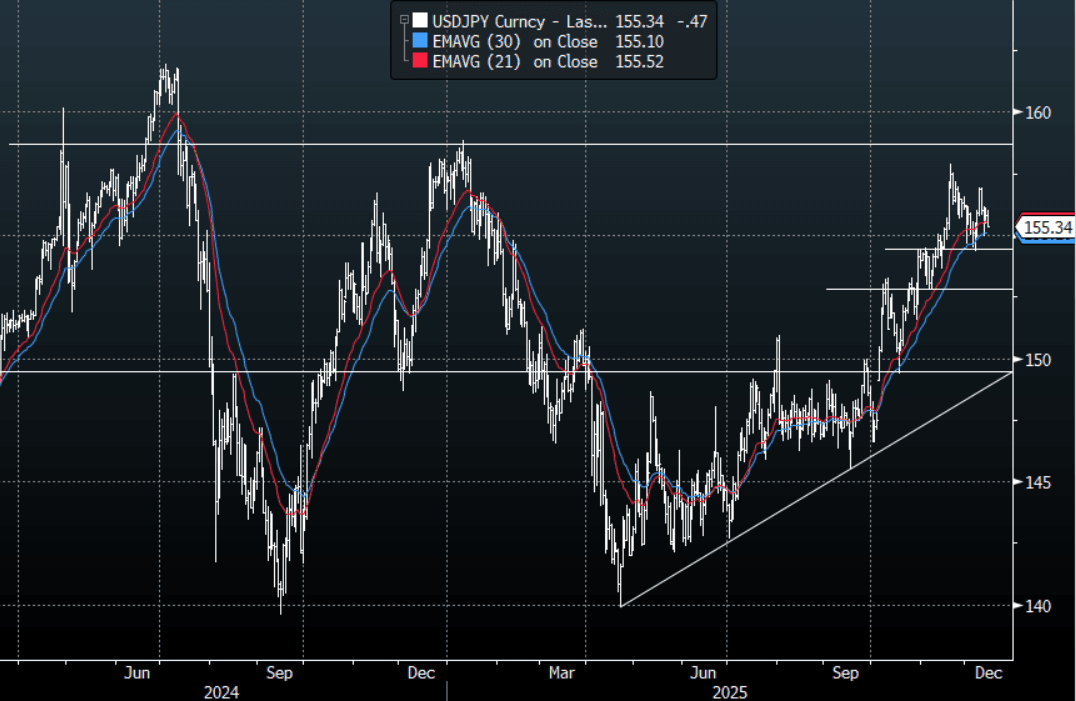

JPY: USD/JPY - Slides Lower After Stalling Around 156.00 Again

The USD/JPY range today has been 155.30 - 155.99 in the Asia-Pac session, it is currently trading around 155.35, -0.30%. The pair saw demand into the Japanese fix but topped out toward 156.00 and quickly turned lower trading heavily thereafter for most of the session. A poor close for risk to end the week, how it starts this week will be important for cross-Yen. The market is pricing in a hike by the BOJ for this week but US yields in the long-end are still under pressure. For the time being this is keeping the JPY confined to a wider 154.50-157.00 range. Technically USD/JPY is in an uptrend, the first big support is back toward the 152.50-154.50 area. In today's Asian session, the resistance back toward the 156.00-156.30 area capped price so look for a retest of the 155.00 area at some point a break of which would then turn the focus toward 154.40.

- MNI: BOJ Tankan: Key Sentiment Rises, Solid Capex Plans. Japanese benchmark business sentiment rose slightly from three months earlier for a third consecutive quarter, while sentiment among major non-manufacturers was unchanged. The Tankan also indicated that capital investment plans by major and smaller firms this fiscal year remain solid and above historical averages, supporting the BOJ’s view that the virtuous cycle from income to spending continues to function.

- Options : Close significant option expiries for NY cut, based on DTCC data: 156.00($907m), 156.50($1.2b). Upcoming Close Strikes : 157.00($3.95b Dec 18 ), 158.00($4.78b Dec 18 ), 159.00($6.46b Dec 18 ) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 96 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

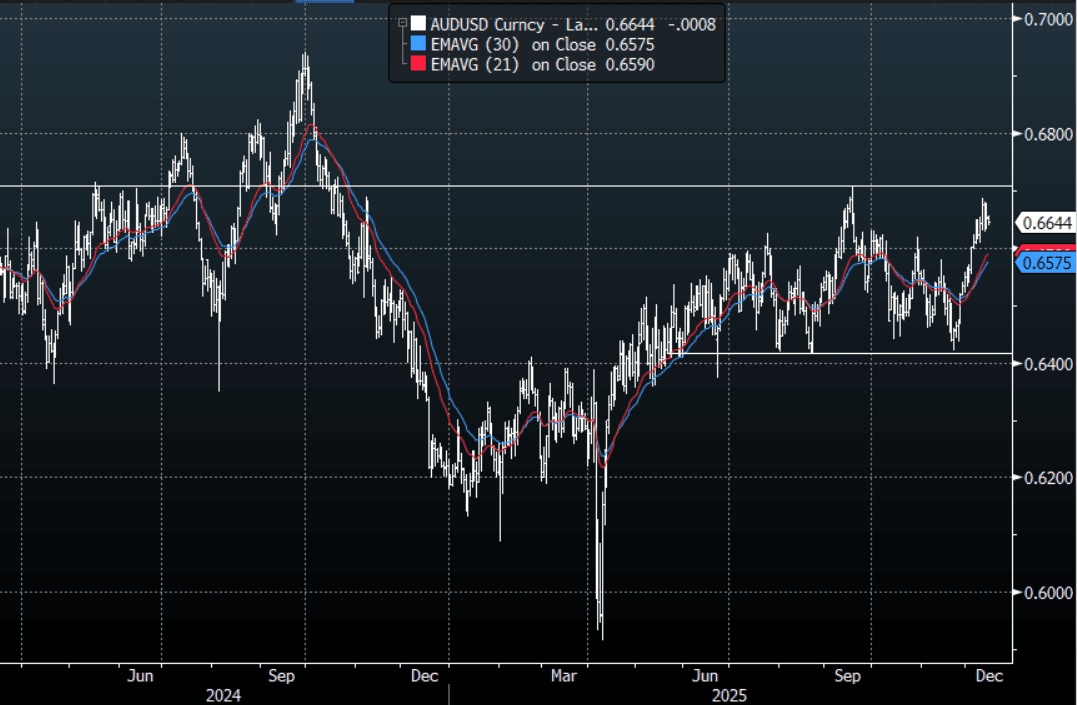

AUD/USD - Holds Up Around 0.6650 For Now

The AUD/USD has had a range today of 0.6638 - 0.6655 in the Asia- Pac session, it is currently trading around 0.6645, -0.05%. The AUD continues to consolidate around the 0.6650 area. The US stock market wobbled on Friday as AI concerns came back to the fore and US yields in the long end tick back up. This saw the USD’s decline stall but it has not bounced, yet. The AUD price action remains very constructive but the way risk starts the week will have important implications for its direction. While the AUD remains above 0.6500-0.6550 I suspect dips should continue to be supported. On the day, I will be watching how risk opens the week and whether the 0.6600-0.6630 will continue to find demand. If this area does not hold it could signal a deeper pullback toward the 0.6550 area.

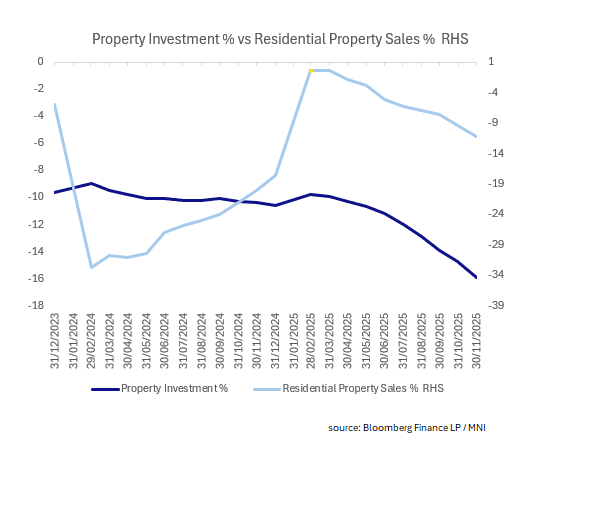

- MNI AU - China Property Investment and Sales Fall Further, No End in Sight: Following on from the release of further price decrease in new and used homes, November property Investment and Property Sales fell to lows of the year. The combined result is the worst in 5-Years. The weakness in the consumer is the challenge right now as the property sector declines continue. Finding a way of halting the slide in prices and hence investment must be key to start the process of rebuilding consumer sentiment.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6555(AUD548m), 0.6650(AUD970m), 0.6750(AUD494m) . Upcoming Close Strikes : 0.6550(AUD1.07b Dec 18 ), 0.6675(AUD8989m Dec 18 ) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 40 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

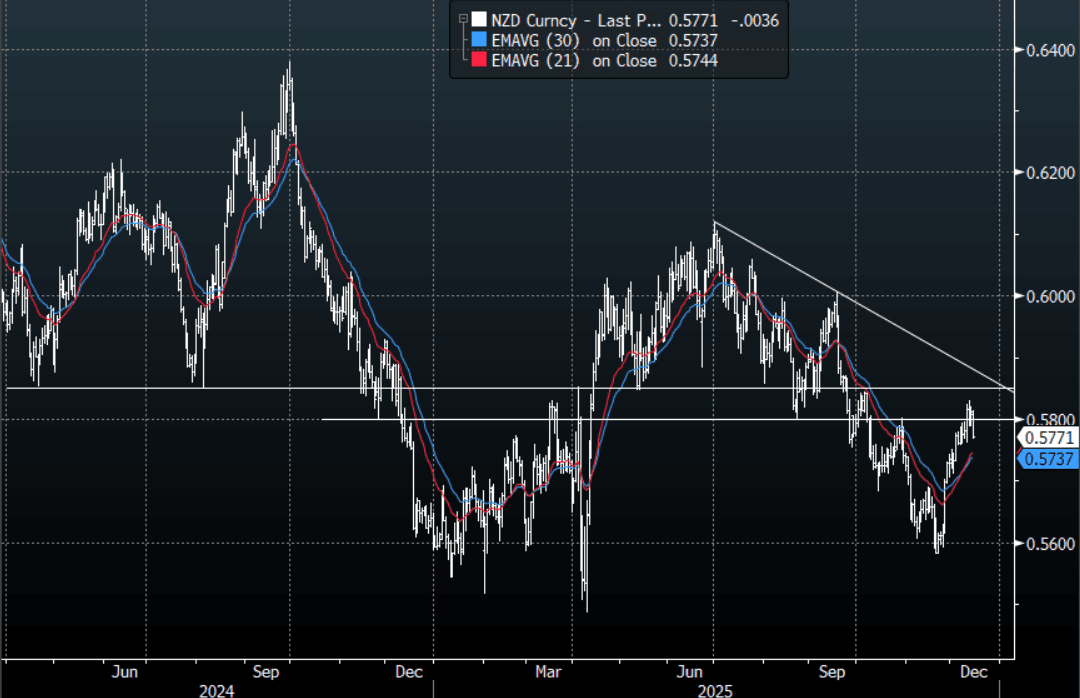

NZD/USD - Fails Above 0.5800, Support seen 0.5730-50 Initially

The NZD/USD had a range today of 0.5766-0.5814 in the Asia-Pac session, going into the London open trading around 0.5766, -0.70%. The NZD has slid lower in our day aided by comments from the RBNZ Governor. The US stock market wobbled on Friday as AI concerns came back to the fore and US yields in the long end tick back up. This saw the USD’s decline stall but it has not bounced, yet. The NZD’s momentum higher looks to have stalled above 0.5800 for now. On the day, price has broken below the 0.5780 area, signaling a potential retracement to the more important 0.5730/0.5750 support. I have this area between 0.5800-0.5900 as being decent longer-term resistance and it has provided some early headwinds on its first attempt.

- RBNZ Governor - Financial Conditions Have Tightened More Than Expected: The RBNZ has released some remarks from new Governor Breman. The Governor states that the economy has evolved broadly in line with the conditions laid out in the Nov policy review: "We continue to see signs that growth is recovering after having stalled in the middle of this year. The labour market is still weak but is expected to recover as demand in the economy strengthens. We remain confident that annual headline consumer price index inflation will decline towards the 2 per cent target mid-point by the middle of next year."

- She added that the OCR projections imply a slight risk of further easing, but: "However, if economic conditions evolve as expected the OCR is likely to remain at its current level of 2.25 per cent for some time.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5650(NZD410m Dec 18 ), 0.5690(NZD531m Dec 18 ), 0.5860(NZD471m Dec 18 ) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 40 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: US Lead Weight on Asia Stocks, China's Property Sector in Focus

The woes in China's property sector was on full show today as the November data dump saw lower prices, lower property sector investment and lower sales. This comes on the back of China Vanke's failed bid to secure enough support from bondholders for its proposal to extend the repayment of a bond due mid-December. The extension plan needed ~90% approval but fell far short, with many holders voting against it.

In Japan markets await the BOJ decision this week with expectations they will raise rates, counter to global trends in interest rates. Markets expect the BOJ to raise rates to 0.75% from 0.50% at their meeting on December 19 and when combined with the lead in from global equities, it weighed heavy on Japan's stocks today. India's stocks are opening with a cautious tone following the global lead in and caution ahead of the wholesale price data release later. Wholesale prices fell by their most since July 2023 in October and whilst they are expected to see an improvement, are also expected to remain negative.

Tech stocks are down -1.5% -3.00% across the region as equity volatility brings into questioning their valuations, given the rally since April.

- The NIKKEI is down -1.35% Monday and at 50,063 is set to test 50,000. The KOSPI is down -1.1% for its worst start to the trading week in some time.

- China's major bourses are all down, with the Hang Seng falling by the most. Down -0 .9%, the HSI led the CSI 300 which is lower by -0.18%, Shanghai -0.11% and Shenzhen down -0.38%

- India's NIFTY 50 has opened up down -0.36% and at 25,959 is testing the 20-day EMA of 25,957

- SE Asia's major bourses are starting the week positively with the Jakarta Comp up +0.60%, the FTSE Malay KLCI up +0.08% and the SE Thai up +0.35%

| CHINA PROPERTY STOCKS | Today's Move |

| Poly Developments and Holdings Group Co Ltd | -1.40% |

| China Vanke Co Ltd | -4.00% |

| Greenland Holdings Corp Ltd | -0.60% |

| China Merchants Shekou Industrial Zone Holdings Co Ltd | -0.22% |

| Sunac China Holdings | -1.50% |

ASIA STOCKS: Fresh AI/Tech Doubts Could Impact South Korea/Taiwan Flows

Equity inflow momentum was mostly positive for EM Asia markets on Friday, although it remains to be seen if these trends persist at the start of this week. Fresh doubts around the AI/chip outlook weighed heavily on tech sensitive bourses on Friday (SOX off 5%). South Korean and Taiwan bourses are down over 1% in the first part of Monday dealings. Per the BBG NBUY function, offshore investors have sold around $387mn of local shares so far today in South Korea's Kospi. Via BBG: "“Investors’ excitement over AI’s capabilities has given way to concerns about accounting issues, earnings and credit quality, mounting competition, returns on invested capital, and the sustainability of the AI trade” (Yardeni Research).

- Inflow momentum has generally been positive for South Korea and Taiwan since the start of Dec, with South Korea only seeing 2 outflows days over this period. For Taiwan net outflows for the past trading month are at -$4.4bn, but in late Nov this metric got close to -$13bn.

- In India, outflow momentum persisted for much of last week, further pushing down year to date outflows. Local bourses did see better trends though from last Friday.

- In South East Asia, trends were mixed, with most notable outflows from Thailand on Friday, although it only just nudged us into net outflows for the past week.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 161 | 1144 | -4052 |

| Taiwan (USDmn) | 395 | 820 | -4103 |

| India (USDmn)* | -205 | -681 | -17765 |

| Indonesia (USDmn) | 17 | 85 | -1560 |

| Thailand (USDmn) | -41 | -8 | -3297 |

| Malaysia (USDmn) | 12 | -115 | -4773 |

| Philippines (USDmn) | -5 | -76 | -832 |

| Total (USDmn) | 334 | 1170 | -36382 |

| * Data Up To Dec 11 |

Source: Bloomberg Finance L.P./MNI

Oil Edges up Monday Off Near Term Lows

- Oil has ticked up in Monday trading in Asia after finishing last week on the back foot.

- WTI is up +0.37% to US57.75 bbl yet remains down over 1.2% in December alone.

- WTI finished down -4.3% last week for it's biggest weekly decline since early October as supply fears continue to pressure oil prices.

- Brent is also up Monday, gaining +0.4% to US$61.45. Brent remains below all major moving averages with the 20-day EMA above at US$62.62 bbl.

- Ukraine overnight announced that it hit a major Russian oil refinery and storage depot overnight

- As markets look towards year end in what has been a volatile and very weak year for oil, it would be reasonable to suggest that markets will remain thin into year end.

- According to a report from BBG Friday, oil traders have decreased their bets with net-long positions the least bullish in seven weeks and the total short only positions the highest in seven weeks.

- In signs that the supply glut is starting to impact behaviour, last week state producer Saudi Aramco recently cut the price of its flagship crude grade for Asia to the lowest level in five years. In addition, the Paris-based International Energy Agency forecasts that there will be a record global crude glut next year.

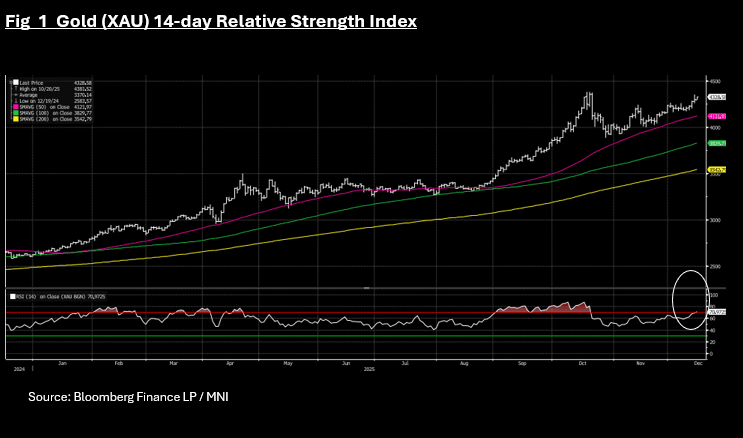

- Gold has continued last week's rally Monday as equity markets across the region have a weak start.

- Gold is up +0.67% to US$4,328.41 and is now -0.60% below the October high of US$4,356.30

- Gains in recent days sees gold now overbought on the 14-day relative strength index. Having spent most of September and October overbought gold then moderated back below.

- Gold will have the dual forces impacting it over the coming days being equity markets and the technical outlook. Equity volatility could provide a natural bid to gold into month end yet US interest rates will continue to be key in the next move for bullion.

- As data continues to flow in the US post shutdown, there will be a lot to digest for gold markets as they assess the probability of rate cuts in 2026.

- Currently the market has only 6bps of cuts priced in for the next FED meeting, suggesting that should this week's data be weaker than expected, markets could look to price in greater expectations for cuts.

- Weaker data could feed into gold prices also. Given gold has no coupon, it is very sensitive to rate cuts (reduces funding costs) and this week could be provide further input into whether the next FED meeting could become a 'live' meeting.

- CMOC Group, one of China’s biggest miners, extended its push into precious metals with a $1 billion deal to buy the Brazilian operations of Equinox Gold Corp. It will take full ownership of two Equinox entities — Leagold LatAm Holdings BV and Luna Gold Corp. — that control several mines or deposits in the South American nation. (per BBG)

- ANZ Group analysts have restated their forecasts for gold, predicting it will reach US$4,800 in 2026.

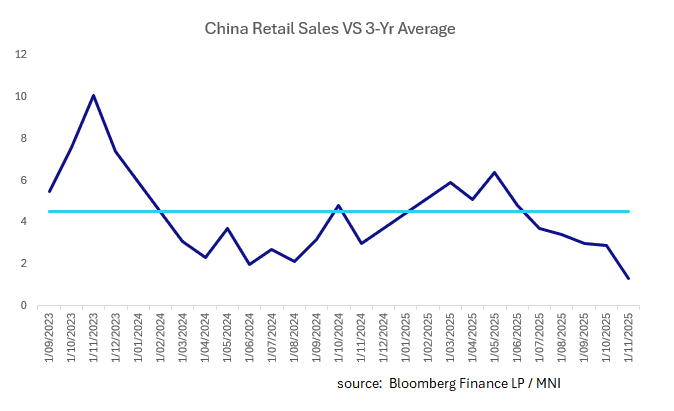

CHINA: NOV. Retail Sales in Surprise Drop

- China's November retail sales had the smallest expansion since 2022.

- Rising just 1.3% it was a marked downturn from 2.9% in October.

- The YTD YoY figure was marginally lower than October at 4.0% but consistent with recent trends.

- The rapid decline in consumer goods, clothing, household electronics, food and services are worrying signs for the outlook for domestic demand and for some domestic commentators, point to the need for further policy response.

- Recent comments from the government suggest that any policy response may not be imminent and that given China is on track to hit its 5% GDP target, may not be forthcoming.

- Equity markets have taken their lead from global moves and are down this morning, whilst bonds are steady with the CCGB 10-Yr at 1.84%

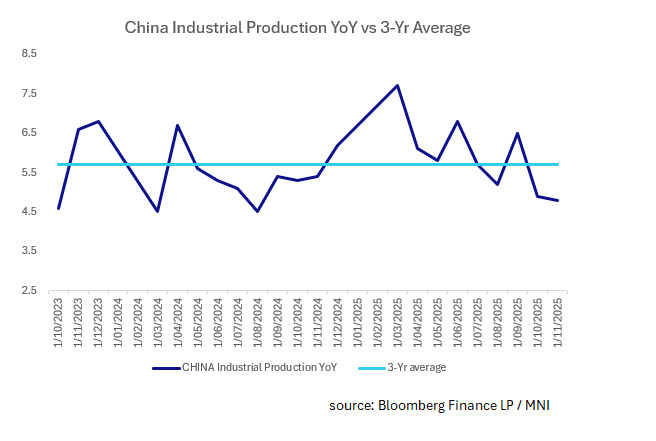

CHINA: Industrial Production Continues Sold Expansion

- China's November industrial production was marginally lower than October, but continues along a robust trend of solid output.

- Up +4.8%, it was marginally down from +4.9% in October.

- The YoY YTD number was +6.0%, just down from +6.1% in October.

- By sector, big increases were seen in coal, oil & gas extraction, food production, pharmaceutical.

- Declines came from food processing, autos and machinery productions.

CHINA: Property Investment and Sales Fall Further, No End in Sight

- Following on from the release of further price decrease in new and used homes, November property Investment and Property Sales fell to lows of the year.

- Property Investment YTD YoY fell -15.9%, the lowest in more than 3-Years.

- New home sales value fell -11.2% YoY, new property construction fell -20.5% YoY.

- The fall in Residential Property sales accelerated in November to -11.2%, from -9.4% YoY, the largest drop in 2025.

- The combined result is the worst in 5-Years

- The weakness in consumer is the challenge right now as the property sector declines continue. Finding a way of halting the slide in prices and hence investment must be key to start the process of rebuilding consumer sentiment.

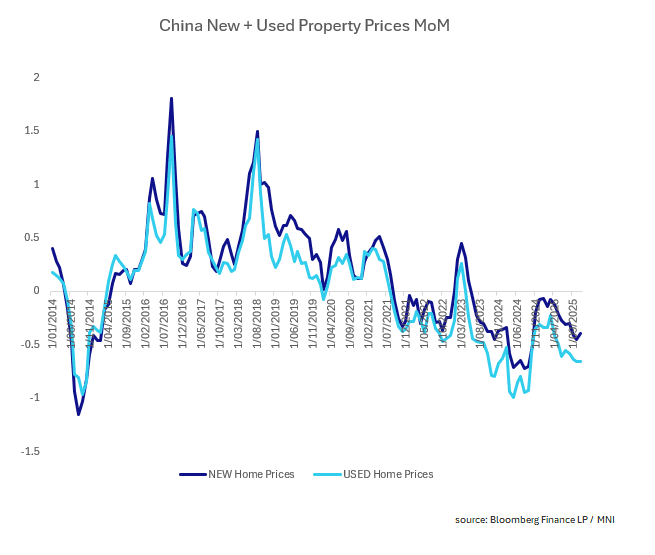

CHINA: Home Prices Fall in November Amidst Vanke's Woes

- New Home and Used Home prices declined in November, in line with prior month results.

- New Home prices were down -0.39%, from -0.45% in October. This marks the 30th consecutive month of declines.

- Used Home prices were down -0.66%, in line with October.

- November home prices fell in 59 of 70 cities month on month with Shanghai recording very modest new home prices growth.

- Whilst there has been no new policy announcements, policymakers continue to discuss various options such as nationwide mortgage subsidies for first-time buyers, increased income tax rebates for mortgage holders, and lower property transaction costs. The timing and final design remain uncertain.

- There is a push to expand the sale of already completed homes nationwide, moving away from the pre-sale model that has eroded buyer trust due to project delays. This aims to restore confidence but puts additional financial strain on developers who must finish projects before selling.

- The "whitelist" mechanism, which provides bank lending to eligible projects, continues to be expanded. In October 2025 an estimated CNY7 trillion in loans had been approved through this system, despite the bank's reluctance to add risk to the sector.

- Continued concerns about China Vanke and its ability to repay outstanding debt remains a key overhang in investor’s minds as Vanke seeks an extension to its payment obligations. China Vanke failed to secure enough support from bondholders for its proposal to extend the repayment of a bond due mid-December. The extension plan needed ~90% approval but fell far short, with many holders voting against it, resulting in volatility for the property sector.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 15/12/2025 | 1000/0500 | * | CREA Existing Home Sales | |

| 15/12/2025 | 1000/1100 | ** | EZ Industrial Production | |

| 15/12/2025 | 1315/0815 | ** | CMHC Housing Starts | |

| 15/12/2025 | 1330/0830 | ** | Monthly Survey of Manufacturing | |

| 15/12/2025 | 1330/0830 | ** | Empire State Manufacturing Survey | |

| 15/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 15/12/2025 | 1330/0830 | *** | CPI | |

| 15/12/2025 | 1430/0930 | Fed Governor Stephen Miran | ||

| 15/12/2025 | 1500/1000 | ** | NAHB Home Builder Index | |

| 15/12/2025 | 1530/1030 | New York Fed's John Williams | ||

| 15/12/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 15/12/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 16/12/2025 | 2200/0900 | *** | Judo Bank Flash Australia PMI | |

| 16/12/2025 | 0030/0930 | ** | Jibun Bank Flash Japan PMI | |

| 16/12/2025 | 0700/0700 | *** | Labour Market - AWE & Unemployment | |

| 16/12/2025 | 0700/0700 | *** | Labour Market - Payrolls & Claimants | |

| 16/12/2025 | 0700/0700 | *** | Labour Market - AWE & Unemployment | |

| 16/12/2025 | 0700/0700 | *** | Labour Market - Payrolls & Claimants | |

| 16/12/2025 | 0815/0915 | ** | S&P Global Services PMI (p) | |

| 16/12/2025 | 0815/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 16/12/2025 | 0830/0930 | ** | S&P Global Services PMI (p) | |

| 16/12/2025 | 0830/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 16/12/2025 | 0900/1000 | ** | S&P Global Services PMI (p) | |

| 16/12/2025 | 0900/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 16/12/2025 | 0900/1000 | ** | S&P Global Composite PMI (p) | |

| 16/12/2025 | 0900/1000 | ** | Italy Final HICP | |

| 16/12/2025 | 0930/0930 | *** | S&P Global Manufacturing PMI flash | |

| 16/12/2025 | 0930/0930 | *** | S&P Global Services PMI flash | |

| 16/12/2025 | 0930/0930 | *** | S&P Global Composite PMI flash | |

| 16/12/2025 | 1000/1100 | * | Trade Balance | |

| 16/12/2025 | 1000/1100 | *** | ZEW Current Expectations Index | |

| 16/12/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 16/12/2025 | 1000/1100 | Foreign Trade | ||

| 16/12/2025 | 1330/0830 | *** | Employment Report | |

| 16/12/2025 | 1330/0830 | *** | Employment Report | |

| 16/12/2025 | 1330/0830 | *** | Employment Report | |

| 16/12/2025 | 1330/0830 | *** | Employment Report | |

| 16/12/2025 | 1330/0830 | *** | Retail Sales | |

| 16/12/2025 | 1330/0830 | *** | Retail Sales | |

| 16/12/2025 | 1355/0855 | ** | Redbook Retail Sales Index |