MNI EUROPEAN MARKETS ANALYSIS: China Equities Lose Ground

- It was quiet on the bond side today, with Japan markets out. We did hear some comments from the LDP leadership candidates. Takaichi noting there may be a need for more bond issuance.

- The USD was steady against the majors, while NZD lost ground. BBG reported a new RBNZ Governor may be announced tomorrow. China equities pulled back in the aftermath of no fresh stimulus hints from late yesterday. The USD was firmer against most Asian currencies.

- Looking ahead we have preliminary PMIs for Sep due out in the UK, EU and US. Fed speak also continues.

MARKETS

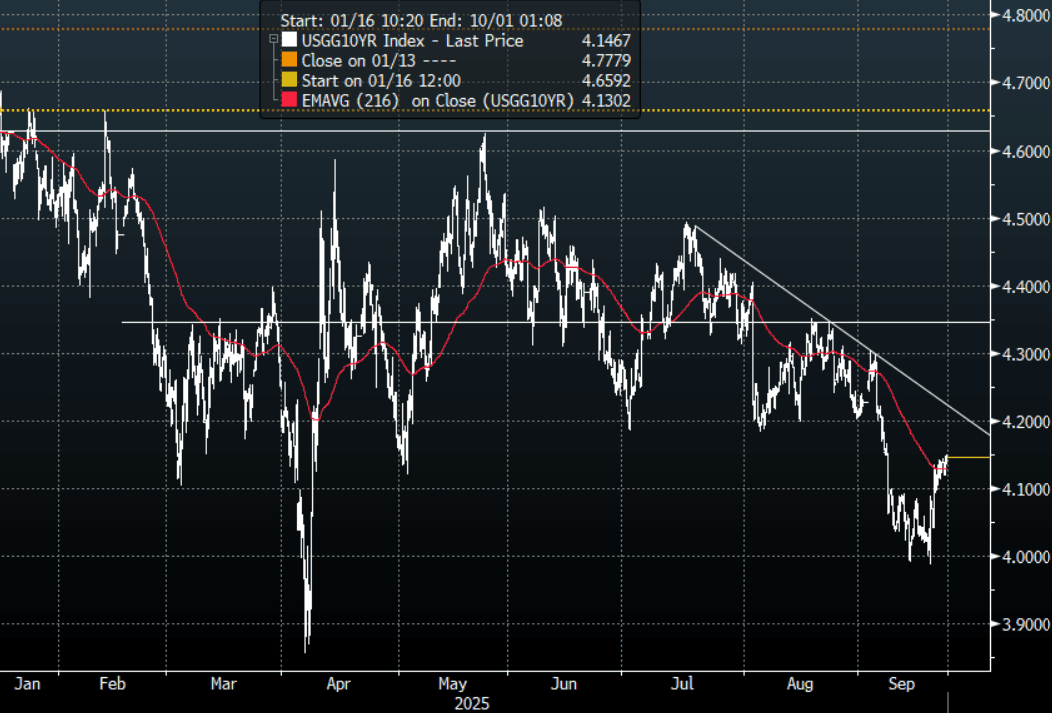

US TSYS: Futures Unchanged In A Quiet Session

The TYZ5 range has been 112-21+ to 112-24 during the Asia-Pacific session. It last changed hands at 112-22+, unchanged from the previous close.

- No cash market today.

- 10-Year Yields could not extend below 4.00% and have bounced as the Fed could not meet the markets very dovish expectations. The first buy-zone is now back towards the 4.20% area where I suspect demand should return initially. A sustained break through 4.00% is needed for the focus to then turn towards the 3.80% area.

- MNI BRIEF: Fed's Musalem Sees Limited Room For More Rate Cuts. The Federal Reserve was justified in cutting interest rates last week but still-elevated inflation and a higher neutral rate mean the central bank might not have room to reduce borrowing cuts much further, St. Louis Fed President Alberto Musalem said Monday.

- Robin Brooks on X: “Global yield curves are steepening, but the truth is that they're still inordinately flat in the big picture. The US yield curve is a case in point. 5y5y forward Treasury yield used to be a full 3 percentage points above 5y yield. We're going back to that.”

- "DIMON SAYS TRUMP ADMIN HAS NOT ATTACKED THE DEFICIT YET, ,SAYS HARD FOR FED TO CUT IF INFLATION DOESN'T GO AWAY : CNBC.” - BBG

- Data/Events: Philadelphia Fed Non-Manufacturing Activity, Current Account Balance, S&P Global US PMI’s, Richmond Fed Manufact. Index

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

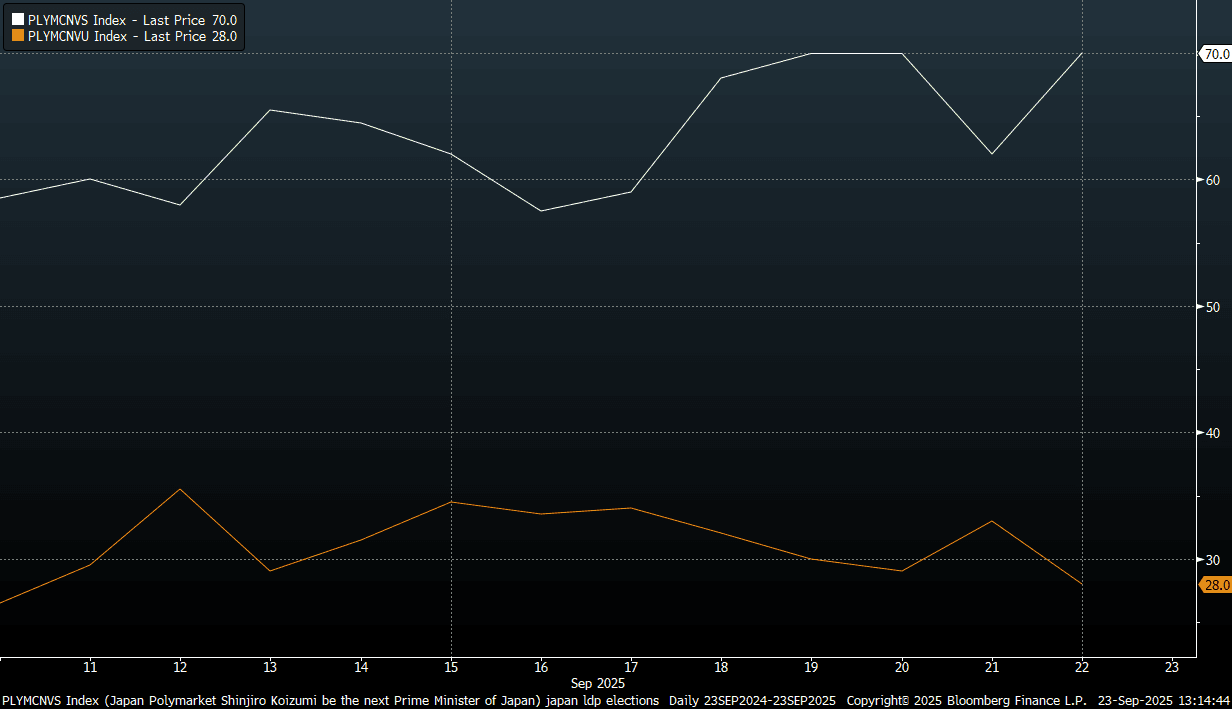

JAPAN: Koziumi Still Seen As Favorite For LDP Leadership Race

Earlier headlines crossed from Japan LDP leadership candidates. Notably from Takaichi we got, via Rtrs, :"JAPANESE PM CONTENDER TAKAICHI: WILL USE TAX REVENUES TO FUND TAX CUT, SPENDING FOR STEPS TO COMBAT RISING PRICES BUT IF NECESSARY, SHOULD ISSUE BONDS.

- This fits with Takaichi's known fiscal expansion viewpoint. Still, she sits well down per Polymarket odds, last around 28, off recent highs.

- Koizumi continues to lead, last at highs of 70 (since the LDP election was called a few weeks ago), see the chart below (Koizumi odds are the white line, Takaichi the orange line). Still, Takaichi remains the top pick among onshore opinions.

- Koizumi noted earlier: KOIZUMI: MUST BE MINDFUL OF NEED FOR FISCAL DISCIPLINE, BUT ACHIEVING SOLID ECONOMIC GROWTH IS BASIS FOR GUIDING SOUND FISCAL POLICY - [RTRS]"

- His remarks are more in line with a status quo fiscal outcome, although changes can't be ruled out.

- The JGBs 2/30s curve has flattened of late, last +225bps, we were around +245bps in early September. Nevertheless, the 2/30 curve remains near its steepest since 2005.

- The LDP election is scheduled for Oct 4.

Fig 1: Koizumi Clear Front Runner For LDP Leadership Race - Per Polymarket

Source: Polymarket/Bloomberg Finance L.P./MNI

AUSSIE BONDS: Little Changed, August CPI Tomorrow

ACGBs (YM -1.0 & XM -0.5) are modestly weaker on a data-light session.

- There was no cash US tsy trading in today's Asia-Pac session, with Japan closed for a holiday.

- Cash ACGBs are 2bps cheaper.

- The bills strip is -1 to -2 across contracts.

- RBA-dated OIS pricing is giving a 25bp rate cut in September a 4% probability, with a cumulative 25bps of easing priced by year-end (based on an effective cash rate of 3.60%).

- The AOFM plans to sell A$1000mn of the 3.00%21 November 2033 bond on Wednesday and A$900mn of the 2.75% 21 November 2029 bond on Friday.

- Tomorrow, the local calendar will see August CPI data.

- (Bloomberg Economics) “Australia’s August CPI report is likely to show inflation holding firm near the top of the Reserve Bank of Australia’s 2%-3% target band. We estimate annual CPI growth stayed at 2.8%, unchanged from July. The annual electricity price increase boosted the July reading, but this will be partially unwound by the federal government’s subsidy in August.”

BONDS: NZGBS: Closed Modestly Richer After A Subdued Session

NZGBs closed 1-2bps richer after a subdued data-light session.

- There was no cash US tsy trading in today’s Asia-Pac session, with Japan closed for a holiday.

- Swap rates closed 1-2bps lower.

- Headlines have crossed from BBG that the new RBNZ Governor could be announced tomorrow. BBG note: "New Zealand is set to appoint a woman to head its central bank for the first time as it seeks to refresh an institution damaged by leadership turmoil.", while also noting the new Governor was expected to come from offshore (i.e. was not a New Zealander).

- “New Zealand is making it easier for migrant workers to come and live in the country, in its latest attempt to bolster the workforce and economy. Announcing two new residency pathways, the minister for economic growth, Nicola Willis, on Tuesday said skilled and experienced migrants could help plug gaps in the workforce.” (per Guardian)

- RBNZ dated OIS pricing closed little changed across meetings. 32bps of easing is priced for October, with a cumulative 58bps by November 2025.

- The local calendar will be empty until Friday's Consumer Confidence data.

- On Thursday, the NZ Treasury plans to sell NZ$250mn of the 4.50% May-30 bond and NZ$200mn of the 3.50% Apr-33 bond.

RBNZ: New Governor May Be Announced Tomorrow - per BBG

Headlines have crossed from BBG that the new RBNZ Governor could be announced tomorrow. BBG note: "New Zealand is set to appoint a woman to head its central bank for the first time as it seeks to refresh an institution damaged by leadership turmoil.", while also noting the new Governor was expected to come from offshore (i.e. was not a New Zealander).

- The appointment comes at a time after recent upheaval for the RBNZ. Governor Orr left the post abruptly in March, while Chair of RBNZ board, Neil Quiqley also left recently.

- Last week's Q2 GDP data was weaker than market and RBNZ forecasts, driving further easing expectations in terms of the market outlook. Current market pricing has roughly 60bps of further easing priced by the Nov meeting (with the current rate at 3.00%). The trough point for rates is seen just under 2.30% in 2026. NZD has underperformed in the wake of these shifts.

- So the new Governor is likely to be scrutinized around the OCR outlook and whether more needs to be done to ensure to boost recovery prospects.

- BBG adds: "The new governor won’t be in place for the next rate decision on Oct. 8, with their term expected to start toward the end of the year."

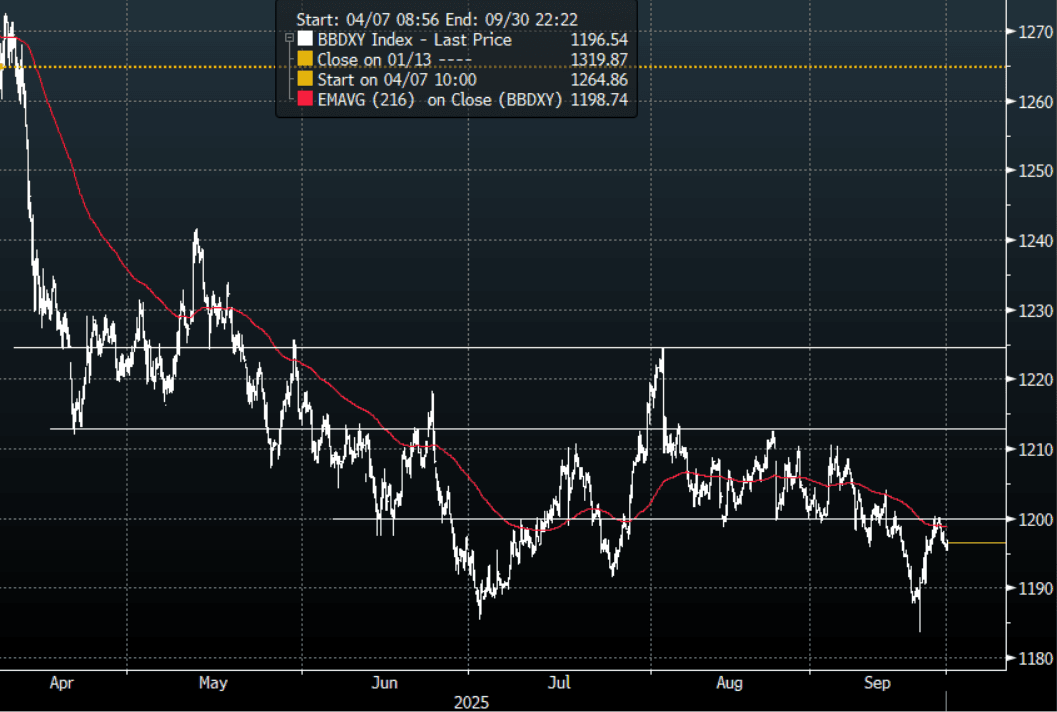

FOREX: Asia FX Wrap - The BBDXY Stalls Above 1200

The BBDXY has had a range of 1195.21 - 1196.90 in the Asia-Pac session; it is currently trading around 1196, +0.05%. The USD stalled just above 1200 for the second time and drifted lower in the overnight session. Price action stood out in that we had some clearly hawkish Fed speak relative to market expectations which the USD completely ignored. Was that the extent of the bounce ? If so, it's a pretty poor effort or does the market start to eventually listen. Should the market stay below 1200 then the focus will again turn back to the pivotal support back towards the 1180 area.

- EUR/USD - Asian range 1.1793 - 1.1820, Asia is currently trading 1.1800. The pair found some demand back towards 1.1700 and is looking to regain momentum higher.

- GBP/USD - Asian range 1.3502 - 1.3527, Asia is currently dealing around 1.3510. The pair rejected the break higher and has moved back into the middle of its recent range. No clear direction for the moment as it consolidates around 1.3500.

- USD/CNH - Asian range 7.1131 - 7.1181, the USD/CNY fix printed 7.1057, Asia is currently dealing around 7.1160. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX -0.10%, Gold $3745, US 10-Year 4.147%, BBDXY 1196, Crude Oil $61.98

- Data/Events : EZ HCOB PMI’s, France HCOB PMI’s, Germany HCOB PMI’s, Spain Trade Balance

Fig 1: BBDXY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

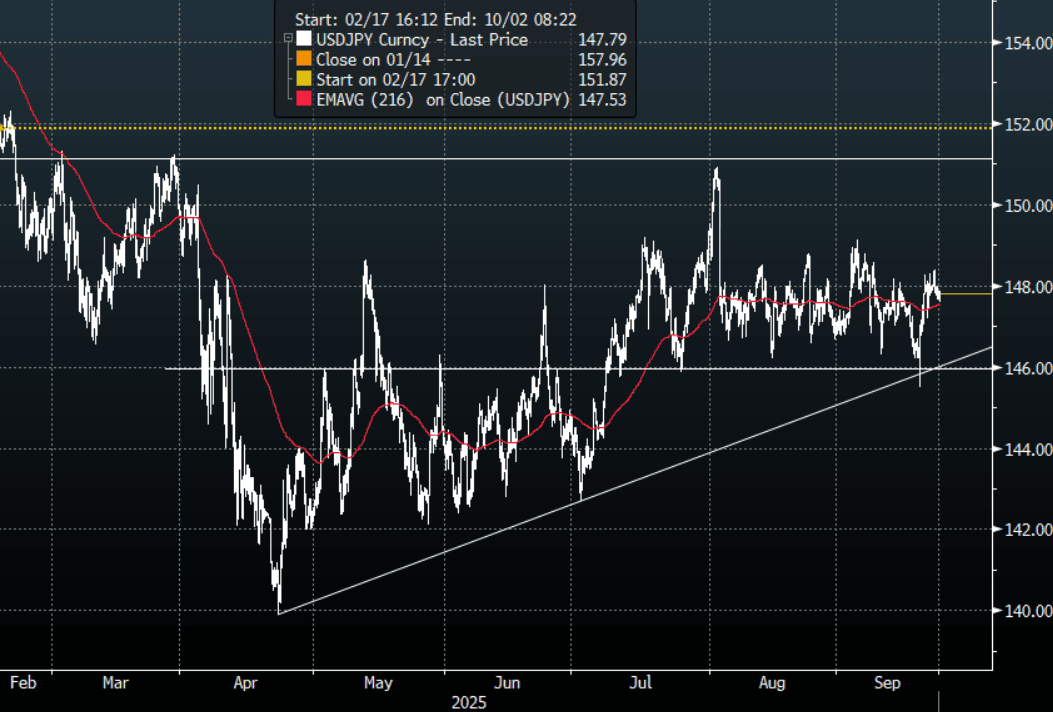

JPY: Asia Wrap - USD/JPY Trades Sideways After Stalling Above 148.00

The USD/JPY range has been 147.60 - 147.87 in the Asia-Pac session, it is currently trading around 147.80, +0.05%. USD/JPY stalled above 148.00 overnight and continues to chop around sideways without really going anywhere. The USD retracement stalled as sellers reemerged even with some clearly hawkish rhetoric from Fed speakers overnight. The price is still in the middle of its recent 146-149 range, and we need a convincing break on either side to see some clearer direction again. Neither the FOMC nor the BOJ were able to provide any clarity, the market will start turning its focus towards payrolls which seems a lifetime away.

- Bloomberg - “Deutsche Bank Says Dollar to Extend Drop Against Yen This Year. George Saravelos, head of FX research anticipates more weakness for the dollar, predicting that it will fall below 140 yen by year-end. Says the need to address inflation in Japan is growing. BOJ rate hikes at a time when the Fed is cutting should support the yen, he says. “Starting from a very undervalued position, the yen has a long runway provided the political pieces fall into place following the upcoming LDP election”

- Koizumi Still Seen As Favorite For LDP Leadership Race : Koizumi continues to lead, last at highs of 70 (since the LDP election was called a few weeks ago). Koizumi noted earlier today: “MUST BE MINDFUL OF NEED FOR FISCAL DISCIPLINE, BUT ACHIEVING SOLID ECONOMIC GROWTH IS BASIS FOR GUIDING SOUND FISCAL POLICY” - RTRS

- "JAPANESE PM CONTENDER TAKAICHI: WILL USE TAX REVENUES TO FUND TAX CUT, SPENDING FOR STEPS TO COMBAT RISING PRICES BUT IF NECESSARY, SHOULD ISSUE BONDS.” - RTRS

- Options : Close significant option expiries for NY cut, based on DTCC data: 145.00($856m), 145.50($750m), 146.00($476m). Upcoming Close Strikes : 145.00($1.52b Sept 24), 152.00($1.67b Sept 26) - BBG.

- CFTC data shows last week asset managers reduced their JPY longs slightly +71162( Last +87239), leveraged funds again used the dip to add their short position believing the support will continue to hold -58811(Last -49951).

Fig 1 : USD/JPY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

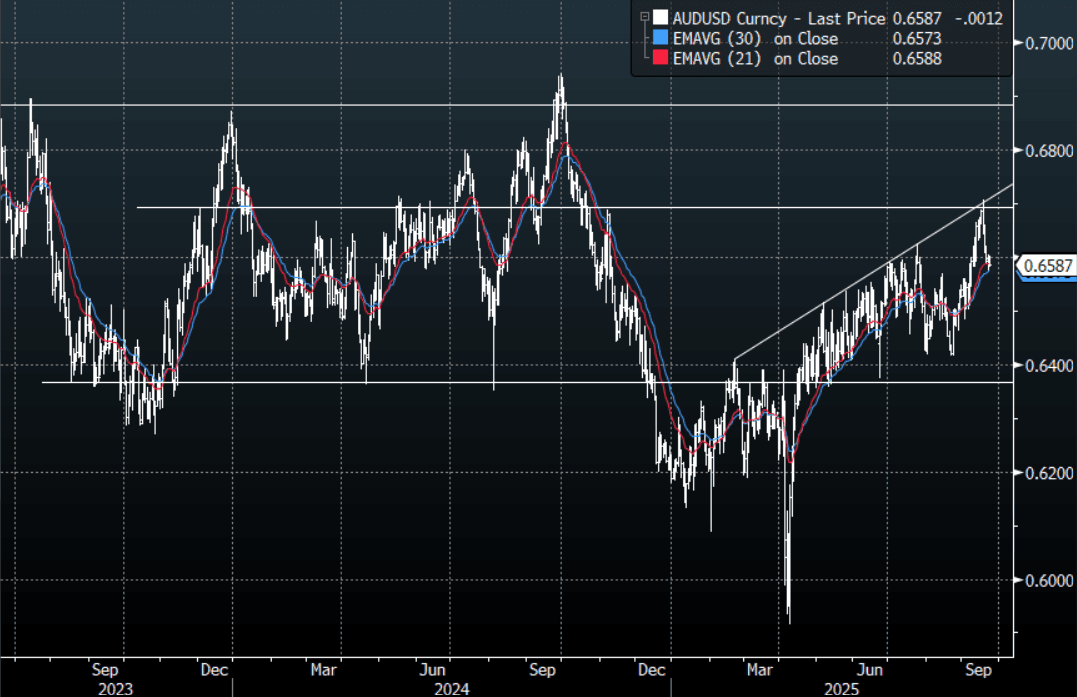

AUD: Asia Wrap - AUD/USD Drifts Lower, Erases Overnight Gains

The AUD/USD has had a range of 0.6581 - 0.6604 in the Asia- Pac session, it is currently trading around 0.6585, -0.20%. The AUD has drifted lower in Asia giving back most of its overnight gains. The USD retracement stalled yesterday as sellers reemerged even with some clearly hawkish rhetoric from Fed speakers overnight. The AUD/USD continues to do some work around 0.6600 and should still see dips supported for now with the first buy-zone back towards the 0.6500/0.6550 area.

- Bloomberg - “Morgan Stanley Says Sell Dollar Versus Aussie and Loonie. The Federal Reserve’s perceived emphasis on the job market at the expense of inflation will see the US dollar’s decline widening, according to Morgan Stanley strategists who now recommend selling the greenback versus the Canadian and Australian dollars.”

- September PMIs Off Recent Highs, But Q3 Average Higher : Australian preliminary PMIs for September fell from their August levels. The manufacturing print came in at 51.6, from 53.0, while services were at 52.0 from 55.8 in August (see the chart below). This saw the composite PMI come in at 52.1 from 55.5.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6530(AUD415m), 0.6650(AUD908m), 0.6680(AUD486m). Upcoming Close Strikes : 0.6450(AUD529m Sept 24), 0.6600(AUD703m Sept 24), 0.6720(AUD791m Sept 24) - BBG

- CFTC Data last week shows Asset managers started to significantly reduce their shorts, -41095(Last -68333). The Leveraged community has pulled back their shorts to be almost flat, -1519(Last -5081).

- AUD/JPY - Asia-Pac range 97.25 - 97.56, Asia is trading around 97.35.The pair has stalled towards 98.50, dips back towards 96.50/97.00 should be expected to be supported now first up.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

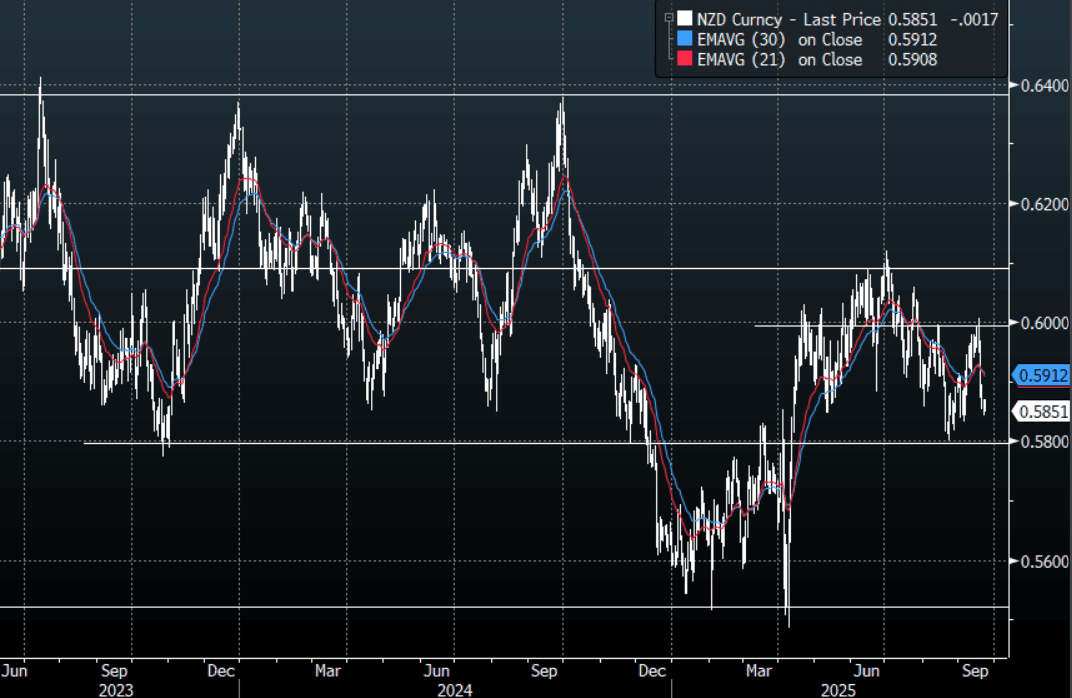

NZD: Asia Wrap - NZD/USD Trades Heavy, Gives Back All The Overnight Gains

The NZD/USD had a range of 0.5849 - 0.5870 in the Asia-Pac session, going into the London open trading around 0.5850, -0.30%. The NZD has drifted lower in Asia giving back most of its overnight gains. The USD retracement stalled overnight as sellers reemerged even with some clearly hawkish rhetoric from Fed speakers overnight. The NZD underperformance got a real nudge from the poor GDP data last week. The initial move lower seems to be stalling for now but I suspect sellers would remerge should the Kiwi bounce back towards the 0.5925/50 area. The 0.5800 is important support, I suspect we will see buyers towards this area initially but a sustained break through there would turn the focus back towards the 0.5500 lows.

- Bloomberg - “New Zealand is set to name a foreigner to head the RBNZ, a person familiar said. Bank of New Zealand said there is a growing likelihood it’s BOE deputy governor Sarah Breeden.”

- “RBNZ Watchers to Assess If New Governor Is Technocrat: CA-CIB. “A key question would be whether the new governor would be a technocrat who focuses on delivering on the RBNZ’s inflation mandate or someone who works more closely with the government to prop up the economy.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5900(NZD372m Sept 24) - BBG

- CFTC Data of last week shows Asset Managers beginning to rebuild their short positions in the NZD, -11933(Last -3121). The Leveraged community is doing the same as it looks to rebuild its own shorts, -5327(Last -1874). Positioning shows the market is again turning bearish on the NZD..

- AUD/NZD range for the session has been 1.1240 - 1.1260, currently trading 1.1255. The Cross has broken above the multiple highs towards the 1.1200 area and is looking to accelerate higher on the back of some very poor NZ Q2 GDP data last week. Dips should now continue to be supported as the market turns its focus towards the 1.1400/1.1500 area.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: China Stocks Decline Following No Announcements

A press conference Monday by Chinese financial regulators — including the PBOC governor and banking and stock market supervisors — drew attention from investors as it is about one year ago when a similar meeting saw a broad package of policy easing measures including RRR and interest rate cuts announced. With no such announcements forthcoming, China's equity bourses are all down today whilst other regional bourses delivered gains.

- The Hang Seng fell yesterday on BYD news and is lower again today by -0.96%. The CSI 300 is down -1.19%, the Shanghai Comp down -1.23% and the Shenzhen Comp down -2.27% .

- The KOSPI is up +0.51% today as Samsung makes new all time highs.

- The TAIEX in Taiwan is up strongly by +1.1% reaching another new high for the index.

- The FTSE Malay KLCI remains stuck at present and is where it started the day at 1,603.

- The Jakarta Comp is hitting new highs of 8,087 today, to be up +0.55%.

- The FTSE Straits Times is up +0.36% and the PSEi in the Philippines +0.30%.

- The NIFTY 50 is lower by -0.23% and continues to underperform regional peers, down for a third successive day.

ASIA STOCKS: Mixed Inflow Trends, Taiwan Sees Outflows Despite Tech Led Gains

Yesterday saw a mixed start to the week from an offshore equity flow standpoint. South Korea inflow momentum was positive, albeit still down from some of the larger inflow days seen in September. The Kospi rose, aided by Samsung shares, which gained post positive chip testing news from Nvidia. Overnight we saw the positive tech equity trend continue, with both the SOX and MSCI IT indices gaining strongly. Nvidia's announcement of investment into OPEN AI helped fuel further gains. So far today, the Kospi is up a further 0.40%.

- In contrast, Taiwan saw modest net outflows. This came despite a further gain in local stocks yesterday (the Taiex up a further 1.18% to fresh cycle highs). As we have noted, given very strong inflows into Taiwan for September to date, we may be seeing some consolidation as the end of month (also quarter end) approaches.

- Elsewhere, Indian inflows were modestly positive into the end of last week. Indian benchmark stock indices are off recent highs but still comfortably up for September to date.

- Indonesia continued to see positive inflow momentum on Monday, but slightly down from the pace seen at the end of last week. Thailand outflow pressures continued though, bringing outflows in the past 5 trading days to over $200mn.

Table 1: Asian Market Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 377 | 1552 | -600 |

| Taiwan (USDmn) | -101 | 692 | 8241 |

| India (USDmn)* | 128 | 334 | -15075 |

| Indonesia (USDmn) | 30 | 148 | -3516 |

| Thailand (USDmn) | -53 | -221 | -2764 |

| Malaysia (USDmn) | -4 | 168 | -3639 |

| Philippines (USDmn) | -6 | 9 | -727 |

| Total (USDmn) | 371 | 2682 | -18080 |

| * Data Up To Sep 19 |

Source: Bloomberg Finance L.P./MNI

COMMODITIES: Oil Gives Back Monday Gains as Gold Steadies

- Oil had posted reasonable gains in the Asia trading day, only to give them back and finish marginally down by the US close.

- Europe's focus on Russian oil flows is creating uncertainty for markets as new sanctions come into place, targeting Indian and Chinese buyers of Russian oil.

- Investors were left to try to assess the impact of Ukraine strikes on Russian oil infrastructure, a move likely to interrupt supply.

- Since the announcement of further supply by OPEC+ it has dampened volatility in oil markets with both WTI and Brent trading in narrow ranges.

- Iraq has announced that they have finally struck a deal with Kurdistan to resume oil exports with as much as 200,000 bbl / day potentially hitting the market, having had exports halted for over pay disputes, stopping shipments for nearly two years.

- WTI finished the US trading session down -0.06% at US$62.14, having been as high as $63.18 earlier.

- Brent closed lower by -0.16% at $66.57 and maintains its position below all major moving averages.

- Gold finished the US trading day, just off recent highs at US$3,741.85, a fall of -0.13%.

- Gold is buoyed by the cut in US rates and is having one of the strongest months of the year, up over 8% already.

- Gold closed Monday at new highs of US$3,746.70, having ended 2024 at $2,624.50.

- The bullish momentum is evident with all major moving averages upward sloping as gold remains above them all.

- Flows into golf ETFs remains strong with investors chasing the tail of strong performance and potentially betting on further rate cuts.

- Zijin Gold International Co's IPO next week in Hong Kong is at risk as the Super Typhoon Ragasa approaches, threatening to close all markets.

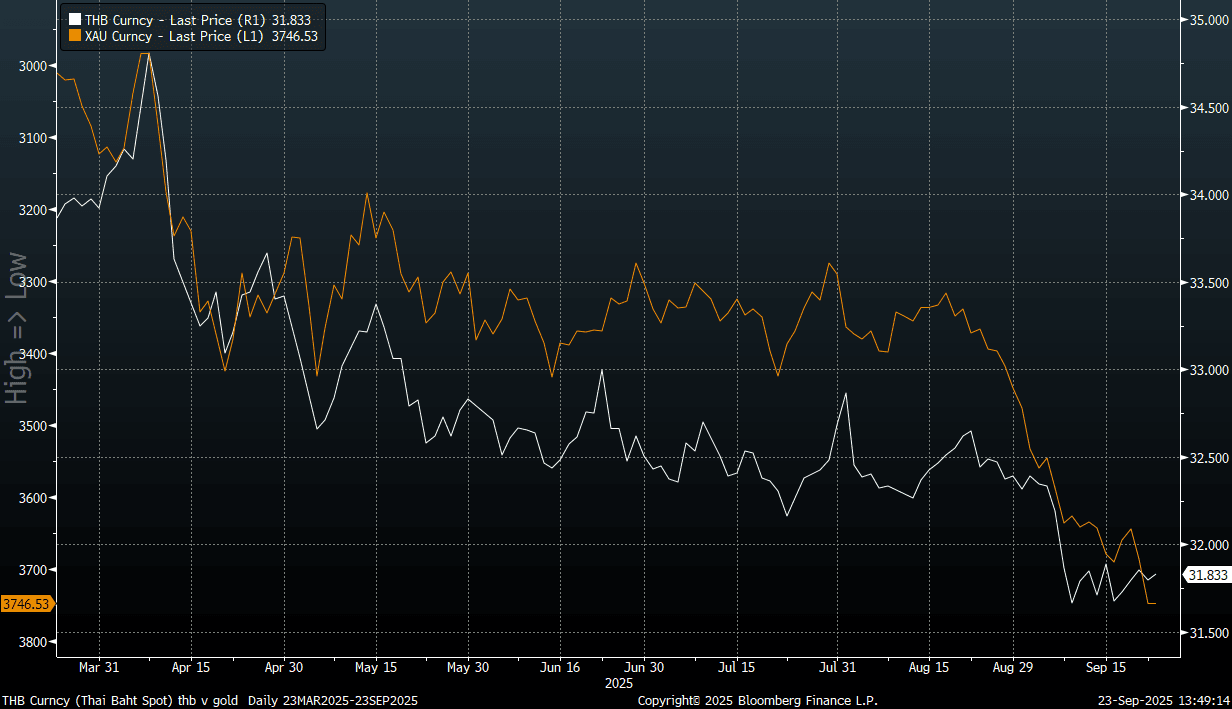

THB: USD/THB Holding Recent Ranges, Lags Gold, Govt To Support Growth

USD/THB tracks within recent ranges, the pair last near 31.80/85, up around 0.10% on end Monday levels. This is slightly lagging softer USD index levels, but only marginally. USD/THB also remains off recent highs close to 31.97.

- THB hasn't followed gold higher. The chart below shows a modest wedge between USD/THB and spot gold prices (which are inverted on the chart). This suggests some success from the authorities, as the verbal jawboning around stronger baht levels, diverging from fundamentals, has certainly picked under the new Anutin government.

- Headlines crossed a short while ago from BBG that the government will move to stabilize baht, although it didn't appear to be provide any fresh insights into what new measures may be undertaken.

- The BBG article did note steps will be taken to boost growth: "A policy announcement to parliament has been tentatively slated for Oct. 1 and Oct. 2. Siripong said the government will outline plans to cut living costs, including by reviving a co-payment program and reducing energy and transport costs." (via BBG).

- Data on Aug auto manufacturing showed it was down 6.11%y/y, while local auto sales rose 5.38%y/y, but the level still fell to +47.6k in the month, from 49.1k in July. This still points to the need for domestic economic support.

- Note tomorrow we get Aug customs trade figures.

Fig 1: USD/THB & Spot Gold Prices (inverted)

Source: Bloomberg Finance L.P./MNI

IDR: USD/IDR Near Monday Highs, Supported Under 16600, CDS Climbs

Spot USD/IDR sits at 16630, up around 0.15% from end Monday levels. We are close to Monday intra-session highs of 16640. We did see intervention headlines cross yesterday after BI Governor Wariyo appeared before parliament. He noted the central bank will keep stabilizing the rupiah amid uncertainty and that the currency will have tendency to strengthen going forward.

- Given we are close to Monday's highs, intervention risks are likely to remain. Pull backs yesterday got to around the 16580 level.

- Higher US yields from Monday, with the real 10yr yield rising to +178bps is helping keep USD/IDR dips supported (although firmer US yields didn't see the majors move lower against the USD on Monday).

- Elsewhere in the cross asset space, local equities remain supported, although offshore investor inflows have slowed from a momentum standpoint. Bond inflows remain negative towards the tail end of last week.

- We also continue to see 5yr CDS track higher, last around +80bps, close to fresh highs since late June.

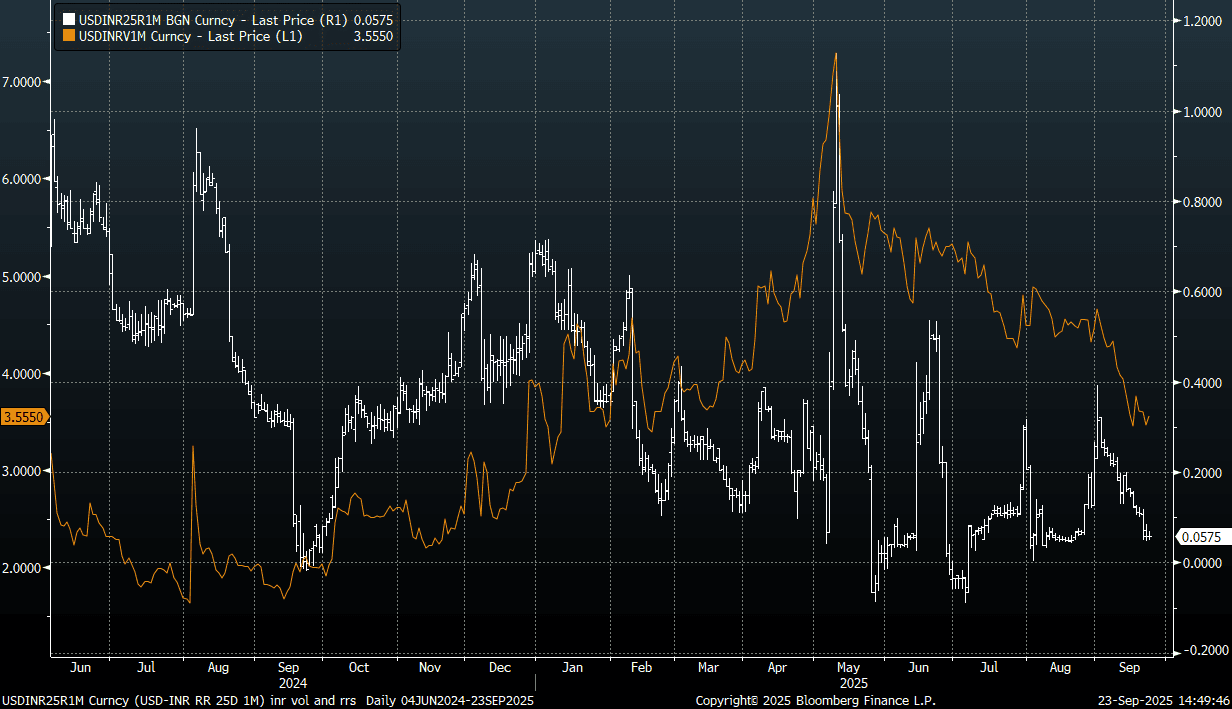

INR: USD/INR Spot To Record Highs, Implied Vol Well Behaved

USD/INR has broken to fresh record highs, last in the 88.55/60 region (up +0.30% for the session). Close to a week ago we were sub 87.00 but dips in the pair have been well supported, as we are yet to see meaningful progress on tariffs, while remittances back into India are seen at risk from the new Trump administration's new visa regulations.

- Headlines crossed earlier from Rtrs that the central bank was likely sell USDs via state banks to curb the USD/INR's rise. This is not surprising as the central bank is likely to manage the pace of depreciation. Without tariff relief the bias in USD/INR is likely to gravitate higher.

- The chart below plots the 1 month USD/INR implied vol and risk reversal levels, which remain well behaved despite this break highs in spot (which again speaks to confidence in the RBI to manage FX trends).

- In a worse case scenario J.P. Morgan sees annual remittances falling by $400mn under the new B-1B visa regulations (via BBG).

- Coming up shortly we have PMI prints.

Fig 1: USD/INR 1 month Implied Vol & Risk Reversal

Source: Bloomberg Finance L.P./MNI

MALAYSIA: Country Wrap: CPI Steady in August

Market Summary: The FTSE Malay KLCI remains stuck at present and is where it started the day at 1,603, whilst the Ringgit was one of the few regional currencies with minor gains of +0.03% to reach 4.1980, below key resistance. Bonds are weak with the MGS 10-Yr yield up at 3.44%

- Malaysia's CPI for August was marginally up at +1.3%, versus +1.2% in July. Core inflation rose +2.0% YoY, Housing +1.2% YoY and some services showing very modest increases. According to the BNM: Inflation Likely To Trend At Manageable Level Of 2.0-3.5 Percent In 2025 compared to an average of 1.8 per cent in 2024. The BNM does not meet again until November 6th. There is very little priced into the MGS curve in terms of rate cuts, only -10bps over the next 12 months. (source MNI)

- Malaysia's targeted RON95 fuel subsidy (Budi95), which will come into effect on Sept 30, is expected to keep car demand steady and delay any major shift towards electric vehicles (EVs), according to research houses (source The Edge)

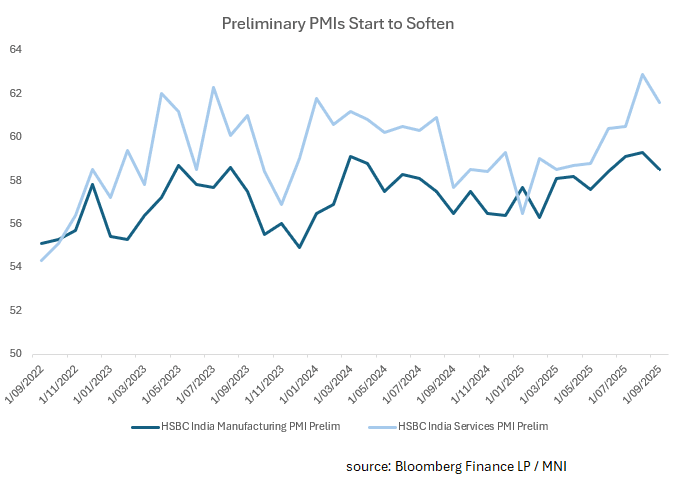

INDIA: Preliminary PMIs Show First Sign of Moderating

- PMIs in India have been seemingly bullet proof, despite the threat of US tariffs hanging over that economy.

- Outperforming regional peers, PMI Manufacturing and Services had reached new highs in August.

- However the preliminary September results have showed the first signs of weakness, coming off from August's highs.

- PMI Manufacturing (prelim) came in at 58.5, from 59.3 prior.

- PMI Services (prelim) came in at 61.6, from 62.9.

- In context these PMIs remain much higher than regional peers and the softening does not ring any alarm bells.

- Nevertheless, the tariff threat remains, particularly following India's continued purchase of Russian oil and these results could represent the beginning of a period of moderating data.

INDONESIA: Country Wrap: FinMin's 5 Priority Strategies

Market Summary: The Jakarta Comp is hitting new highs of 8,087 today, to be up +0.55% whilst the Rupiah falls again by -0.25% to 16,653. Bonds are weak with yields +1-2bps higher. The 10-Yr is at 6.34%

- Finance Minister Purbaya has outlined five priority strategies under a “quick win” program to accelerate economic growth and lift state revenue, which remains under pressure. The measures include a targeted stimulus package, tighter enforcement against major tax delinquents, improved law enforcement coordination, IT system upgrades, and a crackdown on illegal cigarettes. (source Jakarta Globe)

- Indonesia is working on non-fiscal incentives to offset the impact of the global minimum tax or GMT so the country remains attractive to foreign investors. Southeast Asia’s biggest economy has implemented an internationally agreed-upon minimum corporate tax of 15 percent for large corporations as stated by an accord backed by at least 130 countries. The policy aims to prevent big companies from shifting profits and tax revenues to low-tax economies, while also ending the race to the bottom in corporate taxation. The tax applies to multinationals with consolidated global revenues of at least 750 million euros ($885 million). (source Jakarta Globe)

INDIA: Country Wrap: Preliminary PMIs Show First Sign of Moderating

Market Summary: The NIFTY 50 is lower by -0.23% and continues to underperform regional peers, down for a third successive day as the Rupee weakens to new lows of 88.61 whilst bonds drift higher in yield with the 10-Yr at 6.49%

- PMIs in India have been seemingly bullet proof, despite the threat of US tariffs hanging over that economy. Outperforming regional peers, PMI Manufacturing and Services had reached new highs in August. However the preliminary September results have showed the first signs of weakness, coming off from August's highs. PMI Manufacturing (prelim) came in at 58.5, from 59.3 prior. PMI Services (prelim) came in at 61.6, from 62.9. In context these PMIs remain much higher than regional peers and the softening does not ring any alarm bells. Nevertheless, the tariff threat remains, particularly following India's continued purchase of Russian oil and these results could represent the beginning of a period of moderating data. (source MNI)

- A lower inflation print and strong economic growth have led to a majority of economists proposing a pause on policy rates at a consultative meeting held by the Reserve Bank of India governor on Monday and Friday. The RBI regularly holds consultative meetings with economists and market participants to gauge their views on growth and inflation. Another such meeting with market participants like mutual fund managers and treasury heads of banks will be held on Wednesday, said people with knowledge of the matter. (source Econ Times)

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 23/09/2025 | 0715/0915 | ** | S&P Global Services PMI (p) | |

| 23/09/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 23/09/2025 | 0730/0930 | *** | Riksbank Interest Rate Decison | |

| 23/09/2025 | 0730/0930 | ** | S&P Global Services PMI (p) | |

| 23/09/2025 | 0730/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 23/09/2025 | 0800/1000 | ** | S&P Global Services PMI (p) | |

| 23/09/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 23/09/2025 | 0800/1000 | ** | S&P Global Composite PMI (p) | |

| 23/09/2025 | 0830/0930 | *** | S&P Global Manufacturing PMI flash | |

| 23/09/2025 | 0830/0930 | *** | S&P Global Services PMI flash | |

| 23/09/2025 | 0830/0930 | *** | S&P Global Composite PMI flash | |

| 23/09/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 23/09/2025 | 0900/1000 | BOE Pill Fireside Chat At Pictet Research Institute Symposium | ||

| 23/09/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 23/09/2025 | 1230/0830 | * | Current Account Balance | |

| 23/09/2025 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 23/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 23/09/2025 | 1300/0900 | Fed Governor Michelle Bowman | ||

| 23/09/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 23/09/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 23/09/2025 | 1400/1000 | ** | Richmond Fed Survey | |

| 23/09/2025 | 1400/1000 | *** | NAR existing home sales | |

| 23/09/2025 | 1400/1000 | Atlanta Fed's Raphael Bostic | ||

| 23/09/2025 | 1420/1620 | ECB Cipollone In Bloomberg Fireside Chat | ||

| 23/09/2025 | 1635/1235 | Fed Chair Jay Powell | ||

| 23/09/2025 | 1700/1300 | * | US Treasury Auction Result for 2 Year Note | |

| 23/09/2025 | 1815/1415 | BOC Governor Macklem speech in Saskatoon | ||

| 24/09/2025 | 2301/0001 | * | Brightmine pay deals for whole economy | |

| 24/09/2025 | 0030/0930 | ** | Jibun Bank Flash Japan PMI | |

| 24/09/2025 | 0130/1130 | *** | CPI Inflation Monthly | |

| 24/09/2025 | 0600/1400 | ** | MNI China Money Market Index (MMI) | |

| 24/09/2025 | 0700/0900 | ** | Economic Tendency Indicator | |

| 24/09/2025 | 0700/0900 | ** | PPI | |

| 24/09/2025 | 0800/1000 | *** | IFO Business Climate Index | |

| 24/09/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 24/09/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 24/09/2025 | 1300/1500 | ** | BNB Business Confidence |