MNI EUROPEAN MARKETS ANALYSIS: BoJ Oct Hike Odds Around 25%

- Japan's parliament has elected a new PM, with LDP leader Takaichi confirmed today (which from late last week was largely expected by the market). USD/JPY is pushing higher (with BoJ hike odds around 25% for Oct). The expected new FinMin did comment on yen being undervalued in a March interview from earlier this year.

- Risk appetite has been supportive for Asia Pac equities, although US futures sit off earlier highs. The USD is up against all the majors. It has been a quiet session for US Tsy yields.

- Later US October Philly Fed non-manufacturing and September Canadian CPI print. ECB President Lagarde and Board member Lane speak.

MARKETS

US TSYS: Treasuries Trend Sideways in Lacklustre Trading Day

Having finished the overnight US session modestly higher, US Treasury futures failed to follow on with TYZ5 remaining where it opened at 113-19 and USTs moves modest at best.

- The US 2-Yr did very little during the Asian trading day, trending marginally higher to 3.46%

- The US 5-Yr had finished -2bps lower at 3.57% during the US trading day where it remained.

- The US 10-Yr slipped back below the 4.00% overnight, finishing at 3.98% where it has held during the day today with eyes on it overnight to see if it can consolidate below 4.00%.

- The USD 30-Yr was strong overnight rallying 3bps to 4.57%, and continued on in Asia down again to 4.56% The 30-Yr is now back at levels of April.

The key data releases tonight are the Philadelphia Fed Non-Manufacturing Activity, Redbook retail sales and MBA Mortgage Applications.

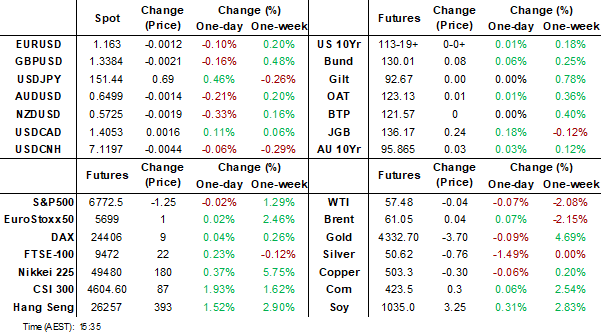

JGBS: Modestly Richer, Oct 30 BOJ Hike At 25% Chance

JGB futures are stronger, +16 compared to the settlement levels, but off session bests.

- Cash US tsys are slightly mixed, with a flattening bias, in today’s Asia-Pac session after yesterday's gains.

- Cash JGBs are slightly richer across benchmarks, with yields 1-2bps lower. The benchmark 10-year yield is 1.0bp lower at 1.664%, outperforming the futures-linked 7-year. This continued the recent trend, which has unwound the relative cheapening of the 10-year earlier in the year.

- Japan sold ¥300bn of 10-year climate transition notes at a cut-off yield that was lower than expectations, signalling lacklustre investor demand. The cut-off yield was 1.680%, compared with 1.695% estimated by traders in a Bloomberg survey. The bid-to-cover ratio was 3.56x, compared with 3.31x in October 2024, the last time the government sold the bonds.

- Swap rates are little changed.

- BOJ-dated OIS pricing is little changed across 2025 meetings compared to early August levels. Pricing is, however, firmer for 2026 meetings out to July. Current OIS pricing implies just a 24% probability of a 25bp hike in October, rising to 65% by December and 82% by January. A full 25bps hike is not fully priced until March 2026. (see chart)

- Tomorrow, the local calendar will see Trade Balance data.

Figure 1: BOJ-Dated OIS – Today Vs. August 1

Source: Bloomberg Finance LP / MNI

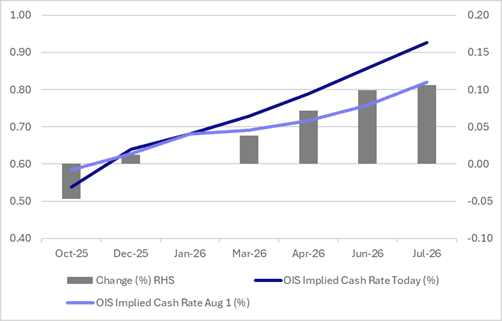

AUSTRALIA: Improved Q3 Job Ads May Signal Better Q4 Labour Market

SEEK data show that labour demand improved over Q3 while supply remains positive it slowed. With Q3 employment rising only 0.2% q/q down from Q2’s 0.6%, SEEK job ads may be signalling some possible improvement over Q4. A stabilisation of the labour market would be helpful for monetary policy decision makers if inflation prints to the upside.

Australia SEEK job ads %

- September SEEK new job ads rose 1.1% m/m, the third straight monthly increase. Ads increased 1.7% q/q in Q3 a clear pick up after Q2’s 0.6% q/q contraction. They are still down 2.4% y/y in September but that follows -12.6% y/y in March and is the best result in almost three years.

- Applicants per job were little changed in August rising 0.1% m/m and 10.9% y/y following July’s 2.8% m/m & 11.7% y/y. It seems that growth in labour supply slowed in Q3 after rising 4% q/q in Q2. In Q3, the labour force grew 1.8% y/y while employment was up 1.5% y/y.

- SEEK noted that a number of large industries had increased job ads including trades & services, manufacturing and transport & logistics. Professional and financial services continue to decline.

Australia SEEK applicants per job 2013=100

Source: MNI - Market News/SEEK

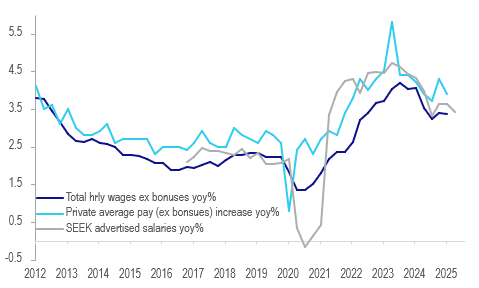

AUSTRALIA: SEEK Advertised Salaries Signal Slight Q3 Wage Slowdown

September SEEK advertised salaries rose 0.3% m/m to be up 3.5% y/y showing steady growth since around mid-year. They increased 0.8% q/q in Q3 to be up 3.4% y/y a slowing from Q2’s 0.9% q/q & 3.6% y/y despite the 3.5% minimum wage increase from July 1. Q3 WPI is released on 19 November and the RBA forecast 3.3% y/y for Q4 in August. The SEEK data suggest that Q3 wage inflation may have slowed slightly, which would be in line with the RBA projections and job growth not keeping up with the rise in the labour force. A positive for the consumption outlook though is that the rise in wages offered continues to exceed inflation.

Australia wage growth ex bonuses y/y%

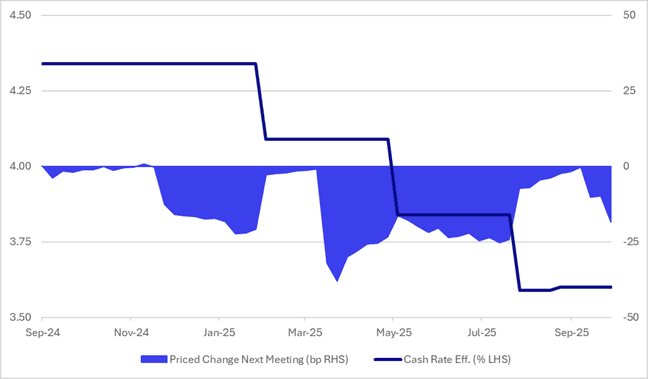

AUSSIE BONDS: Richer But Market Losing Its Conviction About Nov 4 Cut

ACGBs (YM +2.5 & XM +4.0) are stronger and at session highs on another data-light day. The local data calendar remains fairly quiet throughout the week.

- Cash US tsys are slightly mixed, with a flattening bias, in today’s Asia-Pac session.

- Cash ACGBs are 2bps richer with the AU-US 10-year yield differential at +13bps.

- Today’s ACGB auction of the Jun-54 bond showed strong demand, with the weighted average yield printing 0.92bps through prevailing mids and the cover ratio jumping to 4.0533x from 3.3500x from the previous auction. The strong demand came despite the bond’s outright yield being 20-25bps lower than the previous auction and around 30bps below the peak reached in May.

- The bills strip bull-flattened, with pricing flat to +2.

- Despite firming slightly in recent days, RBA-dated OIS pricing remains 7–13bps softer across meetings compared with pre-jobs data levels last week.

- A 25bp rate cut in November is now assigned a 68% probability (peak 80%, pre-data 38%), with a cumulative 23bps of easing (peak 25bps, pre-data 13bps) priced by year-end.

- Compared with the lead-up to previous cuts in this easing cycle, the market appears less certain than usual about a November 4 move.

Figure 1: RBA-Dated OIS – Cash Rate Vs. Priced Change Next Meeting

Source: Bloomberg Finance LP / MNI

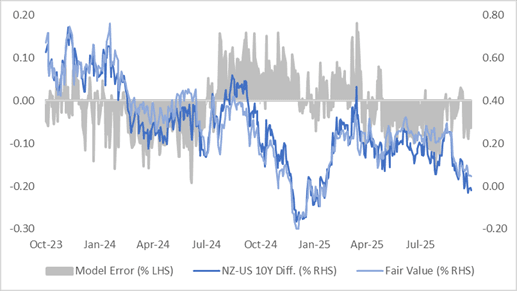

BONDS: NZGBS: Closed Richer, NZ-US 10Y Diff Rich Vs. FV

NZGBs closed at or near session highs, 4bps richer across benchmarks.

- The NZ-US 10-year yield differential is approximately -2bps. However, a simple regression of the 1Y3M forward swap spread against the 10-year yield differential over the past 18 months suggests the current differential is 6bps too low versus FV. (see chart)

- Export growth is a bright spot in the NZ economy, which was up 19% y/y in September after 21% y/y. The strength is being driven by higher dairy prices but also an increase in milk & cheese export volumes.

- Credit card spending in New Zealand decreased by 2.1% month on month to NZ$4.34 billion in September after a 2% increase in August, while credit card balances fell 0.1% to NZ$6.06 billion in September, following a 0.7% rise in the previous month. - MTN

- RBNZ dated OIS pricing closed little changed across meetings. 26bps of easing is priced for November, with a cumulative 36bps by February 2026.

- The local calendar will be empty until next Tuesday’s release of Filled Jobs data for September.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond, NZ$175mn of the 4.25% May-36 bond and NZ$50mn of the 5.00% May-54 bond.

Figure 1: NZ-US 10-Year Yield Differential

Source: Bloomberg Finance LP / MNI

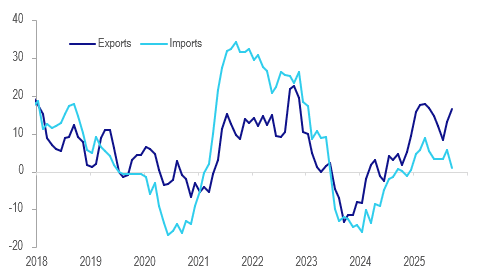

NEW ZEALAND: Export Growth Strong, Imports Reflect Soft Domestic Growth

Export growth is a bright spot in the NZ economy which was up 19% y/y in September after 21% y/y. The strength is being driven by higher dairy prices but also an increase in milk & cheese export volumes. Import growth remains lacklustre reflecting ongoing soft domestic demand. As a result the goods trade deficit in the year to September narrowed to $2.25bn from $3.06bn.

NZ goods exports vs imports y/y% 3-month moving average

Source: MNI - Market News/LSEG

- Statistics NZ reports that Q3 goods export values rose 3.6% q/q after Q2’s -3.4%, while imports fell 0.1% q/q after -0.6%, signalling ongoing domestic weakness in the quarter. Another rate cut is likely in November.

- The monthly merchandise trade deficit is trending higher again after posting surpluses over February to June. September’s deficit was $1.35bn after $1.23bn.

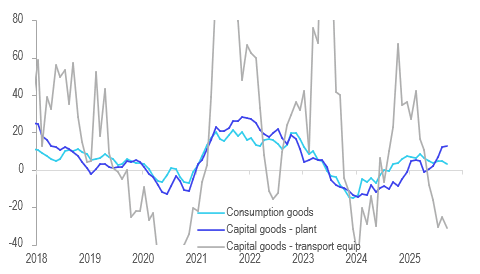

- Imports rose 1.6% y/y up from -1.0% y/y in August. The weakness has been driven by transport equipment which sank -46.1% y/y. Non-transport capital goods imports are strengthening rising 14.9% y/y in September. Consumer goods imports are recovering rising 7.4% y/y but the 3-month average growth rate is still only 3.3% y/y.

- Merchandise exports to NZ’s major destinations are growing strongly with shipments to China up 24.2% y/y driven by dairy and cereal products. They rose 10% y/y to the US due to fats/oils, pharmaceuticals and fruit. Exports to Australia are very strong up 27.7% y/y and are recovering to Japan rising 11.0% y/y 3-month average.

NZ merchandise imports y/y 3-month moving average

FOREX: USD Index Drifts Up, USD/JPY Higher As Takaichi Confirmed As PM

USD/JPY is testing higher as Japan's parliament confirmed that Takaichi will be the next PM. We sit around 151..35/40 in latest dealings, with dips back to 151.00 supported. The result will not have been a surprise to the market, as her election holds since last Friday were close to 100, per Polymarket. Focus will now shift to the policy outlook (with cost of living/fiscal outlook, along with BoJ the early focus points). Earlier, we had headlines that Satsuki Katayama will be appointed as the new FinMin in Japan, who argued in any interview earlier this year the yen was undervalued. This only provided a modest bounce in yen. Other Japan officials have also stated there is no desire to excessively weaken the yen. This, along with intervention risks, may help cap the upside in the pair (outside of broader USD/yield moves). More meaningful resistance is likely in the 152/153 region, while the bull trigger is at 153.27. On the downside, the 50-day EMA is back near 149.00.

- The USD is drifting higher elsewhere as well, although aggregate moves are modest at this stage, with mixed crossed asset trends. The equity backdrop remains supportive, with US equity futures ticking up, while regional Asia Pac markets post strong gains led by the tech side. US Tsy yields are little changed, with the 10yr still under 4.00%. Gold is lower, consistent with some USD support.

- The BBDXY index is back up to around 1210.7 (+0.15% for the session so far), but this is familiar ranges for Oct (earlier highs were just above 1219, while we started the month sub 1200).

- NZD/USD is lower, but at 0.5725/30, remains within recent ranges, while AUD/USD has softened but remains near 0.6500 at this stage. AUD/JPY is edging back towards recent highs, last 98.30/35, aiming for an upside 98.50 test. NZD/JPY is near 86.60, just under the 20-day EMA resistance point and now little changed for the session.

- Later US October Philly Fed non-manufacturing and September Canadian CPI print. ECB President Lagarde and Board member Lane speak.

OIL: Increased Supply Being Monitored, US Inventory Data Tuesday

Oil prices have continued trending lower during today’s APAC session and have looked through news that the meeting between the US’ Rubio and his Russian counterpart Lavrov has been put on hold. The market is focusing on supply/demand developments with seaborne crude in transit continuing to rise as both OPEC and non-OPEC increase production.

- WTI (December contract) is down 0.2% to $56.90/bbl off the intraday low of $56.60. It made a high of $57.02 earlier but the break above $57 was very brief. Brent is 0.2% lower at $60.86/bbl after falling to $60.58. It rose to $61.01 early in the session but the break was only a moment.

- While geopolitical developments continue to be monitored, the focus remains on the expected market surplus by year end which is likely to result in inventory building. Crude at sea continues to rise and Rapidan Energy estimates supply growth is three times faster than demand (Bloomberg). US industry-based stock data is released Tuesday and the EIA Wednesday.

- While a Ukraine peace deal is likely to remain elusive, plans for US and Russian officials to meet including Presidents Trump and Putin had again increased hopes that sanctions on Russian fuel may be eased. The US administration is sceptical that sanctions work but the longer Russia avoids a ceasefire the more likely they will be extended.

- Later US October Philly Fed non-manufacturing and September Canadian CPI print. ECB President Lagarde and Board member Lane speak.

Gold & Silver Fall As Equities & US Dollar Strengthen, Focus Remains On US

Gold has stabilised today during the APAC session after rising 2.5% on Monday. Prices rose to $4375.38/oz and then fell to $4332.95 and are now down 0.4% to $4340.5. Equities are rallying and the US dollar is slightly stronger (BBDXY +0.1%) but the factors bullion ignored yesterday may have also contributed to the pause in the rally. It is in overbought territory, 2025 Fed easing is already priced in, there is talk that the US government shutdown could end this week and US-China trade tensions appear to have eased.

- Both gold and silver continue to hold well above initial support levels of $4140.8, 15 October low, and $48.736, 20-day EMA, respectively.

- The 1 November deadline for a US-China trade deal remains but President Trump said that the US will “be fine” with China. Economic Council Director Hassett also gave indications that the government shutdown could conclude this week.

- Silver is down 1.1% to $51.87 after falling to $51.607. It is a smaller market than gold and so moves tend to be amplified. It is also signalling that it is overbought.

- Equities are stronger across the region with the Hang Seng up 1.7% and ASX +0.7% but the S&P e-mini is flat. Oil prices are lower with WTI -0.3% to $56.84/bbl. Copper is 0.2% higher.

- Later US October Philly Fed non-manufacturing and September Canadian CPI print. ECB President Lagarde and Board member Lane speak.

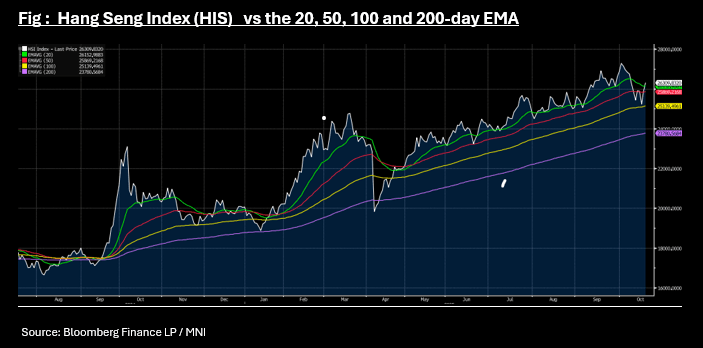

ASIA STOCKS: Trump Comments Drives HSI Above Key Technical

Japanese stocks reached another new high as Sanae Takaichi appears likely to become the next PM and deliver what is expected to be an expansionary fiscal policy and low rates. China's key markets latched onto President Trump's comments that he expects the US and China will have a “really fair and really great trade deal together” with major bourses delivering solid gains. The KOSPI hit yet another new high as the Korea Economic Daily reported that President Lee is considering cutting the top rate on dividends (as per BBG).

- The NIKKEI is up over 700pts today reaching a new high of 49,929 and almost 5% higher in the first two days of the trading week.

- Having trended below the 20-day and 50-day EMA earlier this month, today's gains of +1.8% takes the Hang Seng back above the 20-day EMA of 26,154. The CSI 300 is up +1.5% today for its largest daily gain since before the October National Day holidays. The Shanghai Composite is up +1.20% and the Shenzhen Composite up +1.6% as it nears its 20-day EMA, the second time this month it will try to hold above the key technical.

- The KOSPI is up on the dividend news, trending well above all moving averages and better by +0.6% today, and +2.5% already this week.

- The Jakarta Composite is strong ahead of tomorrow's Central Bank +1.3% as it consolidates above the 20-day EMA.

ASIA STOCKS: Tech Equity Gains Should Support South Korea/Taiwan Inflows

Yesterday saw outflows from South Korea, but Taiwan inflows were positive. For South Korea, this looks to be a pause in what is otherwise a positive flow backdrop, as we continue to see global equity sentiment recover after last week's credit induced wobbles. Apple also buoyed broader tech sentiment as shares rallied on positive reports on new Iphone demand. This should benefit markets like South Korea and Taiwan. So far today, both markets are tracking firmly higher, both at fresh record levels. For Taiwan, yesterday's inflow still wasn't enough to bring the 5-day sum back into positive territory though.

- Indian inflow momentum remained strong, as YTD outflows continue to ebb lower. Onshore equity momentum remains positive.

- In South East Asia, outside of modestly positive inflows for Indonesia (ahead of tomorrow's expected BI cut), we are seeing light outflow pressures for the past 5 trading days elsewhere.

Table 1: Asian Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | -77 | 1135 | 3495 |

| Taiwan (USDmn) | 257 | -973 | 6587 |

| India (USDmn)* | 100 | 760 | -16167 |

| Indonesia (USDmn) | 32 | 11 | -3081 |

| Thailand (USDmn) | 2 | -156 | -3096 |

| Malaysia (USDmn)** | -45 | -135 | -4175 |

| Philippines (USDmn) | -2 | -18 | -716 |

| Total (USDmn) | 267 | 624 | -17153 |

| * Data Up To Oct 20 | |||

| ** Data Up To Oct 17 |

Source: Bloomberg Finance L.P./MNI

INDONESIA: MNI BI Preview-Oct 2025: More Cuts To Support Growth

- Download Full Report Here

- Bank Indonesia stated in September that its decision to cut rates was "consistent with joint efforts to stimulate economic growth", so another 25bp rate cut to 4.5% on 22 October is expected as activity data have softened over the last month.

- Other factors supporting further monetary easing include USDIDR stabilising below 16600 in October, IDR NEER is higher since the September decision, BI’s pro-growth stance, and Fed cuts expected in October and December.

- Also headline and core CPI inflation remain well contained within BI's 1.5-3.5% target band and it expects it to stay there in 2026. However, upside inflation risks could develop given coordinated easing of fiscal and monetary policies.

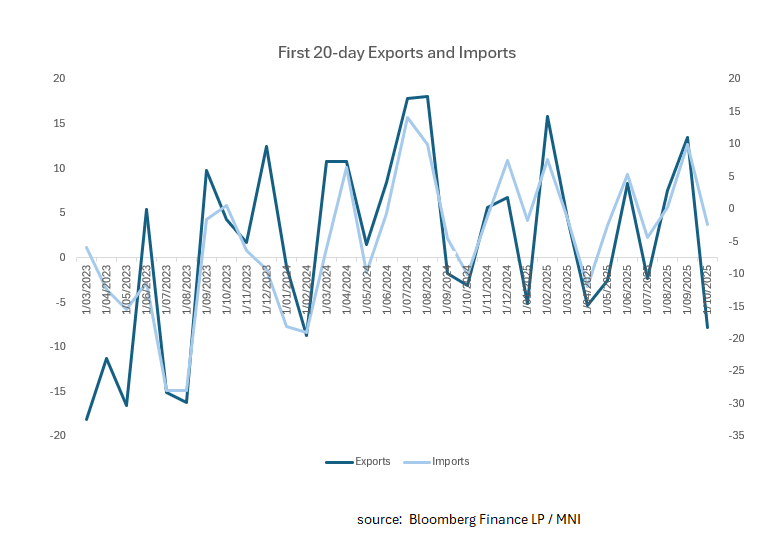

SOUTH KOREA: First 20-days Trade Data Weak, Working Day Differences Key

- South Korea's early export data for October 2025 indicated a significant year-on-year drop primarily due to fewer working days, with the average daily export value increasing, underpinned by semiconductors.

- Exports were down by 7.8% year-on-year to $30.1 billion, with estimates when stripping out working days differences suggest an increase of over 8%.

- Imports declined 2.3% to $32.9 billion resulting in $2.8bn deficit, again mainly attributed to holidays.

- Semiconductors exports surged by 47% to $4.5 billion and oil related shipments rose 6.2%.

- Exports to the US were down over 40%.

ASIA FX: USD/KRW Follows USD/JPY Higher, CNH & TWD Outperform

In North East Asia, USD trends are mixed. CNH is trading resiliently, backed by another low USD/CNY fixing (which was a fresh low for 2025). USD/CNH has tested under 7.1200, but the break lower has been a definitive one. Broader USD sentiment is firmer, with yen (post confirmation that Takaichi is the new Japan PM) and NZD down in the G10 space. CNH/JPY is climbing, last above 21.2250, but short of earlier Oct highs near 21.50.

- China and Hong Kong equities continue to recover strongly. Optimism around a US-China deal following Trump comments is aiding sentiment, with market odds of a 100% tariff rate on Nov 1 remaining quite low.

- Equities elsewhere are positive, although South Korean and Taiwan markets are off earlier highs. Broader tech sentiment remains positive amid optimism around Apple Iphone demand.

- Spot USD/KRW has climbed back to 1425/26, up around 0.35%. The weaker yen is likely a factor, but we might see selling interest re-emerge on moves above 1430/35.

- Spot USD/TWD is holding under 30.60, outperforming KRW. The 1 month NDF has climbed back to this level though. Later on we have Sep Taiwan export orders. The market consensus is for a 18.7% rise, after a 19.5% Aug gain.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 21/10/2025 | 0600/0700 | *** | Public Sector Finances | |

| 21/10/2025 | 0700/0900 | ECB Lane at Macroeconomics and Finance Conference | ||

| 21/10/2025 | 0900/1100 | * | government debt | |

| 21/10/2025 | 0900/1100 | * | government deficit | |

| 21/10/2025 | 0900/1000 | BOE Saporta Fireside Chat at Islamic Development Bank | ||

| 21/10/2025 | 1030/1130 | BOE Bailey & Breeden on Private Markets at Financial Services Regulation Committee | ||

| 21/10/2025 | 1100/1300 | ECB Lagarde Keynote at Norges Bank Climate Conference | ||

| 21/10/2025 | 1230/0830 | *** | CPI | |

| 21/10/2025 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 21/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 21/10/2025 | 1300/0900 | Fed Governor Christopher Waller | ||

| 21/10/2025 | 1915/2015 | BOE Mann Fireside Chat at Lazard | ||

| 22/10/2025 | 0600/0700 | *** | Consumer inflation report | |

| 22/10/2025 | 0600/0700 | *** | Producer Prices | |

| 22/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 22/10/2025 | 1100/1300 | ECB de Guindos at Barcelona Real Assets Meeting | ||

| 22/10/2025 | 1225/1425 | ECB Lagarde Keynote at Frankfurt Finance & Future Summit |