MNI EUROPEAN MARKETS ANALSYSIS: Some Markets Stabilising

- Chinese retaliation on tariffs over the weekend has seen another leg lower for risk assets and the demand for USDs against risk proxies has had another leg. The BBDXY opened around 1262 and is currently trading around 1264. With the equity rotation from the US back to Europe continuing the EUR is probably the best currency to be long of outside of the JPY and CHF.

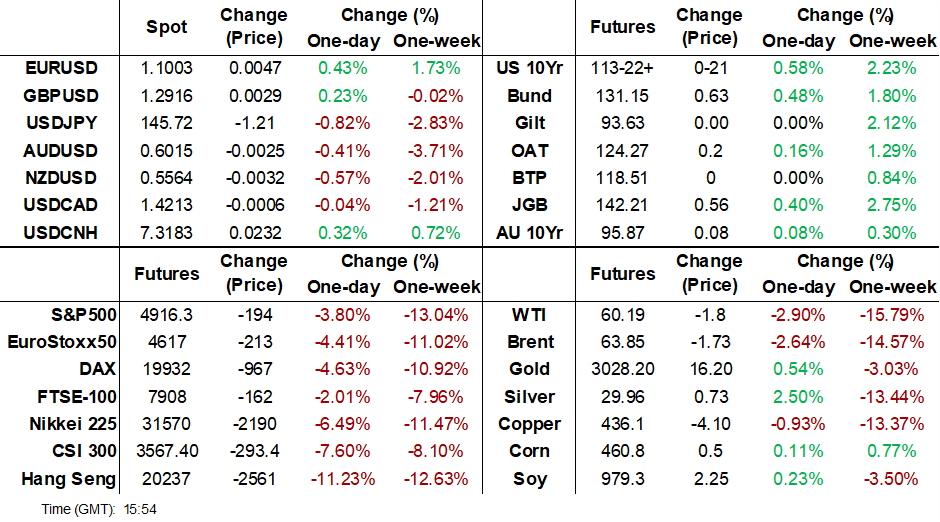

- TYM5 is stronger at 113-21, +19+ from closing levels in today's Asia-Pac session, but well off today's high of 114-10.

- Markets continue to be hit by the ongoing trade-related pullback in risk appetite, although some have begun to stabilise at lower levels due to selling fatigue and profit-taking, such as oil and AUD. Some Asian countries have said today that they will take steps to stabilise markets if needed and Japan has said it will speak with the US.

MARKETS

US TSYS: Cash Bonds Bull-Steepen, Risk-Off Pared

TYM5 is stronger at 113-21, +19+ from closing levels in today's Asia-Pac session, but well off today's high of 114-10.

- According to MNI's technicals team, focus for TYM5 is on technical resistance at 114-16 (2.000 proj of the Jan 13 - Feb 7 - Feb 12 price swing) after having breached round number resistance (114-03.5 high) on Friday.

- Markets continue to be hit by the ongoing trade-related pullback in risk appetite, although some have begun to stabilise at lower levels due to selling fatigue and profit-taking, including risk-sensitive AUD and oil prices. US equity futures are down sharply but also off their intraday lows.

- Some Asian countries have said today that they will take steps to stabilise markets if needed and Japan has said it will speak with the US.

- Nevertheless, the market is continuing to digest the implications of Friday's unveiling of a 34% duty on all US imports by China.

- Cash US tsys are 3-15bps richer, led by the short-end, in Asia-Pac session.

JGBS: Richer, PM Ishiba To Push For Lower Tariffs, 30Y Supply Tomorrow

JGB futures remain sharply higher at 142.19, +53 compared to settlement levels, but well off session bests (142.95).

- “Japanese Prime Minister Shigeru Ishiba says that the government will strongly push the US for tariff reductions, while emphasizing that it does not intend to provoke conflict with the US. Ishiba says the US may have misinterpreted certain trade issues and questions whether the measures align with the US-Japan Trade Agreement.” (per BBG)

- Japan’s leading economic indicator was at 107.9 in February, compared with 108.2 in the previous month.

- Markets continue to be hit by the ongoing trade-related pullback in risk appetite, although some have begun to stabilise at lower levels due to selling fatigue and profit-taking.

- Some Asian countries have said today that they will take steps to stabilise markets if needed and Japan has said it will speak with the US.

- Cash US tsys are 3-15bps richer, led by the short-end, in Asia-Pac session.

- Cash JGBs are flat to 11bps richer across benchmarks out to the 30-year (40-year flat), with the belly leading.

- Swap rates are 7-10bps lower.

- Tomorrow, the local calendar will see BoP Current Account and Trade Balance data alongside 30-year supply.

AUSSIE BONDS: Richer But Well Off Bests, Bus & Conf Conf Tomorrow

ACGBs (YM +10.0 & XM +7.0) are richer but well below today's Asia-Pac session bests.

- Markets continue to be hit by the ongoing trade-related pullback in risk appetite, although some have begun to stabilise at lower levels. US equity futures are down sharply but also off their intraday lows.

- “Australian Treasurer Jim Chalmers blames "bad decisions" on tariffs for global stock market turmoil, despite his department forecasting minor impacts on domestic economic growth and inflation.” (per BBG)

- Cash US tsys are 3-15bps richer, led by the short end, in today's Asia-Pac session.

- Cash ACGBs are 7-10bps richer with the AU-US 10-year yield differential at +23bps.

- Bill strip pricing is +4 to +14, with whites leading.

- RBA-dated OIS pricing gives a 50bp rate cut in May a 55% probability, with a cumulative 119bps of easing priced by year-end (based on an effective cash rate of 4.09%). Earlier in the session, a 50bp rate cut in May was given an 80% probability, with a cumulative 133bps of easing priced by year-end.

- Tomorrow, the local calendar will see Consumer and Business Confidence data.

- The AOFM plans to sell A$400mn of the 4.25% 21 June 2034 bond tomorrow.

BONDS: NZGBS: Closed Well Off Bests With Twist-Steepener, RBNZ Decision On Wed

NZGBs closed mixed, well off session bests, with the 2/10 curve steeper. Benchmark yields finished 3bps lower to 4bps higher after being 9-12bps lower earlier in the session.

- Moreover, the NZ-US and NZ-AU 10-year yield differentials closed 7-8bps wider. At +44bps, the NZ-US differential is at its widest since October last year.

- Markets continue to be hit by the ongoing trade-related pullback in risk appetite, although some have begun to stabilise at lower levels due to selling fatigue and profit-taking. US equity futures are down sharply but also off their intraday lows.

- Some Asian countries have said today that they will take steps to stabilise markets if needed and Japan has said it will speak with the US.

- Swap rates closed 3-9bps lower, with the 2s10s curve steeper.

- "The RBNZ Shadow Board is in favour of lowering the OCR by 25bps to 3.50% this week." (per BBG)

- RBNZ dated OIS has 30bps of easing priced for April, with a cumulative 101bps by November 2025.

- Tomorrow, the local calendar will see the NZIER Business Opinion Survey.

- On Thursday, the NZ Treasury plans to sell NZ$275mn of the 0.25% May-28 bond and NZ$225mn of the 4.25% May-34 bond.

The market has started to realise this is not just a US problem and that a US recession has serious implications for global growth. The Chinese retaliation on tariffs over the weekend has seen another leg lower for risk assets and the demand for USDs against risk proxies has had another leg. The BBDXY opened around 1262 and is currently trading around 1264.

- EUR/USD - has had a range of 1.0882 - 1.1000, it goes into the London open near the Asian highs around 1.0980. With the equity rotation from the US back to Europe continuing the EUR is probably the best currency to be long of outside of the JPY and CHF.

- GBP/USD - range of 1.2824 - 1.2933, but is going into the London open little unchanged from its open around 1.2890.

- AUD/USD - range of 0.5933 - 0.6077. This morning's gap lower on the open from the 0.6070 area in very thin liquidity eventually found some support around 0.5933.We have spent the rest of the session clawing back some of these losses as risk attempts to stabilise the AUD is going into the London session around 0.6020.

- AUD trades very poorly in the crosses with the risk barometer AUD/JPY opening around 89.15 but gapping very quickly down to the lows around 86.20. As risk has stabilised AUD/JPY has clawed back some of these losses and goes into the London open around 87.80.

- USD/CNH - the Asian range has been 7.2927 - 7.3311, we are going into the London session trading near the highs of the day around 7.3200. Traders think a long USD/CNH is one of the cleanest expressions to trade as China retaliates to tariffs. Watch for official smoothing if we approach the 7.3600 area again.

- USD/JPY - the Asian range has been 144.82 - 147.12. The gap lower this morning in risk saw USD/JPY move very quickly back to its lows around 145.00. The JPY is a favourite to own in times of extreme stress and while this market stays under pressure there will be good buyers of JPY. USD/JPY has regained a good portion of its losses as risk found a base and we go into the London open around 146.00.

- Cross asset sentiment trades very poorly US equities down between 3.5/4% after being down more than 5% at one stage. Huge demand for Treasuries testing Fridays lows around 3.87% on the 10yr again. Commodities trade poorly as the market reevaluates what the events of this week mean for Global growth going forward, there seemed to be large Stops going through in Copper touching a low of around 403 in the futures, the move lower though has been completely erased going into the London open with the HGA contract going into the London open around 440 and the longs that have been stopped out scratching their heads.

- Key US data this week will be the US CPI April 10th.

AUDUSD

Source: MNI - Market News/Bloomberg

ASIA STOCKS: Blow to Chinese Investors as CSI 300 Drops over 6%

Investors in China have had a torrid few years given the decline in property prices damaging savings. A huge inflow into bonds followed and late last year data showed that investors were moving out of bonds into equity as the economy showed signs of improvement. Given consumer confidence has been at lows, today’s rapid decline in stocks will be of major concern as the has been the largest decline in over five years.

Taiwan returned from holidays to record decline with a decline now of 20% from the July peak to today.

The Bank of Korea issued a statement today saying that the volatility of stock and fx has increased due to the higher-than-expected tariffs and that they will take available market stabilization measures if needed.

- China’s Hang Seng lead the way today falling by -11.3% having been closed on Friday. The CSI 300 followed suit falling by -6.8% , with Shanghai down -6.8% and Shenzhen down -9.5%.

- The KOSPI fell -4.9%, backing up from week’s falls of -3.6% despite the BOK’s reassurance.

- Malaysia’s FTSE bursa KLCI Index had its worst decline of the year falling -4.33%, following last week’s modest declines.

- The Straits Times in Singapore fell -7.17%, Philippines -4.2% and Taiwan -9.7% making Monday one of the biggest down days in some time.

- India’s NIFTY 50 has had its worst opening of the year down -3.90%, following Friday’s close down -1.49%

OIL: Crude Off Intraday Low But Monitoring Supply & Demand Risks

Oil prices are down sharply again today but off the intraday lows. The continued pullback in risk and concerns over the impact of increased trade protectionism on global demand pressured crude but selling fatigue and profit taking as well as the will from a number of Asian countries to negotiate with the US and stabilise markets saw a levelling out and a modest pickup. The USD index is off its highs to be down 0.1% today.

- WTI is down 2.3% to $60.54/bbl after it approached $61.00. It reached $59.38 earlier but has struggled to hold moves below $60. Brent fell to $63.01 earlier finding support here and then rose towards $64.50. It is now down 2.4% to $63.98 today.

- Saudi Arabia’s decision to reduce its benchmark Arab Light by $2.30/barrel for Asia in May, the most in over two years, added to the tariff pressure on oil markets today. It also cut prices to Europe and the Americas but not by as much. This follows OPEC’s higher-than-expected increase in production.

- Goldman Sachs cut its Brent forecast for the second time in a week. December 2025 has been revised down $4 to $62/bbl, according to Bloomberg, due to US trade policy risking a recession in the US and possibly elsewhere. GS is now forecasting stagnation in the US with risks to the downside.

- China, the world’s largest oil importer, said that it would use policy to defend its economy and urged markets not to panic. It also hasn’t ruled out negotiating with the US.

- Later the Fed’s Kugler speaks on inflation and the ECB’s Cipollone appears. US February consumer credit, German February trade/IP, February euro area retail sales and Canadian BoC business survey print.

GOLD: Key Technical Breached as Gold Falls

- Gold has benefited more than most in the trade war build up yet with it now in full swing, even it is suffering.

- Gold delivered only its second weekly fall for the week last week for 2025, falling by -1.52% as a general commodities rout occurred with London’s Metal Exchange having the biggest decline since early 2020.

- Having reached highs of $3,134.17 at the start of last week, gold saw forecasters restating their year-end forecasts higher and higher.

- Gold broke through $3,000 this morning at the open trading as low as $2,971.30 before bouncing back to $3,028.15.

- Gold has traded through the 20-day EMA of $3034.60 and held, with its next key technical level the 50-day EMA of $2,947.07

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 07/04/2025 | 0900/1100 | ** | Retail Sales | |

| 07/04/2025 | 0945/1145 | ECB's Cipollone At CBDC Conference | ||

| 07/04/2025 | 1430/1030 | Fed Governor Adriana Kugler | ||

| 07/04/2025 | 1430/1030 | ** | BOC Business Outlook Survey | |

| 07/04/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 07/04/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 07/04/2025 | 1700/1300 | * | US Treasury Auction Result for Cash Management Bill | |

| 07/04/2025 | 1900/1500 | * | Consumer Credit | |

| 08/04/2025 | 0500/1400 | Economy Watcher's Survey | ||

| 08/04/2025 | 0645/0845 | * | Foreign Trade | |

| 08/04/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 08/04/2025 | 0900/1100 | ECB's De Guindos At Spanish Banking Association Meeting | ||

| 08/04/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 08/04/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 08/04/2025 | 1400/1000 | * | Ivey PMI | |

| 08/04/2025 | 1400/1600 | ECB's Cipollone at ECON Hearing On Digital Euro |