MNI Europe Pi: Gilts Flat Into Roll, But Overall Long-Leaning

Nov-20 14:59By: Tim Cooper

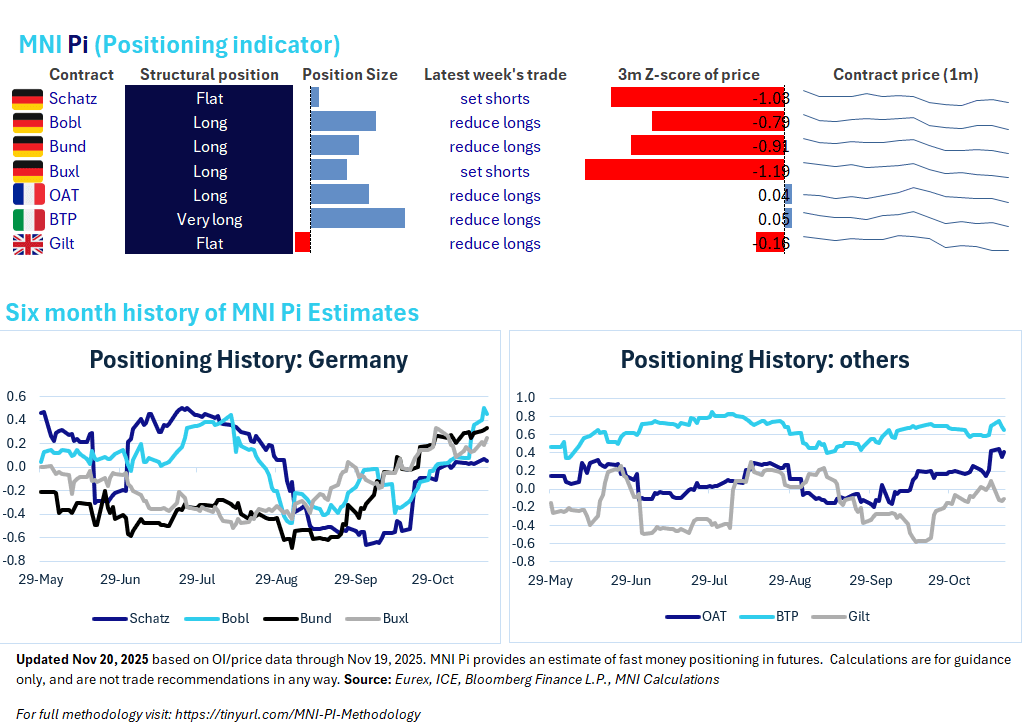

Bunds+ 1

Download Full Document Here

EXECUTIVE SUMMARY

- Structural positioning across European bond futures has transitioned from largely short-leaning in September, to largely long-leaning currently.

- The shift has been led largely by Germany, though overall there are no structurally "short" contracts in the MNI Europe Pi matrix.

- The most recent week's trade (to Nov 19) is largely indicative of long reduction and short-setting, however.

- GERMANY: German contracts' structural positioning has gone from broadly flat to largely long, and stands in sharp contrast to short/mixed in our updates covering September. Bobl, Bund and Buxl have each moved into long territory vs flat previously. Schatz remains "very short" however. The latest's week trade showed short-setting in Schatz and Buxl, with longs reduced in Bobl and Bund.

- OAT: OAT structural positioning has shifted into long territory, breaking out of the flat range it's been in most of 2025. Latest week's trade was indicative of long reduction.

- GILT: Gilt structural positioning was relatively flat going into the Dec/Mar rolls this week, having exited the short territory seen throughout October. The latest week saw some long reduction.

- BTP: BTP remains in "very long" territory, and is not far off its summer longs. Trade indicative of long reduction was seen in the most recent week, however.