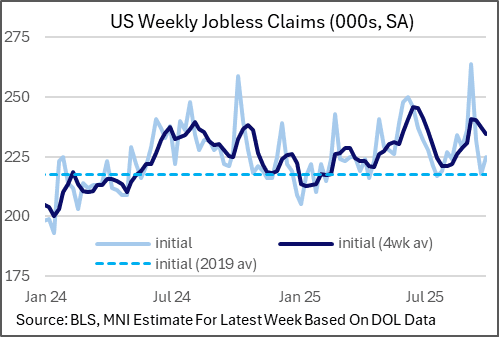

US DATA: MNI Estimates Uptick In Initial Claims To 223-225k Last Week

Oct-03 13:46

Based on state-by-state data released by the Department of Labor, MNI estimates a seasonally-adjusted 223-225k initial jobless claims in the week of September 27. This would represent a 5-7k uptick from the prior week's 218k (unrevised). That would still bring the 4-week moving average down, to 235k (if it's 225k claims for the week) vs 237k prior, for a 4-week low.

- In lieu of the official series due to the federal government shutdown, we are using the basic methodology employed by the DOL and the seasonal factors posted by the BLS to make the estimate. All of the state level claims are non-seasonally adjusted. The actual change in national NSA claims in the latest week is negligible.

- The range depends largely upon assumptions for Arizona, Massachusetts and US Virgin Islands claims, which are not yet available for the latest week. The seasonality of these three geographies doesn't offer much clarity on potential weekly direction, so we've used a small range based on recent trends.

- Note that while Texas had an outsized drop in claims (3.85k), this appears to be a continuation of the fall from the exaggerated elevated claims at the start of September. We continue to await the historic series to be updated to remove the fraud effect but this hasn't yet been done based on the latest data.

- There was also an unusual 3.05k rise in Kentucky claims which is out of the seasonal norm (and by far the biggest rise among all states for the week) - that may be exaggerating the rise in claims though it's unclear what the cause is.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOE: Taylor in the "four plus one camp" camp for cuts this year

Sep-03 13:42

- Taylor states that "the most risky channel for the transmission of inflation expectations back into inflation, actual inflation is through wage bargaining but I think given the softening in the labour market"

- He sees wage growth as slowing: "It's generally coming in in the low threes or thereabouts, and possibly lower, suggesting to me that we are completing that last mile of that trajectory."

- On disinflation is continuing but "It was a new set of shocks that we got in January, administered prices, taxes, a little bit of an energy shock, and now some food shocks. So I think I'm trying to see through that."

- He also notes that displaced goods that would have gone to the US are likely to weigh on UK / European inflation. "I think the tariff issue is a little bit undercooked in our in our baseline forecast. So there's a point of disagreement for me there."

- He also thinks that the neutral rate is lower: "I tend to think the neutral rate of interest is quite low, and so I feel we have further to go to reach neutral, which leads me to think therefore currently we're more restrictive, and that we're plenty restrictive enough to take the remaining underlying inflation out of the economy."

- "I'm more in the four plus one camp in terms of how many cuts per year, maybe four or five, rather than four minus four or three. And so I think that led me to my vote."

PIPELINE: Corporate Bond Update: $1.5B OKB 5Y SOFR Launched, Issuer List Rising

Sep-03 13:37

Meanwhile, the list of issuers climbs to 25 after Tuesday's record 28 names issued $50.95B in debt:

- Date $MM Issuer (Priced *, Launch #)

- 09/03 $2B #AIIB 3Y SOFR+31

- 09/03 $1.5B #OKB 5Y SOFR+43

- 09/03 $1.2B Clarios 7NC3

- 09/03 $600M Tallgrass Energy 8.5NC3.5

- 09/03 $600M Cleveland-Cliffs 8.25NC3.25

- 09/03 $500M OneMain Finance 7.5NC3

- 09/03 $500M Century Comm 8NC3 6.875%

- 09/03 $500M Lithia Motors 5NC2

- 09/03 $Benchmark Colburn 10Y +150a

- 09/03 $Benchmark Pacific Life 30Y +135a

- 09/03 $Benchmark Swedish Export Credit 5Y

- 09/03 $Benchmark BNY Mellon PerpNC5 6.25%a

- 09/03 $Benchmark F&G Global 3Y +130a, 3Y SOFR

- 09/03 $Benchmark Nordea Bank Perp Nov'33 7.25%a

- 09/03 $Benchmark Blackstone Private Credit 5Y +185a

- 09/03 $Benchmark Dow Chemical +5Y +140a, +10Y +170a

- 09/03 $Benchmark Plains All American +5Y +137.5, +10Y +170a

- 09/03 $Benchmark Petrobras Global +5Y 5.7%, +10Y 6.9%

- 09/03 $Benchmark Southern Co Gas 3Y +80a, 10Y +120a

- 09/03 $Benchmark The Commercial Bank (PSQC) 5Y +125a

- 09/03 $Benchmark Turkie Wealth Fund +5Y 7.625%a, 10Y 8.735%a

- 09/03 $Benchmark Sumitomo Life Insurance 30NC10 6.125%

- 09/03 $Benchmark Suzano Netherlands +10Y +180a

- 09/03 $Benchmark PECO Energy 10Y +95a, 30Y +105a

BOE: Greene's vote due to inflation persistence and less risk of weaker demand

Sep-03 13:35

- Greene says she voted for Bank Rate on hold in August due for 2 reasons: "The risk of higher inflation persistence has increased, and secondly, I think the risk of weaker demand has decreased, particularly since May"

- Greene discusses being concerned about inflation persistence and the knock on impacts for inflation expectations.

- She notes that "We expect GDP growth to pick up, underlying GDP growth, particularly, to pick up modestly from here. So that suggests that any kind of labour market shakeout that I had been worried about before probably won't be coming. Employment intentions are still negative, but they're less negative than they had been previously, and that's from our agents that suggests that some of the or much of the adjustment in the labour market may have already occurred." As well as the Agent's survey she points to DMP.

- {gb}Lots of focus on food inflation from both Greene and Lombardelli. Underlining the importance of that box in the MPR and that it really is headline (not just services) inflation that is the most important point for the MPC right now.