EM LATAM CREDIT: MNI EM Credit Market Wrap - LATAM (28 Mar)

Source: BBG

Measure Level Δ DoD

5yr UST 3.98% -10bp

10yr UST 4.26% -10bp

5s-10s UST 27.5 +1bp

WTI Crude 69.1 -0.8

Gold 3081 +24.0

Bonds (CBBT) Z-Sprd Δ DoD

ARGENT 3 1/2 07/09/41 970bp +40bp

BRAZIL 6 1/8 03/15/34 273bp +7bp

BRAZIL 7 1/8 05/13/54 360bp +8bp

COLOM 8 11/14/35 405bp +13bp

COLOM 8 3/8 11/07/54 488bp +13bp

ELSALV 7.65 06/15/35 485bp +24bp

MEX 6 7/8 05/13/37 272bp +7bp

MEX 7 3/8 05/13/55 332bp +7bp

CHILE 5.65 01/13/37 163bp +6bp

PANAMA 6.4 02/14/35 345bp +11bp

CSNABZ 5 7/8 04/08/32 566bp +24bp

MRFGBZ 3.95 01/29/31 306bp +12bp

PEMEX 7.69 01/23/50 670bp +16bp

CDEL 6.33 01/13/35 209bp +10bp

SUZANO 3 1/8 01/15/32 204bp +11bp

FX Level Δ DoD

USDBRL 5.76 +0.01

USDCLP 951.30 +17.76

USDMXN 20.4 +0.11

USDCOP 4202.81 +32.68

USDPEN 3.66 +0.02

CDS Level Δ DoD

Mexico 137 3

Brazil 187 4

Colombia 225 3

Chile 61 2

CDX EM 97.25 (0.15)

CDX EM IG 100.59 (0.09)

CDX EM HY 91.80 (0.22)

Main stories recap:

· A trifecta of disappointing US economic data indicating stagflation triggered broad based global declines in equities and a US Treasury rally of 8-10bps across the curve.

· US real personal spending in February was weaker than expected leading the Atlanta Fed GDP Now first quarter 2025 GDP forecast to be revised lower to -2.8%. The University of Michigan consumer expectations survey was worse than expected while the inflation expectations component rose.

· The February core pce price index, thought to be the Federal Reserve’s preferred inflation gauge, was reported higher than expected.

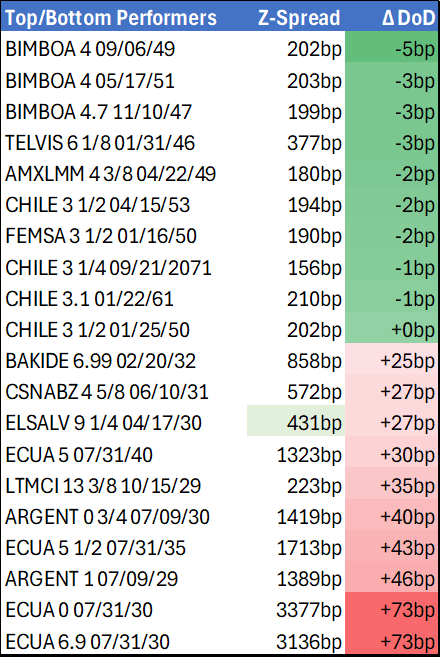

· EM benchmark bond spreads widened out across the globe with most names mid-single digits wider. Some higher quality, IG rated Chile and Mex corporate bonds predictably outperformed while higher beta underperformed.

· The highest yielding Latam sovereign bonds fell the most with prices of Argentina and El Salvador bonds down ¾ point while Ecuador moved ½ point lower.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: US Trade Policy Rekindles Risk-Off Sentiment

- Treasuries bounced off early session lows and look to finish near session highs, curves flatter with bonds outperforming as trade policy concerns rekindled risk-off sentiment prevalent in the first half of the week.

- Risk-off as Pres Trump cabinet meeting marks April 2 when Canada & Mexico "tariffs will go on, not all but a lot of them" , taking a firmer stance on the EU, stating that the decision on tariffs on the EU is 25% and that details will be “coming soon”.

- Tsy Jun'25 10Y futures trade at 110-28 (+10.5) after the bell, piercing resistance at 110-20, the 76.4% retracement of the Dec 3 - Jan 13 bear leg. This broadens the bullish recovery and signals scope for a climb towards the 111-00 handle, ahead of 111-22+, the Dec 3 high and a key resistance.

- New home sales fell much more sharply in January than expected, but this was more than made up for by upward revisions while building permits were revised slightly lower in January’s final reading, to 1,473k - representing a 0.6% decline rather than the initially reported 0.1% rise.

- Canadian dollar and Mexican peso have rallied as a result. USDCAD fell from 1.4360 to 1.4300, while USDMXN fell from 20.47 to 20.29 lows. EU tariff mention saw EURUSD slipping from key resistance around 1.0530 to 1.0485 in short order.

- The upcoming US economic data with the second release for Q4 national accounts on Thursday before the January PCE report on Friday. Real GDP growth is seen confirming what was at the time a softer than expected 2.3% annualized in Q4, whilst there will also be a first estimate for real GDI growth after 2.1% in Q3. However, January’s monthly report (on Friday) is likely to show consumption got off to a much weaker start of 2025.

AUDUSD TECHS: Corrective Pullback Extends

- RES 4: 0.6471 High Dec 9 ‘24

- RES 3: 0.6429 High Dec 12 ‘24

- RES 2: 0.6414 38.2% retracement of the Sep 30 ‘24 - Feb 3 bear leg

- RES 1: 0.6409 High Feb 21

- PRICE: 0.6320 @ 16:22 GMT Feb 26

- SUP 1: 0.6300/6231 Low Feb 26 / Low Feb 10

- SUP 3: 0.6171/6088 Low Feb 4 / 3

- SUP 3: 0.6045 1.500 proj of the Sep 30 - Nov 6 - 7 price swing

- SUP 4: 0.6000 Round number support

AUDUSD traded lower Wednesday. The latest pullback appears corrective, however, the pair has traded through support at the 50-day EMA, at 0.6316. A clear breach of this average would signal scope for a deeper retracement and expose 0.6231, the Feb 10 low. For bulls, a resumption of gains would refocus attention on key resistance at 0.6402/14 - the 100-dma and 38.2% of the Sep 30 ‘24 - Feb 3 bear leg respectively.

US TSYS: Late SOFR/Treasury Option Roundup

Better call buying resumed after SOFR & Treasury options appeared mixed on lighter volumes Wednesday morning. Underlying futures bounced off early session lows as Pres Trump's cabinet meeting rekindled market concerns over global trade policy. Projected rate cuts through mid-2025 have firmed up from morning levels (*) as follows: Mar'25 at -0.7bp (-0.5bp), May'25 at -6.9bp (-6.4bp), Jun'25 at -21.5bp (-19.6bp), Jul'25 at -29.6bp (-27.6bp).

- SOFR Options:

- +8,000 0QN5/2QN5 96.50/97.00 call spd strip, 24.75-25.0

- +7,000 SFRM5 95.62 puts, 1.0

- Block, +15,000 2QM5 96.75/97.00 call spds vs. 95.50/95.75 put spds, 1.0 net calls over

- Block, 10,000 2QM5 96.50/96.75 call spds vs. 95.50/95.75 put spds, 4.0 net calls over

- +5,000 SFRU5 98.00/99.00 2x3 call spds 2.0 ref 96.045

- +5,000 SFRM5 95.62 puts 1.0 ref 95.865

- +5,000 SFRJ5 95.75/96.00 1x2 call spds, 3.5 ref 95.87

- +3,000 0QH5 96.18/96.31 strangle, 13.5

- -5,000 SFRZ5 95.68/95.93 put spds 9.5 ref 96.18

- +50,000 SFRM5 96.18/96.62 call spds .62 on legs

- 16,000 0QK5 96.62/96.93 call spds ref 96.295

- 5,000 SFRZ5 95.50/95.87 put spds ref 96.175

- 2,500 SFRZ5 96.12/96.37/96.62 put flys

- 6,500 0QH5 95.93/96.06/96.18 put flys ref 96.25 to -.235

- 4,000 2QJ5 96.25/96.50/96.62 broken call flys ref 96.27

- Treasury Options:

- Block, total 105,000 TYK5 113.5 calls, 19 vs. 110-20/0.17%

- +15,000 TYK5 112 calls, 33 ref

- -6,750 USJ 119/122 call spds, 33

- over -7,000 USJ5 119/122 call spds, 33 ref 117-09

- -10,000 wk4 TY 111 calls, 6

- 4,500 TYK5 114.5 calls, 10 ref 110-18

- +30,000 TYJ5 109/109.5 put spds, 9 ref 110-11.5

- over 5,500 TYJ5 110.5 calls, 42 last ref 110-12

- over 12,200 TYK5 110.5 calls ref 110-123,100 TYK5 106/108 put spds vs. TYM5 105/107 put spd spds

- 2,000 FVK5 106.75/107.5/108 broken call flys ref 107-12.75