EM LATAM CREDIT: MNI EM Credit Market Wrap - LATAM (25 Apr)

Source: BBG

Measure Level Δ DoD

5yr UST 3.88% -6bp

10yr UST 4.26% -5bp

5s-10s UST 38.0 +0bp

WTI Crude 63.2 +0.4

Gold 3312 -37.4

Bonds (CBBT) Z-Sprd Δ DoD

ARGENT 3 1/2 07/09/41 856bp +3bp

BRAZIL 6 1/8 03/15/34 269bp -6bp

BRAZIL 7 1/8 05/13/54 368bp -2bp

COLOM 8 11/14/35 444bp -3bp

COLOM 8 3/8 11/07/54 531bp -2bp

ELSALV 7.65 06/15/35 451bp +1bp

MEX 6 7/8 05/13/37 289bp +0bp

MEX 7 3/8 05/13/55 354bp +1bp

CHILE 5.65 01/13/37 161bp -1bp

PANAMA 6.4 02/14/35 347bp -4bp

CSNABZ 5 7/8 04/08/32 635bp -6bp

MRFGBZ 3.95 01/29/31 348bp +1bp

PEMEX 7.69 01/23/50 696bp -4bp

CDEL 6.33 01/13/35 231bp -2bp

SUZANO 3 1/8 01/15/32 222bp -7bp

FX Level Δ DoD

USDBRL 5.68 +0.00

USDCLP 934.45 +0.02

USDMXN 19.5 -0.06

USDCOP 4217.65 -49.26

USDPEN 3.67 -0.00

CDS Level Δ DoD

Mexico 139 (2)

Brazil 183 (5)

Colombia 266 (5)

Chile 69 (2)

CDX EM 95.87 0.12

CDX EM IG 100.33 0.13

CDX EM HY 91.40 0.10

Main stories recap:

· Optimism about U.S. tariffs and better than expected U.S. consumer confidence data lifted global equities while U.S. Treasuries continued to rally with a parallel shift down in yields of about 5 bps.

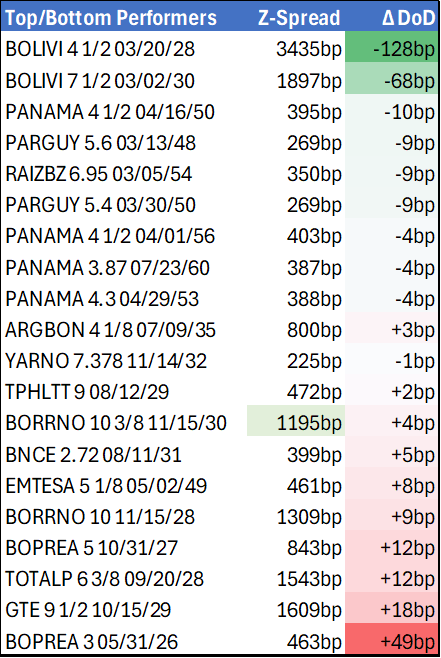

· EM credit rallied globally with high beta generally outperforming. In CEEMEA, African names Ghana, Mozambique and Zambia tightened 20-50bps while in LATAM the rally was a bit more subdued.

· Outperformers in LATAM included Brazil high yield corporate bonds that tightened 7-18bps like Raizen, CSN and Movida as well as Panama sovereign bonds which tightened 4 bps, benefitting from a fall in US Treasury yields, a wide spread for the rating in a rallying market and positive fundamental news.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Shows Through Near-Term Support

- RES 4: 1.4700 Round number resistance

- RES 3: 1.4641 76.4% retracement of the Feb 3 - 14 bear leg

- RES 2: 1.4452/4543 High Mar 13 / 4 and a bull trigger

- RES 1: 1.4402 High Mar 20

- PRICE: 1.4264 @ 16:51 GMT Mar 26

- SUP 1: 1.4235 Low Mar 26 and a key near-term support

- SUP 2: 1.4151/4107 Low Feb 14 / 50.0% of Sep 25 - Feb 3 bull run

- SUP 3: 1.4011 Low Dec 5 ‘24

- SUP 4: 1.3944 61.8% retracement of the Sep 25 ‘24 - Feb 3 bull cycle

USDCAD traded lower again Wednesday and traded through support at 1.4242, the Mar 6 low. Clearance of this level would undermine the bull theme and instead highlight potential for a test of 1.4151, the Feb 14 low and a bear trigger. Moving average studies continue to highlight a dominant uptrend. A reversal higher would refocus attention on the bull trigger at 1.4543, the Mar 4 high. First resistance is 1.4402, the Mar 20 high.

AUDUSD TECHS: Support Holds

- RES 4: 0.6429 High Dec 12 ‘24

- RES 3: 0.6414 38.2% retracement of the Sep 30 ‘24 - Feb 3 bear leg

- RES 2: 0.6409 High Feb 21 and a bull trigger

- RES 1: 0.6391 High Mar 17 / 18

- PRICE: 0.6307 @ 16:50 GMT Mar 26

- SUP 1: 0.6258 Low Mar 21

- SUP 2: 0.6187 Low Feb 4

- SUP 3: 0.6171/6088 Low Feb 4 / 3 and a key support

- SUP 4: 0.6045 1.500 proj of the Sep 30 - Nov 6 - 7 price swing

AUDUSD has recovered from its latest low. A short-term bull theme is intact and the latest move down appears corrective. Key short-term support to watch is 0.6187, the Mar 4 low. Clearance of this level would reinstate a bear threat. First support is at 0.6258, the Mar 21 low. A stronger recovery would refocus attention on 0.6409, the Feb 21 high. Clearance of this hurdle would strengthen a bull cycle and resume the uptrend that started Feb 3.

CANADA DATA: Wholesale Sales Slowed In Feb Per Estimate, Echoing Manufacturing

StatCan published a preliminary estimate that wholesale sales ex petroleum, products, other hydrocarbons, oilseed & grain rose 0.4% M/M in February.

- While still a prelim estimate, and a pullback from 1.2% in January, this would still mean elevated growth in wholesale sales on a 3M/3M annualized basis (7.4%, after 8.1%,), and the highest Y/Y rate (using SA series as a comparison) in 10 months (3.1%).

- The reading "reflects higher sales in the machinery, equipment and supplies subsector", per StatCan.

- Friday's GDP release brings expectations for a pickup in January growth to 0.3% M/M vs 0.2% prior - the chart below shows that after January's pickup in both wholesale and manufacturing sales, activity is seen to have weakened in February.