EM LATAM CREDIT: MNI EM Credit Market Wrap - LATAM (23 May)

Source: BBG

Measure Level Δ DoD

5yr UST 4.08% -1bp

10yr UST 4.51% -2bp

5s-10s UST 42.8 -1bp

WTI Crude 61.7 +0.5

Gold 3361 +66.3

Bonds (CBBT) Z-Sprd Δ DoD

ARGENT 3 1/2 07/09/41 861bp +5bp

BRAZIL 6 1/8 03/15/34 261bp +4bp

BRAZIL 7 1/8 05/13/54 371bp +4bp

COLOM 8 11/14/35 413bp +2bp

COLOM 8 3/8 11/07/54 504bp +2bp

ELSALV 7.65 06/15/35 446bp +4bp

MEX 6 7/8 05/13/37 280bp +4bp

MEX 7 3/8 05/13/55 345bp +5bp

CHILE 5.65 01/13/37 158bp +3bp

PANAMA 6.4 02/14/35 337bp +4bp

CSNABZ 5 7/8 04/08/32 563bp +5bp

MRFGBZ 3.95 01/29/31 277bp +6bp

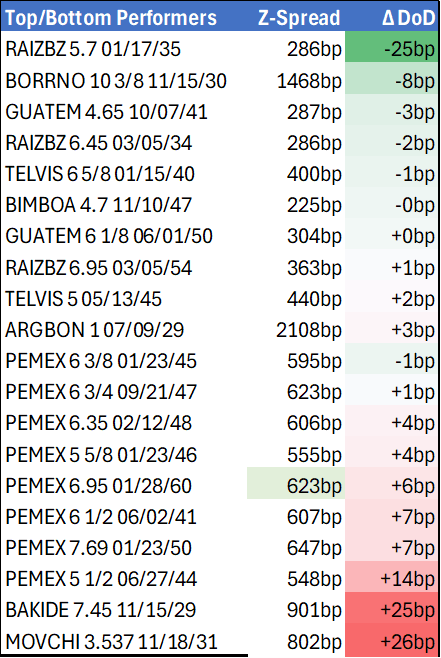

PEMEX 7.69 01/23/50 646bp +10bp

CDEL 6.33 01/13/35 217bp +4bp

SUZANO 3 1/8 01/15/32 216bp +4bp

FX Level Δ DoD

USDBRL 5.65 -0.06

USDCLP 938.95 -3.60

USDMXN 19.2 -0.07

USDCOP 4152.46 -22.88

USDPEN 3.66 +0.00

CDS Level Δ DoD

Mexico 122 1

Brazil 169 2

Colombia 230 1

Chile 59 1

CDX EM 96.66 (0.18)

CDX EM IG 100.78 (0.09)

CDX EM HY 92.45 (0.30)

Main stories recap:

Comments

· Stocks headed south and the U.S. Treasury curve steepened initially after President Trump threatened 50% tariffs on the European Union by June 1. As an added bonus, he also threatened all imported mobile phones with a 25% tariff.

· Stocks recovered and Treasuries closed relatively flat across the curve, but the damage was done in EM as spreads widened on benchmark CEEMEA bonds by about 0-5 bps and then LATAM similarly.

· Pemex underperformed, with bonds widening by about 10 bps. The Mexico owned oil and gas exploration and production company announced cost cuts and April production figures today, neither of which were significant enough to impact valuations or the credit profile.

· Brazil’s Raizen outperformed as bond spreads tightened about 10 bps on expectations of further asset sales to reduce debt.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Trade Wars Are Not an Easy Win, Negotiations Take Time

- Treasuries finishing near late session lows, curves continue to unwind Monday's sharp steepening with short end rates weaker vs. Bonds. Busy session for chasing tariff related headline risk.

- Treasuries opened higher as Pres Trump softened his stance on sacking Fed Chair Powell and reducing China tariffs, improved sentiment also lifting S&P eminis with ESM5 futures tapping 5499.75 high.

- Rates gapped higher briefly on a WSJ article that rehashed possible China tariff cuts, but support was short lived as markets assessed potential reductions, non-unilateral negotiations as well as comments from Tsy Sec Bessent's "in need of a rebalancing".

- US Treasury Secretary Bessent further stated that there is no unilateral offer from Trump to cut China tariffs, and that a full China trade deal could take two-to-three years.

- Tsy Jun'25 10Y futures currently -3.5 at 110-22 vs. session high of 111-18.5. Initial technical support at 110-15 (Apr 15 low) followed by 109-08 (bear trigger). Curves holding flatter profiles but off lows, 2s10s -5.713 at 52.252 (46.527 low), 5s30s -6.569 at 81.760 (77.371 low).

- Cross asset: Bbg US$ index near session high currently +6.84 a t 1228.46; stocks firmer but well off highs: SPX eminis +90.50 at 5405.25 (5499.75 high), Gold cratered: down over 103 at 3277.5 earlier trades 3295.5 at the moment, crude retreated as well (WTI -1.36 at 62.31).

USDCAD TECHS: Corrective Bounce

- RES 4: 1.4415 High Apr 1

- RES 3: 1.4296 High Apr 7

- RES 2: 1.4165 50-day EMA

- RES 1: 1.3906/4029 High Apr 17 / 20-day EMA

- PRICE: 1.3871 @ 16:29 BST Apr 23

- SUP 1: 1.3781 Low Apr 21

- SUP 2: 1.3744 76.4% retracement of Sep 25 ‘24 - Feb 3 bull run

- SUP 3: 1.3696 Low Oct 10 2024

- SUP 4: 1.3643 Low Oct 9 ‘24

A bearish theme in USDCAD remains intact for now despite Wednesday’s spot rally. Fresh cycle lows continue to highlight a resumption of the downtrend and signal scope for a continuation near-term. Potential is seen for a move towards 1.3744, a Fibonacci retracement. Moving average studies are in a bear -mode position, highlighting a dominant downtrend. First resistance to watch is 1.4029, the 20-day EMA.

PIPELINE: Corporate Bond Roundup: $4B Walmart Leads Midweek Supply

$11.85B to Price Wednesday

- Date $MM Issuer (Priced *, Launch #)

- 04/23 $4B *Walmart $750M 2Y +22, $750M 2Y SOFR+43, $1B 5Y +37, $1.5B 10Y +52

- 04/23 $2.25B #QXO Inc. 7NC3 6.75%

- 04/23 $1.5B *OCP $750M 5Y +235, $750M +10Y +260

- 04/23 $1.25B *Rentokil Terminix $750M 5Y +115, $500M 10Y +135,

- 04/23 $1B *Jane Street 8NC3 6.75%

- 04/23 $750M *Bank of Peru 10.25NC5 6.5%

- 04/23 $700M *Guardian Life 5Y +80

- 04/23 $400M *Hanwa Futureproof 3Y +95