EM LATAM CREDIT: MNI EM Credit Market Wrap - LATAM (16 May)

Source: BBG

Measure Level Δ DoD

5yr UST 4.07% +1bp

10yr UST 4.44% +1bp

5s-10s UST 37.1 -0bp

WTI Crude 62.4 +0.8

Gold 3199 -40.7

Bonds (CBBT) Z-Sprd Δ DoD

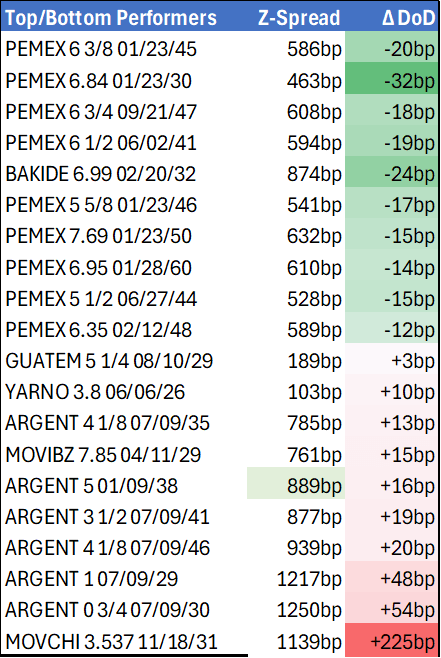

ARGENT 3 1/2 07/09/41 877bp +20bp

BRAZIL 6 1/8 03/15/34 257bp -3bp

BRAZIL 7 1/8 05/13/54 367bp -3bp

COLOM 8 11/14/35 412bp -5bp

COLOM 8 3/8 11/07/54 502bp -3bp

ELSALV 7.65 06/15/35 417bp -2bp

MEX 6 7/8 05/13/37 273bp -2bp

MEX 7 3/8 05/13/55 336bp -1bp

CHILE 5.65 01/13/37 152bp -4bp

PANAMA 6.4 02/14/35 321bp -4bp

CSNABZ 5 7/8 04/08/32 555bp -2bp

MRFGBZ 3.95 01/29/31 256bp -15bp

PEMEX 7.69 01/23/50 632bp -16bp

CDEL 6.33 01/13/35 201bp -2bp

SUZANO 3 1/8 01/15/32 210bp -3bp

FX Level Δ DoD

USDBRL 5.67 -0.02

USDCLP 942.78 +3.74

USDMXN 19.5 -0.03

USDCOP 4177.00 -23.38

USDPEN 3.69 -0.00

CDS Level Δ DoD

Mexico 121 (1)

Brazil 166 2

Colombia 226 (1)

Chile 57 (0)

CDX EM 96.97 0.06

CDX EM IG 100.95 0.01

CDX EM HY 92.93 0.11

Main stories recap:

Comments

· President Trump’s “big, beautiful bill” stalled out in the House budget committee as representatives debated how to pay for the tax cuts but that didn’t prevent U.S. equities from closing higher today. The committee is meeting again Sunday night so that may have left people sidelined until Monday.

· U.S. economic data was weaker than expected while consumer expectations for inflation were higher, but Treasuries were mostly unchanged as fiscal policy dominated sentiment.

· The EM primary market quieted down after a hectic week while in the secondary market Asia and CEEMEA benchmark spreads generally tightened.

· LATAM followed through with tighter spreads as well. Pemex and Marfrig outperformed. Pemex was following through from yesterday’s report from a large bank that raised their recommendation due to expected support from the Mexican government.

· Marfrig bond spreads tightened 15bps today on news that it would merge with BRF. Marfrig already owned 50.5% of BRF and proposed in a stock swap to buy the remaining balance.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US DATA: Treasury Cash Gains Look Healthy After Tax Day Take

The Treasury General Account soared by $185B on Tuesday's key tax collection day, to just over $600B - easily the highest cash level since late February.

- At this point, tax revenue is coming in at a pace almost exactly in line with 2024, at $270.3B collected in each year when considering corporate and individual collections for tax day and the preceding 5 days.

- Unusually, though, individual tax collection didn't jump as much as may have been expected on April 15: to $53B from $48B, suggesting that many individual taxpayers submitted on Monday instead of waiting for the Tuesday (in 2024, April 15 fell on a Monday).

- And also unusually for the April tax deadline day, corporate tax payments eclipsed their individual counterparts, coming in at $65B vs $24B the prior day (usually it's a little more spread out across days).

- Either way, the jump in the TGA is a good sign that estimates of the "x-date" for Treasury running out of cash will not have to be pulled forward as a result of the early tax take. We didn't see many estimates of today's collection but Wrightson ICAP estimated that the TGA would rise by $165B today, so this was eclipsed by $20B.

- As the chart below shows, this is easily the most important day for the TGA increase - and gains so far are tracking ahead of prior years.

US TSYS: Persistent Inflation Concerns on Larger Than Expected Tariffs

- Treasuries look to finish near late session highs Wednesday, gathering risk-off support as Fed Chair Powell discussed his outlook at the Chicago Economics Club, stocks extended lows (but drew some buying late). Chairman Powell warned inflation may be more persistent due to larger than expected tariffs, exacerbated by policy uncertainty.

- "I do think we'll be moving away from" the dual mandate goals "probably for the balance of this year. Or at least not making any progress, and then we'll resume that progress as we can," Powell said.

- Treasury Jun'25 10Y futures trade +11 at 111-13.5 after the bell vs. 111-17.5 high, just off technical resistance at 111-25 (50.0% retracement of the Apr 7 - 11 bear leg), 10Y yield at 4.2806% (-.0524). Curves are steeper but off first half highs: 2s10s +1.691 at 50.081, 5s30s +4.769 at 83.808.

- The NY Fed services business activity index was weaker than expected in April as it failed to bounce and instead dipped to -19.8 (cons -12.1, 4 responses) after -19.3 in March. Other important details within the report were notably glum, with the current business climate falling further to -60.7 from -51.7 (-21.8 in Jan having averaged -24.5 in 2024 for example) to its lowest since Feb 2021.

- March industrial production was largely as expected, with headline IP growing contracting by 0.3% M/M (-0.2% survey) but prior upwardly revised by 0.1pp (+0.8%). Manufacturing production rose by 0.3% (0.2% survey 1.0% prior upwardly revised from 0.9%). Capacity utilization fell slightly (77.8% vs 78.2% prior).

MNI: US TSY TICS NET FLOWS IN FEB +$284.7B

- MNI: US TSY TICS NET FLOWS IN FEB +$284.7B

- US TSY TICS NET L-T FLOWS IN FEB +$112.0B