EM LATAM CREDIT: MNI EM Credit Market Wrap - LATAM (07 May)

Source: BBG

Measure Level Δ DoD

5yr UST 3.87% -2bp

10yr UST 4.28% -2bp

5s-10s UST 40.4 +1bp

WTI Crude 58.0 -1.1

Gold 3374 -58.2

Bonds (CBBT) Z-Sprd Δ DoD

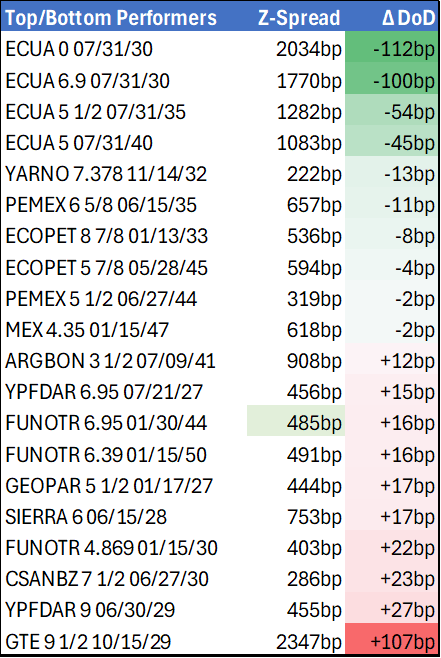

ARGENT 3 1/2 07/09/41 868bp -9bp

BRAZIL 6 1/8 03/15/34 278bp -1bp

BRAZIL 7 1/8 05/13/54 380bp -0bp

COLOM 8 11/14/35 450bp -3bp

COLOM 8 3/8 11/07/54 539bp -1bp

ELSALV 7.65 06/15/35 476bp -3bp

MEX 6 7/8 05/13/37 290bp -3bp

MEX 7 3/8 05/13/55 358bp -3bp

CHILE 5.65 01/13/37 160bp -2bp

PANAMA 6.4 02/14/35 342bp -2bp

CSNABZ 5 7/8 04/08/32 619bp -7bp

MRFGBZ 3.95 01/29/31 322bp -4bp

PEMEX 7.69 01/23/50 727bp -6bp

CDEL 6.33 01/13/35 214bp +0bp

SUZANO 3 1/8 01/15/32 227bp -3bp

FX Level Δ DoD

USDBRL 5.75 +0.04

USDCLP 945.73 +5.38

USDMXN 19.6 -0.06

USDCOP 4287.15 -17.92

USDPEN 3.65 -0.01

CDS Level Δ DoD

Mexico 138 (3)

Brazil 181 (0)

Colombia 266 (2)

Chile 69 0

CDX EM 95.84 0.07

CDX EM IG 100.32 0.03

CDX EM HY 91.32 0.12

Main stories recap:

Comments

· The Fed left the policy rate unchanged as expected while US equity prices advanced and US Treasury yields fell 2 bps.

· EM benchmark bond spreads generally tightened across Asia, CEEMEA and LATAM.

· Ecuador bonds outperformed with prices up nearly 2 points as market friendly president Noboa gained support from left leaning legislators in the national assembly.

· An overall tightening bias today helped Argentina bonds tighten about 10-15 bps as well.

· We got some earnings reports today from Brazil paper company Klabin as well as Chilean retailer Falabella and Colombia government majority owned energy company Ecopetrol. We didn’t see much market impact from the Klabin or Falabella news.

· Ecopetrol bonds tightened about 10 bps, but we attribute that more to overall market beta than fundamentals as earnings were lackluster.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Corrective Bounce

- RES 4: 1.4452/4543 High Mar 13 / 4 and a bull trigger

- RES 3: 1.4415 High Apr 1

- RES 2: 1.4304 50-day EMA

- RES 1: 1.4296 Intraday high

- PRICE: 1.4225 @ 16:58 BST Apr 7

- SUP 1: 1.4028 Low Apr 3

- SUP 2: 1.3986 Low Dec 2 ‘24

- SUP 3: 1.3944 61.8% retracement of Sep 25 ‘24 - Feb 3 bull run

- SUP 4: 1.3894 Low Nov 11 ‘24

USDCAD has recovered from last week’s low. For now, the move higher appears corrective. The sell-off last week confirmed a clear reversal of the bull cycle between Sep 25 ‘24 and Feb 3. Price has traded through a key support at 1.4151, the Feb 14 low, and this signals scope for an extension towards 1.3944, a Fibonacci retracement. On the upside, key short-term resistance is seen at 1.4304, the 50-day EMA.

US DATA: Surprise Pause In Consumer Credit Growth Back In February

- Consumer credit surprisingly fell by $0.8bn in February vs expectations of a $15bn increase.

- It also followed sizeable downward revisions, with $8.9bn in Jan ($18.1bn initially) and $27.1bn in Dec ($37.1bn) although there was an upward revision to -$5.6bn ($14.0bn) back in November.

- Credit growth therefore essentially paused in February (and in both revolving, +0.1bn, and non-revolving, -$0.9bn alike) in the first month under limited tariff announcements (10% tariff on China announced Feb 1, 25% tariffs on steel & aluminum to come Mar 12 and floating idea of reciprocal tariffs).

- The sudden pullback in credit growth is surprising considering surveys such as today’s Dallas Fed’s banking survey taken Mar 24 – Apr 2, which showed a notable moderation in loan demand but to levels that were still stronger than much of 2023-2024.

- However, the credit impulse on a 3mth vs 3mths a year ago basis is still mildly positive after the very strong $27.1bn increase in credit the month after the presidential election despite the above downward revisions. It has however waned from a brief positive boost seen in late 2024 - see charts.

US TSYS: Heavy Volumes, Exceedingly Wide Ranges As Tariff Negotiations Proceed

- Treasuries look to finish weaker, low end of very wide range (TYM5 111-15.5 low vs. 114-10 overnight high) as markets started to anticipate easing impact from last week's sweeping tariff announcement as more countries look to negotiate or at least respond to the Trump administrations trade policy.

- Heavy volumes (TYM5 over 5.3M after the bell) trades -13.5 at 112-02, curves steper: 2s10s +7.370 at 40.989 (32.805 low vs. 45.006 high), 5s30s +4.087 at 74.100.

- Sharp risk-off tone early overnight buoyed Tsys (10Y yield tapped 3.8693% low before bouncing to 4.2122% during morning trade) as stocks gapped lower on the open. Focus squarely on US tariffs and foreign countries response - rates gapped lower midmorning but quickly rebounded after erroneous headline of 90 day tariff delay made the rounds.

- Bbg reported that “Trump administration officials are debating the merits of creating a new exporter tax credit, a move that offers an implicit acknowledgment of the harm that the White House’s tariff policies risk inflicting on US companies.”

- Dearth of economic data today and tomorrow, focus on Wednesday's March FOMC minutes, CPI data on Thursday and PPI on Friday.