EM LATAM CREDIT: MNI EM Credit Market Wrap - LATAM (06 May)

Source: BBG

Measure Level Δ DoD

5yr UST 3.90% -4bp

10yr UST 4.30% -4bp

5s-10s UST 40.5 +0bp

WTI Crude 59.0 +1.9

Gold 3420 +86.1

Bonds (CBBT) Z-Sprd Δ DoD

ARGENT 3 1/2 07/09/41 879bp -5bp

BRAZIL 6 1/8 03/15/34 278bp -1bp

BRAZIL 7 1/8 05/13/54 379bp +3bp

COLOM 8 11/14/35 452bp -3bp

COLOM 8 3/8 11/07/54 539bp -3bp

ELSALV 7.65 06/15/35 478bp +4bp

MEX 6 7/8 05/13/37 292bp -4bp

MEX 7 3/8 05/13/55 360bp -3bp

CHILE 5.65 01/13/37 163bp -0bp

PANAMA 6.4 02/14/35 343bp -1bp

CSNABZ 5 7/8 04/08/32 627bp -3bp

MRFGBZ 3.95 01/29/31 325bp +5bp

PEMEX 7.69 01/23/50 732bp +6bp

CDEL 6.33 01/13/35 213bp +4bp

SUZANO 3 1/8 01/15/32 229bp +2bp

FX Level Δ DoD

USDBRL 5.71 +0.02

USDCLP 940.25 -1.33

USDMXN 19.7 -0.04

USDCOP 4305.07 +5.02

USDPEN 3.65 -0.01

CDS Level Δ DoD

Mexico 140 (3)

Brazil 181 (2)

Colombia 267 (4)

Chile 69 (2)

CDX EM 95.79 0.15

CDX EM IG 100.30 0.04

CDX EM HY 91.22 0.17

Main stories recap:

Comments

· U.S. equities pulled back today amid further trade policy anxiety as President Trump met with the newly elected Prime Minister of Canada Mark Carney.

· U.S. Treasury yields glided lower ahead of tomorrow’s Federal Reserve meeting when policymakers were expected to leave the Fed Funds rate unchanged. A USD42bn 10-year Treasury auction was well received, pricing 1 bp through the 10-year yield at the 1pm cutoff.

· Oil prices recovered 3% as US domestic producers seemed to react to the recent weakness by announcing cuts in production plans.

· The EM primary market marched on while the window remained open with a financial out of Korea, two gold miners from CEEMEA and two Colombian issuers in LATAM.

· Both LATAM issues were effectively inaugural as one of the companies hadn’t issued an international bond in 8 years and for the other a new Bloomberg ticker was created.

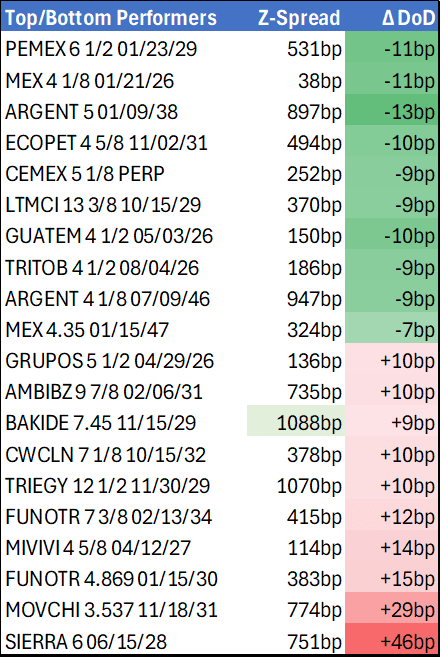

· Benchmark bond spreads generally widened though we finally saw bounce back in some oil related credits with the recovery in oil prices today. Bonds of Colombia and government controlled energy company Ecopetrol tightened 4-9 bps across the curves.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 10-YEAR TECHS: (M5) Strong S/T Bounce

- RES 3: 96.501 - 76.4% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 2: 96.207 - 61.8% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 1: 95.915 - High Apr 4

- PRICE: 95.860 @ 16:42 GMT Apr 04

- SUP 1: 95.420/95.300 - Low Feb 13 / Low Jan 14

- SUP 2: 95.275 - Low Nov 14 (cont) and a key support

- SUP 3: 94.640 - 1.0% 10-dma envelope

Aussie 10-yr futures extended a recent strong bounce through to the Friday close, putting prices through the top end of the recent range. The confirmed breach of 95.851, the Dec 11 high on the continuation contract, reinstates a bull cycle and focuses attention on resistance at 96.207, a Fibonacci retracement point. A stronger bearish theme would expose 95.275, the Nov 14 low and a key support. Clearance of this level would strengthen a bearish condition.

USDCAD TECHS: Bearish Structure

- RES 4: 1.4452/4543 High Mar 13 / 4 and a bull trigger

- RES 3: 1.4415 High Apr 1

- RES 2: 1.4308 50-day EMA

- RES 1: 1.4242 High Apr 4

- PRICE: 1.4196 @ 17:10 BST Apr 4

- SUP 1: 1.4028 Low Apr 3

- SUP 2: 1.3986 Low Dec 2 ‘24

- SUP 3: 1.3944 61.8% retracement of Sep 25 ‘24 - Feb 3 bull run

- SUP 4: 1.3894 Low Nov 11 ‘24

USDCAD rallied Friday, but remains lower on the week after Thursday’s downleg. The move down has confirmed a clear reversal of the bull cycle between Sep 25 ‘24 and Feb 3. Price is through a key support at 1.4151, the Feb 14 low. This signals scope for an extension towards 1.3944, a Fibonacci retracement. On the upside, key short-term resistance is seen at 1.4308, the 50-day EMA.

CANADA DATA: Unexpected Jobs Contraction Boosts Implied April BOC Cut Chances

Canadian employment unexpectedly contracted in March, falling by the most since January 2022 at -32.6k (+10.0k expected, +1.1k prior) in a sign that the trade war with the US is spilling over increasingly into the "hard" data. The unemployment rate ticked up 0.1pp to 6.7%, in line with expectations and below the November 6.9% high, though unrounded it rose from 6.55% to 6.71% - the largest increase since November.

- The drop in employment was largely due to a 62.0k drop in full-time positions (after -19.7k, the 2nd straight drop), with part-time up for the 4th consecutive month at 29.5k (after 20.8k prior) - that mix is clearly indicative of hiring uncertainty among firms.

- The monthly full-time drop was the 2nd largest since the pandemic lows in the labour market (April 2020). Goods producing jobs fell by 12k (2nd consecutive decline), while services shed 21k (wholesale/retail trade and Information, culture and recreation led losses).

- The participation rate dipped 0.1pp to 65.2%.

- Wages were soft, dropping 0.2% M/M for the first drop since November, with the Y/Y rate slipping to 3.6% from 3.8% prior. The rise in permanent employees' wages of 3.5% Y/Y was well below the 4.1% expected (4.0% prior).

- Market-implied probability of an April BOC rate cut rose to as high as 68% after the data before settling the day at around 55%. That compares to 40% prior to Wednesday's US tariffs announcement.