EM ASIA CREDIT: MNI EM Credit Market Update - Asia

Asia emerging markets USD sovereign and agency spreads have a positive bias this morning, with spreads up to 1bp tighter. Regional equities are more or less unchanged on the day, with no particular outliers. In terms of primary, the USD Malayan Bank 3Y, the USD Agricultural Bank of China 2Y and the EUR Korea Land & Housing Corporation 3Y priced overnight, and mostly around our fair value estimates. This morning China Resources Land launched a new USD 3Y deal (and CNH) and we see fair value around T+81bp area versus an IPT of T+120bp area.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

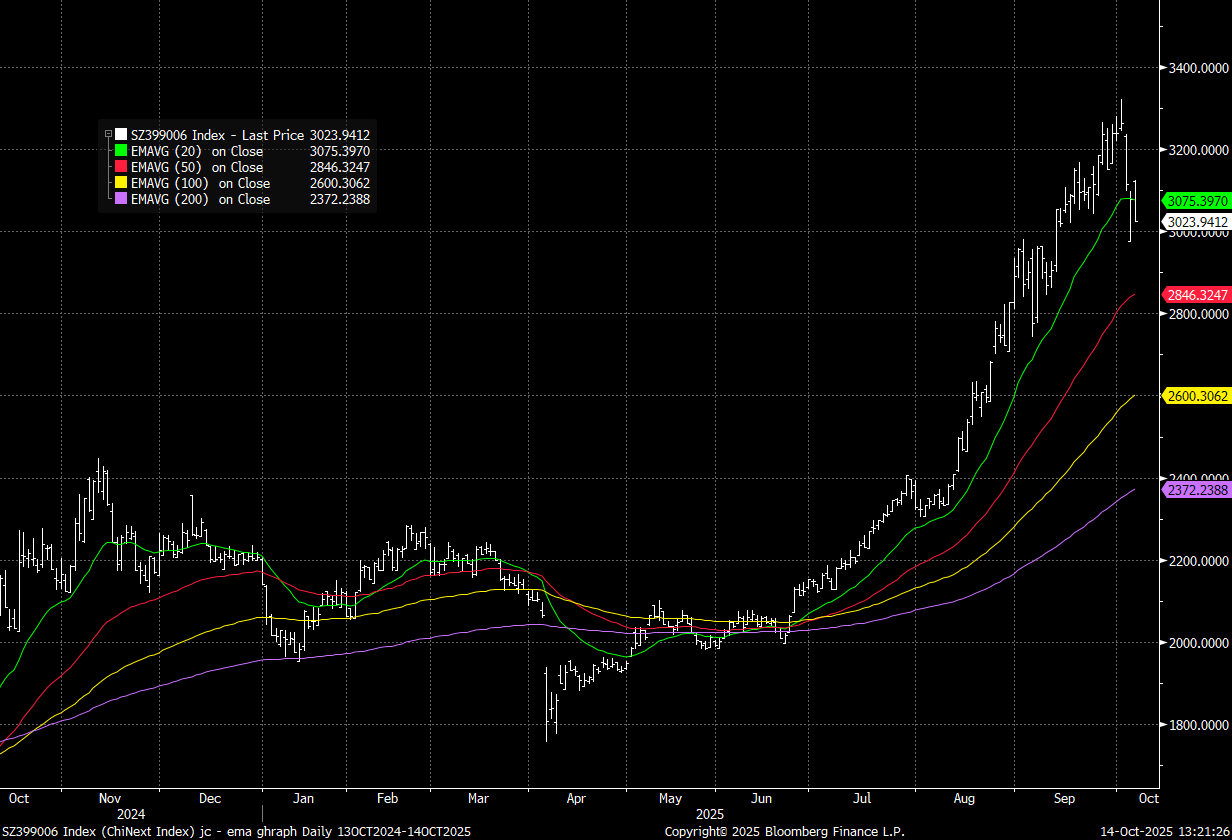

CHINA STOCKS: China/HK Equities Still Struggling Despite Better Global Trends

China/HK equities still struggling to maintain positive momentum, despite the broader gains seen over the past 24hrs in global equities. With sentiment stabilizing amid Trump's softer comments around China. Positioning/valuation concerns (tech headwinds amid export control fears) may also be playing a role. Chipmaker Wingtech also down earlier today after the Dutch government took control of its Nexperia unit.

- The Chinext is plotted in the attached, still above yesterday's intra-session lows, but sub 20-day EMA.

Fig 1: Chinext Equity Index Versus Key

Source: Bloomberg Finance/MNI

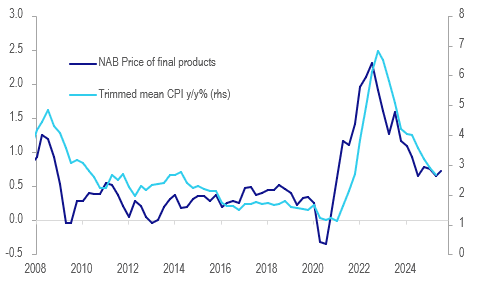

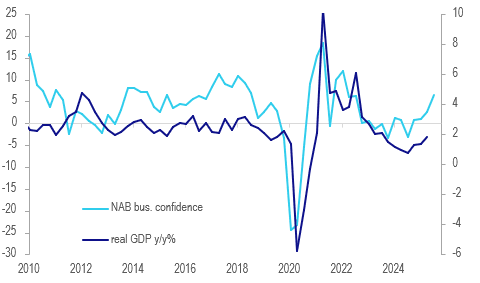

AUSTRALIA DATA: NAB Survey Shows Recovery Continued & Inflation Stable In Q3

The September NAB business survey showed the gradual recovery in the Australian economy continued. Business confidence rose to 7.3 from 4.3 while conditions were similar to August at 7.6. The Q3 averages though were their highest since Q1 2022 and Q2 2024 respectively, suggesting stronger Q3 GDP growth. While the price/cost components were a bit higher in September, they were little changed in Q3 signalling steady inflation. The data are consistent with activity picking up and concerns that disinflation has stalled, and so with the RBA remaining cautious.

Australia NAB business prices vs trimmed mean CPI %

- Given the volatility amongst some of the components of the monthly NAB survey, it is worth looking at Q3 averages to gauge the recovery and inflation picture in the quarter. Its measure of labour demand fell over 2 points to 2.9 in September but the Q3 average was stable at 3.5 consistent with the RBA’s assessment that labour market conditions are “broadly stable”. September jobs print Thursday and a 0.1pp rise in the unemployment rate to 4.3% is forecast.

- The increase in September business conditions was driven by a pickup in trading to 16.0, its highest since November 2023, and profitability to 5.9, best in almost 18 months. However, forward orders declined to -2.3 from +1.1 but while still weak in Q3 improved one point to -0.5.

- Average Q3 labour cost growth was steady at 1.6% 3m/3m while purchase costs moderated 0.1pp to 1.4% (it has held around 1.5% for 6 consecutive quarters). Final product prices rose 0.7% 3m/3m, in line with 2025 average, while retail prices increased 0.8% down from Q2’s 1.0%, lowest since Covid-impacted Q4 2020. Cost, retail and final product price growth rose in September while labour costs fell 0.1pp.

Australia NAB business confidence vs GDP y/y%

Source: MNI - Market News/LSEG

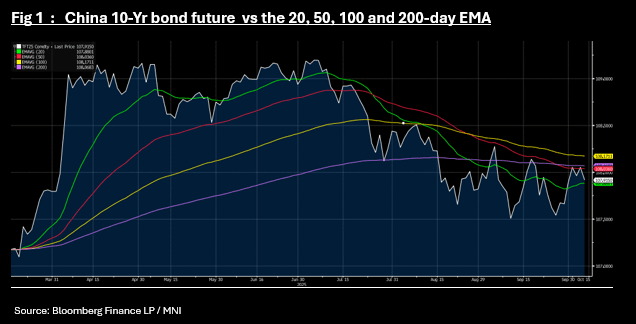

CHINA: 10-Yr Bond Future Tests Key Technical

- Bond futures are lower in morning trade, with the 10-Yr down -0.14 as equities open stronger.

- The fall in the 10-Yr saw the future trade near to the 20-day EMA of 107.87, failing to break below.

- The 2-Yr is down -0.02 at 102.346 to move further below all major moving averages.

- The 10-Yr CGB is up marginally in yield at 1.85% and continues to trade in tight ranges between 1.80% - 1.90% and has been unable to break clear of this range, despite the issuance across central and regional government and despite the absence of PBOC buying. The equity strength of late has failed to push yields dramatically higher either suggesting that we could be in this range for the near term or until further policy were to be announced.

- China is issuing CNY40 bn of 2045 bonds today as the key issuance for the week.