EM ASIA CREDIT: MNI EM Credit Market Update - Asia

Asia Emerging Markets USD sovereign and agency spreads are trading within a -2bp to +5bp range this morning, with Malaysia as the main outlier. Our USD proxy (KNBZMK 34s) tightened another 2bp today. Regional equities, except for the Korean KOSPI which gained 0.6%, are generally trending lower.

On the news front, ANZ Bank announced AUD1.1bn of charges relating amongst other items to redundancies and regulatory fines, most of which were already public information, market impact neutral. China Vanke reported very weak results overnight, as expected, with Shenzhen Metro’s support necessary to meet future obligations, overall negative for credit.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Cash Bonds Little Changed At Lunch

At the Tokyo lunch break, JGB futures are stronger, +11 compared to settlement levels.

- The Q3 Tankan survey printed in line with expectations and Q2 but FY25 capex intentions increased 1pp to 12.5%. Large company business conditions have been moving sideways at a solid level since the start of last year, especially for the non-manufacturing sector.

- The large manufacturers' index rose 1 point to 14 in Q3 while the outlook for Q4 is forecast to deteriorate 2 points. The series has not been affected by new US tariffs and the 2025 average is slightly higher than 2024's.

- Non-manufacturers' conditions were steady at 34, well above the series average of +7.3, with the outlook at 28.

- Small non-manufacturers are also outperforming manufacturers with the index at 14 (down 1 point) compared to +1 (stable). The outlook for both sectors improved 1 point.

- The September BoJ summary of opinions showed a bias towards a resumption of tightening.

- (Bloomberg) Japan will get its second prime minister in just over a year when the ruling Liberal Democratic Party holds a leadership election on Oct. 4.

- Cash US tsys are slightly mixed, with a steepening bias, in today's Asia-Pac session after yesterday's modest twist-steepener.

- Cash JGBs are little changed across benchmarks.

- Swap rates are flat to 1bp lower, with a steepening bias. Swap spreads are mixed.

AUSSIE BONDS: Holding Cheaper, Market Continues To Price Out RBA Cut

ACGBs (YM -4.0 & XM -5.5) remain weaker.

- S&P Global PMI Manufacturing Index falls to 51.4 from 53 in Aug.

- Cash US tsys are slightly cheaper in today's Asia-Pac session after yesterday's modest twist-steepener.

- Cash ACGBs are 4-7bps cheaper with the AU-US 10-year yield differential at +22bps.

- The latest ACGB Dec-34 supply achieved a weighted average yield that printed 0.40bp through prevailing mids (per Yieldbroker). However, the cover ratio decreased to 2.1033x, thelowest since its debut in 2023, from 3.1708x.

- The bills strip is -4 to -6 beyond the first contract.

- RBA-dated OIS pricing has firmed modestly across meetings following yesterday’s RBA Policy Decision. Pricing across meetings is 1-4bps firmer than yesterday’s pre-RBA levels. Notably, this post-RBA move leaves pricing some 10-19bps firmer than last Wednesday’s pre-CPI levels.

- A 25bp rate cut in October is given a 35% probability, with a cumulative 11bps of easing priced by year-end.

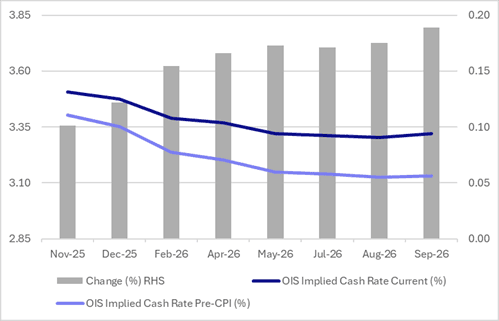

STIR: RBA Dated OIS’ Firming Since August CPI Extends After RBA Decision

RBA-dated OIS pricing has firmed modestly across meetings following yesterday’s RBA Policy Decision.

- At the time of writing, pricing across meetings was 1-4bps firmer than yesterday’s pre-RBA levels.

- Notably, this post-RBA move leaves pricing some 10-19bps firmer than last Wednesday’s pre-CPI levels.

- A 25bp rate cut in October is given a 35% probability, with a cumulative 11bps of easing priced by year-end.

Figure 1: RBA-Dated OIS – Current Vs. Pre-CPI

Source: Bloomberg Finance LP / MNI