EM ASIA CREDIT: MNI EM Credit Market Update - Asia

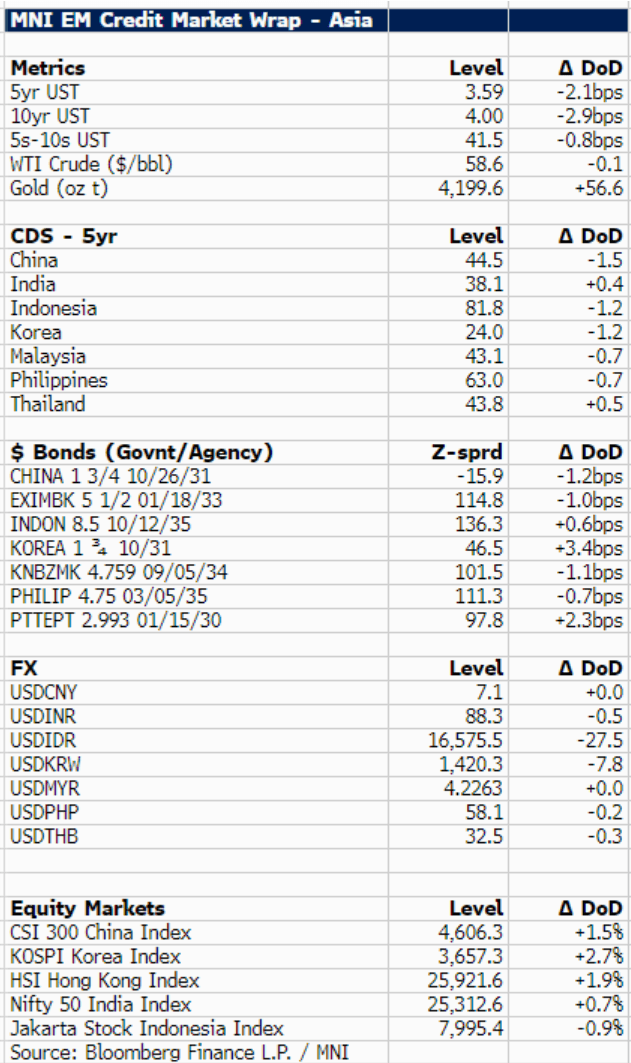

10-year US treasury yields were around 3bp lower at 4.0%, as Fed Chairman Powell stated inflation and employment outlooks remained stable since September, leaving two more rate cuts this year on the table.

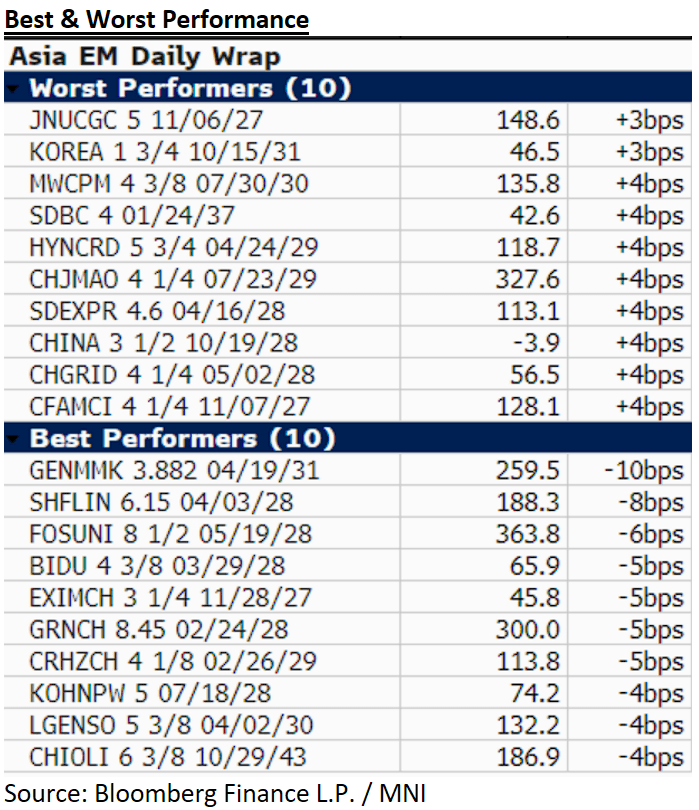

We followed LATAM, where secondary benchmark spreads were mixed, Brazilian corporate bonds recovered from significant losses late last week, such as Raizen up 5 points and CSN up nearly 3 points. Argentina sovereign bonds ended the day lower.

Asia EM USD sovereign and agency spreads traded in a -1bp to +2bp today, while regional equities are mostly in positive territory, led by the Korean KOSPI (+2.7%).

In primary markets, KEB Hana Bank priced its 5Y USD deal overnight broadly in line with fair value (T+43bp). China Water Affairs brought a USD 5NC3 deal (IPT 6.375% area; our fair value around 6.2%), while Korea has mandated banks for a new USD 5Y issue likely to come next week. Separately, Sunac China’s creditors have agreed to the company’s restructuring plan.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITIES: ROLL PACE - Triple Witching Friday

EQUITY ROLL PACE: Some might favour rolling earlier, ahead of the FOMC.

US:

- ESA: 26%.

- NQA: 13% (below pace).

- DOW: 20% (below pace).

EU:

- VGA: 10% (below pace).

- Banks: 7% (below pace).

- Stoxx600: 9% (below pace).

- Dax: 10% (below pace).

- FTSE: 13% (below pace).

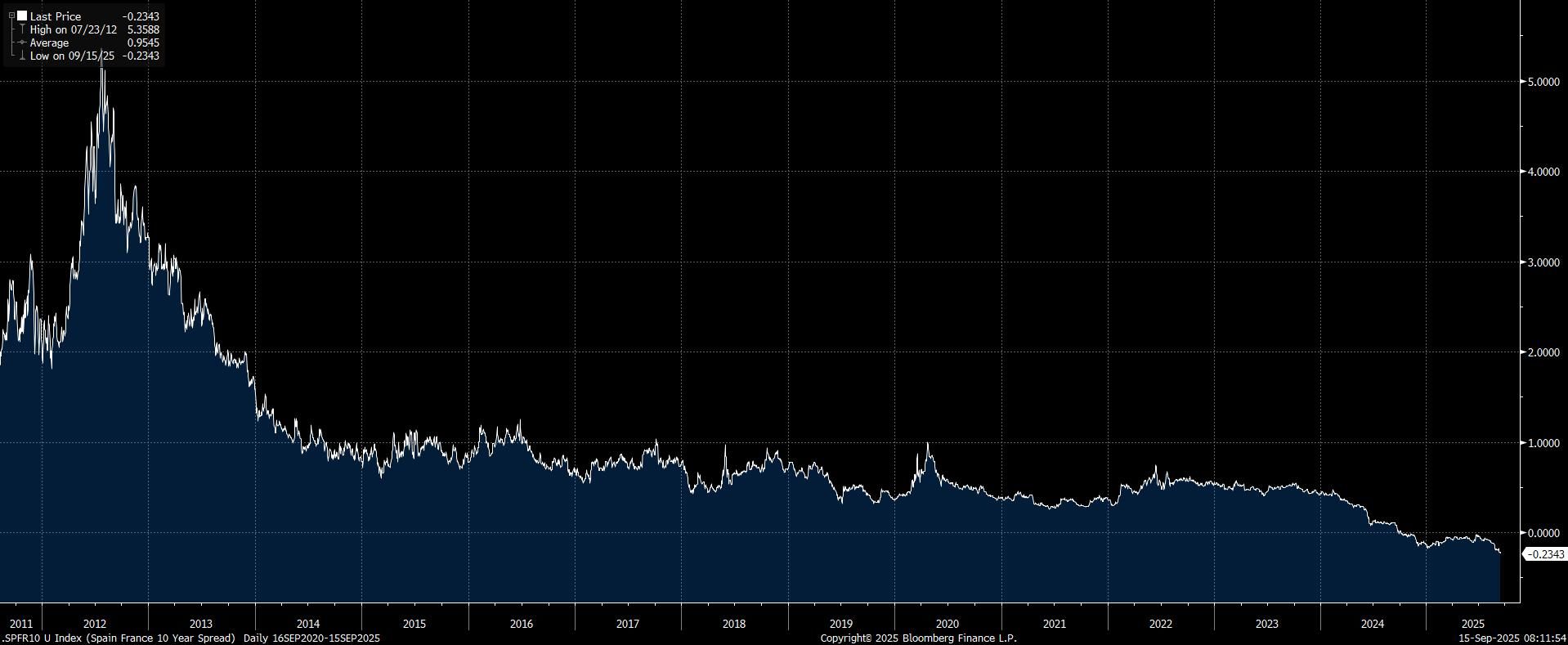

EGBS: OATs Lag Iberians As Ratings Convergence Continues

Friday’s rating actions help drive moves in EGB spreads early today, with Spanish (S&P upgraded Spain to A+; Outlook Stable) & Portuguese (Fitch upgraded Portugal to A; Outlook Stable) 10s flat vs. Bunds, while French paper is ~1.5bp wider (Fitch downgraded France to A+; Outlook Stable).

- Friday’s moves underscored the idea of rating convergence between France & the Iberians, given the political and fiscal risk evident in the former.

- The 10-Year Spain/France/Portugal fly is on track for a fresh cycle closing low, trading through -23bp.

- We highlighted the likelihood of the moves for both France and Portugal last week.

- Commerzbank suggests that the fallout for OATS is “likely to be limited, given that OATs are already trading markedly cheaper than double-A or single-A rated peers. While some investors may start to reduce single-A OAT exposure, others may use average ratings, adjust the rating thresholds in their EGB benchmarks, or utilise more attractive spread levels. We close our tactical OAT-Bund spread tightening view and turn neutral for the time being”.

Fig. 1: 10-Year Spain/France/Portugal Butterfly (bp)

SILVER TECHS: Continues To Appreciate

- RES 4: $43.000 - Round number resistance

- RES 3: $42.974 - 2.382 proj of the Jul 31 - Aug 14 - 20 price swing

- RES 2: $42.606 - 2.236 proj of the Jul 31 - Aug 14 - 20 price swing

- RES 1: $42.464 - HIgh Sep 12

- PRICE: $42.160 @ 08:13 BST Sep 15

- SUP 1: $40.195 - 20-day EMA

- SUP 2: $38.745 - 50-day EMA

- SUP 3: $36.216 - Low Jul 31 and a key support

- SUP 4: $35.285 - Low Jun 24

Trend signals in Silver remain bullish. The metal traded higher Friday and this delivered a fresh cycle high. The extension confirms a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Moving average studies are in a bull-mode position, reinforcing current trend conditions. Sights are on $42.606 next, a Fibonacci projection. Initial support to watch is $40.195, the 20-day EMA.