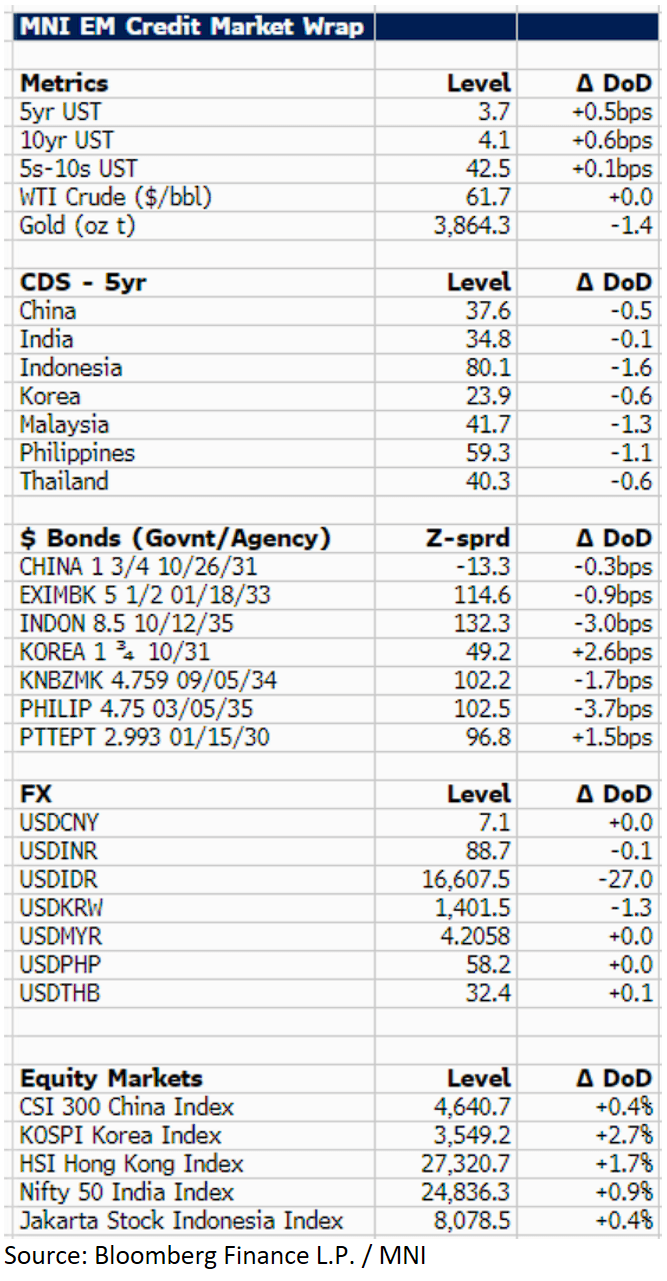

EM ASIA CREDIT: MNI EM Credit Market Update - Asia

US Treasury yields are 1bp higher at 4.2% with the US government shutdown underway. In LATAM hours, USD benchmark spreads widened 5–10bp, while in contrast Asia spreads were 1–4bp tighter today. Thailand was the main outlier, a couple of basis points wider, after the deputy finance minister highlighted the need to maintain currency stability. Regional equities are higher, led by the KOSPI (+2.7%) with SK Square (+16%) and SK Hynix (+10%) rallying after SK Hynix struck a chip supply deal with OpenAI for its Stargate data centres. Separately, Moody’s revised JSW Steel’s outlook to positive from stable as leverage is expected to keep improving. No new issuance reported.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: EUREX Roll pace update

EUREX ROLL PACE: Volumes are starting to pick up now, especially in Bobl.

- Buxl: 30%.

- Bund: 23%.

- Bobl: 32%.

- Schatz: 27%.

- BTP: 15% (below pace).

- BTS: 21%.

- OAT: 26%.

FOREX: Yield Pressures Culminate in Early USD Rally; GBP/USD Hit Hardest

In tandem with the step lower in GBP/USD at the open, the USD is rallying against all others - benefiting from the pretty aggressive move in longer-end yields. US 30y yields are within range of 5.0% for the first time since mid-July and that, compounded by the slippage in equities, is driving the USD here.

- As a result, GBP/USD is narrowing in on the Friday low, EUR/USD is through yesterday's lows and USD/JPY is closing in on clustered resistance between Y148.78-88, marking the Aug22 high and the 200-dma respectively.

- Move most observable against JPY and GBP here, with the impact of Gilt weakness and widening US-JN yield spreads making themselves be felt most keenly. UK DMP output price expectations data and retail sales could prove illustrative this week - but it's UK politics that will likely provide the clearer medium-term driver, as 30 year yields hit levels not seen in over 25 years today - pressuring the government headed into the Autumn budget - the date for which is yet to be set.

EGB SYNDICATION: Italy New 7y/30y Dual Tranche: Guidance

New 7-year Nov-32 BTP:

- Guidance: BTPS+10 Area. Benchmark: BTPS 3.25% 07/15/32

- Size: Benchmark. MNI pencils in E5-10bln (with risks skewed towards E7-8bln)

- Coupon: Semi-annual, act/act, short first

New 30-year Oct-55 BTP:

- Guidance: BTPS+9 Area. Benchmark: BTPS 4.3% 10/01/54

- Size: E5bln WNG.

- Coupon: Semi-annual, act/act, short first

Across both lines:

- Issuer: Italy Buoni Poliennali Del Tesoro (BTPS)

- Exp. Ratings: Baa3/BBB+/BBB

- Format: Reg S, dematerialized, 144A eligible

- Settlement: Sep 9, 2025 (t+5)

- Denoms: 1k x 1k

- Bookrunners: BBVA, Citi, DB (B&D), JPM, MS, Nomura

- Timing: May price today.

As per Bloomberg and MEF, with MNI colour added.