EM ASIA CREDIT: MNI EM Credit Market Update - Asia

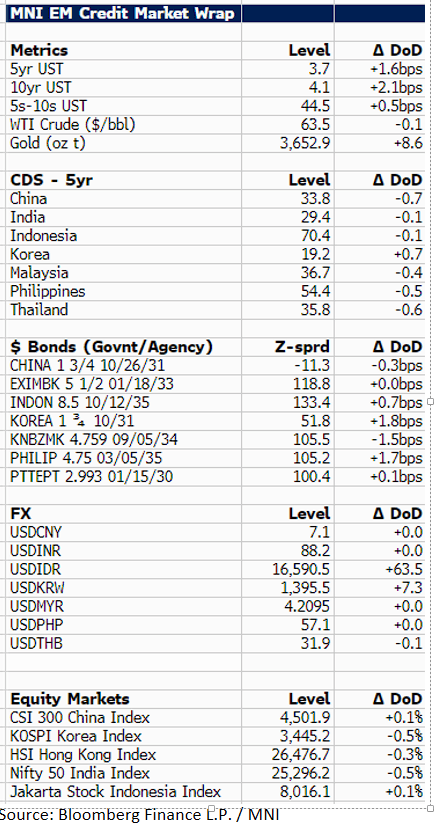

US Treasury yields are 2bp higher at 4.1% during the Asia session. We tracked LATAM developments, where Argentina’s sovereign bonds declined about 4 points today, pressured by the central bank’s use of scarce USD reserves to intervene in the foreign exchange market.

In Asia, EM USD sovereign and agency spreads traded within a narrow -2bp to +2bp range, with no significant outliers. Asia equities were marginally lower.

In South Korea, government plans to restructure the steel industry due to oversupply and global pressures are moving forward. Hyundai Motors downgraded its 2025 operating margin target to 6-7% from 7-8%, citing tariff-related costs, spreads remained unchanged.

In India, Adani Ports were cleared by the securities regulator SEBI of some allegations made by now-defunct short-seller Hindenburg Research, and spreads improved by a few basis points.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: RIKSBANK SEES SOME PROBABILITY OF FURTHER CUT THIS YEAR

- MNI RIKSBANK LEAVES POLICY RATE ON HOLD AT 2.0%:

SEK: Weakening Into Riksbank

SEK is weakening a little into the Riksbank decision. EURSEK up 0.2% at 11.1996 at typing. Initial resistance the August 7 high at 11.2206.

GILTS: Off Early Lows

Gilts see similar price action to GBP STIRs at the open, moving lower, before recovering on cues from EGBs and the lack of meaningful hawkish repricing in the short end in the wake of the CPI data (we detailed the reasons why we thought that would be the case ahead of time).

- Futures traded as low as 90.54 before recovering to 90.77.

- Bears remain in technical control, initial support and resistance located at 90.43/91.32.

- Yields ~1.5bp lower across the curve.

- The May high in 10s (4.80%) remains untouched.

- 50s have pierced 5.00% over the past couple of sessions, but bears failed to force a meaningful move above the psychological level, 4.965% last.

- Outside of the CPI data, Brightmine wage growth (released overnight) once again held steady at 3.0% in Y/Y terms for the three months through July.

- Little of note on the UK macro calendar for the remainder of the day.