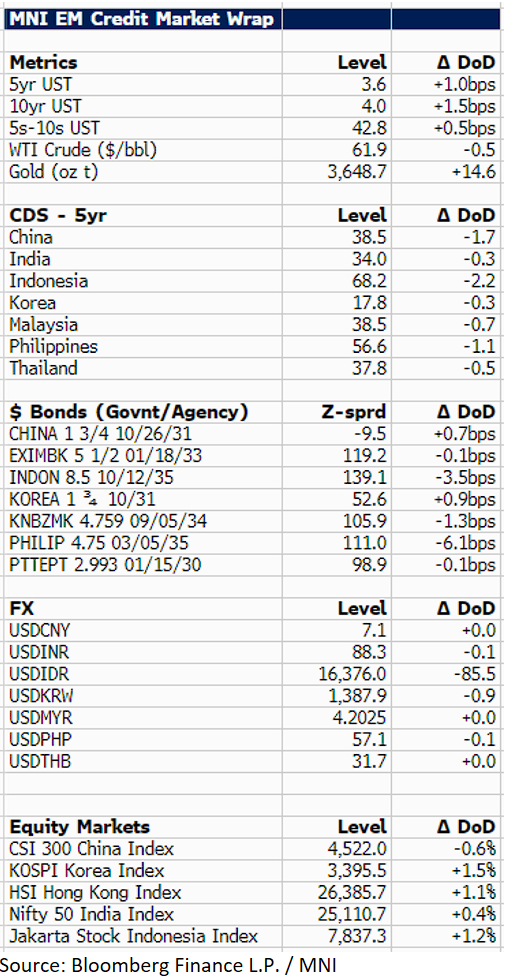

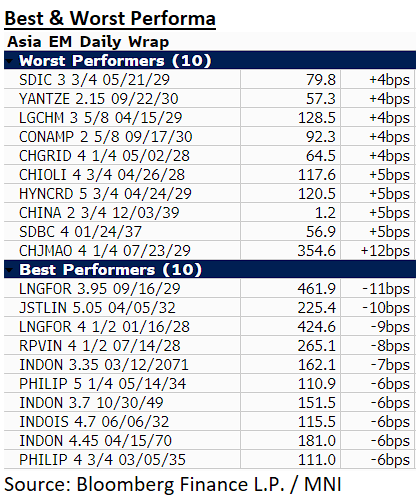

EM ASIA CREDIT: MNI EM Credit Market Update - Asia

US Treasury yields are 1bp higher at 4.0% during the Asia session. We followed LATAM, where USD benchmark bonds were for the most part 2-3bp better, with markets awaiting any moves by U.S. President Trump in response to Brazil’s Supreme Court sentencing of Jair Bolsonaro for over 27 years in prison. In Asia, EM USD sovereign and agency spreads also traded tighter, with the Philippines outperforming (PHILIP 35s -6bp). Regional equities were higher, with the Hang Seng +1.5% leading the pack.

In other news, SK Hynix announced it was ready to mass produce its HBM4 memory chip, a positive development - equities like it (+7%) and credit also better (HYUELE $ 30s, -2bp). Adani Ports made it clear to shipowners and operators that sanctioned vessels will not be welcomed at Adani ports, perhaps a pre-emptive move while India and US trade talks are ongoing. Hyundai confirmed that the repatriation of Korean workers from the US would delay battery plan construction for 2-3 months. No new issues today, but we expect the a new $ deal from the Export-Import Bank of Korea next week, and potentially a deal from Korean Air Lines.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BUNDS: ING Wary Of Higher Long-End Yields & Steeper Curves

ING believe that “the long end will remain susceptible to yield increases”.

- “10s30s is testing the highs of 2021 again, but more common when the ECB rate cycle bottomed were curves of 60bp and beyond. Also, the underlying swap curve is still some 20bp away from the highs of 2021”.

- They still expect “further pressure to materialise for (ultra-) long-end rates from German fiscal policies as well as the ongoing transition of Dutch pension funds to the new defined contribution system. And that is on top of any bearish impulses that could still come from outside the Eurozone”.

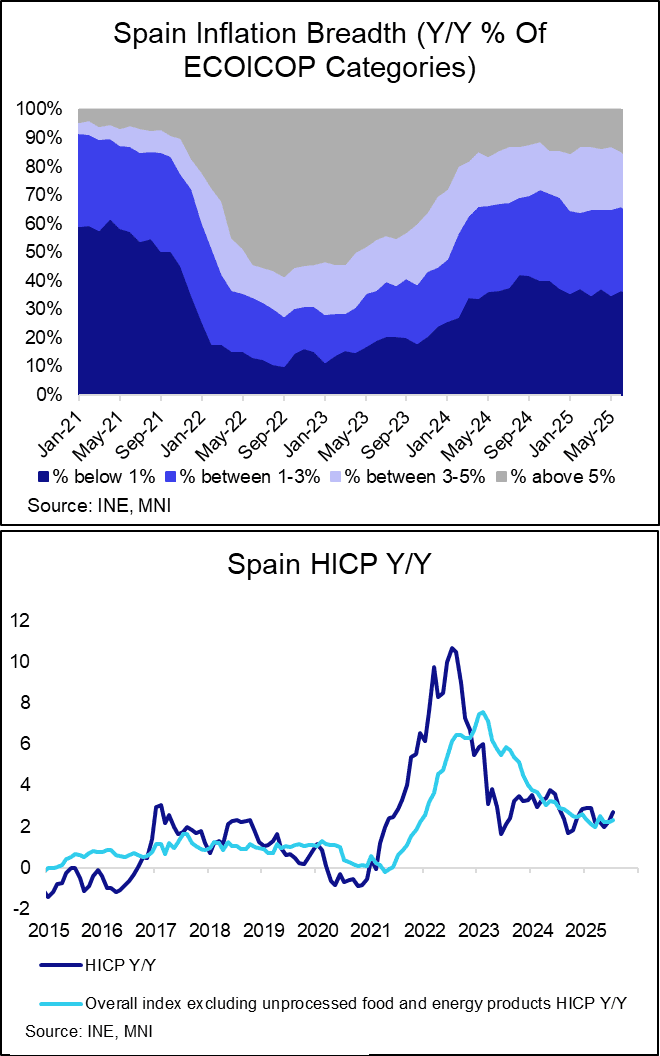

EUROPEAN INFLATION: Spain Final July HICP Confirms Flash, Airfares Push Up Core

Spanish final July HICP confirmed flash estimates at 2.70% Y/Y (vs 2.27% prior), while the monthly reading was revised up a rounded tenth to -0.3% (-0.34% unrounded, vs -0.4% flash). Excluding energy and unprocessed foods, HICP accelerated a touch to 2.34% Y/Y (vs 2.22% prior).

- As indicated in the flash release, there was a rise in electricity inflation (17.30% Y/Y vs 9.00% prior) which pulled the energy component higher in July. Energy HICP was 2.97% Y/Y (vs -0.77% prior).

- Elsewhere, services inflation ticked up to 3.63% Y/Y (vs 3.42% prior). This was mostly driven by a rise in airfares (international flights inflation was 13.61% Y/Y vs 3.46% prior), and to a lesser extent medical services, recreation and culture and accommodation inflation.

- Non-energy industrial goods pressures remain subdued, easing to 0.15% Y/Y (vs 0.29% prior).

- Unprocessed foods fell to 7.76% Y/Y (vs 8.45% prior), but remain elevated. Processed foods, alcohol and tobacco ticked up to 1.32% Y/Y (vs 1.20% prior).

- The proportion of HICP subcomponents with annual inflation rates above 5% rose to 18%from 15% in June, the highest since March 2024.

BUNDS: Full reversal in the German 30yr Yield

- Long end Germany Buxl lead the bounce to keep moving away from Yesterday's low.

- The German 5/30s printed a 98.28 high on the Cash Open, but now seeing some flattening bias, falling towards 96.00.

- That part of the Curve was trading around 94.57, when the 30yr Yield printed a 14yr High.

- The 30yr Yield is fading back to the July high it broke Yesterday, Buxl futures was trading around 115.38.

(Chart source: MNI/Bloomberg Finance LLP).