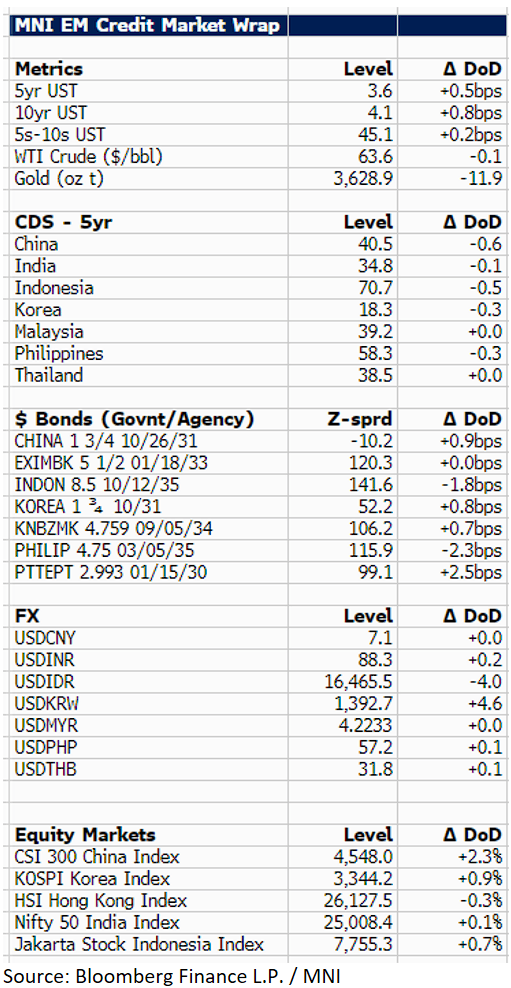

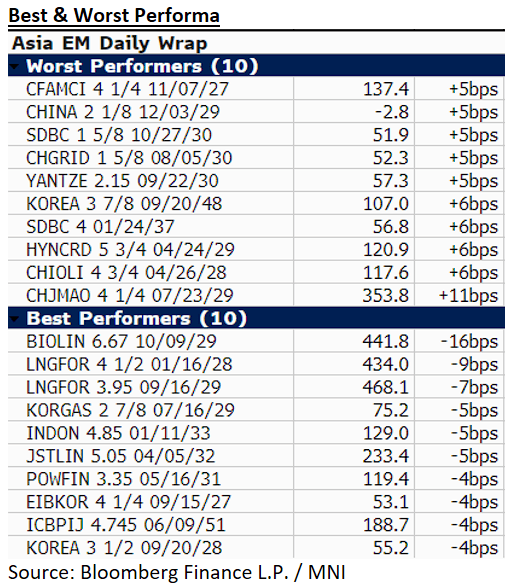

EM ASIA CREDIT: MNI EM Credit Market Update - Asia

US Treasury yields are 1bp higher at 4.1% during the Asia session. We followed LATAM, where issuance was the name of the game, with a three tranche Colombia sovereign deal in Euros totalling EUR4.1bn and a USD200mn PerpNC7 from development bank Bladex and more expected later today. In Asia, it was a fairly quiet sessions, with Asia EM USD sovereign and agency spreads trading in a -2bp to +3bp range, with Thailand the underperformer (PTTEPT 30s +3bp). Regional equities are mostly higher, with the Hang Seng marginally lower. In other news, detained Korean workers were deported today, but the US appears open to creating a new visa category, which would support longer term visas. The new Korea Housing Finance deal was priced overnight (T+40bp), more or less in line with our FV estimate (T+43bp), but no new issues today.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITIES: Option Expiry on Friday

We have Equity Option expiry this Friday, in Notional terms:

US:

- SPX: $1.29T vs $1.23T (last Friday).

- NDX: $54.97bn vs $52.42bn.

- Amazon: $18.40bn vs $17.48bn.

- Apple: $19.56bn vs $16.75bn.

EU:

- SX5E: €150.77bn vs €148.31bn.

- SX7E: €3.26bn vs €3.15bn.

- DAX: €22.38bn vs €22.13bn.

- UKX: £9.47bn vs £9.56bn.

- Lloyd's: £9.08bn.

FINLAND AUCTION PREVIEW: Nordea See RFGB Value Vs OATs Ahead Of Auction

Looking at today's auction with the 3.00% Sep-35 / 0.25% Sep-40 RFGBs on offer by Finland, Nordea "prefer to increase exposure in the 10-year segment, particularly considering the enhanced liquidity characteristics at this point on the curve" given the "relative stability of the 15-year sector on the Finnish curve".

- They highlight the recent Fitch Finland downgrade to AA (outlook: stable) on July 25th had "no substantial repricing of the Finnish curve" as an effect as the downgrade was "largely anticipated" by markets.

- They did note some spread widening between Finland and Austria in the 10-year segment, which they attribute to "the strong performance of Austrian bonds following their RAGB 02/35 tap", however.

- They do also "find value in establishing long positions in Finland against short positions in OATs ahead of this upcoming auction, as autumn will likely introduce uncertainty regarding the French political landscape, while global geopolitical risks persist with downside risks predominating across multiple dimensions."

STIR: US CPI and Headline Flow Likely To Drive EUR STIRs Today

With today’s regional calendar light, EUR STIRs will look to headline flow and the US CPI report for intraday cues. The OIS-implied probability of another 25bp cut this cycle continues to gradually fall, with the March 2026 contract now pricing 16bps of cuts (vs 23bps at the start of last week).

- ECB officials have suggested that a fresh deterioration in data is required to deliver another cut in September, meaning focus remains on next week’s flash PMIs and the August flash inflation round at the end of the month.

- Euribor futures are flat to +1.0 ticks through the blues, perhaps seeing some spillover from this morning’s UK labour market report (see earlier posts for more).

- ERH6 continues to hover just above support at 98.095 (August 1 low), currently +0.5 at 98.115.

- The August German ZEW survey is due at 1000BST, but markets don’t tend to put too much stock in this release.

| Meeting Date | ESTR ECB-Dated OIS (%) | Difference Vs. Current Effective ESTR Rate (bp) |

| Sep-25 | 1.912 | -0.6 |

| Oct-25 | 1.878 | -4.0 |

| Dec-25 | 1.814 | -10.4 |

| Feb-26 | 1.796 | -12.2 |

| Mar-26 | 1.760 | -15.9 |

| Apr-26 | 1.759 | -15.9 |

| Jun-26 | 1.761 | -15.7 |

| Jul-26 | 1.763 | -15.5 |

| Source: MNI/Bloomberg Finance L.P. | ||