EM ASIA CREDIT: MNI EM Credit Market Update - Asia

Asia EM USD sovereign and agency spreads are trading in a -2bp to +2bp range this morning, with Malaysia the outperformer. Our Malaysia USD proxy (KNBZMK 34s) is around 2bp tighter, otherwise the bias is wider in Asia. Regional equities are higher, with Indonesia's JCI +0.8%, a rebound following yesterday's reaction to a change in Finance Minister. In other news we are hearing India Prime Minister Modi and US President Trump, making positive overtures about future talks. Outside of Asia, news that Russian drones entered Polish airspace will be closely monitored by investors. In corporate news, LG Energy has reportedly halted construction of US plants in response to Korean workers being repatriated after immigration raids. We also see a mixed bag in China real estate with Longfor reporting August sales down 27% YoY, while China Jinmao was up 46% in the month. CATL is also reported to be restarting lithium mining operations, which is expected. Finally, we see a new 5Y USD deal from Korea Housing Finance.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

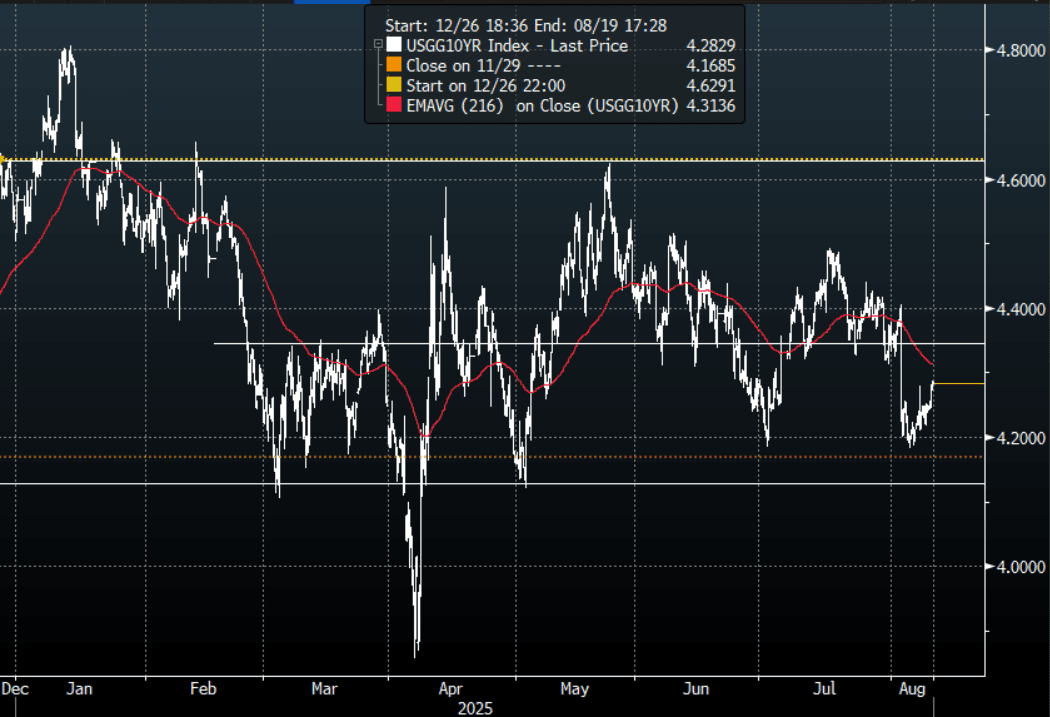

US TSYS: Futures Trade Slightly Higher

The TYU5 range has been 111-25+ to 111-29+ during the Asia-Pacific session. It last changed hands at 111-29, up 0-02+ from the previous close.

- The 10-year yield had a powerful move lower in reaction to the NFP data, breaking below its 4.30% pivot within the wider range 4.10% - 4.65%. This now turns momentum lower in yields and you could expect buyers of treasuries on bounces back towards 4.30/35% now looking to initially test the 4.10% area.

- Bob Elliott on X: “Used car prices have been a big negative on CPI for the last 3m. A notable difference from the broad trend of underlying used car prices going from a significant disinflationary pressure to a modestly inflationary one over the last year or so.”

MNI DATA - Tuesday’s CPI report headlines the US economic calendar with analysts expecting core CPI inflation to gain momentum in July as the acceleration in core goods inflation continues. We’re starting to get into larger tariff impacts on core goods but the largest could be reserved for Aug-Sep by some estimates. We are currently tracking unrounded core CPI estimates at around 0.32% M/M after the 0.23% in June at what would be the strongest M/M print since January.

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

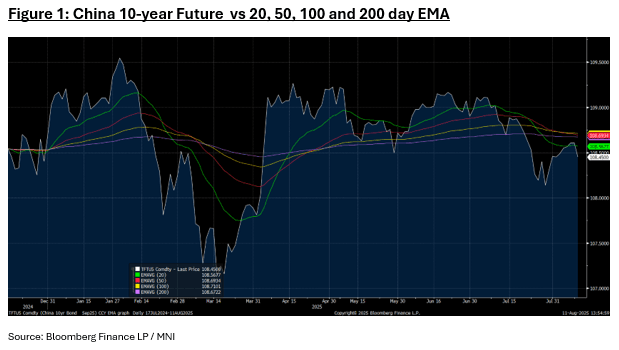

CHINA: Bond Futures Down in Morning Trade

- China's bond futures have begun the week with falls in Monday's morning session.

- After finishing last week up by +0.16, the 10Yr bond future has given all of that back in this morning's session, falling -0.16 to 108.45.

- Having trade last week above the 20-day EMA (of 108.56) the sell off this morning sees the 10Yr track below all major moving averages.

- The 2-year future is lower by -0.01 at 102.35, having traded near to the 20-day EMA of 102.37 before turning lower again.

- The 10YR Government bond has seen yields climb +1.5bp to 1.71%

MNI EXCLUSIVE: Limited PPI Impact From China's Supply Reforms

A leading commodities expert shares her view on China's supply reforms.

On MNI Policy MainWire now, for more details please contact sales@marketnews.com