EM ASIA CREDIT: MNI EM Credit Market Update - Asia

Asia EM USD sovereign and agency spreads are trading in a narrow range of -2bp to +4bp today, with Malaysia as an outlier—our USD proxy (KNBZMK 34s) widened by 4bp. Overall, the market feels weak ahead of Fed Chair Jerome Powell’s upcoming speech at Jackson Hole. Equity markets are mostly lower, with South Korea’s KOSPI down 2%, weighed by declines in nuclear-focused names Doosan Enerbility and KEPCO E&C, likely reflecting ongoing concerns around the Westinghouse agreement. In other corporate news, UltraTech Cement is on track to reach its cement capacity targets a year early in 2026; South Korea is exploring possible petrochemical support mechanisms; and PLDT is signalling a potential IPO of its digital banking division, Maya. Additionally, Swire Pacific has launched a new USD bond mandate.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

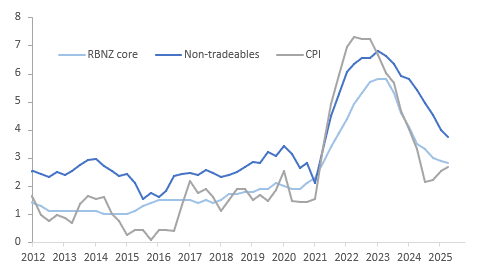

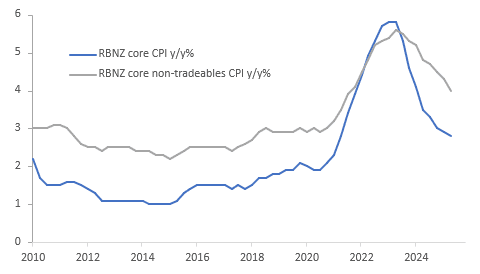

NEW ZEALAND: RBNZ Core Inflation Measure Moderates Slightly

The RBNZ’s sector factor model result for Q2 was in line with other underlying CPI measures showing that core inflation remained below the top of the 1-3% target band. Its measure of core inflation eased 0.1pp to 2.8% y/y, the lowest rate since Q2 2021, and is now only 0.1pp above headline CPI. Underlying non-tradeables also continued to moderate. Thus with activity data still lacklustre, another 25bp rate cut on August 20 seems likely coinciding with an update in staff forecasts.

NZ inflation y/y%

- The sector factor model’s estimate of core non-tradeable inflation declined to 4.0% y/y in Q2 from 4.3%, the lowest in almost 4 years. The headline measure dropped 0.3pp to 3.7%.

- Underlying tradeable inflation remained very low at 0.7% y/y up slightly from Q1’s 0.5%, compared to the headline at 1.2% y/y.

- Earlier today Q2 trimmed mean CPI was steady at 2.5% y/y but CPI ex food, fuel & energy ticked up 0.1pp to 2.7% y/y.

NZ underlying inflation y/y%

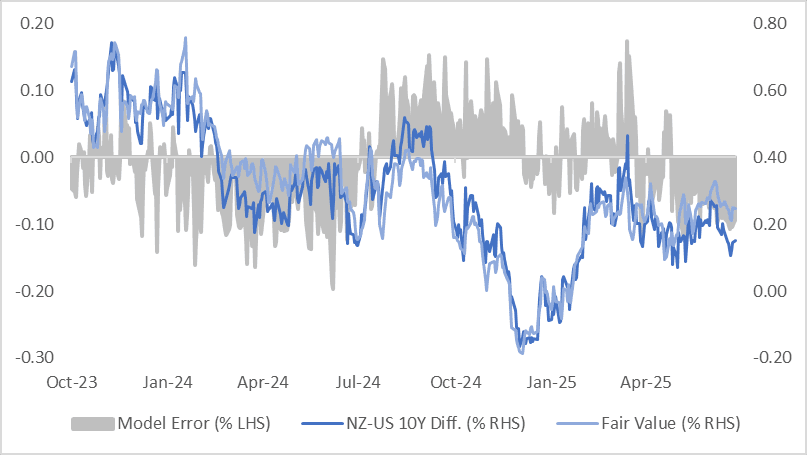

BONDS: NZ-US 10Y Differential Near Mid-Point Of This Year’s Range

NZGBs are 3-5bps richer today on the day and after today’s Q2 CPI data.

- With cash U.S. Treasuries not trading during today’s Asia-Pac session (due to the Japan holiday), and U.S. futures trading slightly higher, the move leaves the NZ–US 10-year yield differential around +15bps.

- At this level, the spread remains near the midpoint of the -20bps to +40bps range observed year-to-date.

- However, a simple regression of the 1Y3M forward swap spread against the 10-year yield differential over the past 18 months suggests the differential is currently about 10bps below its estimated fair value of +25bps.

- The regression’s standard error has remained within ±15bps over the past year, underscoring some inherent variability in the relationship.

- The 1Y3M spread continues to anchor market expectations around the longer-term path of yield convergence.

Figure 1: NZ-US 10-Year Yield Differential

Source: Bloomberg Finance LP / MNI

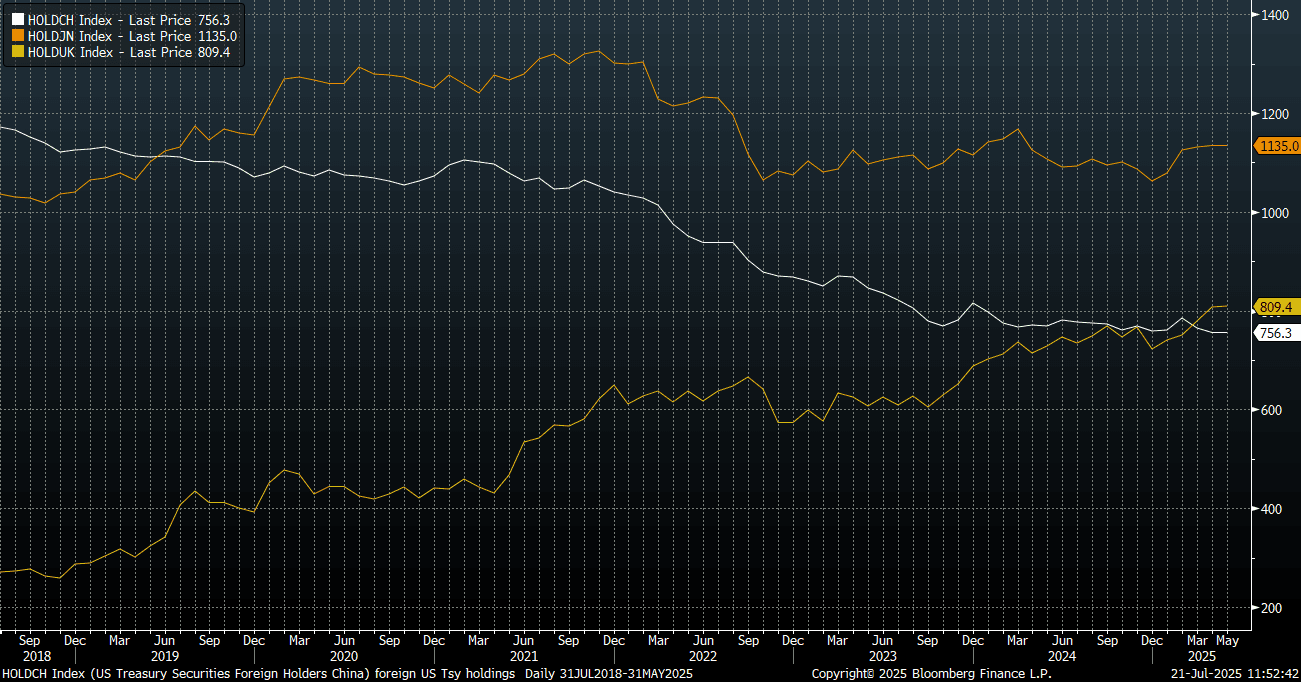

CHINA: China To Reduce UST Holdings Further

- A news article from the Government run China Daily this morning indicates that a strategic move is beginning in China, that may have profound implications for the US and their fiscal position.

- China Daily reports that is is a 'strategic necessity' for the scaling back of holdings in US Treasuries, given the declining confidence in the dollar as the reserve global currency.

- The article states that China intends to pursue a more balanced, controllable allocation of FX reserves and likely to increase its holdings of non-dollar assets, including financial instruments of Asian trading partners.

- Yu Yongding, an academic member of the Chinese Academy of Social Sciences, called for China to continue reducing US government debt holdings in an orderly manner and that in extraordinary times, extraordinary measures are called for.

- The latest Treasury holding data shows the UK taking over China as the third largest holder of US Treasury securities, see the chart below (China holdings are the white line).

- China has total holdings of USD 756.3 billion, to now rank third in largest holdings behind Japan and UK, according to US Treasury data. This shift marks a significant moment in the global financial landscape. The last time the UK ranked ahead of China in US debt ownership was in 2000—more than two decades ago. China holdings have flatlined somewhat in recent years, after falling through much of 2021-2023.

- The Governor of the PBOC Pan Gongsheng has been clear in his assessment of the risks associated with the USD dominance and that the fiscal position of the US economy, could spill over into global markets.

- China's FX reserves recently increased to US$3.32tn, its highest level in a decade.

Fig 1: China, Japan and UK Treasury Holdings

Source: Bloomberg Finance L.P./MNI