EM ASIA CREDIT: MNI EM Credit Market Update - Asia

Asia EM $ government and agency credit is trading in a narrow range this morning (–1bp to +1bp), as Thailand and Malaysia have agreed to a 19% tariff rate with the U.S.—matching Indonesia’s rate and in line with expectations. Asian equity moves are led by Korea’s KOSPI, which is down 3% following news of a proposed capital gains tax increase. On the corporate side, a flurry of results has been reported, including from Rizal Bank, Metro Bank, Medco Energi, and Indofood CBP. There has been no new $ issuance this morning.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Futures Slightly Weaker, Heavy US Calendar Before Long Weekend

In early afternoon trade, JGB futures weaker, -5 compared to the settlement levels, after reversing modest overnight gains.

- Japan’s monetary base fell 3.5 percent in June from a year ago.

- Japan’s super-long bonds are set to remain under pressure in the medium term as local life insurers may offload holdings to sidestep impairment losses on deeply discounted debt. (per BBG)

- (Bloomberg) -- Japan will continue actively negotiating tariffs in good faith with the US for both countries’ mutual benefit, Deputy Chief Cabinet Secretary Kazuhiko Aoki says at a regular press conference on Wednesday.

- Cash US tsys are little changed in today's Asia-Pac session after yesterday's twist-flattener. Wednesday's US data focus is on MBA Mortgage Applications at 0700ET, Challenger Jobs at 0730ET followed by ADP Employment Change at 0815ET. No Fed scheduled Fed speakers. Thursday is a heavy data day with NFP added due to Independence Day holiday closure on Friday.

- Cash JGBs are little changed across benchmarks out to the 10-year and ~1bp richer beyond. The benchmark 10-year yield is 0.5bp higher at 1.40% versus the cycle high of 1.596%.

- The swaps curve has twist-steepened, with rates 1bp lower to 1bp higher. Swap spreads are tighter out the 10-year and wider beyond.

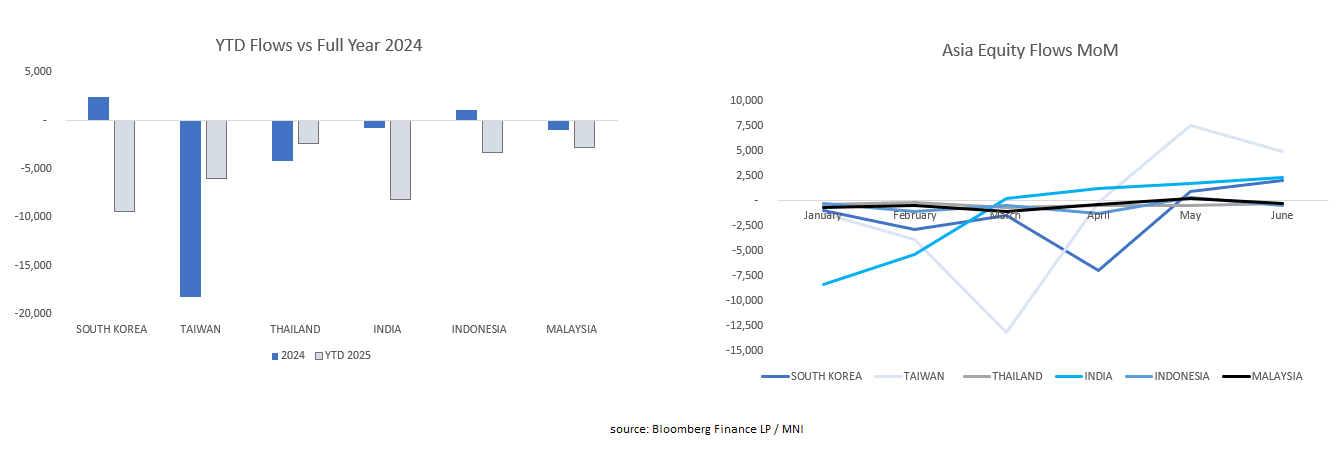

ASIA STOCKS: Is the tide Coming Back in for Asia Stock Flows

- We report each day the flow data for major regional bourses which suffered heavily under the threat of tariffs.

- However in recent months we have seen strong inflows into Taiwan, India and South Korea, and whilst year to date flows remain negative there appears sufficient evidence to ask whether the worst is over for outflows for major regional bourses.

- The flows began to turn positive when tariffs were paused in April with Taiwan the biggest beneficiary thanks to its semi-conductor manufacturers.

- USD weakness is a potential positive catalyst for the second half of 2025 for Asia flows, particularly if trade agreements are reached.

AUSSIE BONDS: Cheaper, Narrow Ranges, Heavy US Calendar Today & Tomorrow

ACGBs (YM -3.0 & XM -3.0) are modestly weaker on another subdued day of trading.

- Australian retail sales rose a modest 0.2%m/m in May, after a revised flat outcome in April (originally reported as a -0.1% dip). The market consensus for the May outcome was a +0.5% rise. Other data showed May building approvals up 3.2%m/m, which was slightly below the 4.0% forecast. The April fall was revised to -4.1%m/m.

- Building approvals rose 3.2% m/m (estimate +4.0%) in May versus a revised -4.1% in April.

- Cash US tsys are little changed in today’s Asia-Pac session after yesterday’s twist-flattener. Wednesday's US data focus is on MBA Mortgage Applications at 0700ET, Challenger Jobs at 0730ET followed by ADP Employment Change at 0815ET. No Fed scheduled Fed speakers. Thursday is a heavy data day with NFP added due to Independence Day holiday closure on Friday.

- Cash ACGBs are 2-3bps cheaper with the AU-US 10-year yield differential at -11bps.

- The bills strip has bear-flattened, with pricing -1 to -4.

- RBA-dated OIS pricing is slightly firmer across meetings today. A 25bp rate cut in July is given a 95% probability, with a cumulative 82bps of easing priced by year-end (based on an effective cash rate of 3.84%).