EM ASIA CREDIT: MNI EM Credit Market Update - Asia

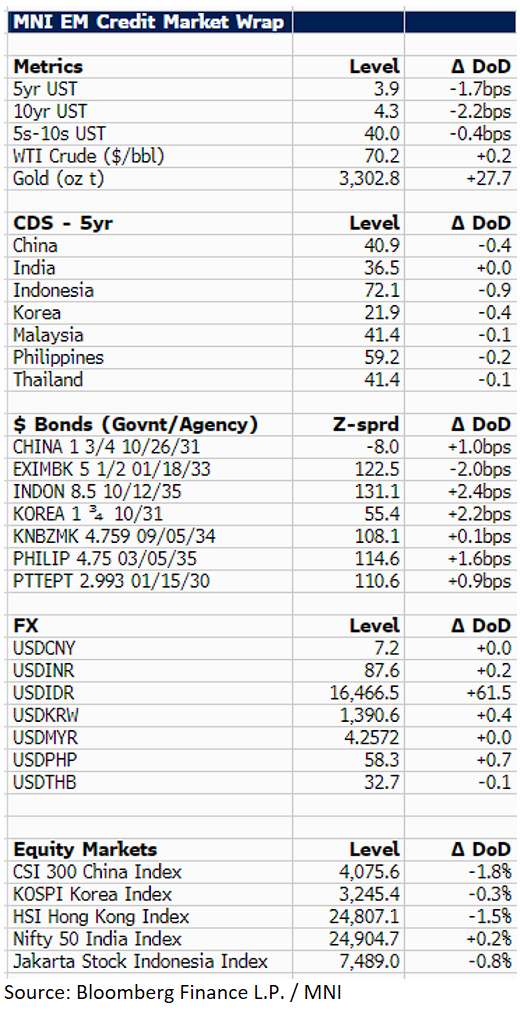

US Treasury yields were 2bp lower at 4.3%, with the FOMC holding the federal funds target rate steady overnight; market attention is now on initial jobless claims due later today. We followed on from LATAM where $ benchmark spreads were around 2-3bp wider. In Asia, EM saw a similar move with $ credit 3bp wider, amid a news-heavy session dominated by trade negotiations.

In terms of tariff deals. South Korea agreed to a 15% tariff with the US, a deal that also included $350bn in US investments and zero tariffs on imported US goods. No deal has been reached with India, so a 25% tariff will take effect from August 1, with the possibility of an additional, unspecified “penalty” on India for buying Russian oil and weapons - we expect trade discussions to continue. Thailand has agreed to a deal following its ceasefire with Cambodia; while details are pending, the tariff rate is expected to be close to Indonesia’s (19%). An agreement with Malaysia is expected tomorrow.

In corporate news, SK Innovation (Ba1neg/BBB-neg/NR) reported Q2 results in which leverage took another leg higher (c. 15x), raising potential rating concerns. Additionally, JD.com confirmed its bid for Ceconomy, valuing the company at c. $2.5bn, ratings are expected to be affirmed given JD.com's strengthened business profile.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: EUROZONE JUNE FINAL MANUF PMI 49.5 (49.4 FLASH; 49.4 PRIOR)

- MNI: EUROZONE JUNE FINAL MANUF PMI 49.5 (49.4 FLASH; 49.4 PRIOR)

MNI: ECB 1-YEAR CONSUMER INFLATION EXPECTATIONS 2.8%

- MNI: ECB 1-YEAR CONSUMER INFLATION EXPECTATIONS 2.8%

- MNI: ECB 3-YEAR CONSUMER INFLATION EXPECTATIONS 2.4%

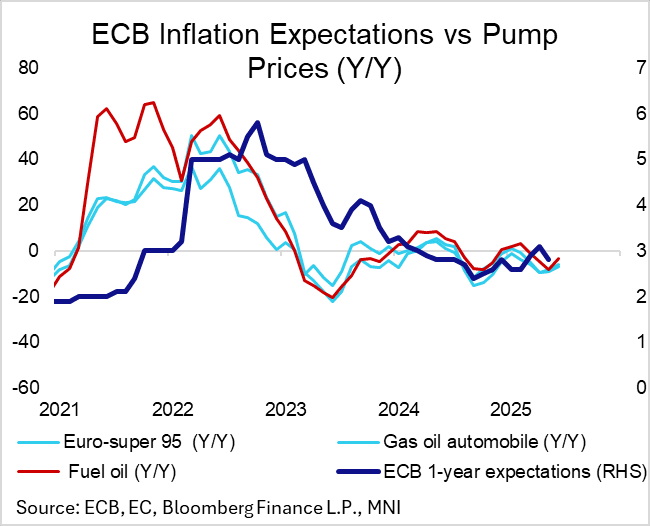

EUROZONE DATA: 1-year Ahead Inflation Expectations Fall 0.3pp To 2.8%

ECB 1-year ahead inflation expectations fell to 2.8% in May, down from 3.1% in April and 2.9% in March. Lower energy prices through May were likely the main driver of the fall, with European Commission pump price data indicating a notable sequential fall in auto, gas and heating fuels.

- 3-year ahead expectations eased a tenth to 2.4%, after two months at 2.5%, now back in line with the 2024 average. 5-year ahead expectations were unchanged at 2.1% for the sixth consecutive month.

- The release notes that "uncertainty about inflation expectations over the next 12 months decreased in May, reversing the increase observed in April”.