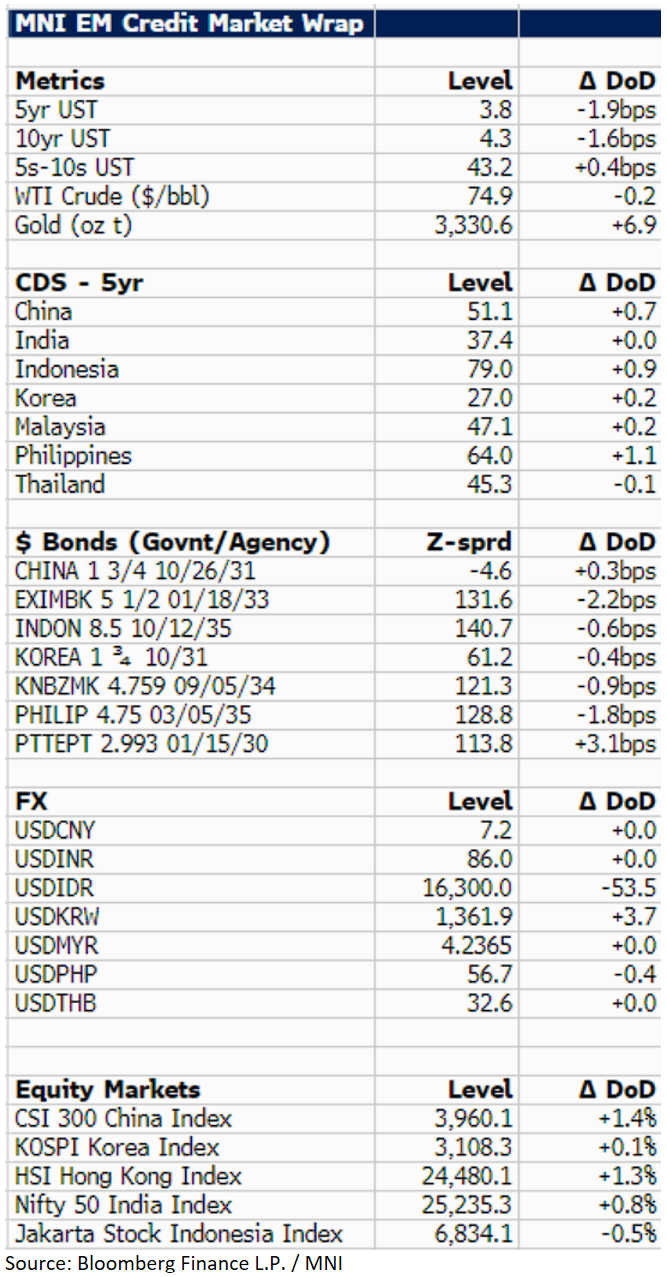

EM ASIA CREDIT: MNI EM Credit Market Update - Asia

U.S. 10yr treasury yields are 2bp lower at 4.3%, while the market waits on any new developments in the Middle East.

In LATAM hours the positive move in equities and the Treasury rally was supportive for higher yielding liquid bonds in the market like Argentina sovereigns that rallied 1 ½ points. In Asia EM $ credit is trading around 2bp tighter, the outlier being Thailand. Our Thai $ proxy, PTTEPT 01/30, is around 3bp wider on the day. The Bank of Thailand rate decision was in line with expectations and unchanged at 1.75%. Asia equities had a positive bias, with the tentative ceasefire between Israel and Iran currently holding.

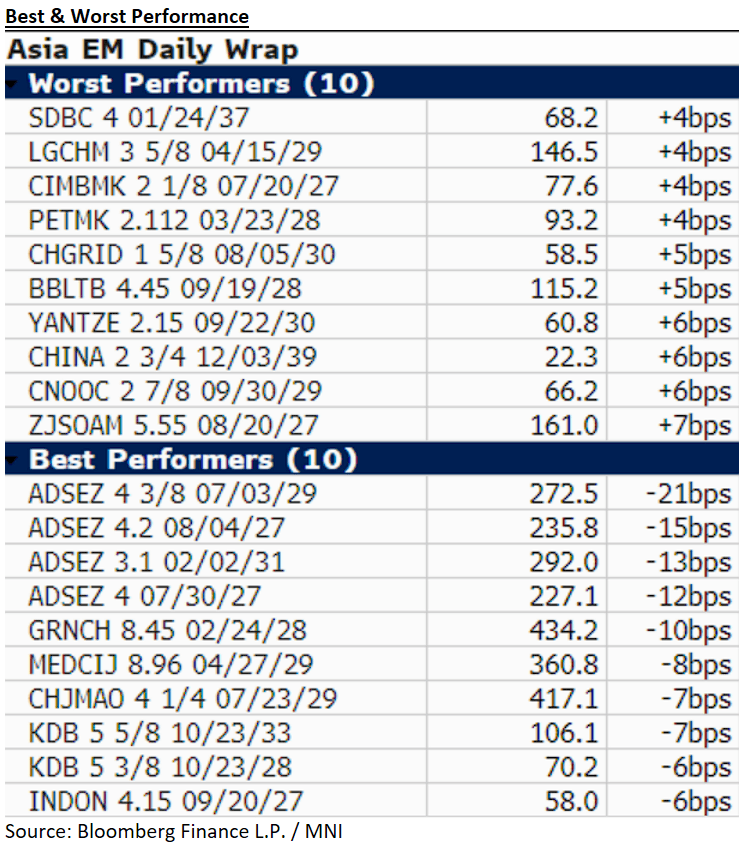

Overall relatively quiet in terms of single name news, though Adani Ports continues to outperform (-10 to -20bp). In primary, no new deals, though mandates from Korean issuers, NH Investment & Securities and LOTTE Property & Development.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SOFR: OPTIONS: SFRU5 97.00 Calls Lifted

SFRU5 97.00 calls paper paid 2.5 on 3K.

BOBL: Futures Blocked

OEM5 5,963 lots blocked at 118.860, looks like a buyer based on prevailing quotes but Subsequent price action points to a seller. DV01 ~EUR370K.

SCANDIS: Important Supports Being Tested Across Scandi Crosses

Important supports in Scandi crosses are being tested this morning, clearance of which could extend recent outperformance against the broader G10 basket. The improved risk backdrop following the US/EU 50% tariff delay has provided a tailwind to NOK and SEK today, though the Scandis also traded resiliently in the wake of Trump’s initial tariff announcement last Friday.

- This suggests the broader theme of rotation out of the USD is continuing to benefit NOK and SEK (alongside the EUR) as has been the case through this year.

- Key near-term supports to watch:

- EURSEK (-0.3% today at 10.8010): April 4 low at 10.7941. A clear breach of this would expose 10.6652 (April 3 and multi-year low).

- USDSEK (-0.5% today at 9.4820): April 22 low at 9.4704.

- EURNOK (unch today at 11.4830): May 23 low at 11.4621. The cross has pared around 80% of the sharp 8.55% rally seen between April 2 – April 11

- USDNOK (-0.5% today at 10.0690): December 2023 low at 10.0562, clearance of which would expose the July 2023 low at 9.9249.

- The last week’s price action still leaves an uptrend in NOKSEK intact, with the uptrend drawn from the April 9 low underpinning the cross, helping narrow the gap to the key 0.9500 medium-term pivot level.

- This week’s Scandi calendar is heavy, with activity data due from both Sweden and Norway. While a June Norges Bank cut seems highly unlikely at this stage, a weak set of Swedish readings could tilt the balance in favour of a June Riksbank cut to 2.00%.