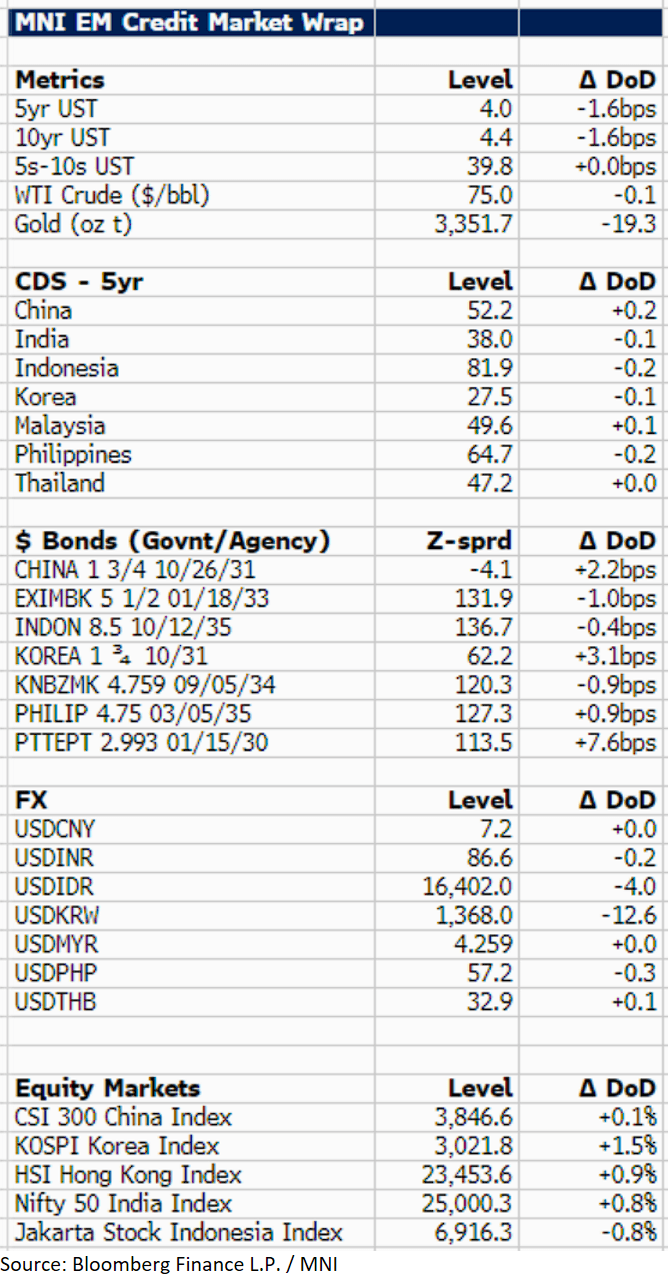

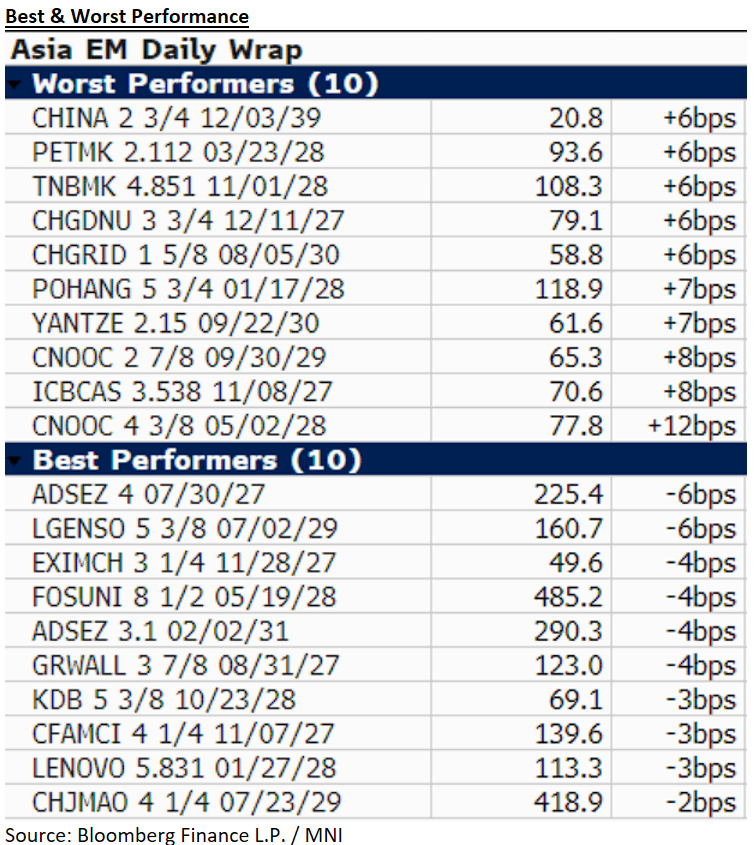

EM ASIA CREDIT: MNI EM Credit Market Update - Asia

U.S. 10yr treasury yields are 2bp lower at 4.4% as the market awaits possible intervention by the U.S. in Iran. In Asia, EM $ spreads turned weaker during the course of the day, the main underperformers being Korea (+3bp) and Thailand (+8bp). Thailand reported year-to-date foreign tourist arrivals down 3.6% YoY, and with a political crisis looming, may remain under pressure. Malaysia also reported exports down 1.1% for May, weaker than estimates (+7.5%). In terms of credit, news flow has been muted following the US holiday, though we note Biocon has raised cash for debt repayment, positive. Finally, the Bank of East Asia subordinated rating was cut one notch to Baa3 by Moody's on an earlier AT1 redemption.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Next Support Breached In Futures

Gilts sell off following the CPI data.

- Futures through next support at the May 19 low (90.86), printing as low as 90.72 before recovering from lows.

- Bearish technical trend remains intact, with next support at the April 11 low (90.47).

- Yields see a parallel ~3bp shift higher.

- SONIA futures tick further away from lows as gilts stabilise, last 0.25-3.0 lower.

- BoE-dated OIS shows 37bp of cuts through December vs. 35bp ahead of the gilt open.

- On the supply front, the DMO will sell GBP4.25bln of the 4.00% Oct-31 gilt today.

- Little else of note on the UK calendar for the remainder of the day, which will leave focus on macro inputs and continued digestion of the CPI data.

STIR: Euribor Outperforms SONIA Post UK CPI; Focus On ECB Speakers Today

Euribor futures outperform SONIA counterparts following the firmer-than-expected UK CPI report, currently little changed through the blues versus yesterday’s settlement levels. ERZ5 reached a post-UK data low of 98.205, but has since moved back to 98.220, unchanged on the session. The ECB’s reaction function is dominated by the weak growth outlook at present, placing focus on tomorrow’s May flash PMIs and any updates on EU-US trade talks.

- The SFI/ER Z5 spread reached a fresh multi-month high of 205bps at the SONIA open, but has since eased a touch back to 203.5bps.

- ECB-dated OIS continue to price just over 50bps of easing through year-end. July pricing will be in focus if there is a re-escalation of tariff tensions or if incoming growth data is weaker than expected, with just 6.5ps of cumulative cuts priced at present.

- Today’s regional data calendar is light, but there are several ECB speakers scheduled. Vice President de Guindos presents the ECB’s Financial Stability report at 0900BST (a summary was published yesterday), with Centeno, Lane and Escriva scheduled later. Lane speaks on “Negative interest rates and the impact of monetary policy”.

| Meeting Date | ESTR ECB-Dated OIS (%) | Difference Vs. Current Effective ESTR Rate (bp) |

| Jun-25 | 1.941 | -23.1 |

| Jul-25 | 1.875 | -29.7 |

| Sep-25 | 1.761 | -41.1 |

| Oct-25 | 1.714 | -45.8 |

| Dec-25 | 1.652 | -52.0 |

| Feb-26 | 1.637 | -53.5 |

| Mar-26 | 1.626 | -54.7 |

| Apr-26 | 1.639 | -53.3 |

| Source: MNI/Bloomberg. | ||

SILVER TECHS: Support Still Intact

- RES 4: $36.000 - Round number resistance

- RES 3: $34.903 - High Oct 23 ‘24 and the bull trigger

- RES 2: $34.590 - High Mar 28

- RES 1: $33.686 - High Apr 25

- PRICE: $33.103 @ 08:12 BST May 21

- SUP 1: $31.668/651 - Low May 1 / 15

- SUP 2: $30.915/28.351 - Low Apr 11 / 7 and the bear trigger

- SUP 3: $27.686 - Low Sep 6 ‘24

- SUP 4: $27.180 - Low Aug 14 ‘24

A bullish theme in Silver remains intact and the latest pullback that started Apr 25, is likely a correction. Key short-term support has been defined at $31.668, the May 1 low (pierced). A clear break of this level would signal scope for a deeper retracement and open $30.915, Apr 11 low. For bulls, resistance to watch is $33.686, the Apr 25 high. Clearance of this level would confirm a resumption of the uptrend.