EMERGING MARKETS: MNI EM Credit Market Update - Asia

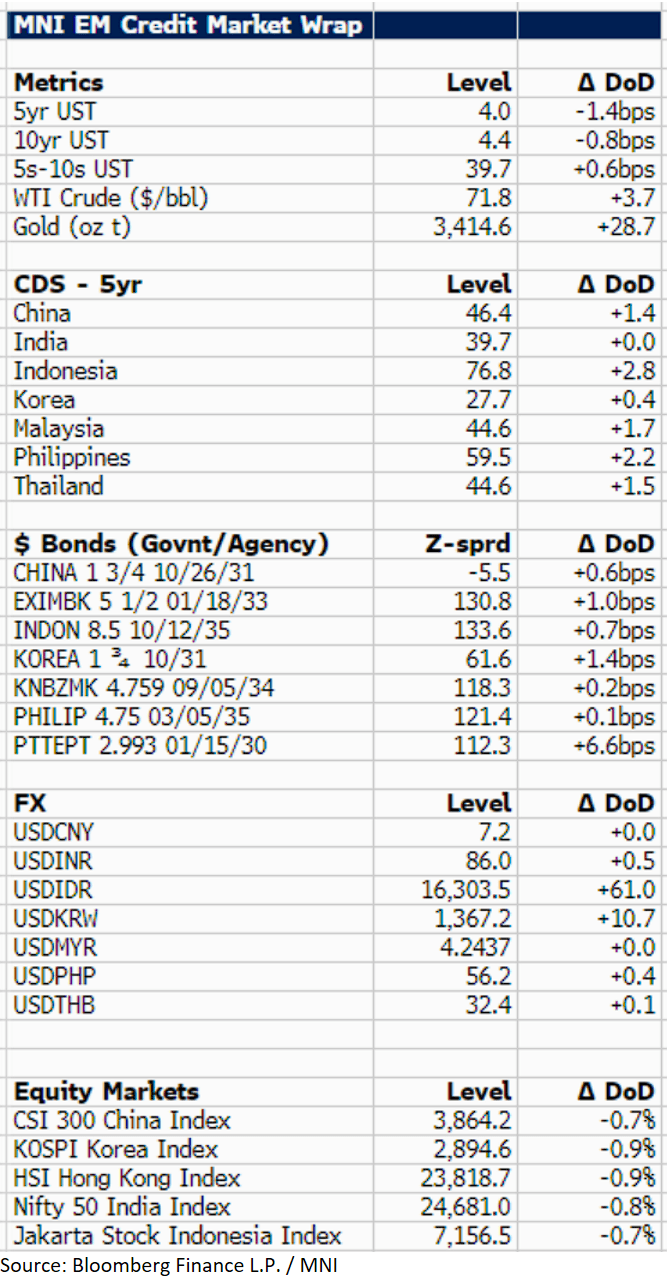

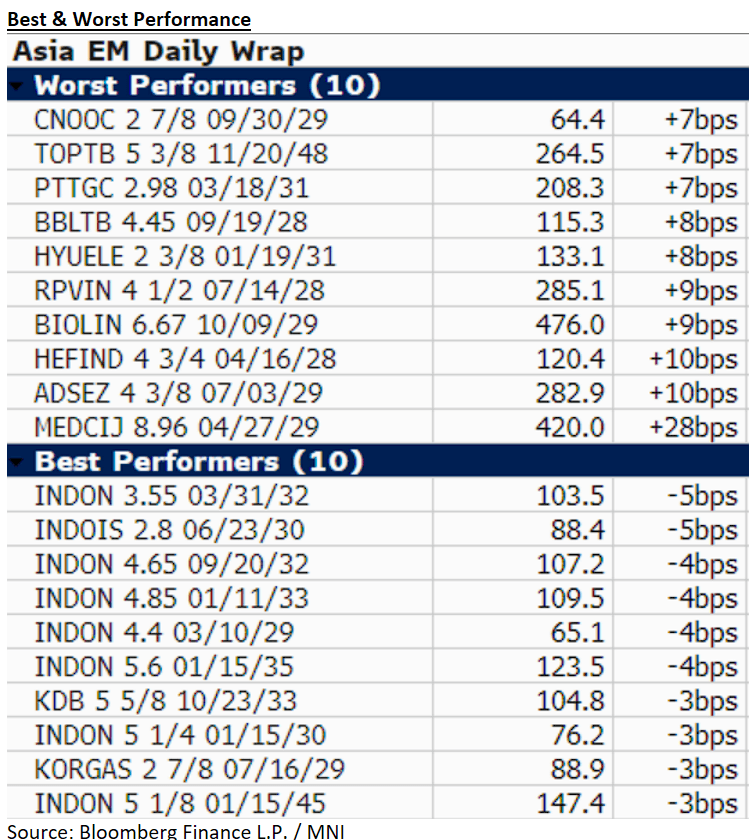

U.S. 10yr Treasury yields are 1bp lower at 4.4% with markets now focused on geopolitical risks in the Middle East. We followed on from LATAM, where spreads had widened 2-5bps as prices lagged the U.S. Treasury rally. Asia EM $ credit today was weaker, with govie/agency $ spreads up to 7bp wider on the back of Israeli action in Iran. Thailand was the underperformer with our $proxy (PTTEPT 01/30) +7bp. In terms of individual credit, corporate actions were topical, LG Chem announced plans to sell its Water Solutions business for KRW1.4T ($1bn), which had been reported as a possibility back in April, spreads unchanged on the day. Vanke also reported selling all of its Treasury A shares for c. $67m for working capital needs. Finally, Reliance Industries announced it had sold a 3.7% stake in Asian Paints for INR77bn ($900m).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EUROPEAN INFLATION: German Inflation Breadth Broadly Unchanged In April

MNI’s inflation breadth tracker (see chart below) shows disinflation overall continuing to stall in April, with the percentage of ECOICOP (European classification of individual consumption according to purpose, a standardized category split) items printing at or below 1% unchanged 42.8%. In the high-inflation categories, similar trends could be observed, with the percentage of categories above 5% falling just 0.3pp to 14.8% in April.

EUROPEAN INFLATION: German CPI Details Suggest Intact Underlying Disinflation

German final April HICP was unrevised from the flash readings at 2.2% Y/Y (2.3% prior) and 0.5% M/M (0.4% prior). The final reading to CPI was also unrevised at 2.1% Y/Y (2.2% prior) and 0.4% M/M (0.3% prior). Core CPI accelerated 0.3pp to 2.9% Y/Y, a rate not seen since January.

- Overall, the data confirms the main conclusions from the flash / state-level reading - services accelerated materially (contribution +0.20pp vs prior) on the back of the Easter effect while goods inflation slowed (contribution -0.25pp vs prior) following lower energy prices.

- Without (volatile) airfares adding 0.16pp and package holidays adding 0.08pp to headline vs March, services inflation's contribution to headline would have been lower than the month before.

- This speaks in favour of the process of underlying services disinflation being intact.

SWAPS: Recent German ASW Narrowing Stalls

German ASWs vs. 3-month Euribor are little changed on the day, recovering from session lows alongside outright bonds as equities move away from session highs.

- The recent move lower in ASWs has stalled a little over the past 36 hours, after the narrowing impulse from the moderation in Sino-U.S. tariffs moderated.

- ASWs trade closer to their cycle closing lows than their April highs, given the recovery in risk appetite/row back of U.S. tariffs.

- Medium-term, supply considerations are set to present ongoing pressure for long end spreads, but any further sell offs in spreads are unlikely to be linear, given the macro volatility evident at present.