MNI ECB Preview: Relative Resilience Confirms In A Good Place

Dec-16 11:07By: Chris Harrison and 1 more...

Bunds+ 2

DOWNLOAD FULL REPORT HERE

EXECUTIVE SUMMARY

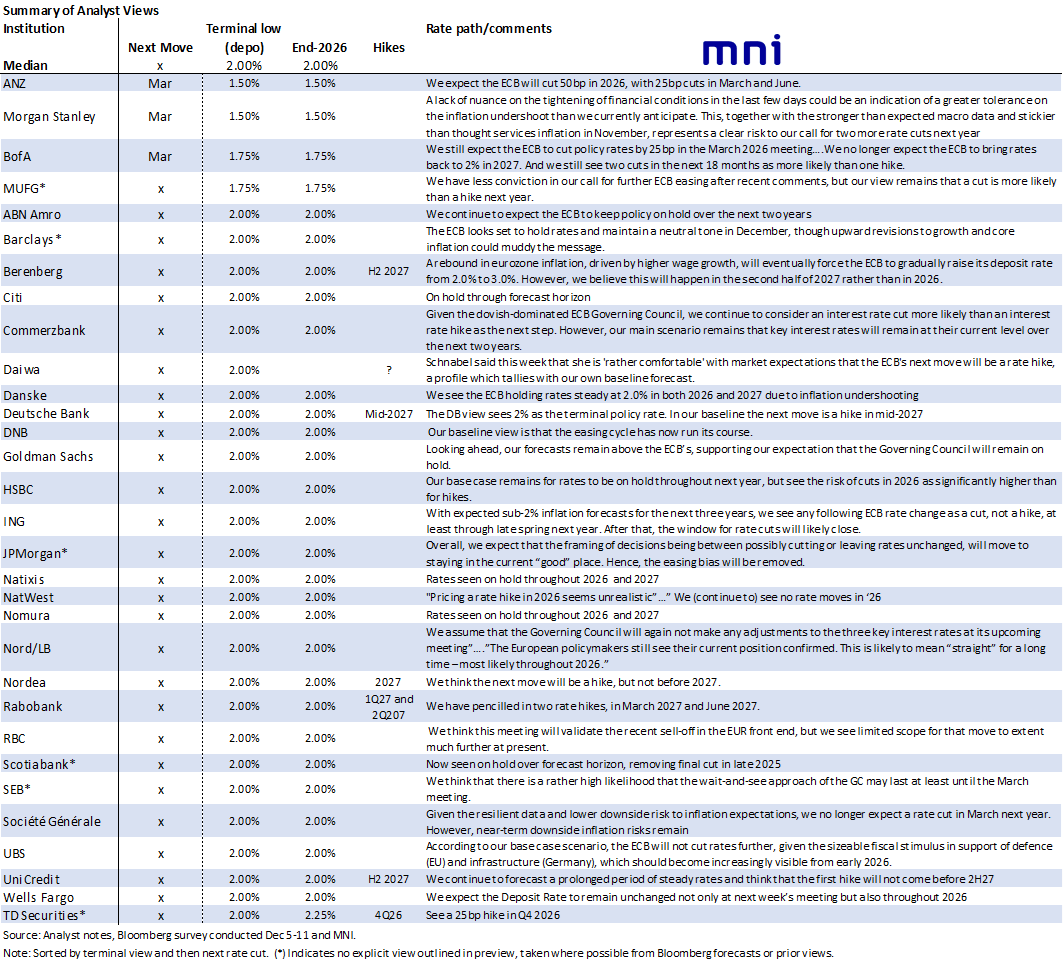

- The ECB is again fully expected to leave its three key rates on hold on Thursday, including a 2% deposit rate nicely within the 1.75-2.25% neutral rate range estimated by ECB staff.

- This time though the meeting comes against a backdrop of a very mild hiking bias to end-2026, helped by recent rhetoric from Schnabel, which despite having been pared fairly notably in recent days is still a change from a modest easing bias ahead of recent meetings.

- We expect primary focus on the updated macroeconomic projections and the balance of risks to inflation and growth. Analysts expect upward revisions to both GDP and core HICP projections.

- We expect a repeat of a data-dependent and meeting-by-meeting approach, with no pre-determined path.

- OIS price 2bps of easing through June 2026, before the implied curve steepens into year-end. There are just under 5bps of hikes priced through end-2026, down from a hawkish extreme of 10bps on Dec 10.

- The euro has been pushing back towards recent highs after a sizeable push higher since late November, although increases are milder when comparing with ahead of the Oct meeting or less so again ahead of the cut-off for the September projections. Effective exchange rates remain elevated which could see some sensitivity to any dovish surprises.

- We’re still to receive the final November HICP report on Wednesday, day one of the two-day ECB meeting, with its potentially important details of drivers of stronger services inflation.