MNI ECB Preview: Enjoying The Good Place

Oct-28 16:16By: Chris Harrison and 1 more...

Bunds+ 2

Download Full Report Here

Executive Summary

- The ECB is fully expected to again leave its three key rates on hold on Thursday, including a 2% deposit rate nicely within the 1.75-2.25% neutral rate range estimated by ECB staff.

- ECB President Lagarde is expected to continue to suggest policy is in a good place, echoed by a broad range of ECBspeak save for some nuances in views on both the dovish and hawkish end of the spectrum.

- Lagarde is also likely to reiterate a data-dependent and meeting-by-meeting approach with no pre-determined path.

- Focus should be on the balance of risks. Areas we’ll be watching include the extent to which supply chain disruption following Nexperia chip shortages and broader concerns around China rare earth exports are painted in a hawkish light, as well as how much weight Lagarde puts on Friday’s strong flash PMIs.

- This meeting is likely seen as a stepping stone to December’s updated economic projections, which will include new forecasts for 2028. Any hints here will likely shape market reaction although we see Lagarde opting for a broadly neutral tone to maintain optionality.

- OIS prices just 1.5bp of cuts to year-end, suggesting a neutral tone won’t have much impact, building to only about half a 25bp rate cut out in Sep 2026.

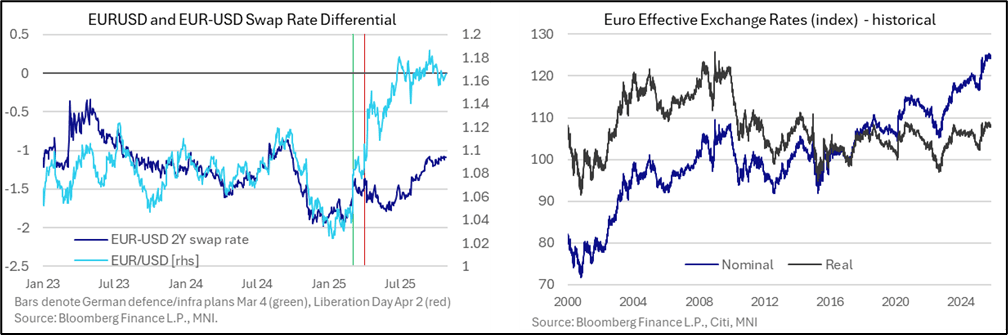

- The Euro could be more sensitive to any dovish surprises with a nominal effective exchange rate close to historical highs although there are clearly broader factors here beyond just a rate differential story.

- Note there are some notable data releases due on the morning of the ECB decision which could alter expectations for Lagarde’s tone, including Q3 national accounts, September unemployment and Germany/ Spain HICP. Eurozone-wide HICP inflation for September follows the day after the decision.

A still elevated exchange rate ahead of the meeting: