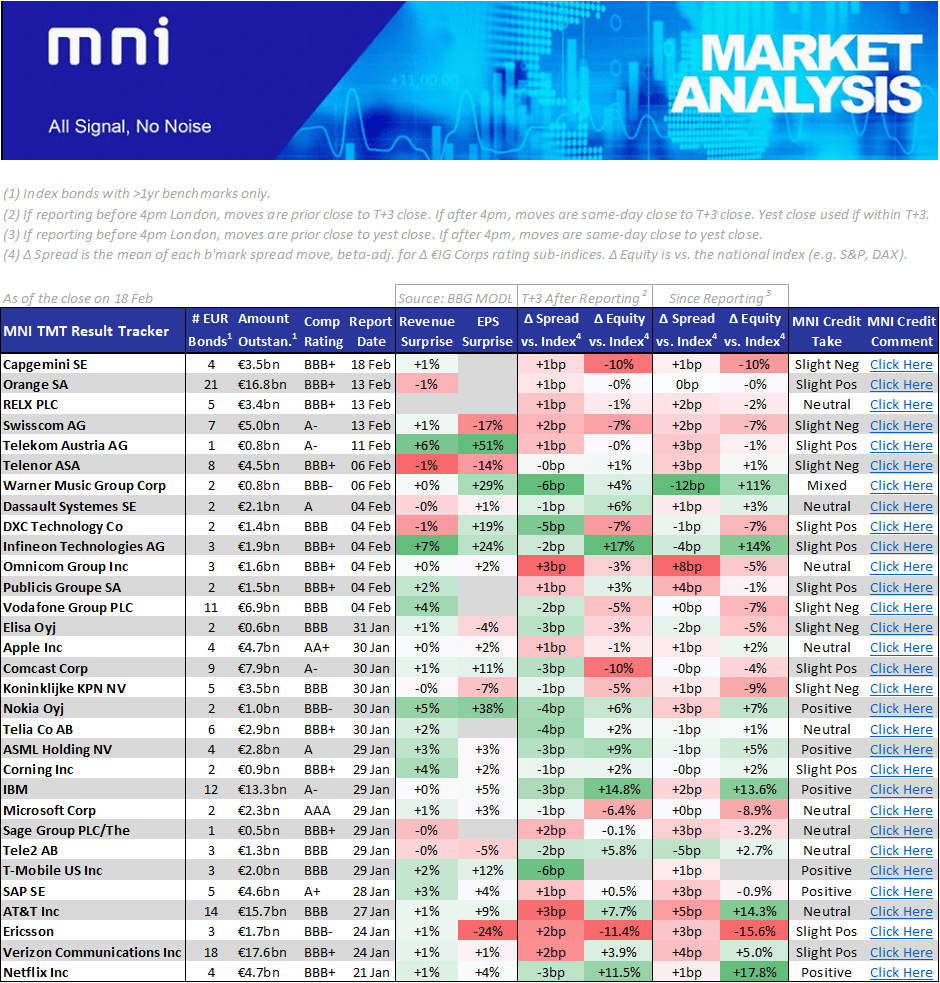

EU TECHNOLOGY: MNI Earnings Tracker: TMT

MNI TMT Result Tracker (19 Feb) 164309.pdf

- We have made some changes to our tracker; each bond is now beta-adjusted for the change in the relevant €IG Corps rating sub-index where before we just adjusted using the broader €IG Corps index (i.e. spread moves for a BBB+ name like Infineon or a BBB- name like Nokia are now adjusted for changes in BBG’s Triple-B Corps Index). Moves as of yest close.

- This has had a negligible impact so far given the level of prevailing compression between rating buckets but will paint a more accurate picture during less stable market conditions.

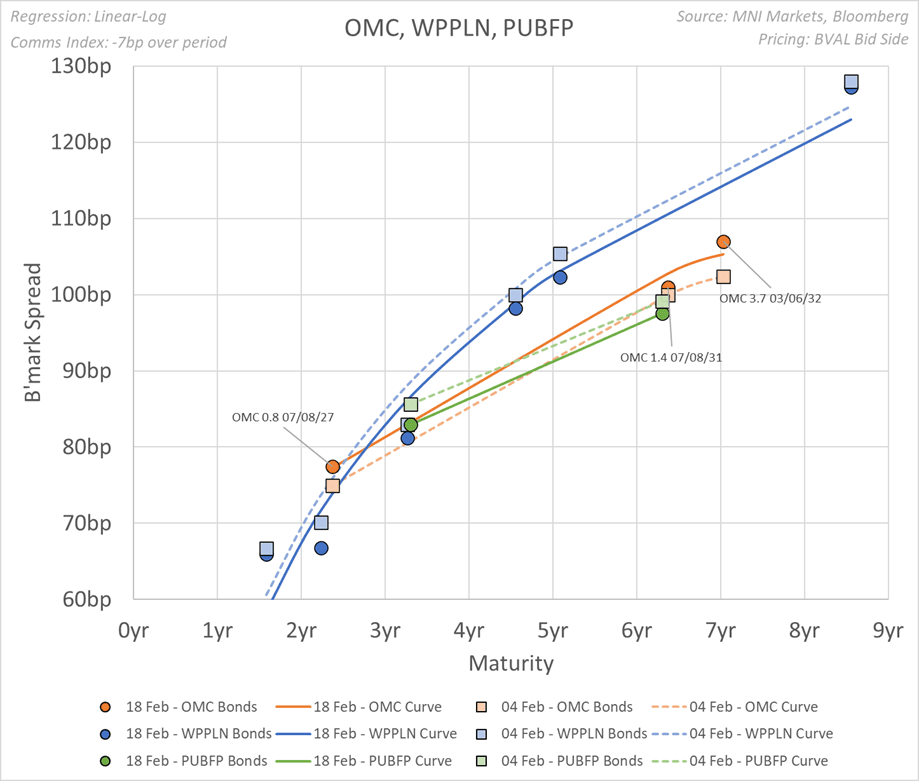

- Omnicom now stand out as the worst performing name with the long end widening by 3bp since reporting despite the triple-B corps index tightening by 8bp. We saw earnings as broadly neutral though note that IPG reported soft results on 12 Feb.

Also flagging a sources piece from a publication called Ad Age on Friday night that the FTC has opened an initial antitrust probe into the OMC-IPG deal; https://adage.com/article/agency-news/ftcs-antitrust-review-omnicom-ipg-deal/2602591.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CANADA DATA: Capex Plans Firm Despite Uncertainty But Excess Capacity Remains

In addition to inflation expectation components noted earlier, the BoC’s Business Outlook Survey pointed to some sequential improvement in demand expectations although excess capacity remains and the BOS indicator is still below average. The pick-up in capex intentions is notable to us considering “prevalent” uncertainty around the incoming Trump administration’s policies but it was in part catch-up of postponed plans.

- “Overall business sentiment remains subdued, but firms are beginning to anticipate improvements in sales activity. Meanwhile, businesses expect growth in costs to continue to ease and growth in selling prices to stabilize.”

- “After a period of weak demand, firms expect their sales growth to improve over the coming year. This expectation is largely driven by recent interest rate reductions and the anticipation of further cuts ahead.”

- “With lower financing costs and improving demand outlooks, intentions to increase investment have become more widespread among firms. Part of this is a resumption of previous plans that were postponed.”

- That’s despite “Uncertainty about the effects of the new US administration is prevalent, with firms commonly anticipating higher input costs due to trade tensions” but the fact that this is partly catch-up takes some of its gloss off.

- “Most businesses reported having some spare capacity. Because of this, hiring plans remain modest. Binding labour shortages are not widespread, and most firms describe the availability of outside labour as improved compared with one year ago.”

- With signs of improvement in this report at least partly conditional on further rate cuts ahead, Desjardins, for example, continue to see a case for their baseline of rates going to 2.00% in early 2026.

OPTIONS: Tuesday NY Cut Should Take Focus Given Trump Heads, Return of US

With the US returning in earnest tomorrow for the first full day of the second Trump Presidency, and the sharp USD swings today, we'd expect focus on Tuesday's expiry schedule to pick up into 10am NY time.

Decent optionality building around the $1.04 handle and above in EUR/USD, while a sizeable strike in USD/JPY at Y156 could limit losses:

- EUR/USD: $1.0300(E2.0bln), $1.0325(E3.3bln), $1.0400(E2.2bln), $1.0415-20(E1.3bln), $1.0450(E921mln), $1.0490-00(E1.4bln)

- USD/JPY: Y153.00($1.5bln), Y156.00-05($2.2bln)

- AUD/USD: $0.6200(A$775mln), $0.6245-50(A$939mln)

- USD/CAD: C$1.4285($703mln)

ECB: /SWAPS: ECB Survey Highlights Deteriorating Market Liquidity In Autumn 2024

The ECB’s December 2024 SESFOD survey (Survey on credit terms and conditions in euro-denominated securities financing and OTC derivatives markets) reports a tightening in credit terms and conditions between September and November 2024 “as general market liquidity deteriorated”.

- “A small net percentage of survey respondents expected overall terms to tighten further across all counterparty types in the three months ahead (i.e. in the period from December 2024 to February 2025)”.

- “A significant net percentage of survey respondents reported that financing rates/spreads had increased for funding secured against all collateral types”.

- “Survey respondents also reported increased demand for funding across all collateral types. Moreover, they reported a slight deterioration in the liquidity and functioning of collateral markets”.

- A reminder that German paper saw a notable cheapening against swaps through the Autumn, with the Bund ASW (vs 3-month Euribor) tightening from over 25bps at the end of September to below 0bps by mid-November (an all-time/cycle low).

- Despite retracing a portion of those moves in the second half of November, long-end spreads have re-approached those record levels this month. Analysts have highlighted increased free-float from ECB balance sheet run-off and heavy sovereign supply as fundamental drivers of swap spread narrowing in 2025.

- Press release: https://www.ecb.europa.eu/press/pr/date/2025/html/ecb.pr250120~9384966317.en.html